An early warning system exists for monitoring stress in the New Zealand personal debt markets.

It is the data supplied by the Insolvency & Trustee Service (ITS) of the Ministry of Business, Innovation & Employment.

They supply weekly lists of those who file for personal bankruptcy, or file for the bankruptcy-lite process of a "No Assets Procedure". They also record the number of companies being liquidated through their procedures, almost all micro or small business units.

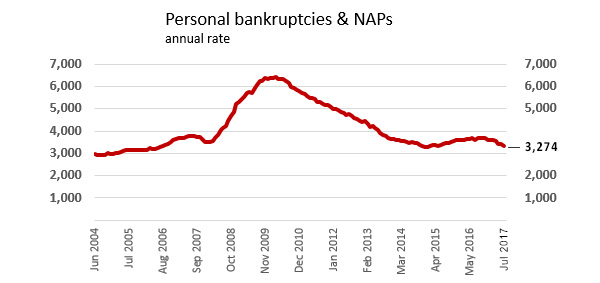

We have been tracking their reports and data weekly since July 2003. That is fourteen years, and long enough to compare where we are today with where we were before the Global Financial Crisis.

In the year to last week, we are now almost at the lowest absolute level of bankruptcies since 2006.

There are seasonal patterns in the weekly data, and processing bulges-or-droughts from ITS occasionally.

But last week, in the whole country, only 49 people came to an unfortunate debt hurdle: 26 declared bankruptcy, 19 filed for 'no asset procedure' and another 4 SMEs were placed in liquidation. In the same week a year ago, the numbers were 42, 20, and 1, totaling 63.

But to iron out the unnatural weekly variability, the most instructive way to assess the trends is on an annual, 52 week basis. It is low, by any measure.

Whatever the issues we may have over income levels, affordability, or poor financial choices, fewer people than ever are unable to handle their financial obligations and need to be tipped into bankruptcy.

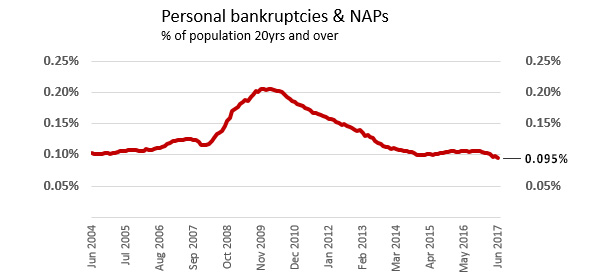

And if we do this on a 'per capita' basis, as the proportion of the population 20 years and older, we are now at a record low.

We have now dipped below 0.1% of the adult population who are forced into bankruptcy each year. It is now down to one person in every 1,053. As far as records go back on this consistent basis, it has never been above one in 1000 before.

There are no signs of significant personal debt stress in New Zealand at present, and to be fair there hasn't been since 2014.

You can stay up with the weekly changes here.

113 Comments

"fewer people than ever" - ever being since 2004 :-)?

er, yes. Would be keen to get this data from earlier (if it is consistent). Any suggestions?

Well, surely the Companies Office/Insolvency and Trustees Service ought to be able to give it to you!

What a useless analysis. "People manage to pay their debts during periods of predominantly and historically low interest rates and rising house prices". The latter probably provides cover for those debts ie equity growth keeps the creditors under control. When this process goes into reverse....mmm probably not so much.

two reasons for debt issues: splitting from your partner and interest rates. It is good to know that Kiwis are now in stable relationships. Can anyone estimate the debt stress if mortgage rates were 10%?

No. But the RBNZ requires banks to stress-test borrowers at the market rate plus 200 bps. And the Aussies require that test at "over 7%" which means at least 7.25%. (And the Aussie test applies in NZ to Aussie-owned banks.) I am sure someone in some bank has done a 10% test just for the heck of it. But don't forget the national LVR is way less than 30%, so don't expect it to be as catastrophic as you might assume. FHBs are not the whole, or even the dominant presence in the housing market. And a FHB is no longer one in five years or so. It is a temporary position.

That is reassuring, knowing we will be OK if mortgage rates hit 7 percent. I always believed the RBNZ was stress testing the banks.

New comers to NZ and young successful couples will have LVR nearer the 80%. A 20% drop in Auckland prices is quite possible. A doubling of interest rates would force prices down much further. Maybe the banks won't go bust as in 2008 but it may be very unpleasant for many innocent families. As Harold Wilson said the unemployment rate is 100% when it is you who is unemployed. And likewise repossession of say one in 50 homes would be catastrophic for 10,000 Auckland families.

I also would not underestimate our exposure to the Australian property market via our common banks. If that market turns to custard our banks will be under all sorts of stress and mortgage lending will dry up. Australia has all the indications of a disaster waiting to happen.

Will the "young successful couple" remain successful if prices drop 20 percent.

It will age them.

"national LVR is way less than 30%"

What's the source of this David? I see NZs largest lender ANZ (per their March GDS) has $40b of their $75b loan book on LVRs 60%+ ... so it would be impossible to average LVR "way less than 30%."

Does the RBNZ publish figures? Could only see on new lending (C30)

I believe David is using aggregate mortgage debt against value of housing stock . 240B / 1 trillion. Auckland sits on about 545 Billion in' value '. IMF puts our housing scheme at number 1, ditto OECD, ditto the Economist. ditto rational thinkers.. When she blows.containing a Rangitoto eruption would be easier.

If that is his method, it's flawed.

Not every house has an encumbrance. Surely, doing an aggregate LVR can only use the value of the attached property, not all stock. Even then, aggregate LVR is a little bit pointless, it's about distribution of LVR. For example, if person A has an 85% loan and his neighbour with an identical house has a 0% loan (b/c he paid his loan off but left the mortgage in place) then the aggregate is 42.5%, but that doesn't stop person A from going into negative equity if values drop 20%, or being under severe stress if interest rates go to 7%.

Agreed, you have to compare mortgage debt against the value of homes with mortgages, not total housing stock value.

LVR is irrelevant. Relying on the asset side of your balance sheet to justify a high level of debt is bonkers when the debt has itself been applied to pump up the assets on your balance sheet. When credit volume falls generally the value of the assets will fall, but your debt won't. So the margin of safety implied by these LVRs is illusory.

I agree that the V in LVR is a little subjective in credit fuelled environment. However, even the starting point of the assumption (lending divided by total 'value') was an incorrect premise.

Many commentators assume that if house prices dropped say 20% there would be calamity. But no, there would not be a whole heap of mortgages called in because of negative equity. The banks measure the lvr against the last valuation used which in many cases would be the last time there was a top up or when the house was purchased. So even though some would indeed be in negative equity territory all it would mean is that they are pretty well locked in place until prices rise again.

The bigger issue is definitely rising interest rates. Even though banks stress test with a higher interest rate that is on a net surplus model or debt servicing ratio that is ultimately dependent on rising incomes to alleviate stress and still leaves very little surplus.

It's interesting that under the interest rates prevailing around 2008 the payments on a 30yr mortgage for a $600k house were very similar to today's payments on a 30 year mortgage for a $1m house.

Good observation on the LVR front.

Although, this does assume that RBNZ retains the same setting of using origination value as the V. Which isn't a given.

The interest rate issue is of greater concern, as is expiry of Interest Only periods, where Principle payments might be required if the value has dropped 20%...

That doesn't sound right to me, V will be measured at or about the date of the relevant calculation, it will be a moving target. That's what banks do now, it seems to me the numbers are reasonably dynamic

No, they arent. If you read Bank disclosure statements (e.g. ANZ's) LVR is calculated as current exposure divided by origination valuation.

I'd suggest that somewhere around 2014, if not 2012, the population at large became more cautious with their spending and debt levels; not least because the RBNZ gave them a bit of a hand!. The GFC was a nasty near-miss for some I'd wager, and the fact that many New Zealanders daren't ask for a pay rise, and opt for 'keeping the job' instead, might be the counter argument to the above.

Life is great when house prices are exploding and interest rates are super low.....

Exactly

But not for pension funds & anything requiring (actual) return on investment ...

Suppressed interest rates designed to keep (current) debt manageable also slowly bankrupts the future's ability to service those promises (like Super) ... because the promises assumed a certain cash return on those old investments....

Ah...the current generation living off the backs of the young and upcoming generations.

"Filing for bankruptcy" is not a particularly good metric for measuring debt stress. Surely a better metric for debt stress is the proportion of income allocated to repaying debt.

Furthermore, I am not aware of any household data in NZ that measures the ability of households to handle unforeseen circumstances. For example, x months of cash savings at hand. In Australia, 54% of h'holds have less than $10,000 in cash savings and 69% have less than $30,000, according the he ME Household Financial Comfort Report.

https://www.mebank.com.au/media/2511295/Household-Financial-Comfort-Rep…

Australia also has the superb Digital Financial Analytics. It appears that a substantial proportion of Aussie households are dealing with debt stress based on their metrics.

http://www.digitalfinanceanalytics.com/blog/tag/mortgage-stress/#_ftnre…

""Filing for bankruptcy" is not a particularly good metric for measuring debt stress."

I agree. That's kind of like saying that dying is 'health stress'

It would be an emergency if there was a massive upswing in bankruptcy or other debt related actions. Being at low interest rates people shouldn't be over extended or in trouble. I suspect the interest rate required for a major problem to occur is decreasing. If we return to the total interest paid prior to the GFC a lot of people will be in financial difficulty. That's a long distance away at this point, but who knows what the future holds.

This type of news will help National win the next election

Yep - I reckon National will dine out on this news.

Looks like they might get another term anyway.

Labour still struggling away - but sadly lacking punch.

Yes I totally agree. National will have at least 2 more terms I think.

What we need is for Labour to win a term, cause / coincidentally be in power during the next recession and set the stage for a real (smaller) government to get into power and stay there for 3 or 4 terms.

Umm, Which next recession?

Oh ... you mean the one that will be caused by L/G & NF coalitions assuming power?

Exactly. Even if the fractured left coming to power doesn't spook the markets, the cacophony of at times dichotomous policies should be enough to cause the recession.

If we can believe one of Winne the Pooh's bottom lines - a mid term binding referendum on the Maori seats, Labour will never agree to this as would be an early Turkey Xmas.

They have always held nearly all these for many years and it would be the end of Labour as we know it.

So only question is - Are we going to have a binding mid term referendum on the Maori seats.

Winne knows full well Labour will never agree to this and the seats are toast in any referendum as recommended by the Electoral Commission report of some years ago.

My bet - Yes - the referendum is on ! So another National led government.

Interested in others thoughts ?

Those who vote on the Maori roll would just vote on the main electoral roll. So little effect on Labour or anyone other than the Maori party.

It depends on the actual location of the voters. The Maori electorates overlap multiple general electorates.

For example: Te Tai Tonga, covers the entire South Island plus Wellington City.

If you move those votes, it will either make Labour win their current electorates by more, or perhaps have a slightly closer loss in National held seat. But it is unlikely to provide them an extra seat.

So on the whole, removing the Maori electorates will be detrimental to Labour

Levels sitting about the same as late 2007 as far as I can see and I think we know what happened next.

Perhaps not the greatest leading indicator of "trouble at Mill"!

Imagine a parliament with just 100 seats - another binding referendum.

Can a statistician say what would happen with larger electorates - would they not by definition tend to be closer to national as in across NZ not current local electorate party voting numbers ?

Imagine if an elected government actually followed referenda... this country would be nirvana.

Re: electorates, I assumed that a smaller parliament would mean fewer list seats, not fewer electorates? or would it require both?

"it has never been above one in 1000 before."

Never been below? 1/1053 is less than 1/1000.

Fair enough. You are right.

My take on this..

1. Home ownership rates has been decimated under National so it's not surprising that this early warning indicator isn't flashing red. (another topic but huge problems are now projected into future when renters go to retire)

2. The decline in sales is originating from Auckland, where the prices are based on Chinese investors. Another danger is the money being pulled back home. Like in the Asian financial crisis of the 90's, the free-flow of capital made the situation worse. Interesting papers here and here, there are analogies.

3. Thelma and Louise (banks and borrowers) have driven off the cliff but are blissfully unaware of gravity as the car coasts forward. That's what I think of when I look at the prices on homes.co.nz. It takes time for people to convert their panic into action and put their house on the market and we're not there yet.

4. At the moment many home owners are super relaxed because they know there's a buyer for their house somewhere in China. If that perception suddenly changes then the complacency will give way to sheer terror as the market reverts to "fundamentals" P/E & P/I etc.

At the moment many home owners are super relaxed because they know there's a buyer for their house somewhere in China

Wow!

No wow factor. That's just BBQ banter. Everyone hopes that a Chinese buyer will pay them a king's ransom for their home. Doesn't mean it represents reality.

No, I think this comment genuinely reflects the level of stupidity and greed regarding foreign buyers that exists in this market. It verges on hysteria.

You need to think like Family Feud. "It's not what's right. It's what 100 NZers think"

The housing prices didn't get to where they are by Facts, due diligence, and stone cold Logic.

Well, they are in for a rude shock. Last time I looked, mass hysteria did not constitute a fundamental capable of supporting the property market

The smart ones have paid off debt over the last 8 years. The rest...well it's up to the masses now.

The 40% or so of new borrowers on interest only loans haven't paid off a goddam cent.

Hallelujah again Bobster, you've hit the Nail this time - well done :)

please allow me to finish your sentence by saying : and have bought two more rentals properties :) and paying less tax than before and living happily and relaxed.

Eco Bird - the saying is true...ignorance really is bliss.

:) .. read my post at the very bottom and tell me what you thing - then we will discuss "ïgnorance"

Think you're best left in bliss

Exactly, interest rates have been low enough now for long enough to really smack that mortgage. If on the other hand you have been stupid and used the low interest rates and the doubling of your house value as an excuse to use your house like an ATM then you deserve to be kicked in the arse if the interest rates spike.

Eco Turd, he's talking to you mate! Mr negative geared interest only, and proud of it. Please sort your finances out and get them on a more stable footing, while you still (barely) have time. I am worried about you. Seriously.

Sorry, not sure what happened with my spellcheck there. Freudian slip.

Thank you for your concern - I will survive ...

Being a "boomer" , I must say I have a yen for the old days; in fact I can renminbi when petrol was 10c a litre.

36 cents a gallon , and coin operated pumps

RBNZ painted a slightly different lead indicator in their FSR May 2017

…but indebtedness has continued to rise.

Household debt-to-disposable income rose to 167 percent in March,

and debt has also increased as a proportion of income in the agriculture

sector (figure 2.8). While low interest rates have eased debt serviceability

burdens, higher indebtedness has made borrowers more vulnerable to a

sharp rise in interest rates or a fall in incomes

http://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Financia…

The 167% is the canary in the coal mine. The bankruptcy filings are the dead miner in the coal mine.

MisterB I agree as people tend to fall for faulty technical analysis logic. Chart based analysis is historic in nature and tells you what has happened after the event. Looking for bankruptcies or other financial last resorts is very historic, by the time they work their way through the system it can be a year or two after the event that caused the financial failure.

Totally agree

Tough news for the interest.co armageddon forecasters club. Add that banks ppn of lending to high DTI/LVR, is considerably down, mortgage stress indicators are moderate, recent surveys showing a majority of people consider they have enough income for their needs, interest rate increases remaining a shimmering distant mirage, and it's possible some of the dystopians contributing to this august site could shortly be overcome by existential crises.

Armageddon forecasters don't really exist. Nobody can accurately forecast Armageddon or even a housing crash. Prior to the GFC, there were even fewer people who could entertain the possibility.

J.C. As an investor I've lived through a number of significant downturns and every time it happens there are fevered doomster zealots saying 'told you so'. Of course, eventually they will be right. But between their brief moments of glory they endure long periods of grim foreboding while we investors just get on with it, build our assets, try to manage our exposure to black swans and deal with what life throws at us. The GFC was a severe hit for many but in time markets recovered.

This is not like "any other downturn". Household debt vs income is at unheard of levels (170%). Prices are at multiples of income that are twice the long term average and make news even on an international scale. 40% of new borrowing is interest only. Yields are at an all time low. To return to long term averages via wage growth would take decades.

I mean, the fall in prices that is coming will not come like a bolt from the blue. I don't know whether it will be gradual or sudden. It has been well signalled. An investor who is "in it for the long term" and chooses not to leave the market when prices are 10x income, and with all these other "credit bubble" indicators flashing like crazy, needs their head read. Seriously.

Bobster. So be a clever little pony and tell me where those investors should put their money?- because it has to go somewhere and doing nothing is not an option , especially if they live off returns. Equities at record PE ratios, banks at negative real interest rates and who, according to the Megiddo valley tribe, are fiddling their stress testing to produce false equity to debt ratio numbers so could themselves turn turtle.

Irrational exuberance has over driven Auckland property prices and the inevitable correction has arrived. The extent of this is yet to be experienced and interest.co commentators have multiple views but really it's yawn, snore. A number forced to sell will take a haircut and exit but most will ride the escalator down. Aucklands suppressed housing demand is not going away so the floor will be found in due course; there will be some wailing and wound licking but mostly sitting tight, waiting and hoping. Not exactly the pathos and drama which the doomsday club get off on.

Any investment where it is not likely to be a loss of at least 30% of its real capital value over the next 5 years. Doing nothing IS a better option than keeping it invested in property right now. Yields are terrible, no one is investing for yield at these prices. Who is living off property yields @3% gross in Auckland? Who is even breaking even at that level? No one.

Our best guess of the floor is long term averages. Do the maths.

Who wouldn't exit an investment when it was at a level that represented a multi generational high, when the only way in real terms is down? The greedy and the stupid. And there's plenty of those here, unfortunately.

Agree Bobser - I think what we've witnessed over the last 5-10 years in our property market is a once in a 100 year event...to think its the 'new norm' is naive...

https://caldaro.files.wordpress.com/2011/01/case-shiller-updated.png

{kind=link}

Incredible how fast bankruptcies almost doubled in 18 months during the GFC, and that was with the OCR being cut from over 8% down to 2.5%.

And here we are all these years later with an OCR of 1.75% and nowhere to go (or not far anyway).

Just goes to show, if you don't have a job, an interest rate cut doesn't help that much. Maybe New Zealand is special and we'll never go through another recession? Nah. Maybe everyone can switch from principal and interest to interest only....nope, 30%+ of mortgages are already interest only.

I don't think the canary is coming back out of the mine.

We'll have a financial event at some point which will make most of the country hurt. The household debt levels built up at this point are exceptionally high. Sure there's a chance the debt could be slowly wound down but it's more likely that something will go wrong where all the debt is concentrated.

What would be the impact of "winding down" on consumer spending? Probably quite noticeable. Probably not good for the money tree economy as well.

There's seemingly still room for debt to be reduced without major impacts. Although I could be wrong and we might be past the point of no return with our current household debt.

Net international indebtedness is falling - albeit off the back of rising overseas equity values. And that rise could reverse. But given a significant portion of household debt is owed by mum and dad investors and will be backed by solid equity in other property, mass foreclosures aren't likely.

A decline in property values will negatively impact a banks collateral level, regardless of which property constitutes that collateral. It could be the family home. At some point the bank will require a repayment of debt to restore its collateral levels given a fall in property prices. Unless the investor has the means to repay that debt the additional equity can only be obtained by sale of the investment property (ies). So foreclosure is not the issue, the issue will be a banks requirement to maintain its collateral ratios which will trigger sales.

Agree. I was using the term foreclosure analogously. You correctly identify income as the key issue that will drive stress and trigger forced sales. Simple changes in DTI driven by falling valuations will not, of themselves, create mass selling and plunge the market. A severe downturn in the economy however, will definitely do so.

No, you missed the point, falling property values will cause forced sales and reduced new borrowing, as banks will look to maintain their collateral ratios. That is regardless of income deterioration. "Plunge" is your word, but falling values will more or less be self perpetuating in terms of reduced availability of credit.

Totally agree. The interest only mortgage figure is frightening. In July last year it was 40% of new borrowing. Gold plated ponzi financing.

Haha but the culture we have in this country at present is that if the canary died the shift manager (National) would claim it to be a sign of success - and the people would rejoice while suffocating (on debt).

I think this article is quite misleading...

The misleading content is from MBIE. They are a troubled ministry and no doubt will do whatever they can to get in the good books with National.

The invention of Interest only loan is the best thing since sliced bread ...

I would like to put my neck out and suggest this to ponder:

Who controls interest rates' movements in the World? ... answer the Federal Reserve - all RBs in the developed world ( who matter) are somehow connected to what the FED does as it controls the main moneyhub in the world - It is the US$ that regulates the prices of all commodities, Bonds, and Food - the main reserve currency in the world - FED controls US$ price ...

RBNZ said that they have to move in tandem with everyone else ... The FED said lately that we are going to raise it slowly but surely in a way that does not cause huge disturbances in the world monetary system ... and will shrink their balance sheet through monitoring the health of the economy blah blah ...

We all know that interest rates are taxes paid by everyone ( borrowers or Not) to the lenders ( that applies to individuals and nations alike) and these amounts of interest money find their way to the few big money sources in the world by means of a funny yet complicated capillary effect. So when and how can this happen and should we be worried ??, ... It will happen when their "customers" show signs of recovery and having enough money to pay the extra gradually without rocking the boat ... and regardless if we are poor or rich as everything is proportional ..

In my opinion that is few years away and we shall gradually get used to incremental increases as they dribble in ... We hear almost all RBs around the world ensuring their customers that it will happen slowly and the message is : Don't Panic

So no shocks are to be expected and No recessions will miraculously appear no matter what the doom and gloomers predict unless an idiot or two ignite a big war somewhere or an asteroid hits earth. Most economists have thrown away the fundamental book and succumbed to the fact that controlled money creation could indeed be swept back slowly over a long period of time ... and at the pleasure of the Printer.

For all the above, I sleep better at night, .... I stand to be corrected.

Alex Jones, is that you?

Sorry I missed your point...

Are you implying that the Fed is God and Janet Yellen will make it okay for you to speculate on house prices?

Animal Spirits are more powerful than tinkering with interest rates....Reckon Yellon's husband might know a few things about that (the books he did with Shiller are worth reading if you haven't read)

you are right, you missed the point big time

this has nothing to do with speculation ...or house prices

It's these types of interactions that really worry me about the lending that's been going on by our banks in this country...

Ok, all BS aside...Banks ( and any Lender) know what they are doing and what they are up to - they have deep pockets to make sure they stay afloat - anyone suggesting that they lend recklessly and causing credit bubble etc needs a bit more education on the matter ... they follow risk factors and profiles, they have business plans and balance sheets as well as share holders.... they float with the big system riding their wave and I can assure you that they do not throw money around to everyone walking through the door ...their current lending serviceability rate is around 7.85% ..i.e. they lend you money as if you are going to service it at that rate.

My line of thinking was that as long as the main lenders of the world are not in Panic Mode, but far from it, then we do not have to worry too much about rising interest rates sharply or very soon as some are suggesting.

Again ignorance is bliss...

You said all BS aside but then you said banks know what they're doing..? Sure about that? - history doesn't give them such a great track record. It's their job to portray that image and their economists have to follow the party line - I.e the one that is best for business and doesn't scare the herd too much when things look risky...(or are about to deleverage). The advice/outlook to the public is almost certainly different to the one they discuss internally (the actual assessment of risk and market conditions). The last thing they want is a run made against them if sentiment shifts...

It's hard to tell if you're being serious or sarcastic. Do you really believe that the US Fed and Banks can tell if another recession is possibly going to hit? The same organizations that had no idea about the GFC?

Or maybe you are right. Maybe they got their hammer out and hit their crystal ball, which now has a 100% prediction accuracy. After all, whoever heard of a bank ever being greedy and lending recklessly and going under or being bailed out... *cough* BNZ *cough*

Yep, you have been living under a rock for the last 10 years.

The Bank of England, with similar household debt levels to ours, are getting mighty worried Eco Bird:

The first signs of the Bank’s anxiety about consumer debt came from its governor, Mark Carney, a month ago, but Brazier’s comments marked a ratcheting up of Threadneedle Street’s rhetoric.

“Lenders have been the lucky beneficiaries of the benign way the economy has evolved. In expanding the supply of credit, they may be placing undue weight on the recent performance of credit cards and loans in benign conditions,” Brazier said.

The willingness of consumers to take on more debt to fund their spending helped the economy grow strongly in the six months after the EU referendum, a period when the Bank expected growth to fall sharply.

Over the past year, Brazier said, household incomes had grown by just 1.5% but outstanding car loans, credit card balances and personal loans had risen by 10%.".............

And re the GFC as it played out in the UK:

“Complacency gave way to crisis. Companies and households were unable to refinance their debts. The result was economic disaster. In this country alone, close to a million jobs were lost and more than 100,000 businesses failed. Too much debt made the financial system, and the economy, unsafe. Too many people paid the price when those risks materialised.”

https://www.theguardian.com/business/2017/jul/24/bank-of-england-househ…

Thank you David,

Why are we comparing ourselves to the UK or any other country?

We all know how messed up their banking is? no need to go into details on that...Barclays and RBS fiascos etc...

I know where you are coming from but that is all good in theory, however each country's financial situation is different ...and i believe that RBNZ is keeping a tight lid on the market and running stress tests to assure market stability.

When I hear that there are people who have a debt to income ratio of 170% , I say great, one more idiot will be out of the way soon .... If there are lenders of last resort who want to put their entire business at risk by making unsecured loans then that is their mistake when these loans default...and consequently few illiterate borrowers will end up in the gutters ..it happens everyday.

Assuming that everyone is signing up bad risky loan and they will all default once interest rates go up by 2-3 % or house prices ( in the given set of circumstances) will drop 30% overnight then that's a bit rich and ludicrous.

There is a certain amount of reasonable risk taken in doing business everyday and without that there wont be any advancement or improvement in life - everyone might as well shut shop , stay home, and pray !.

I know that all our major banks are responsible and prudent and the majority of borrows are too .... and the proof was in the relatively little damage we had in NZ during the 2008 GFC collapse.

Thank you Eco Bird, fair enough but we have become too dependent on rising debt to underpin our economy. Last financial year we bunged 28 billion of new money (through private sector debt) into our economy - one dollar in eight of our gross turnover (GDP). A significant moderating of that, never mind it actually stopping would pretty much break the economy with some very serious consequences.

How much higher can we keep pushing our debt ratios? Your figure of 170% is actually pretty close to the average not an outlier. The Kiwi household debt to income (168%) is now one of the highest in the world and significantly higher than the UK where there is considerable concern as per the article I linked to.

https://tradingeconomics.com/new-zealand/households-debt-to-income

thanks David,

Yes we are / have been borrowing more as a nation since 2012 and that is to sustain our way of life, pay for the ever demanding services needed, pay for two earthquake damages and so on ...and it is also higher because our export prices and trade size is not increasing enough to balance that out - add to that our productivity as a nation is not improving fast enough.

Yes housing borrowing has added to the tally in recent years but that does not mean borrowers are going to default anytime soon - Ordinary Households cannot have 168% d/I ratio - they wont be able to sustain that for 3 months let alone years, so this generalization and using the figures this way is incorrect in my view -

if there would be a default, then it will be the Government and the Banks who own and owe the most of that debt - Unlike Joe Blogs, these people can and are allowed to negotiate their way out / reschedule and have the backup of the RB and the big boys ( with tightening of fiscal policies etc) ....

hence my view that doom and gloom is exaggerated in the current economical environment and throwing around these 168% debt figures just fuels a fire that is yet to exist.

NZ is growing at a good rate of 3.6% pa and that is allowing us to pay our way in both moving forward and paying debt. Some of that growth is trickling down into people 's income allowing them to advance ... and maybe borrow for more growth.

If Eco Bird accurately reflects the instincts and intellect of the average property investor, the country is well and truly screwed

Eco bird - you obviously don't subscribe to Minsky's theory of financial instability. We've had one "exogenous shock" already in the form of a policy change from Beijing. Imagine a sharp movement in exchange rates.

Hi fat pat,

One can imagine all sorts of interesting events from an exchange rate movement to a banking system collapse to a war.

But that's precisely why people put their loot into property: it gives far greater security in the longer term when things go belly-up.

You could be right, but it that depends on how you define "belly up". I was thinking price declines & negative equity, the bank impolitely asking for it's money back, financial strife in China, negative feedback loops involving reversal of capital flows & depreciation of the NZD by say 30% vs the USD.

good point about instability - but the issue is not people putting "their loot" into property but leveraging into property, and everyone clamouring to do that in an easy credit environment has therefore driven the cost of those houses up, like bidding on a signed beiber t shirt.

That's precisely what causes things to go belly-up and although it gives the illusion of security, a leveraged negative cashflow property is worth exactly only what the next purchaser can or will pay for it.

That's why I posted the link to that Minsky paper in an above comment (also below). The paper highlights that domestic leverage is not the only risk. The carry trade, interest rate arbitrage, people borrowing overseas to speculate in NZ, there's been a lot of that going on and it matters a great deal. Of course you're right if the transactions carry no leverage then there's less risk, but who knows what percentage of the foreign buyers were levered up? I guess we could be about to find out.

https://www.ucm.es/data/cont/media/www/pag-41460/Minsky%20theory%20of%2…

Ok so interest rates are very low but what about the 30 year mortgage factor? Many people will still have mortgages into their senior years. Without the large capital gains of recent times this is going to be an increasing stressor ipredict.

No evidence of personal debt stress. What about the explosion in size of payday lenders and the likes of those that offer debt consolidation loans. This always happens at the mature end of a debt driven binge! Bargains rife soon!

Can you link to any analysis concerning this explosion? It's no good just stating it without backing it up with some data.

Household debt to income has risen from 80% in 1996 to 170% today. What else do you need to know. Debt is at unprecedented and unsustainable levels. What part of that don't you get?

This article states that we are not under stress. I was just looking for data concerning the explosion of payday loan places.

Thanks Instant Finance...

My goodness... there is so many doom and gloom folks around here ..it is scary.. but i will rest my case - this discussion is hopeless :) .. keep up the good work guys...

June trade surplus $242 million, boosted by dairy exports ...:)

@Eco Bird - You continuously mistake a healthy and rational fear of a bursting bubble with "doom and gloom" ...

Your response to very legitimate concerns shared by the overwhelming majority of central bankers, economists, real investors et al, around credit bubbles and household indebtedness and the institutionalised QE of the last 8 years is always "stop being so gloomy, be happy!"

That's akin to telling someone driving a car towards a cliff to change the radio station instead of turning the wheel.

You've made no case to rest, let alone a coherent one. Better to have everyone think you're an idiot than post in the middle of the night and confirm the fact.

look my friend, you ( and the overwhelming majority) can keep worrying about HH debt and that nonsense and shiver under all this stress you are creating for yourselves ... while I continue to running my business smoothly in this fearful Gloomy environment and enjoy my early retirement ... I have eyes, ears, and brain to resolve data and facts and make my own decisions.

Unlike you and some others here, I am not here to prove a point .... I sounded my views and opinion ( and that is my case) - it's too bad that you disagree , but hey that is life ... we dont need to agree .... So chill , i suppose the housing market is stressful enough for you nowadays . no need to get stressed about my comments :)

I have made more (physical money in addition to the paper money ) in the last 8 years than in the previous 8 ... You see, some of us enjoy our music while driving steadily towards a cliff - its fun , you should try sometime ! ... bungy jumping will be a good practice for that .....OH, BTW we are not in a bubble of any shape or form.

Your statements "OH, BTW we are not in a bubble of any shape or form." and "I have eyes, ears, and brain to resolve data and facts" are contradictory.

Of course, your business, which you've gone on record saying is OK at zero or even negative yield, is hardly a business is it, so I wont be making any financial decisions of the back of anything you have to say.

For your reading:

What is a 'Bubble'

A bubble is an economic cycle characterized by rapid escalation of asset prices followed by a contraction. It is created by a surge in asset prices unwarranted by the fundamentals of the asset and driven by exuberant market behavior. When no more investors are willing to buy at the elevated price, a massive selloff occurs, causing the bubble to deflate.

Read more: Bubble http://www.investopedia.com/terms/b/bubble.asp#ixzz4nuh8TLfe

Follow us: Investopedia on Facebook

Sure, rental properties at a yield below the cost of interest is a fundamentally good decision, apparently.

Key words mate "When no more investors are willing to buy at the elevated price," we are not there yet my friend ..don't be fooled with the winter and election slow down - just be patient ... you will see them coming out of the woodworks ... and just don't take anything you read for granted. you have to hang fundamentals out to dry at times, and have them with a grain of salt ... There is No bubble :)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.