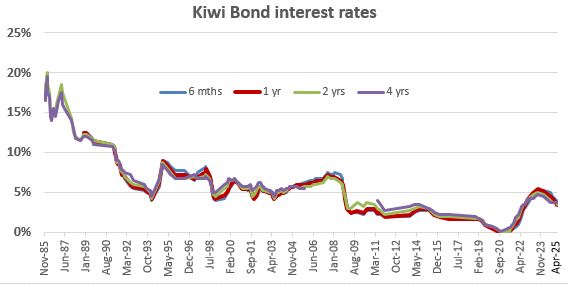

Kiwi Bonds set a practical 'risk-free' benchmark for term deposit savers to refer to.

The Depositor Compensation Scheme (DCS) is getting closer to launch on July 1, and that Government scheme will effectively guarantee all bank account deposits to $100,000 (including term deposits TDs).

As the covered institution will be paying a fee for the coverage, this is a cost that will likely be passed on to savers through lower offer rates.

The net effect could be to drive term deposit rates down to Kiwi Bond levels.

Kiwi Bond rates have varied a lot over the years. Since the GFC, they have been unusually low, although because they have been low for a long time (more than 12 years), these have become 'normalised'. During the pandemic they fell to virtually nothing.

Even the recent rises haven't yet raised these rates to pre-Global Financial Crisis (GFC) levels.

Pre-GFC, when enthusiasm for residential real estate investment seemed unconstrained (and term deposit saving was out of favour), risk premiums were low, even if term deposit rates were above 7%.

But the GFC shook savers' confidence in private financial institutions (remember the finance company carnage?), and those risk premiums rose sharply.

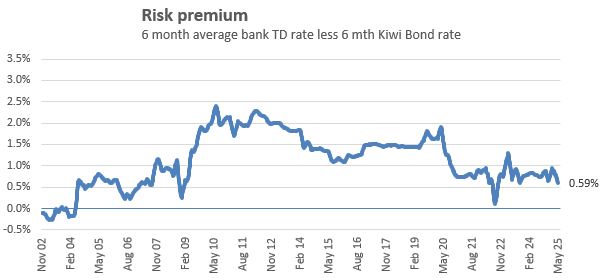

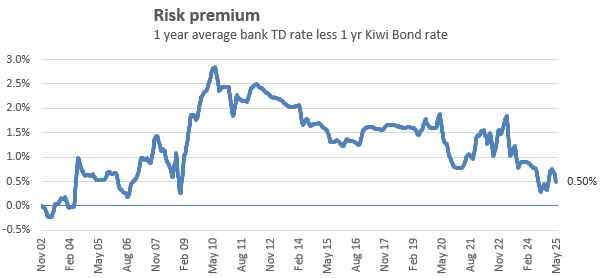

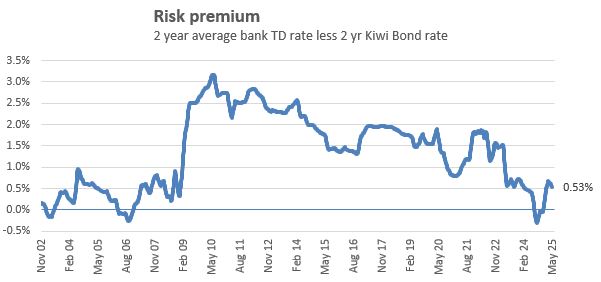

The above three charts track the average risk premium over bank rates.

But since the pandemic, they have fallen away, now to about only +½%, even as recent TD offer rates rose. (They jump around a bit due to the timing of the Kiwi Bond rate changes.)

The DCS could be another event that either lowers them further, or even has them vanish - because term deposits actually become risk-free to the $100,000 level.

Worth watching will be offer rates from non-bank financial institutions (NBFIs) that are also covered by the DCS. Those NBFIs are probably expecting to benefit from stronger inflows of deposit demand as savers spread their DCS coverage around to compound the $100,000 safety net. But if that does happen, those NBFIs will be challenged finding safe sustainable loan demand. Along with the DCS fees they will have to pay, this will limit what they can offer, effectively squashing the risk premium they have traditionally offered.

Better risk premiums (and higher return offers) will then come from NBFIs that are not covered by the DCS. Without considering risk, they will look good on the face of it at the advertised levels. Buyer beware.

Kiwi Bond interest rates were last changed on February 27, a fourth straight reduction. We have no idea when the next review will happen, or what that future change will be. But we would not be surprised if it is yet another cut.

5 Comments

Kiwibonds would be a lot more popular if we didn't have to buy them through Computershare.

With RealMe, there's no reason why they can't be sold directly to the public.

Agree. Computershare is a dreadful organization and service. How they can even be relevant in 2025 is beyond me. How can they be the official registrar, issuing agent, and administrator for Kiwi Bonds? Link Market Services is also a clown show in my opinion. The Japanese (MUFG) have taken over Link Market Services and I would suspect they could handle things better.

Nobody is factoring-in real risk.

Nobody.

Even Schiff, with his 'Fish Reserve Notes' failed to ask whether fish-stocks were being depleted (although he got the rest reasonably right).

that's the real problem with the banks isn't it? Bond interest rates are the 'Zero Risk' rate as stated in the first line, but banks are not zero risk. From some perspectives it can be argued they are far from being zero risk, hence the need for the OBR and the DCS, but they don't offer anything close to a reasonable interest rate to compensate for that. At the same time they have lobbied Governments to effectively gain control of most if not all societal (legitimate) money flows. These are PRIVATE business's who have gained the position to dictate to the country on economic activity. That this was allowed in the first place and is continued to be tolerated is utterly unacceptable in my view.

and the problem is bigger than this. Governments have abrogated their responsibilities and ceded responsibility in part to the private banks for money creation, allowing them to direct money flows into the economy in ways that they directly profit from. A contributor to some streams (Colin Maxwell), has commented that governments who retain control of money creation have significantly better performing economies than those who surrendered the ability. There's the clue about what should be done.

Gotta say the pay to comment feature isn’t working well thus far. Comment sections are now often locked when articles are published. E.g. today's Morning Briefing, yesterday's RBNZ article, etc...

Whether it’s a bug or a policy change, it’s making the experience of paying to comment far less appealing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.