2017 was a year in which the official cash rate remained unchanged at the record low level of 1.75%.

And that lack of change was reflected in term deposit rates as well.

However, it must also be noted that term deposit rates stayed well above the OCR level. And there was no slipping lower over the whole year.

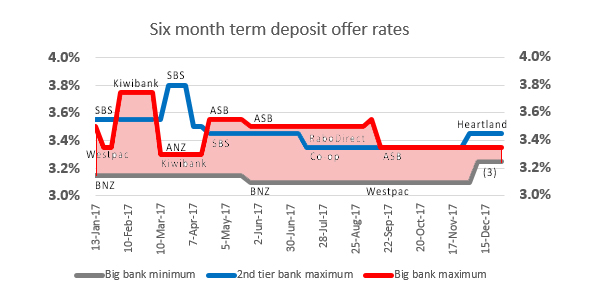

Short term rates - we will use the six month duration as the indicator - pretty much ended up where they started. The average of the five main banks started at 3.31% and ended at 3.30%. The average of the smaller banks started at 3.28% and ended at 3.25%.

But it was competitive pressures that brought the better returns; six month rates topped out at 3.75% with the Kiwibank offer in February. At the end of the year, Heartland was offering the highest rate for this term at 3.45%.

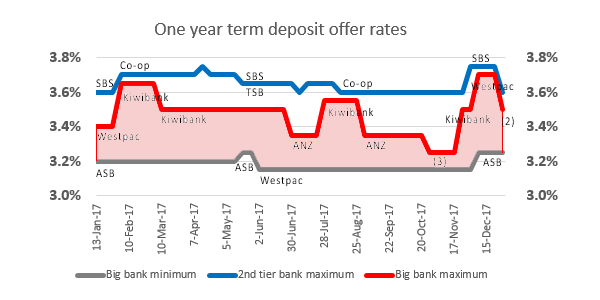

Believe it or not, the range was wider in 2017 for a one year term deposit. ASB and Westpac focused their offers elsewhere and left their one year offers low, although Westpac hit the market with a surprisingly generous (in the context of this market anyway) 3.75% for a very short burst in December. SBS Bank went one better.

Otherwise it was Kiwibank who was keenest in the one-year duration. It has to be said though that the rate premium for one year over six months was pretty minor.

Remember, sub 4% rates in the one year duration has extended now for more than two and a half years, and is starting to look more like 'normal'. Rates this low are not 'normal' however - it is the recent period that is the aberration. Savers will be asking: when will it pass?

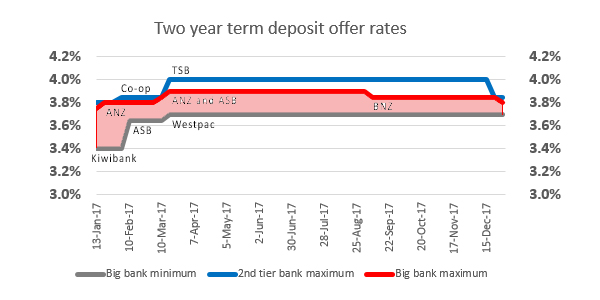

There was more on offer for a longer duration. The two year offer of 4% from TSB for most of the year stood out. And at this term, there was very little between any of the rivals, main bank or challenger bank.

For all that, term deposit savers had to cope with essentially unchanged rates from levels we saw in 2016; with the added disadvantage that bank offers changed less frequently making management of a TD portfolio just that frustratingly more difficult.

The banks put subtle pressure to go longer. The premium from one to two years averaged under +20 bps at the start of 2017, but more than doubled to over +40 bps by October, before slipping bank to just over +30 bps at the end of the year. Is +30 bps enough to entice you to lock your funds up an extra year to two years?

With the 'experts' suggesting that the OCR won't change much in 2018 either, savers may be facing another year of similar circumstances.

Our separate review of risk suggests that financial markets don't price in much risk premium for political uncertainty and change. Nor are they demanding the risk premiums they used to for the more esoteric options. But some unexpected 'jolt' may change all that, and in a hurry. Or it may not, if recent history is any guide.

You can find all current term deposit rates here and here.

Remember, "you can't go broke making a profit" so financial decisions are best made with the information and perspectives you have at the time you need to make them. Second guessing the future is like gambling and not a wise move for financial decisions.

In terms of overall rate competitiveness, here is how these banks positioned themselves on average over all of 2017, and at the end of the year for a one year term deposit:

| relative price competitiveness | 2016 average | 2017 average | year-end | |

| one year term deposit only | rate % | rate % | rate % | |

| #11 | HSBC | 2.92 | 2.90 | 2.90 |

| #10 | BNZ | 3.31 | 3.22 | 3.50 |

| #9 | ASB | 3.25 | 3.23 | 3.25 |

| #8 | Westpac | 3.28 | 3.30 | 3.50 |

| #7 | ANZ | 3.33 | 3.33 | 3.30 |

| #6 | SBS Bank | 3.36 | 3.36 | 3.60 |

| #5 | RaboDirect | 3.45 | 3.40 | 3.40 |

| #4 | Heartland Bank | 3.43 | 3.42 | 3.60 |

| #3 | TSB Bank | 3.27 | 3.46 | 3.30 |

| #2 | Kiwibank | 3.37 | 3.59 | 3.50 |

| #1 | Co-operative Bank | 3.36 | 3.63 | 3.60 |

14 Comments

I have found the BNZ to be competitive due to its rates being for 5 grand upwards and also allowing you to get the interest to be paid out monthly.

During the year the Kiwibank explicit govt guarantee has been removed, so there is no (published) security advantage there any more.

Interest rates for savers haven’t been worthwhile for so,long it isn’t funny!

Why would you want a rate of 2% by the time you are taxed???

Housing investment provides both a rental return plus capital gain.

Yes you need to manage it and repairs etc. but when you can get returns of 15% from rents and capital gains it leaves the saving with term deposits for dead!

Please provide evidence of this 15% return (and by the way the share market rose 22% last year).

Yes. FYI, the ROI after tax and fees on the Smartshares NZX50 for 2017 was approx 3.5-3.8%. Not that much better than term deposits.

Global share trusts work just fine & beat the DOW with further to run according to technical analysis reports

Auckland property in limbo overall but Auckland central doing fine

2018 looks ever likely to provide the catalyst for another GFC but who knows

Not sure where you've got those returns from - smartshares website reports ~20% annual returns as of the end of November, and there were additional gains after that.

http://smartshares.co.nz/types-of-funds/smartlarge/fnz

https://www.nzx.com/instruments/FNZ

My guess is that he was looking at the after tax yield on the reported dividends, and kinda forgot to include any of the capitol gains that occurred. Amazing as to how uninformed some people remain, despite the relative ease of using google or other search engines.

Time for Winston to introduce attractively pegged Govt Bonds for seniors. Keep the funds for NZ, have them available for the government to use instead of the dominating all powerful banks. Flow on after Kiwi Saver etc. Crackers!

Cannot dispute the reasoning of that obviously. Just wish though “generally” carried with it fiduciary disciplines that prevented wholesale blow outs by govts such as in recent times, headquarters & trappings for instance Ministry of Health, MBIE.

Kiwibonds are already available. 2.25% interest paid quarterly. Whats the problem?

Seniors already have a pretty good run at it with Super and other benefits – albeit their nest egg is sadly just a bunch of feathers at current rates.

I wonder just who are the bigger mugs in all of this mess right now – savers and their somewhat pitiful (and that’s before tax) rates of return or those buying into rather over-heated asset classes which may well face a nasty painful cooling process in the future.

So, unless have we have completely done away with the concept of economic cycles there is much more to be played out.

Though to be fair – over the past few years it certainly has been buyers / investors / speculators (1) savers (0).

https://www.cnbc.com/2018/01/02/markets-testing-fed-as-the-dollar-falls…

I'd love the US Fed and ECB to get into some sort of rate hike competition.

Then NZD falls.

OCR needs to go up then.

Dreams are free.

Retirees are just spending their capital/savings instead of trying to eke out their 3% interest return less tax.

Add to the low interest earnings, more retirees are reaching 65 still with a mortgage.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.