By Elizabeth Kerr

I love getting questions from readers about lifestyle design and the money machine so this week I’m going to share one with you all.

"Hi Elizabeth,

Our goal is to have a money machine which will deliver us from the shackles of working until a ripe old age.

We’re mid 30s and about to have our first baby in August forcing us down to one income.

We don’t know whether we should sell our Auckland investment property now and live mortgage free,

Or would we kick ourselves 10-15 years down the track when the house value may have doubled?

What would you do if you were us?

Sincerely Tom and Jessica."

Their budget as follows:

| monthly | Income | Expenses |

| Lifestyle design | $ | $ |

| Tom's net income | 5,600 | |

| Jessica's net income | 4,100 | |

| Car - insurance/rego/repairs/service | 150 | |

| Rates | 250 | |

| House - insurance/contents/odd bills/gardens | 250 | |

| Power/gas/phone/internet | 450 | |

| Union fees | 55 | |

| Insurance - medical/life/trauma/income protection | 250 | |

| Spending | 800 | |

| Food | 800 | |

| Petrol | 100 | |

| Mobile phone | 45 | |

| Home mortgage (Tauranga) | 3,900 | |

| Personal loan | 45 | |

| Baby fund (for when a single income) | 1,000 | |

| Emergency fund | - | |

| KiwiSaver (Tom) | 100 | |

| Savings account - furniture/holidays | 200 | |

| Xmas fund | 85 | |

| Top up for Auckland renter | 1,200 | |

| --------- | ---------- | |

| Total lifestyle | $9,700 | $9,700 |

| Rental property - Auckland | ||

| Rent | 1,900 | |

| Mortgage - interest only | 2,300 | |

| Rates | 250 | |

| Expenses - savings/vacancy | 480 | |

| House insurance | 90 | |

| Total rental property | $1,900 | $3,120 |

Dear Tom and Jessica,

First things first ... a bit of butt covering. Please remember I’m not an authorised financial advisor therefore I urge you to seek professional advice for any changes that you might make as a result of this communication.

This message does not represent the views of interest.co.nz or their team; and I might change my mind about what I’ve written at any time with or without telling you.

I’m not allowed to be giving advice therefore best to think of this as a written version of my internal thoughts and nothing more. What you do with it is entirely up to you.

Now where was I ? ah yes ...

On first reading your email it seems you are asking a real estate question as opposed to a money machine question but hopefully I have answered both for you below.

You need something you can set and forget when it comes to your finances for the near term (2 -3 years); something that you can just trust in, and then focus on getting on with your everyday lives as new parents and future funders (okay future funders’ sounds really dorky but just go with me ...).

Let’s start ... Man you have loads of money coming in but your budget is haemorrhaging. Go and divvy it up into non-negotiables and everything else buckets right this instant!

The Auckland property makes a monthly loss of $1,220 which you have to top up from your personal income which is not ideal at this stage in your lives – can you increase the rent at all or reduce the expenses in this space? If not that is okay for now, no need to panic.

You have no emergency fund.

Yes you have credit cards and yes you can draw down from your overpaid mortgage (maybe – not all banks allow this without having to re-apply) but both of these options have to be paid back.

If your emergency involves a loss of income then you’re screwed.

I suggest you take some time out from overpaying your mortgage to build into this fund if you need to. Might as well get it over with while you are both earning.

You need enough money in your emergency fund to cover all living expenses and mortgage repayments for at least three months plus three months top-up for your rental.

Murphy’s law dictates that once you have this emergency money you will probably never need to use it and it will just be another asset in your money machine arsenal.

But not having this money is like playing with matches as a gas station. Should Tom drop dead Jessica will need this money to look after the bills and babies until your insurance is paid out.

Right, the goal for you right now should be to fund your entire family lifestyle on your luxurious income starting right now! Iron out any kinks in your communication around spending now so that when bubba comes along you are both humming to the same tune.

You do not need $200 per week for food. Food is just to stop you BBQ’ing any low flying native birds. $100 is more than enough for two but seeing as you are used to spending much more I’m going easy on you here. You should aim for $120-$150.

Please cut down your ‘spending’ account by at least 70%. If you need to spend that much each month then either your budget is broken somewhere or you are buying stuff you really don’t need.

$1,020 for xmas presents each year is excessive by my measure. Do you have 34 family members you have to buy for? Halve it!!

I see you have $7,244 saved for bubba already. Babies don’t cost that much and contrary to everything you are told you hardly need anything at all.

As long as they have a safe place to sleep everything else is a bonus.

Don’t be suckered into designer prams, designer cloth nappies kits (they don’t always work), change tables, nappy bags or baby baths. Also, don’t start thinking that just because you are having more kids that you need to buy the best. The big heavy expensive pram that needs a degree to use and an SUV to cart around will be cast aside as soon as bubba can sit in a light and cheap umbrella stroller.

I know they trick you into thinking you can convert the pram for two children, and that you will be jogging around the block with your celebrity pre-baby body by 6 weeks but none of that is useful.

You can have a very generous $1,000 for buying baby stuff to set up your home and see you through the rest of your pregnancy. And just in case keep an additional $500 aside for any extra support you might need such as breastfeeding support or physio in the weeks following. Don’t feel hard done by – many people do it all on much less with no lasting effects on their children.

This leftover $5,744 is deposited into a new income called Future Funding. All of Jessica’s money between now and when the baby is born is deposited into this account.

This money is then used to meet the shortfall on for the Auckland property for the time that Jessica is not working. By the time she finishes work you will have $32,800 (plus $5,744) plus any maternity leave pay which takes care of your emergency fund as well.

Booyah – you can afford to keep the Auckland property!!!

Now in answer to your question about kicking yourself later if you sell the house now, history shows that in 10-15 you most probably will – but that is not the game for you right now.

Right now you need to ask yourself ... do you think the house will increase by more than $14,640 in value each year that you are topping it up? If the answer is 'yes' then I'd keep it. If it’s a 'no' then you’re essentially pissing money down the drain for now so I’d sell it and invest the top-up money elsewhere.

As much as I harp on about preparing a money machine I understand there are seasons in life, so rather than you trying to live on one income, keep up with your investment mortgage and siphon off enough for a money machine at the same time; just stick to the first two goals for now.

When Jessica returns back to work continue in the same vein of living off your income alone and all that new income from her can be deposited into your Future Funding account to be used as money machine arsenal and to knock over your home mortgage and student loans. After 3 -4 years of this I think you would be very impressed with how far you’ve progressed.

Ten years after that and I'd be thinking about how you want to spend all that free time you both could have.

There is an immense freedom to being able to live off one income.

As a team you are well on track to achieve an early retirement via a well designed lifestyle.

Warm regards,

Elizabeth Kerr

64 Comments

I know your are not an investment advisor but I can't believe you didn't include any discussion on the risk involved in keeping their "investment" property. I put investment in quotes because with such negative cashflow it is speculating, not investing. They have an interest only mortgage on it, which tends to imply they are highly leveraged. Consider the following scenario - which I am not predicting, but is certainly one possibility of many possible futures (that's what risk means). Interest rates rise, increasing the payments. However, because there are so many speculators like themselves who can no longer afford the negative cashflow they will all run for the exit at the same time, decreasing house prices. Now their mortagage is worth more than the house is and they can't afford to sell, and they can't afford the now higher monthly payments. Risk! They should sell the Auckland rental and invest the monthly amount (plus any principle they get back, which I would assume there is at least some), in something that has a lower possibility for bankrupsy. They could learn about other options for investing beyond term deposits and property - something kiwis seems stunningly uninformed about.

In NZ the advice on investing is very poor. Diversification and asset allocation is poorly understood. Property is just one of the areas you should be invested in. Putting all your eggs in the property basket is a long-term recipe for disaster.

When will interest.co.nz provide a decent series on how to invest *outside* of property? What little advice there is in NZ is normally setup to benefit the providers not the investors.

KiwiMM... absolutely agree with you on all fronts. People should scramble there eggs around a bit.

The problem i think is after the middle squeeze have spent all their money on their lifestyle there isn't much left over for investing and it's easy to just get another mortgage for leveraging into property. Then they stop after this step and go back to upgrading cars and overseas holidays. I think if people stopped spending so much then they would have the ability to explore other investment options besides property.

All good and fine. But until they reduce their own home mortgage, a rental is going to be expensive cost...as all money going into the rental could reduce their own interest bill.

If their own mortgage is the result of an attempt to get the deposit for the rental then they have had very poor financial advice. It is better to take on 100+% loan for the investment than redraw on a personal usage item, as the the 100+% loan's interest cost is deductable against future profits, whereas it takes a good paper trail and very tricksy to get IRD to accept the interest on the personal mortgage.

The spending so much is entirely un-linked to property or style of investment.

The property investment is linked to yield in Auckland (absolute terms, not %), the value of future security value due to prices rising in that area, and most of all, the leverage available to increase yield %. These factors make for a solid investment platform.

For the same money, given their income, The Auckland market is probably still a little out of their price range, unless they're expecting a windfall to remove that negative gearing. Being interest only, negative geared is a very dubious position. Perhaps playing "Rich Dad's electronic boardgame" doodad and buying the apartent block too early will demonstrate the problem.

In a normal world thats reasonable advice. However, currently valuations are stretched everywhere. Cash is yielding higher then stocks now, a 10% "correction" (now there is a good example of newspeak) in stocks can wipe out years in dividends, if you are even getting them. If you are financially smart you may find a good stock somewhere, but most people are not, case in point, buying a rental that costs you money every month.

If done in the right way property can be a great lifetime investment, not a recipe for disaster. The trouble is that someone buys a renter that costs them money every month, thinks they have an asset when in actual fact they have a liability, and thinks this means they are an investor.

I make money through my business, and store it in property, all putting money in my pocket. I would never buy a rental that cost me money. I could care less how much the property market drops, because the rent covers my mortgage and puts a bit of money in my pocket. it's not easy to find that kind of property, but they do exist. The highest ROI on the monopoly board is from the cheap streets. People love the bling though.

Putting all your money in stocks is a recipe for disaster, bonds are not much better. Owning your own business is ok, if you have the motivation and skills, but it can be a lot of work. A cashflow positive rental that can pay off the mortgage in 30 years, I just don't see the risk?

"A cashflow positive rental that can pay off the mortgage in 30 years" is indeed low risk (biggest risks would be a big spike in interest rates that turn it cashflow negative or damage that is not insured (not sure what that would be)) but that is certainly not what this couple have . They have a severly cashflow negative property that they pay interest-only mortgage payments on in a housing market that is overvalued by a large number of metrics. In any normal market your low risk rental property would also be relatively low return (relative to riskier investments). How people can think that property can be both low risk and high return over long run shows a severe lack of understanding of market forces.

Definatly an interest rate spike would be an issue, however my assumption is that interest rates will generally stay in line with economic growth et al. so high interest rates, good growth, rent increase will be ok. Or something along those lines. It's kinda like the two guys getting chased by the bear and one says to the other, I don't have to outrun the bear... I just have to outrun you.

An interest spike is a bad thing for a marginally cashflow positive situation.

But for people paying into an interest only situation it would be catastropic.

Excellent comment about risk Avatar. And good thinking all the way thrugh Elizabeth.

Seems to me this couple are mad keen to get ahead. But there are no good options. No prediction but the property is in bubble territory. New Zealanders wisely are wary of the financial services sector. The bad experience there is not just a PR problem, it's real.

So what is it they can do ??

It's hard (though not impossible) to save your way to prosperity.... but some investment needs to take place. I think they have behaved responsibly with what they do know today.... and could withstand the impact if the worst would happen tomorrow.

Im tinkering with a column on what id do from inside the bubble (if there is one)..... watch this space.....

I stand by my non-advice. The financial sky is not falling therefore I put “risk” in quotes. I did take into account the LVR's across both properties combined with the fact that Jessica can return back to work without too much fuss, and they could reduce the negative gearing if the aforementioned was to happen was also factored in. Additionally with a bit of tinkering around their personal income they can easily withstand some market carnage. I don’t think that speculating is always a bad thing - it’s not like their investment house is in Eketahuna.

Risk does not get mitigated by the sky not falling in. Risk is ever present and the likelihood of an adverse event is increased the longer the good times continue. Nobody consistently predicts when recessions or crashes will occur so the best course of action is to set yourself up to weather the storms when (not if) they come.

I can't believe you put risk in quotes. I don't think the sky is falling - actually I own my own home in Auckland. But you must admit there is at least a 5% chance of the path I outlined. Personally I will be very surprised if in 10-15 years my house is worth more in real terms than it is now, so it doesn't form much part of my own "money machine" plan. Speculating IS a bad thing when it is your ONLY plan. If you speculate with 5-10% of your money, no problem at all. Currently they have no diversity and lots of risk - like all such plans it could go very well or it could go very wrong.

Elizabeth, you can't negative gear your own (consumer) house because the interest isn't deductible.

According to the given data, how can they remove the negative gearing on the rental ($1200/month)? The only way to do that is reduce the rental house loan (where is the windfall coming from??) or slash rental costs (no insurance??) OR to increase the rental income? If the later is an option they should be doing that already rather than dump their own money in.

Exactly! I don't disagree with you. That is one of the areas they are now exploring.

Sell the Auckland property, buy a lower priced property which will get u positive cash flow....Tauranga/Wellington. Any leftover cash can be used to reduce your personal mortage or put it into a good dividend stock, should you ever need the money asap, just sell the shares.

That is not a bad option either...... it then comes down to what i wrote in last weeks column.... do they play the capital gains game or positive cashflow game. I see if they stay in auckland in the very near future they could achieve both.

They don't have a positive cashflow game. That's the problem. IMO They'd be better to sell the rental, pay off the house, then look to buy a rental - the level of negative gearing they have at the moment isn't profitable (ie they're not reducing principle and they are still paying home interest).

This would be my suggestion too, if you wish to keep a foothold in the property market.

Look outside Auckland for lower leverage, possibly split the equity and buy 2 lower priced properties so selling 1 can halve your commitment quickly. Setup your loan with part fixed %, part floating revolving credit facility to allow excess income to reduce interest but remain available as cash if required without penalty.

Otherwise, give it a break for 12-18 months, sell and save, use the leave to look for a bargain, maybe a do up if you are handy, repurchase with a plan and more equity when the income returns to full steam.

Hammer that budget, stay home for a while, enjoy the simple things, dont buy frills for the baby.

100 dollars a week food, for 2 people? Show us that shopping list!

yes, I would like to see it as well. I budget and spend that for each family member and Im told I am tight with money on food. Cutting my food budget in half would be a dream event, LOL it is my single biggest consistant spend.

The Hamilton budget advisory centre has a menu and cook book for $100 per week which feeds 4 hungry people 3 meals plus snacks and desserts everyday for a week. It is mainly comprised of whole foods ie fruit, vege, meat, oats and eggs. You can call them direct for a copy To be posted to you. Last I spoke to them it was not online. It can be done with a little planning and commitment.

test it for 6 months (dont forget to include travel costs)

Was that comment meant to fit in here? Do you mean the travel costs to collect the food?

when it comes to food I don't the it matters whether you like it all the time or not... You eat it to stop being hungry and to give your body nutrients. If food is part of how one derives pleasure from life then they might forgo something else in favour of spending more here.

People who have tried those recipe books often find that they are less effective than advertised. Many of the meals aren't filling and some are beyond the skills of many people.

Supermarkets deliberately as a marketing strategy drop prices on one section of their product, to get the prices in those books often means tripping around several places to find find which store has the bargins.

As for liking it or not,,, that might work for the financially driven but many peoples' partners and children will have issue with such tactics.

There can be some excellent tips though, how to use cheaper cuts more effectively. how to preserve multiple portions of cheap vege and specials for use in future dishes.

Fortunately we're not seeing the promotion of home gardening, which seldom works and is immensely time consuming.

I rarely endorse something I haven't personally tried. It is a great resource ! If partner and kids can do better within the same parameters then go for it. Food slips into the coupon cutting housewife category for me so I tend not to focus on it in my writing too much. If the minimum effective dose can be purchased for less than what you are currently spending then why wouldn't ya?

Poached pigeon? Sautéed sparrow?

The Q is what about the potential for substantial loss?

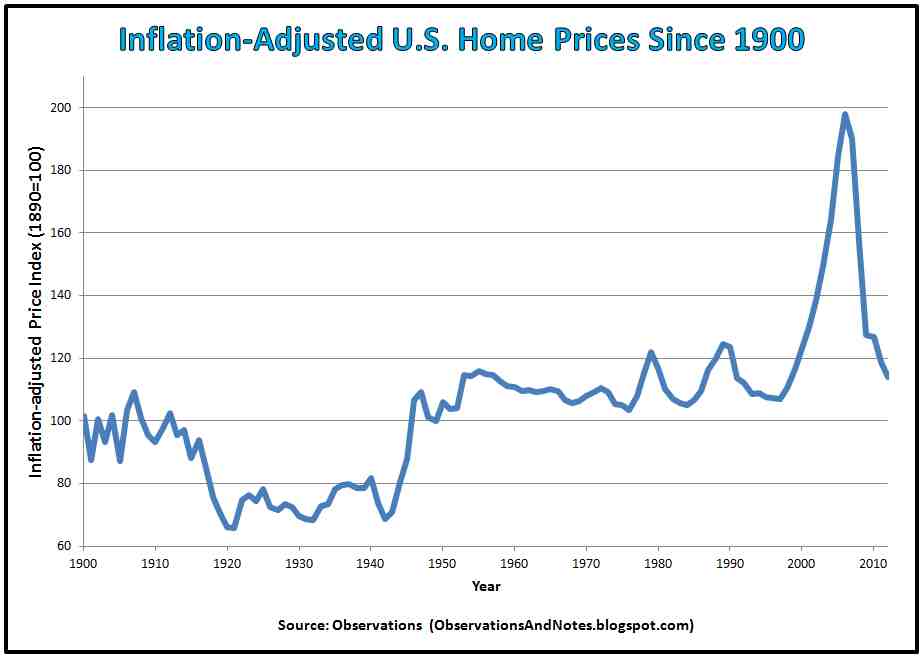

They are in their 30s. As BH and others have pointed out demographics alone are against further long term housing capital gains for the next 30 years IMHO. Let alone all the other nasties, huge global debt, peak just about everything.

My view is we'll see some substantial drops in the next decade as post peak oil effects makes our global economy shrink substantially. indeed by 2050 in effect oil is gone, used up.

What will the world look like in a no oil world? 15~35years from now?

let alone all the other mess.

In a deflationary environment debt remains and is harder to service if not impossible. So I personally see a 50~75% drop in house prices but the couple will be stuck paying teh original borrowing off.

I see lac has suggested shares, again the P/E ratio looks insane on many stocks even before all the negative issues above are considered. It also takes weeks to sell shares and in a 1929 like event just who will be buying? Then consider all the micro fast trading that takes place and a mom and pop investor are just canon fodder if trying to play the same game.

Good luck with the gamble is all I can say.

It's been a long time since I replied to a comment here...

Just looking for some clarification on your views Steven (not disagreeing). Are you expecting these 50-75% price drops in housing across all of NZ, or predominantly Auckland? And when do you envisage they will occur or start to occur?

I think a correction is due in the next 1-4 years personally, I don't imagine it will be 50-75% though (I'm basing this purely on the fact of NZ's legislated minimum wage and it's comparison to average earnings etc; coupled with our inwards immigration figures).

Some Q.

Basically I follow the Steve Keen and Nicole Foss view on houses and incomes until someone shows me some better model/outlook.

So all of NZ and indeed globally (though Nicole Foss say 90% losses, I assume in real terms). Not Auckland on its own, I cant see why there would be such a big drop in just Auckland without there being a big event externally doing everyone over.

a) Housing today generally is x2 wages so when you correct for that alone its a 50% loss in BAU always growing scenario.

b) the post peak oil view, ie BAU finished with.

Take a look at house prices pre-fossil fuel age the prices inflated very little, "suffered" a huge bump in prices during and we are going back to pre-fossil fuel age. So I cant see how houses can stay priced as they are.

(cant find the graph right now)

c) Finance ponzi scheme. Could be this financial mess, 1929 triggered the last one.

Historically (pre 1800) houses didnt inflate much in price. Indeed generally there was not much inflation pre 1800, or rather it was balanced it seems by periods of deflation when things got out of wack,

https://medium.com/@zavidovych/what-we-can-learn-by-looking-at-prices-a…

and 1900+

http://earlywarn.blogspot.co.nz/2010/04/five-centuries-of-inflation.html

or what happened in the last Great Depression to house prices,

http://4.bp.blogspot.com/-kjOHoEKbH7A/ULQgiAZ45RI/AAAAAAAABh4/8U-RJx1-p…

{kind=link}

(in fact the entire thing is well worth reading),

http://observationsandnotes.blogspot.co.nz/2011/07/housing-prices-infla…

When?

Multi-billion dollar Q that one.

Like putting your fingers in a buzz saw and wondering which tooth took your index finger off. Its messy and it hurts but does it matter?

Within the next 1 to 4 years is probably a very good time frame, I cant see it being 10+ as that is long past peak oil by the look of it now.

Parts of the USA lost 35%? and I dont think that was the main event, that is before us I think, ergo Im leaning to a very big drop in prices.

Steve Keen's comments/ work with Minsky make me think it wont be a small event.

Cant happen of course, this time is different. We are all going to be rich and live happily ever after.

So I sit back with these views from others v the ponzi players outlook and I just wait to see who is correct.

Thanks for that - some very interesting information.

There have been some changes in economies from the 1200-1500 time period though - with services being added, whereas in those medieval times it was predominantly a goods market driving inflation etc. The information should still largely hold true though in that the values should stay in line with inflation (even with the services market added to the various economies).

The pieces I'm not clear on (this isn't from your links or reply btw, but the link talking about debasing gold and silver currency made me think of it) - is how we adjust for things like the global economy. The rationale for my previous sentence is as follows: as most of us know and acknowledge - the vast majority of the world has been printing a lot of money in recent years, aka they have devalued their currencies by printing. In NZ, we have not been doing this to the best of my knowledge.

If the amount of printed money (or paper money) in circulation increases, I suspect the value of land/houses/productive assets should increase as the value of the currency has been decreased. However, given we haven't been printing in NZ... but the rest of the world has... how does this then affect prices in the NZ market?

Regardless, I think a correction is coming and is needed. The quantum and the timing is up in the air and I suspect the NZ market won't be the first one to drop severely.

The effect of peak oil is going to be interesting for most of us, I can see peak oil driving prices down, and driving prices up (as it will be less efficent to produce certain building materials etc)... I also wonder what contingencies the oil companies have up their sleeves... because they'll have known for years peak oil has been coming, and I doubt they'll be ready to fade away without a fight...

This is internet not personal financial advice.

Consider the "Baby Fund", "Xmas Fund", "Personal Loan","Savings Account" These are "dead money".

The personal loan has how many years to go? What is interest rate?

If it is under two years, redirect all 4 funds into paying it off immediately.

If it is over two years, look at rolling it into your mortgage (preferrable the rental mortgage if possible* where it will be deductible interest).

Look at paying down your own personal house mortgage asap. The interest you pay there isn't reclaimable, and chances are the "Funds" and "savings" you are dealing with give less interest that the low rate in the mortgage. If your mortgage is over 70k, look at taking a 70k floating and the rest on interest only fixed.

If you need a fund for Baby (and often babies don't really need much, or for living costs - well eat, pray for sleep, clean and feed baby also not an expensive lifestyle).

As for the Xmas Fund... if you're spending more than a weeks pay, which SHOULD be coming out of your personal spending allotment, then you're overspending. That level of spending is for people without Mortgages and Personal Loans (and who aren't saving for babies/college funds).

The other "non-impact" item you should consider, is that of the Top up for the renter. Since you are still paying off your own interest un-recoverable mortgage, the rental should be on the cheapest interest only rate you can. All principal payments from your own tax-paid funds should come off that own mortgage first.

What is this entry : "Expenses - savings/vacancy" ?

Personal spending listed is very high, considering much of the personal spending such as cellphone, internet, power,food, petrol, personal loans are already broken out into different areas. I'm not sure if there is a career portion to this (some people have high clothes or event attendance requirements) but it's high for people paying off debt (your home mortgage) and saving for an event (baby, rental). ok 2 events.

Babies. They grow -really- fast. Although at first to exhausted parents it doesn't seem like it. People will give you stuff - they want to give you stuff. It's part of the big tradition, and since they grow so fast most of it's top notch, and you just dump the crap anyway. And then you pass on the rest to others when their turn comes. Limit yourself to a couple of really special items and no more. You'll get way more joy from what your child is doing, than how they're attired etc.

Emergency funds...personally I'm against them. Dead money if you have debt. But take a real hard look at what kind of size fund you're talking about. Car accident? Dental? Minor medical? What is the real risk - what do you need for emergency level "get through it". Chances are, anything big would be a loan or mortgage extension...which means paying down own home mortgage would be best - put that equity where it can work, you can always call it down later - or at least make sure your bank is using an offsetting system, where positive balances in a savings account, is taken off your mortgage debt before daily interest is calculated.

Now the Auckland house.

You're paying your own mortgage and debts which are non-receoverable interest, so until those are reduced the rental mortgage needs to be minimised to interest only.

You've already done that, but concerned about the honey-pot "savings/expense" you've got there... So having said that:

You are currently paying the bank $1,200 a month for the privilege of letting someone else live there with their rent subsidised ! What generous people you are.

Is there any strategic reason you are holding on to that specific property?

If you focus all your efforts removing your own loan and mortgage interest burden, how many years is it before you can start reducing the principle on that rental principal? considering you're blowing $14,000 a year helping someone else live cheap.

If your own loans/mortgage have little to go then maybe the rental could be worthwhile and we can measure the merits of the investment and getting it to the point where it's going to pay for itself without sucking interest money off you. Property is a great investment...but a lousy hobby.

The property itself.

What is its future value looking like? If it's reached it's 10yr peak value, then even if you were holding on to it as a retirement rental, it might be worth putting it on the market given baby and your constant loss.

If it's a perfect do-up or the worst house in best street or some other niche earner for you, then it's future value might project enough gain....but at 14k a year cost possibly not.

Normally you'd look at the profit on disposal (how much cash you'd be left with after lawyers and commissions and mortgage break fees) vs the income via rental over 5 or 10 yr periods.... but you're not making rent, it's COSTING you rent. Which means just how much is it worth holding on to the place to you?

Unless this place would be hard to replace, or unless you were make a large loss on disposal, IN MY OPINION, you would be financially better off to sell and pay off your non-recoverable interest.... however !!!! If doing so would leave you with cash surplus, you then have to consider inevstment opportunities...which is another discussion, which *might* mean there's a small chance it's worth keeping. (but seriously with the debt-service interest only at 1200 outgoing, my instinct would be to doubt that and look into something with smaller purchase size value (eg shares, where 10k or 50k will give a solid an liquid blue chip investment, without massive payout to the bank for the privilege)

* as mentioned you should put as many expense on the rental mortage as possible and as little on yourselves, due to the home property not being recognised as an investment for tax purposes. This can't be done directly for legal and ethical reasons, but it does mean that you're better getting a loan for rental the house in a separate account if you need stuff for the rental, than it is to pay for yourselves. If you need to paint, get a extra pot, or cement, pay for it from the rental account, do the rental work, all legit; "dispose of the minor leftovers" by putting them towards your projects. Put all research and misc items on the rental, that reduces the groundwork for your own. But keep it clean, the idea is to bend the rules, not break them. Don't order several extras just so you have spare, but ordering one extra paint or bag etc is normal practice - as long as no-one abuses the privilege we keep getting "our quarter coin"

Wow cowboy, you really went to town on this today. Great work !!

Interesting debate ansd living in AK diring the 87 crash i witnessed some of the negative scenarios hinted at here actually occuring.

Since then however i heard a yank advisor offer some pretty sound advice on becoming wealthy - live within 90% of your means!

In other words, irrespective of how much you earn or develop as income put 10% of it away somewhere untouchable. Preferably with compounding interest rates.

Not easy, particularly with the excessively high living costs in the smoke, so requires significant discipline, but it can yeild impressive results in short order!

10% is great if you want to retire at 65. I currently put away 50% and this means I can retire around 45. See here for details of how your savings rate affects your retirement age:

http://www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-be…

10% is just not good enough. It takes 51 years to gather what need if you only sock away 10%. So if you start working at 20 years you can afford to retire at 71. It needs to be 15 a 20% minimum to meet a deadline of 65. Comment for murray66

10 years ago I used the sorted.org retirement calculator. According to them, to retire at 65 on my then financial path, I needed to spend $15 more a week.

that 10%, does it include targeting your housing cost.

once you take into account Time Value of Money, saving for age 65, without allowing for capital asset adjustment, can be daunting.

One reason I'm very much for provincial rejuevenation or retirement orientated sub-urban/central increase in intensification. With 40yrs of real effective inflation of 3 - 10% pa, a self-owned accomodation is a real bonus when the life expectancy is unknown, and future rents are likely to be a marginally higher yield than now to cover insurances, rates, and landlords wage increase in a more expensive world.

People in my parentsw era bought houses for 30k and a windfall of $50,000 would setup a person for life. Now the houses are 30k and that windfall is around _average_ annual wage. A million might sound like a lot now, and 2.5 million a good setup, but that might only get you a couple of nice houses today. so in 50years what is 30 million going to get you? Will your 10% p.a. now really kick out perpetuities that will hold up when average wage is 400k p.a. ?

also hiding away 10% even in a savings account, while it is good to "pay yourself first", is a fools paradise if you're paying more than ~3% in interest elsewhere.

Far better to learn some delayed gratification (yeah haha not like me) to stop getting interest bills, snowball away the consumer interest, then have room to pay yourself 10% or more

Several years ago I concluded that I will have to work until I drop dead, or am to unwell to work.

10~20% assumes someone else is working and you are profiting from their work quite probably at their expense.

In 2008 my pensions lost 22% of their then value, the present payout at 65 is now half hat when discussed at 17. So one huge loss in compound interest and capital.

So put if away yes, but have it so you can turn on a sixpence if needbe.

No point living on 90% of their income, if they're wasting 10% of that 90% on bad investment, which is why they're asking the hard question about the negatively geared rental house.

Lost only 22% in 2008? Lucky (or wise) you. How about much more at age 68 (vested in the USA)?

The only people who lost money in 2008 were people who sold. If you just held on you more than recovered the losses. This is investing 101 - don't turn paper losses into real ones unless you absolutely have to. But you shouldn't have to because you shouldn't have money you want to use in the next 5-10 years in risky funds. Personally, having seen this all play out before, I bought near the bottom of 2008 and ended up doing very well out of it (I have now sold some of these funds, so they are real gains, not just paper ones). Is it all going to turn to custard as Steven predicts - I have no idea, so I just maintain a very diversified approach (some cash, some property, some stocks, etc.)

When you have pension plans managed by "professionals" you cannot do jack in terms of control. I learned that the pensions industry is one huge pillaging con, now I do my own thing.

With professional units it's hard to ladder your investments when you perceive the market is turning. (Shifting from one style investment to different style of same of near value, to avoid a drop, then back when it starts rising again. similar to rachetting (which is more often via thrrd party guarantee system)

Regular portfolio rebalancing does this for you. You sell out when a portion of an asset class when it gets too high and re-distribute the proceeds to the other (relatively cheaper) areas.

Many professional portfolios have "early withdrawl" penalties to stop "rushes" from causing a shortage in holding cash; this often makes rebalancing prohibitively expensive. But I agree that it is something that should be monitored frequently.

Yes, my 10 year old share holdings all show 200-400% gains even though we had the GFC. Buy, hold and re-invest dividends and let compounding growth do the work.

Luck, the private pensions I have are locked i cannot manage them, big mistake but then at 17 & 24 it seemed a good idea. And yes one is locked into USA funds, so I wont be surprised if its all lost shortly.

Fortunately it wasnt part of an endowment mortgage, the "advisor" really pushed for that but I stayed table mortgage, seemed KISS. That was a good call as things turned out or I'd be buggered still owing 1/2 my mortgage at 65.

"wise" when I came to NZ I could see it was a pain in the ass (read expensive) to transfer them from the UK so I didnt. I decided then to buy shares from then on, on an ongoing basis as they can be sold quickly and easily. Sold those out as well a few years ago and paid down debt, I have not profited from the dead cat bounce, sure but I can live with that.

All pensions can be cashed out albeit at fairly poor rates. In the UK you can then move the funds into a SIPP and invest as you wish. I would like to see this option here in NZ.

More simply, how are they planning to handle around 7500 of expenses (assuming they cut out all the discretionary stuff, but keep both mortgages) on a single income of 5600?

Doesn't add up.

Agreed.

Once they go to one income they can't even afford their own mortgage and rates and insurance plus the loss on the rental, so they have to both always work. ($3900 +$250+$250+$1200=$5600!)

This couple are in a terrible financial position. What were they thinking buying a rental that losses $300 per week? At current interest rates if your rental portfolio is losing money you must be doing something wrong...

I'm about the same age as this couple. My first rental cost me $30pw and made me $50pw surplus on top of that (in 2001). Now it costs me $30pw (mortgage gone but rates/insurance up) and makes me nearly $200pw surplus. My second cost $300pw and made $150pw surplus on top, even if I hadn't paid off the mortgage it would now cost only $250pw and make me $310pw surplus (in reality it costs me $50pw as the mortgage is paid off and makes me $510pw surplus).

Their bank manager will have a conniption if he reads this article...

I wish I had done something like that back then, I was too busy being young and stupid. Can you still do deals like that? I think those returns were pretty normal back then, is that true?

You can still get pretty respectable returns today, it all depends on what you are looking at.

Yes higher returns were more frequent back then, but those two properties mentioned were different locations hence the 10 fold difference in purchase price, although the first cheapie was certainly the better returner.

Dozens of properties later, it certainly made sense to start early, however others have done equally well focusing only on their careers, although that does require constant and seemingly unending work...

Yeah I agree, I can still get a positive cashflow, but it looks as though you may have been getting well in excess of a 50% cash on cash return, which I cannot find these days. Agree re. the unending work career, I plan on semi retiring at the end of the year. Something I couldn't have done if I'd been buying negatively geared properties hoping for capital gains.

How much equity did you go in with?

I'm wondering what kind of LVR these folks had, to end up with an interest only 1200 contribution on top of rent AND a mortgage. Is the home mortgage for the deposit?? How much longer until both mortgages are cleared according to their long term budget plan?

Excellent question cowboy.... I can you they are almost done on their personal home loan. The $3900 includes an overpayment towards this mortgage and will leave them with a debt free house with an approx value of $725k. I can also tell you there is serious room to wiggle the investment property back into positive ground AND that this property is in a prime Auckland location which is boding well in this current capital gains climate. I would predict that in 2.5 years time they have no home loan, no personal loans and a positively geared property in a prime Auckland location and the financial wherewithal to live off one income and invest the other...... If they so desired all of that of course.

Get the loan and credit cards clear asap. They're high interest but not only that they can be cleared quickly, which gives a great sense of accomplishment. Immediately snowball those loan repayments into the home mortgage - it's attracting an interest cost which isn't recoverable. Whether this is done via mortgage payment or banks offsetting is up to them.

That includes the "envelope budgeting" - while they're paying off loans and interest then savings carry an immediate opportunity cost - again a bank offset loan might let them have cake and eat it too. (The banks love it because it keeps their loan book more stable and they don't have to re-sell the house loan product early, and you're more likely to spend your savings)

If they can wiggle that investment back from $1200/month interest only loss situation, I'd have to ask with raise eyebrow, why are they doing that. I'm assuming interest only, so they CAN pay down the home interest, but at $300/week loss why are they wearing this? Is it a family tenant?

2.5 yrs is short time frame, and paying off your last 10% of home loan early is generally a waste of capital (cheaper to redraw a living loan, than document a new one).

Likewise as long as the property is positive geared, unless there is a need for the income, its probably the cheapest capital raising they can get *provided* their consumption debt isn't costing them.

At that point they need to talk to a real FMA, see what investment vehicles they would enjoy, and what property risk level they would enjoy.

But that 1200 interest free cost, just really isn't on.

2.5 years though, probably isn't worth the commission loss on an auckland property. Whats the upgrade cost risk (is it modern/multi-story/character/etc ?)

Its (IMO, as always) time to start figuring in a CGT on 5+yr disposal plans.

My opinion thought is that IF they can tidy up some personal interest, then they will be in the market for an investment anyway, and if they can get that 1200 down to something realistic (under 100 tops) then they might have a viable investment opportunity. but 1200 regular loss, been there, and experience says "just no".

another thought, once their consumption debt is down to minute levels, and that 1200/month loss is fixed, then is the time to build the Baby fund and other jamjar/envelope savings projects but not before then (it;s really a cash management technique that one, not a financial/budget one, so for that they need surplus ca$h, not a 1200/month loss)

I figure they'd kick their home mortgage out to 20-25-30 year for the duration of partners off work time, certainly for the majority of the house loan.

That is another card worth having up their sleeve ....

Working For Families to the rescue.

HA!! That has to be my favourite comment of the day !!! :)

Thanks all, Some great comments on this today. Tom has enjoyed following them too. Might check in with them at the end of the year and see what they did. Everything is always clearer in heindsight.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.