By Jenée Tibshraeny

How can you be confident about investing in financial markets when there are so many forces at play that can make or break your investment?

US President Donald Trump could push North Korea over the edge, interest rates could stay low for longer, world leaders could adopt more ambitious carbon emissions targets, China could up the ante on its capital controls, or Winston Peters could become Deputy Prime Minister.

No one knows what the future holds.

The question is, who’s in the best position to protect your money from the risks and see where the rewards lie?

There’s a school of thought that navigating the minefield that is the market is humanly impossible, so over the long term you’re best investing in funds that tracks the market. I looked at how you could do so through passively managed or exchange traded funds in this piece.

There’s another school of thought that you’re best paying higher fees for a fund manager to keep re-jigging your investment to beat the market. I consider this option in this instalment of my Generation Rent Investment Guide.

The basics

If you’re a KiwiSaver member, you’re probably already investing in a managed fund, where your money is pooled with other investors’ and spread across different kinds of investments.

The beauty of this is that you get access to assets and products you wouldn’t always be able to invest in on your own. Your risk is also reduced by your investment being spread across a range of these.

While you decide what sort of fund you would like to invest in based on your risk appetite, you’re pretty much leaving it to the experts to do the work.

An Authorised Financial Adviser (AFA) at Hassan & Associates, Simon Hassan, says: “While the research shows that few active managers outperform passive funds over the long term, capable active managers can add value, especially by reducing risk.

“If this makes investors feel a bit more comfortable during or after a downturn that can be worth a lot.

“Good active managers may use derivatives to hedge currencies, or to limit 'downside risk' - seeking to lessen the impact of a market downturn. Others try to add value by researching little known (say smaller, or emerging) companies.”

Hassan suggests investing in a mix of actively and passively managed funds.

Nonetheless, if we’re just looking at the active side of things, these are some of the questions you should be asking as you weigh up your options:

- What am I trying to achieve?

Before you do anything, you have to identify your risk appetite and decide what sort of asset class you would like your fund to be based on.

There’s a quiz, as well as other basic investment information, at sorted.org.nz, which will help steer you in the right direction.

Conservative funds are more weighted towards bonds and cash than growth funds, whereas growth funds are more weighted towards equities and property.

- How active are ‘active’ fund managers?

Once you have a clear idea of your risk and the time you have to maximise returns, AFA and Summer KiwiSaver investment committee chair, Martin Hawes, suggests you check how actively managed a fund really is.

You should ask yourself whether the higher fees you’re being charged are for true active management, or whether the fund is actually just a closet index-tracker.

Melville Jessup Weaver actuaries Ben Trollip and William Nelson consider the issue: “If I [a fund manager] were to hold 48 of the 50 stocks in the S&P/NZX 50 index (at their index weights), and just slightly overweight Xero and underweight Trade Me, would you be happy paying me a large fee?

“With over 90% of my portfolio simply replicating the index, perhaps you’d argue I’m due at most 1/10th of a full active management fee.

“After all, most of my portfolio would generate the index return, making it unlikely that the overall result would differ too much from the benchmark.”

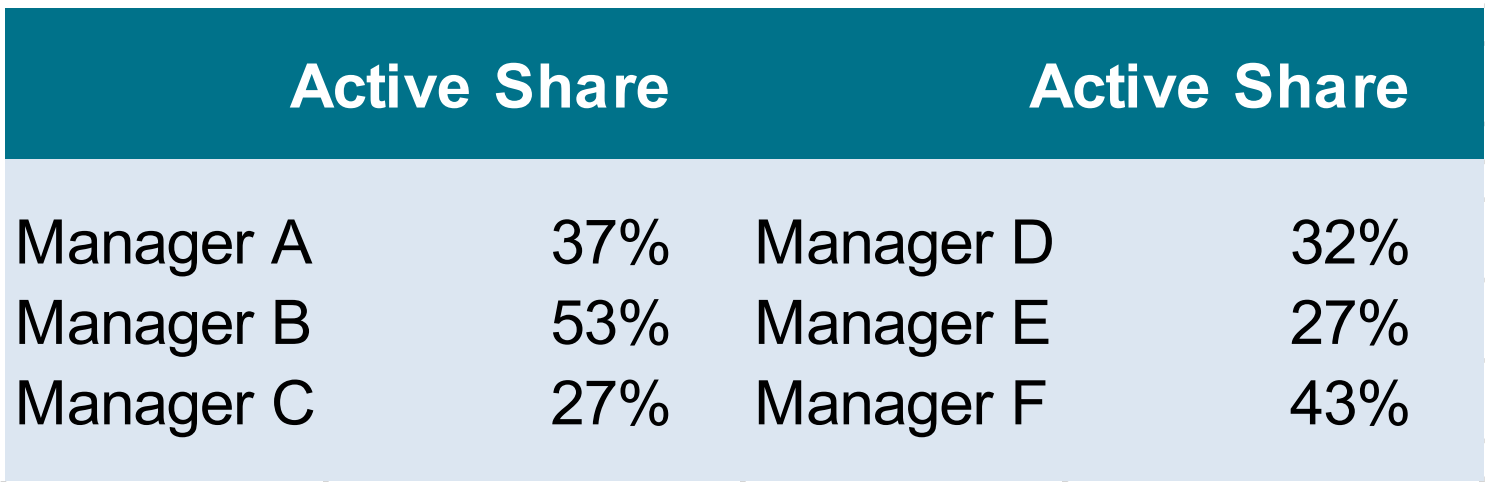

They go on to explain: “One way to quantify activeness is “active share”. Active share measures the level of activeness by tallying up how different a portfolio is to the benchmark.” (See their paper for a longer explanation).

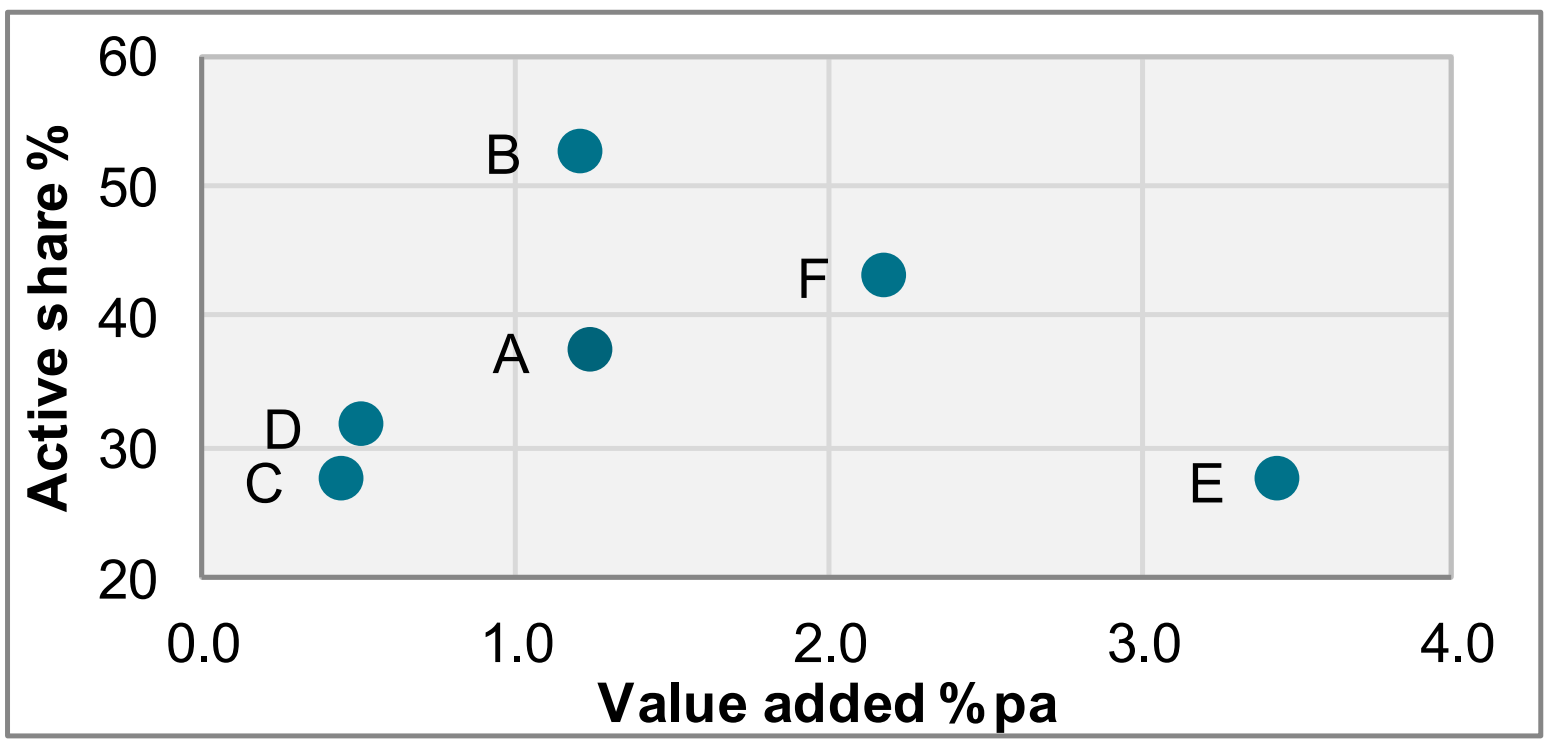

The six New Zealand equity managers Trollip and Nelson looked at in December last year, have active shares of between 27% and 53%.

“This is perhaps surprising for a cohort of “active” managers,” they say.

"Managers C and E have just a net 27% of their portfolios different to the index – or, put another way, they are 73% passive! These managers are relying on just a net 27% of their portfolios to reach their value added target.”

Although Trollip and Nelson have looked at a small sample, the funds with more active share generally perform better.

Yet Trollip and Nelson recognise it’s difficult for New Zealand fund managers to differentiate from the index as much as their counterparts overseas, as our market is very concentrated.

So while you should make sure you are getting what you pay for, they say you should be sure of your risk tolerance “before blindly pursuing high active share portfolios”.

Hawes recognises it is difficult for retail investors to calculate active share, but says you can look at the top 10 or 20 holdings in the portfolio and see how closely they align to the index.

- By how much can fund managers adjust their asset allocations?

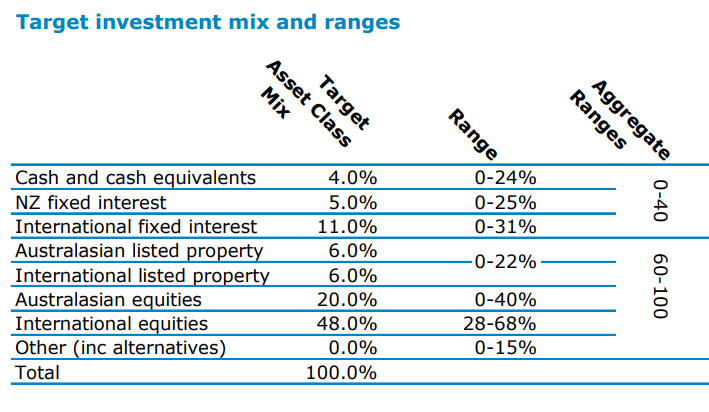

The other thing to look at is how much flexibility fund managers have to adjust their asset allocations to best manage risk as market conditions change.

This information should be in a fund manager’s statement of investment policy or product disclosure statement.

As you can see in this example, ANZ’s Growth fund managers have quite a bit of flexibility in the way they allocate funds.

Hassan says it’s also important fund managers have a “disciplined approach”, with “clearly defined asset selection, portfolio construction and management processes” that don’t veer from one idea to the next, and stay 'true to label'.”

In other words, you don’t want to find out that a ‘NZ share fund’ actually includes a lot of fixed interest, or derivatives for example.

Hawes goes on to say that while it’s one thing for fund managers have the mandate to allocate assets tactically, it’s another thing whether or not they actually do so.

How are you and I supposed to find out the extent to which they’ve done so as market conditions have changed? Simply ask?

It’s not that simple according to Hawes: “One of the really difficult things [in] this whole thing regarding funds is that the retail investor, without independent research, will find this really hard to do. Like really hard.

“Financial advisers… spend pretty much all their working hours looking at this stuff. But a retail investor, even if they knew what they were looking at, they probably wouldn’t have the time…

“Morningstar and the likes are making visits to the fund managers and saying: ‘What are your processes and who are your people?’ which are the two key things.

“Whereas if you rang a fund manager and said, ‘I’d just like to come in and have a really good chat because I’m thinking about investing $10,000', they’d stifle their laugh, only because they’re being polite.”

Ouch.

- How have fund managers weathered past storms?

While these structural considerations are paramount, there’s no getting around the fact you’re going to look at what a fund’s past returns are.

Hassan warns this is a “folly”, as just because a fund has performed well in the past, doesn’t mean to say it will do so in the future.

I agree, but believe there’s value in taking a long term view of a fund’s performance.

Sure its returns may have been good over the last couple of years while the market’s been a box of butterflies, but how did it perform relative to the market during the 2008 Global Financial Crisis?

- Exactly what are you paying fund managers for?

Paying higher fees (of around 4% for example) is part of the managed fund package. However you need to weigh up whether you’re getting bang for your buck, in terms of returns and active management.

Furthermore, Hawes is morally against fund managers charging performance fees.

He says it’s a “one-sided deal” for them to receive a fee for beating the market, but not lose out if they don’t beat the market.

Yet with boutique fund managers typically the ones charging performance fees, Hawes admits many that slap on these fees are actually very well performing.

He still calls performance fees “a nonsense” as they incentivise fund managers to chase returns, not manage risk.

- Who are the individuals you’re entrusting your money with?

Equally as important as the process being followed to invest your money, Hawes suggests you pay attention to the people doing the job.

Ultimately he says: “People invest with people.”

Have a look at how a fund manager has dealt with market peaks and troughs in the past.

Albeit from a biased position, Hawes says it can be beneficial investing in a fund where there are “people with a profile” involved.

“I’m thinking of myself here as well, with my involvement with Summer KiwiSaver. It’s a completely different beast when your name is over the door… [You’re] basically putting your reputation on the line.”

Of course, you don’t simply want to invest in a fund due to it having high profile managers, but reputation and accountability are worth considering.

This is all too hard…

If you’re anything like me, at this point you’re thinking, how am I meant to weigh up all these factors and make a well informed investment decision?

Retail investors are on the back foot when it comes to getting access to information and it seems that unless you have hundreds of thousands of dollars to invest, it’s going to be difficult to get help. Even Hassan says his average client has around a half a million dollars invested.

Don’t despair.

Hassan reassures me there are still AFAs who will advise you. You just need to make sure the advice is independent. It’s better for you to pay your adviser’s salary than the firms whose products they’re providing “advice” on doing so.

If you think you’ve got this under control yourself, I suggest you ask fund managers as many questions as you need to ensure you’re confident in your investment decision.

With the proliferation of KiwiSaver, and a generation of younger people looking to the equity rather than property market, I believe fund managers would be foolish to be dismissive of prospective clients - no matter the size of their wallets.

Take it from the journalist - do your homework, ask, and don’t settle for convoluted responses that mask the facts.

21 Comments

Although I own my house so am probably not considered generation rent. I am still finding this series of articles very interesting and informative.

Thanks for posting them.

Trust me this works , especially if you gear the investment 1:1

No idea what you mean, please explain

Margin lending. You use the existing equity in shares/bonds/funds as leverage to borrow more capital to invest. Its the same concept as borrowing against your first home to buy another property.

Personally I'm kind of wary about mutual funds. The majority of ones I find fail to constantly beat the benchmark index their associated with. They can be quite good for access to niche markets like emerging companies, pharmaceuticals, infrastructure in multiple countries etc though.

But you have no choice with kiwisaver you have to be in a fund, as an industry they have us by the short and curlies

That's not strictly true. Simplicity is a good option for lower fees, and is more akin to an index fund rather than a mutual one as they don't actively trade. Also, Superlife allows you to invest in individual ETFs as well as pre-packaged funds which are a combination of ETFs (again, not actively traded).

Simple 3 step process for investing in the sharemarkets:

1 - find passive ETFs that track diversified baskets of shares that match your outlook (e.g. NZ, US, sectors etc). If in doubt, go for the most diversified (Total World)

2 - invest in the ones with the lowest fees

3 - relax safe in the knowledge you are not buying yachts for fund managers

This is the correct way to invest.

Passive investing in indexes with low fees, DCA and rebalancing are important too but if you put your money in passively this tends to carry out those tasks automatically.

It's not the only way to invest but this is the least effort and least stress way.

If you go Total World then re-balancing is automatic by default. Dollar cost averaging is only better if you have a steady income. If you have a lump sum to invest, you are more likely to do better investing it all now (as the overall trend is upwards).

Absolutely. I know someone who did a statistical check to see the best way to deal with lump sums, the answer always comes up to just put the whole lot in at once.

Agreed, except for the relax part. What happens during the next bear market? History suggests retail investors can't take the stress of watching their investments collapse and will cash out at the bottom only to reenter the market near the top. One of the weakness of ETF's is they enable investors to trade them at a click of a button.

The relax part is critical to success. Set and forget your regular investment and then only check balances rarely.

Got all that but ultimately I am not planning to die happy in the knowledge that my set and forget fund is still trundling along. As with all investments the problem comes if you just happen to need to cash up or start drawing down for income, just when the market is on a downer. No real answer to that one I guess.

What about looking at the 5 year+ performance and assessing the fund volatility as well as the return.

Milford provides graphs for their various funds, most of them don't fluctuate much,apart from their highest risk Dynamic fund.

Some with good long term average returns contain a lot of nerve wracking rises and falls; all other things being equal I'd go for the less volatile personally.

One issue to be aware of is that for the last 8 years (give or take) the volatility in the market has been low so if you run traditional standard deviation or volatility calculations over a time series of data you are going to get results that show an uncharacteristically low number and one that is probably not a true reflection of the risk.

The current risk indicator that funds in NZ have to show is also skewing results to the downside and providing investors with a false sense of security in the current environment. We are seeing Balanced Funds and Growth/Aggressive Funds with the same risk indicator.

Rather than just concentrate on the lowest volatility you also need to look at the long-run risk adjusted returns and a funds downside risk (Sortino ratio) numbers over the last 10 to 20 years to probably get a good idea of the volatility of the funds over different market conditions.

We have never had such low interest rates to underpin the share market, so going way back in time before some managed funds and/or fund managers even existed might not be that useful.

The Milford Growth I'm with has been unusually cautious holding quite a bit of cash on occasions which probably morphs it into a lower risk/gain category, and I'm sure other growth funds have been careful riding the Trump bump.

Yup, save the hassle and fees. Just invest in an ETF.

I'm not sure I agree with your dislike of performance fees. Would you prefer Manager A who charged a 2% management fee and no performance fee or Manager B who charged no management fee and 20% of performance over a benchmark? Manager A is incentivised to gather assets regardless of performance while Manager B will probably keep the fund small so as to maximize performance. I agree this could encourage Manager B to take on more risk however if they also have their own capital at risk there is an alignment of interests which would tend to minimize this effect.

Performance fees can also drive the wrong behaviour as fund managers increase risk to chase the big returns and generate higher returns and this triggers performance fees. Performance fees mean more revenues for firm, of which portfolio managers are generally shareholders = bigger bonus for P/Mgr

Tell me who is actually the beneficiary - the client who is exposed to more risk or the P/Mgr who gets a bigger bonus for taking on more risk using client money

Do fund managers have to say if they get paid fees by the funds etc they invest in ? Financial advisers are meant to disclose if they are paid commission etc. Does the same apply to say my Kiwisaver fund manager?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.