Despite affordability pressures, credit bureau Centrix says more people are taking on larger mortgages to get on the property ladder.

In Centrix's latest monthly credit indicator report, chief operating officer Monika Lacey says mortgage lending remains in “positive territory” but buyer confidence has started to slow down due to higher borrowing costs.

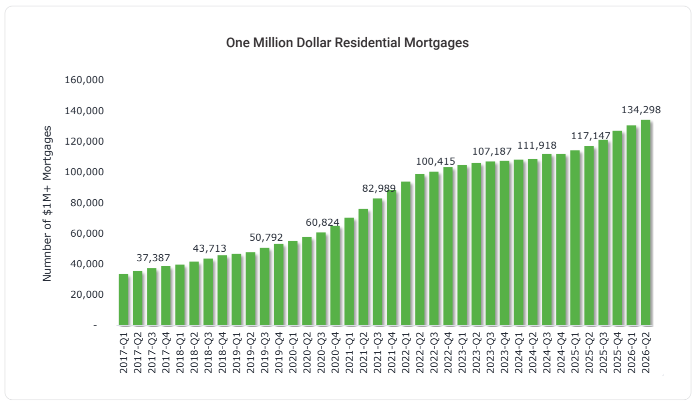

Centrix's data shows that in April, the number of borrowers with mortgages exceeding $1 million rose 15% year-on-year. More than 134,000 homeowners are now in this category following a plateau during the softer property market environment during 2023 and 2024.

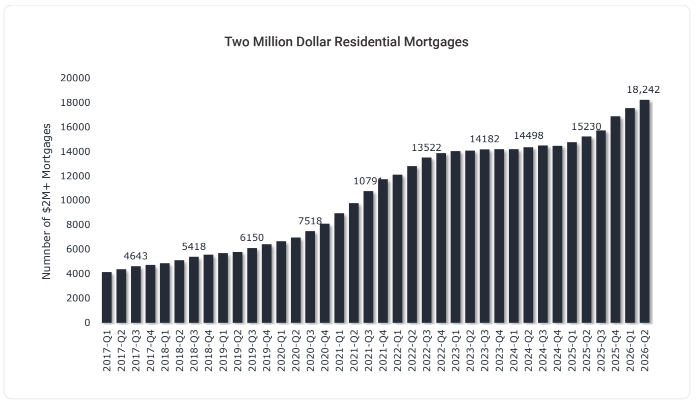

Higher-value lending is climbing as well, with over 18,000 borrowers now holding mortgages above $2 million, a figure that has “grown rapidly” over the past 12-18 months, Centrix says.

There are also signs of “renewed momentum” among first-home buyers, who now make up 25% of new mortgages due to easing lending rules and lower rates.

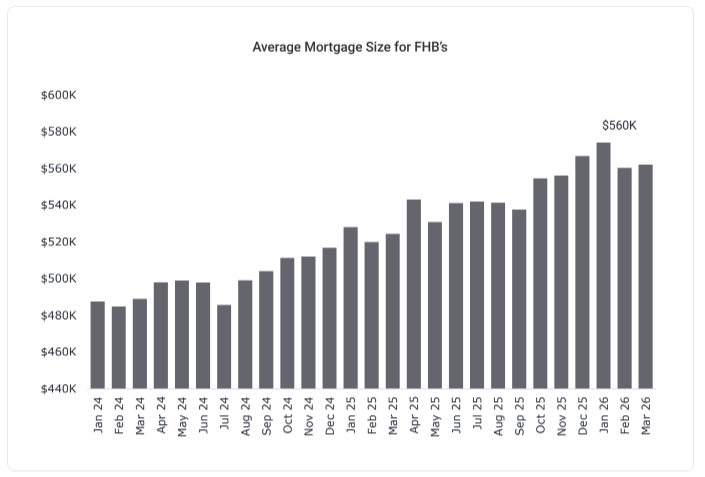

According to Lacey, overall loan sizes are increasing as borrowers take on larger mortgages to get on the property ladder.

“Affordability pressures persist, with average loan sizes rising to $560,000 in early 2026. The typical buyer is now 37, and while that trend has stabilised, those entering the market tend to have relatively strong credit profiles,” Centrix's report says.

The latest home loan figures from the Reserve Bank (RBNZ) found that more than a third of homes sold in April were likely bought by first-home buyers. Banks approved 2,858 mortgages to first-home buyers in April, accounting for 37% of all mortgages approved for the purchase of a residential property.

Residential mortgage arrears improving

According to Centrix, residential mortgage arrears continued to improve in April, falling to 1.29% from 1.39% in the previous month, with 21,100 accounts past due on payments. The credit bureau says this marks a 13% year-on-year improvement and reflects the impact of lower interest rates on easing repayment pressures and stabilising household finances after a period of strain.

Financial hardship cases have declined 9.3% year-on-year, with 13,450 accounts currently reported in hardship. While this is up slightly by 50 accounts month-on-month, April’s hardship figures are reversing the upward trend seen since late 2022, Centrix says.

Among the financial hardship cases, 36% relate to mortgage payments, 35% to credit card debt, and 34% to personal loans.

According to Lacey, credit conditions at the consumer level are showing some signs of stabilisation, with consumer credit demand down 1.9% year-on-year in a softer economic environment. Fewer borrowers are falling behind on repayments, and arrears rates are continuing to decline.

Centrix says 11.25% of consumers were behind on payments in April, down from 11.72% a month earlier. The total number of people in arrears has dropped to 443,000 and is now 9.5% lower year-on-year, supported by improving economic conditions and lower rates. Despite this, 96,000 borrowers remain over 90 days overdue, with renter households “disproportionately affected”.

Centrix found personal loan arrears improved to 9.2% in April, down 8% year-on-year, indicating a gradual easing in repayment pressure. Buy now pay later (BNPL) arrears also declined to 8.3%, down 5% year-on-year, while retail energy arrears edged down to 4.2%, broadly in line with last year. Telco arrears showed the most significant improvement, falling to 8.3% from 11.1% a year ago.

Centrix’s data comes from 97 registered banks, finance companies, utility companies, telcos, and other business contributors to comprehensive credit reporting (CCR), providing payment behaviour data. Major bank contributors include ANZ, ASB, BNZ, Westpac, Kiwibank, TSB Bank and The Co-Operative Bank.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.