After years of discussion about preventing financial advisers on commission from providing conflicted advice, the Government has released a detailed proposal on exactly how it would like advisers to be more transparent.

The Ministry of Business Innovation and Employment (MBIE) has released a discussion document outlining what information it wants advisers to disclose, and how it wants them to disclose it.

The proposed regulations, which the public have until May 25 to provide feedback on, support the Financial Services Legislation Amendment Bill currently before Parliament.

The Labour-led Government has adopted the previous government’s view that imposing stronger disclosure requirements is the best way of “overcoming information asymmetries and improving transparency of, and confidence in, financial advice”, as opposed to capping or banning commissions as UK and Australian authorities have done.

MBIE suggests advisers make the existence of any commissions, incentives or conflicts of interest public from the get-go; providing clients more detailed information further down the track.

What this would actually look like

A firm might stipulate on its website that its advisers receive commission payments.

When an adviser engages with a prospective client and finds out the “nature and scope” of services they’re after, they’d be required to detail any commissions or incentives.

For example, explain that if the client chooses to take out insurance from Insurer A, the adviser would receive a commission of 200% of the first year premium, whereas if the client goes for Insurer B, they would receive a commission of 150% of the first year premium followed by annual commission of 5% of the premium.

If the client progresses things and the adviser recommends they go with Insurer A, the adviser would have to confirm they would receive that 200% commission. They would also have to detail things like if the they write X number more policies with Insurer A that quarter, they would receive free tickets to the annual conference in Hawaii.

At this point the adviser would also have to disclose information like a requirement for the client to pay them for any lost commission should they cancel the policy within the first three years.

Striking the right balance

In the discussion paper MBIE asks submitters to consider how prescriptive regulations should be.

Its view is that “regulations set out what information needs to be disclosed at certain points in the financial advice process, but provide flexibility in terms of precisely how this information is provided”.

MBIE also says: “To reduce the likelihood of disclosure becoming overly complex, we think that only those commissions and incentives which might be perceived to materially influence the financial advice should be disclosed.”

While it provides detailed case studies of the disclosures that would have to be made in different scenarios, it doesn’t define what "material" is.

A staged approach for other disclosures

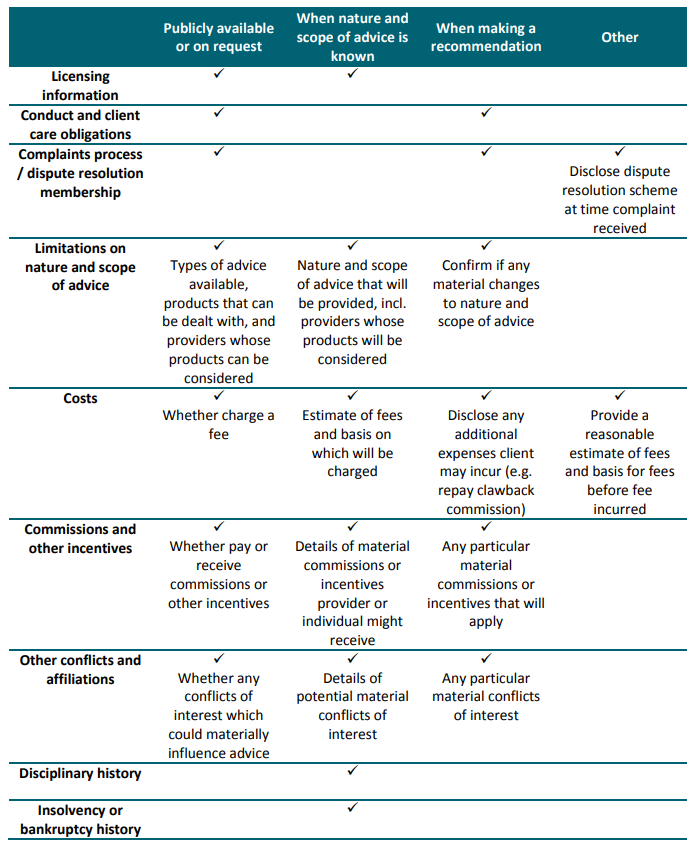

The discussion paper goes beyond commissions. It details the other disclosures MBIE proposes advisers make at different stages of the advice process.

It says firms/advisers should publicly provide a “general description of the limitations in the nature and scope of the advice that can be given”.

For example, on their website they say they only weigh up products from Insurers A, B, C and D.

Then when they find out what sort of service a client is after, they should make clear which insurers they will consider in their assessment. IE Only Insurers A and B, as Insurers C and D don’t provide the type of insurance the client is after.

MBIE also takes this staged approach to proposing how advisers disclose information about the fees they charge, any relevant insolvency, bankruptcy or disciplinary history they have, and the dispute resolution scheme of which they are a member.

Here’s a summary of its proposal:

Additional options

MBIE is also considering the following:

- Requiring advisers to provide clients with a prescribed notification, warning them of the risks of replacing financial products. IE, that they won't be covered for a pre-existing medical condition they are currently covered for if they change insurers.

- Requiring advisers to use a set template to detail what disclosures clients can expect them to make through the advice process.

- Introducing separate requirements for when advice is given via a robo-advice platform or over the phone. For example, requiring financial advice providers to disclose how a robo-advice platform works. IE that the advice is automatically generated by an algorithm based on information provided by the consumer.

- Requiring any disclosures made verbally to be supported in writing.

19 Comments

Only question you need to ask your financial adviser is "If you are so good at this, why are you still working?"

But seriously, looking at the above I see one major issue with the type of disclosure they are suggesting.A lot of "Clients" are now likely to make decisions based solely on the Adviser getting the lowest commission, rather than what is best for them (the client).

Then those clients are muppets.

I'm glad they are making this transparent. If the adviser can't justify their advice past the incentives they are getting then look elsewhere.

Yes, they are muppets.

Point is disclosure is not the answer. No commissions is the answer.

Like most things these days, we refuse to treat the problem, instead focusing on the symptoms.

How would getting rid of commissions improve access to professional and independent financial advice for New Zealanders?

It removes the potential bias/conflict of interest with regards to the advice.

If the Adviser gets paid the same, regardless of the product they sell. Then they are more likely to sell you the right one, rather than the one that earns them the most.

At the moment they clip the ticket everywhere.

% of your capital invested (i.e. doesn't matter if they win/lose you money, they still get paid)

Annual fees (Fair enough)

Commission on products sold. (wonder what they are going to sell you)

Really, they should only receive an annual fee, and a percentage of the returns (I.e. incentivise them to make money/care for the customer)

At the moment the majority of financial advice is provided by vertically integrated sales organizations (banks). The difference between them and independent advisers is that advisers are personally liable for the advice provided to clients. If you go to a QFE adviser (call centre staff and mobile mortgage manager for lending) there is no liability and no requirement to even provide advice - they are there to cross-sell you products from one financial service provider. In the case of QFE advisers it doesn't matter if the deal you're being offered is the best deal or the worst deal in the market - it's the only deal they're able to offer.

If a financial adviser offers you only the product which gives the best commission then they've offered you the exact same advice you get from a bank. This doesn't happen though as financial advisers rely on their reputation and are required to offer advice, not sales.

Your original post mentioned getting rid of commissions as a solution to this issue. This would obviously mean that the majority of independent advisers would exit the industry and New Zealanders would need to rely on bank sales staff with less knowledge to provide them with advice.

So how to remove conflicts of interest? More streamlined commissions would be a start - try convincing the banks of that though. In NZ they've moved to longer clawback periods and re-introduced trail for mortgages to ensure advisers keep clients on their books for longer. Some have minimum conversion rates and pay bonuses to advisers who write the most volumes with them - none of which is in the clients best interest.

In Aussie they're talking about removing trail commissions which would encourage brokers to churn clients once the clawback period ends.

What to do then? A client first approach should be the focus. Not a profit first approach based on protecting revenue for banks and legislation with heavy influence from lobbyists.

YHL,

I spent over 30 years in financial services in the UK.,before retiring in 2002. Before 1986,it was the Wild West and not dissimilar to NZ now. Our firm,in which I was a partner,moved first to taking no initial commission and only a trail commission-thus cutting the initial cost to the client,while helping our long-term cash flow. Then,we began to offer a fee based service and this grew steadily.

Now,the UK has banned commissions and overall,I believe that this has helped make the industry more professional. I had to sit written examinations(not multiple choice questions) in the mid 90s,though I already had professional qualifications. My old firm(now limited) has continued to thrive.

It is quite simple,commissions distort advice,but sadly,it is clear that successive NZ governments are not prepared to take any serious steps to sort the industry out.Consumers will continue to be sold policies,principally on the basis of the commission they generate.personally,I wouldn't touch a commission based salesman(they are not advisers)

DYOR.Costs nothing except time.

Brilliant, the coalition of losers now meddling in another business.

Best they concentrate on their own business first, in trying to make the country run successfully without worrying about poking their noses in someone’s else!

Classic!

Eh?

"The Labour-led Government has adopted the previous government’s view that imposing stronger disclosure requirements is the best way of “overcoming information asymmetries and improving transparency of, and confidence in, financial advice”, as opposed to capping or banning commissions as UK and Australian authorities have done"

For the hard of thinking, pertinent words in that sentence are "has adopted the previous government's view"

Yes, but you forget one thing: when National does it it's good and proper; when Labour does it, it's evil communism.

Surely COL or coalition of losers refers to property speculators? I cannot think of a better fit!

I am not a flippen speculator but a very successful property investor, that is doing great social work by providing shelter

What a load of C***. English is not my first language, but I am pretty sure social work has different meaning.

The Financial Services Legislation Amendment Bill was introduced by the National-led Government. In fact it had been on track to being passed before the election.

If you think it is heavy-handed, the UK and Australia have gone even further than NZ is in reforming their financial advice industries.

This is despite the Financial Markets Authority and consultancy Melville Jessup Weaver being among those who have done reports in recent years showing how the current system, which includes commission payments, isn't protecting consumers.

I suggest trying to understand an issue before making polarising, ideological generalisations about it THE MAN 2.

Here are some stories we have done on commissions in the past.

Well aware of that but COL needs to concentrate on their own stuff at the moment as they are a total rabble

If National do something they are acting okay but if Labour do the same thing they are a bunch of losers.Says it all really.

A few years back we where going to harmonise our regulation with Australia (APRA?) Seeing as Australia has very tight rules around disclosure, is well resourced to manage emerging compliance issues and many of New Zealand financial institutions are subsidiaries of Australian patent companies it would make sense in a way.

What's wrong with commissions? Plenty of industries operate successfully on commissions. How about we start looking at the banks?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.