By David Chaston

On Thursday, September 22, 2016, newly appointed Reserve Bank of Australia Governor Philip Lowe was asked this question in his appearance before the Australian Parliament's economics committee:

"Why are credit card interest rates as high as 20% plus even after official interest rates have fallen to record lows?".

The question is not unique; it has been asked many times of others.

But his answer was unique: Lowe said he did not know.

"I wish I knew the answer to that", he is reported as saying.

"If you ask the same questions in your subsequent hearings, I will be interested in the answers," Lowe added.

He is referring to the same Australian committee's role in quizzing the CEOs of their four pillar banks. They will each separately appear before this committee next week for a four hour individual grilling, an event that will become an annual one on their calendar.

The credit card question is sure to be raised.

What about in NZ?

It is equally relevant on this side of the ditch. Last year Commerce and Consumer Affairs Minister Paul Goldsmith and the Commerce Commission made it clear they either won't or can't do anything about high credit card interest rates.

In the past, when the benchmark OCR went up, credit card interest rates went up by a similar amount. Banks claimed credit cards were funded at rates based on the 90 day bank bill rate.

And when they went down, those same interest rates tended to slide back as well, maybe with a small lag.

But since 2012, that changed.

Credit card rates did not respond to falling wholesale rates.

We will be watching those Australian hearings carefully for the explanations given by the bank bosses.

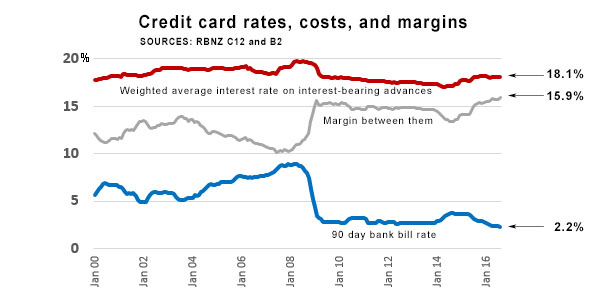

Margin swells

Meanwhile, back in New Zealand, the margin between the "weighted average interest rate on interest-bearing advances" on credit cards as revealed in the Reserve Bank of New Zealand data series C12, and the 90 day bank bill rate (RBNZ B2) has grown to its highest level since these records began.

And that comes as the wholesale benchmark has reached a record low.

Why isn't competition working in the credit card market?

Clearly Philip Lowe doesn't know, but would be keen to find out.

It is reasonable to suspect the RBNZ and Commerce Commission don't know either.

Banks seem to have implicitly decided to not compete on price. Or maybe there are some quiet signals coming from the credit card interchange brands? It is hard to know, but clearly there are no price competitive instincts in this sector.

Deluded optimists

And the situation is not helped by customers.

About 40% of credit card customers pay their balances off on time, without incurring any interest costs.

However, that leaves a surprising number of users who succumb to these 20% interest rates.

They have been labelled as "deluded optimists" who believe they will pay their cards off on time. They're not concerned about rates either because they falsely believe they won't have to pay them. Psychological tests show the more likely people are to select cards with high rates, the more optimistic they are about life.

Banks focus their promotion of credit card benefits around 'rewards' and 'low or no-rate balance transfer terms'.

Both are honey traps.

'Rewards' only work for the very disciplined, and usually come with cards that have a high annual fee.

Promotional 'balance transfer terms' are an even stronger honey trap. The benefit is real for the balance transferred, but any additional charges to the card attract the full interest rate. However, you also give up all interest-free days. It is this lack of interest-free days that most consumers don't know about, and is the trap. It is very hard to make a balance transfer on to a new card at the promotional or zero rate, and then not use the card at all during the promotional period. If you do, the bank has gotcha.

This is how one bank explains it:

You can make new purchases and cash advances on the credit card you transfer an outstanding balance to. Both will incur the current standard purchase interest rates from the date the transaction is made with no interest free days.

This disclosure is there in full; it is just not in the promotion and certainly not in the customers mind when they sign up.

Effectively, as the RBNZ data shows, banks use slick marketing to take the focus off high credit card rates, make low promotional rates slip into high effective rates quickly, and bait clients with 'rewards' that come with high costs.

'Deluded optimists' think they can avoid these traps, but the data shows the extent of their delusion. Bank profits reinforce the delusion.

33 Comments

About 40% of credit card customers pay their balances off on time, without incurring any interest costs.

However, that leaves a surprising number of users who succumb to these 20% interest rates.

No more problematic than those leaving vast sums (~$150 billion) on O/N terms for little or no interest which represents inordinately cheap liability funding for the nation's banks - sticky or otherwise View data

Step One: Open 3 credit cards. One with a $500 limit, two with $10,000.

Step Two: Balance transfer 10,000 from both cards to the $500 card.

Step Three: Withdraw $20,000 from $500 credit card and invest for <1yr in low risk investments.

Ensure you make minimum payments on $10,000 cards and NO PURCHASES.

Congratulations, you are paying 0% interest on $20,000 and earning 3-4%

Am I missing something...I'll start inuring interest after month 1 of paying only minimum amounts rather than the outstanding balance?

There will be a cash advance fee when you withdraw the 10k from each card. Banks aren't dumb. They are very VERY shrewd.

There is a cash advance fee: $1.

Trust me, I did my research and I am currently doing this.

Riiiiiiight. I think you're in for a surprise when one year ticks over. Credit card yearly fees x 3 will wipe out your 4% return on $20k quick smart. Don't forget tax on the Interest. Not to mention the negative effect on your credit rating. Remember paying your credit card off in full (not generating interest for the bank) will make you deadbeat in the eyes of credit issuers. You might find that credit will be a little more expensive down the road for you. Be warned....the banks eat people like you for breakfast, lunch and tea.

I think you're clutching at straws here mate, it's very easy to do this. I do it successfully too on a larger scale. Banks waive CC fees each year when I threaten to cancel, there is minimal to no effect on your cc rsting (positive payment histories help for future) and banks don't care.

Cash advance usually starts a higher interest rate than the balance transfer from an existing credit card.

If this does work for you be aware that there is a major risk if you miss the minimum payment date by one day, or some other event happens in your life that sticks you with large credit card debt. One mistake and you'll be set back.

A couple of years ago this was quite popular and with sums an order of magnitude higher than $20k. I had thought the banks had realised their error and excluded cash advance portions from the interest free transferred balance (ie something in the fine print of the deal).

Perhaps they consider it not significant enough to worry about.

Don't forget to factor in the annual credit card fee. Why 3 cards? that works with 2?

Easy to apply for two balance transfer cards. To get the balance transfer you need another card that isn't a balance transfer card. If you only had two cards you could only get $10k at 0%, rather than the stated $20k at 0%.

Balance transfer. 0% interest for 12 months.

"Get 0%p.a.1 for 12 months when you transfer a balance from another credit or store card to a BNZ Low Rate MasterCard."

I get around this by never using one. Simple

I get around it by having an automatic payment of the balance on the due date. That way I also get up to 50 days interest free and I get ASB true reward dollars. You just need to make sure you don't spend money you don't have...

Jimbo, i think youre deluding yourself somewhat. IF you have money then why not just pay for it then and there mate? Why do you require the use of a 50 day grace period if that is your intention anyway? Is it loyally points? Or What?

I see the need for credit card ONLY in places like the US where many accommodation places will only accept cc.

You get up to 55 days interest on the cash in your bank account or you save the interest on the cash sitting in your revolving credit mortgage account. I get airpoint dollars as well. I am about $500 to $600 a year better off using this arrangement (yes I factored in the credit card annual fee).

$500-600? Wow. So... Really you do it to save a few cents? Lol right.

I smell a very tight budget as the real reason

Why so sensitive? We also use our platinum cards as much as possible: convenience, travel insurance (covers the annual fee right there), a bit of float and at least $700 per year extra to spend. We're not on a tight budget but I reckon $700 is a bit of real money. Of course, we always pay off our credit cards.

If you don't see those benefits - or, lack the discipline required - fine. But why rip into others?

Im actually in no way being sensitive as you put, that would be you i suspect. All im saying is i see through all total bs regarding people who use cc thinking they are onto some great winning formula we should all envy. What they are ACTUALLY doing is trying to escape other bigger debt using a cc. Lets just be honest about it. Banks don't issue cc to lose money. They have many avenue streams around them, including selling the data to third party finance and marketing companies

60% don't pay off their balance each month, must be far more stupid (or desperate) than I thought.

I wonder, if you asked, what percentage realized that each time you use your card you are creating money that you are about to get charged interest on.

Credit card interest rates aren't that far from personal loan interest rates. If people need a personal loan they often just apply for a credit card as it's easier. They also get used to bridge finance on occassion.

What you'll find is that only 50% of the total are living beyond their means. Some of the people I help sort out their finances in the US have gone up to $100k of accumulated credit card debt by the time they reach their 30s. Then only when they have a cash flow crisis (think of the minimum payments) that they decide to try and take action.

Yes, I'm sure there are many and varied reasons for using the CC that are not stupid; keeping a struggling business afloat through a difficult time for example. I have always believed, and taught my children that no consumer item is worth getting yourself enslaved for. Some folk really do get themselves into a hell of a mess though.

There are obviously some clever tricks to use when it comes to credit cards, as mentioned above. However, if you are an ordinary consumer, there is no need to have a credit card when there are now debit cards to do the same job. If you don't have your own funds you shouldn't make purchases. Simple.

Lenders use them to pray on the financially illiterate and poorly disclose the consequences of default, namely a destroyed credit rating, or even worse, bankruptcy.

I disagree. If you're an ordinary consumer ... why spend your own money when you can spend credit and pay off in full up to 55 days later? Platinum may cost more but free travel insurance and usually 1% rewards back. Now the real issue is not paying it back, if that's you, you need a low rate non-reward card or better yet live within your means.

It's a no brainer really - if you put everything through it, it's way more than self funding, incl all fees etc. Add in the sweet zero percent money juggling between cards and you're away. It's probably why there's fewer 0% offers in market now :)

Perhaps it's my Scottish Presbyterian upbringing,but I am highly debt averse.

I use my Platinum card for all major purchases-flights etc and pay the balance off before incurring interest charges. The annual cost of the card is more than met by the 1% cash back and I make use of the free travel insurance.

I wonder if our spineless government would have a little more backbone if the banks,or some of them,were NZ owned?

Long story short, couple of years ago youngest daughter looked at a personal bank loan. Finance rate on $5000 for 1 year 35%. She sucked it up and survived without.

This explains why there is no competition - the banks all own one another

http://blog.creditcardcompare.com.au/big-four-ownership.php

That chart has been debunked many times before. It represents a complete misunderstanding of how bank trust departments work. Just because some many shareholders have the same trustee does not mean the trustee 'owns' the shares. Far from it.

No they do not own each other and its not what the article says about the Aust nominees arms of these banks. It must be true because you read it on the internet!!

Credit cards are more destructive than pokies.

More people get into a financial mess due to credit cards that they do from pokies. Yet we have gamblers anonymous but not credit card anonymous.

Before credit cards there was cheques and lots of people wrote bouncing cheques. The banks loved bouncy cheques because they would charge about $20 every time your cheque bounced.

Nothing changes only the means of messing up your finances with lots of help from the banks

Credit cards should be banned.

Speaking of pokies this is a good article ... very dangerous devices....

At uni they taught us 18months of slots was equivalent to 10 years horse gambling due to the large number of positive reinforcements whilst playing.

http://www.bloomberg.com/news/articles/2016-09-27/hooked-aussies-play-a…

As many as 500,000 people in Australia either have a gambling problem or risk developing one and slot machines pose the biggest risk, the government estimates. Problem gamblers can lose around A$21,000 a year each, it says.

Pushing for more protective legislation, some lawmakers gathered in Sydney on Tuesday to urge gaming addicts and industry insiders to tell their stories.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.