The Minister of Commerce and Consumer Affairs Kris Faafoi says he is establishing new powers allowing him to potentially regulate new credit products like buy now pay later as they come onto the market.

Companies offering consumers buy now pay later services have been growing rapidly in both Australia and New Zealand. They allow people to buy products and pay for them later in instalments. And while they don’t charge interest rates, they often charge penalty fees for the likes of late payments.

Faafoi notes the Government looked into these payment methods as part of last year's review of the Credit Contracts and Consumer Finance Act (CCCFA), but the Ministry of Business, Innovation and Employment (MBIE) found no evidence as yet of serious harm.

"However, I am creating a new regulation-making power, which can bring new products such as these under the Credit Contracts and Consumer Finance Act, if needed in future,” Faafoi says.

“I’m aware of new types of post-purchase payment methods such as Afterpay, where goods are received upfront and paid for in instalments without incurring interest. I would recommend to borrowers that they check the conditions of these products before using them, as default fees can be charged if they fail to pay any instalments or pay them late and these can be considerable. Any goods purchased have the usual consumer protections under the Fair Trading Act.”

A Commerce Commission spokesperson says it is also aware of the growth of such buy now pay later schemes in New Zealand.

“Most of these products are not consumer credit contracts and providers are not subject to the primary consumer protection provisions of the CCCFA. There is potential for these transactions to cause consumer harm and we are aware of the report recently completed by Australian Securities and Investments Commission (ASIC).”

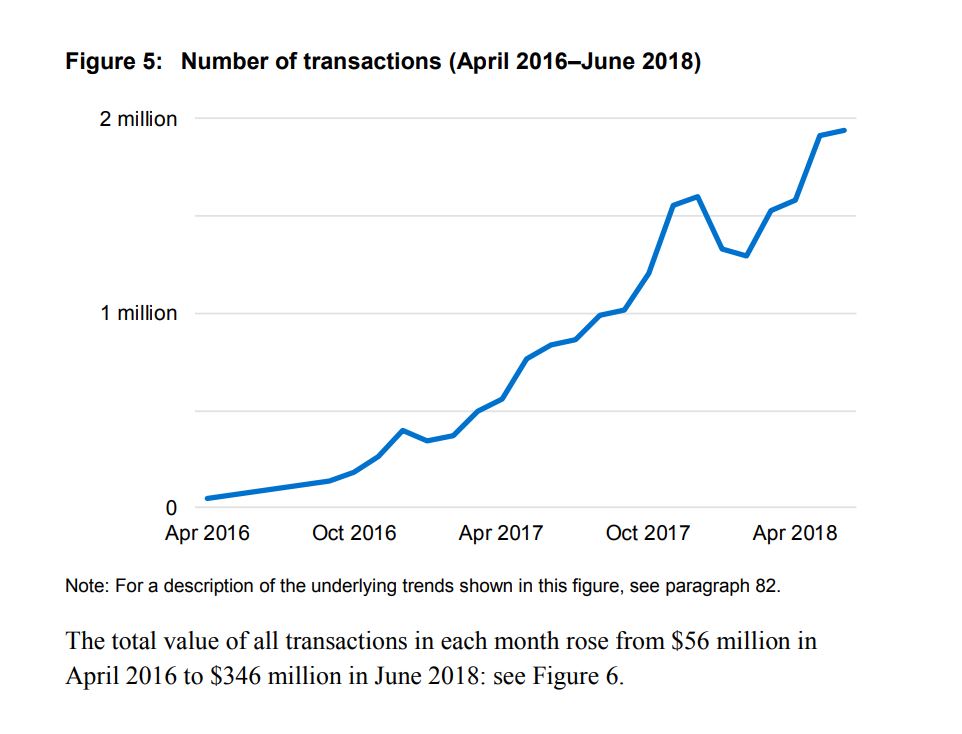

In November last year ASIC issued a report looking at the buy now pay later providers across the Tasman.

The review found the providers were influencing the spending habits of consumers, and in particular, younger people.The commission revealed that Australian consumers using buy now ay later services had increased five-fold from 400,000 customers in 2015-2016 to two million in 2017-2018. While the number of transactions had increased from about 50,000 in April 2016 to 1.9 million in June 2018. As of June 30 last year Australians owed A$903 million of outstanding buy now pay later debts.

In October MBIE issued its Regulatory Impact Statement alongside the Government's proposed changes to the CCCFA. It highlighted the growth of the interest free buy now pay later providers, including Afterpay, PartPay, Laybuy and OxiPay.

But MBIE said that the fledgling industry wouldn’t come under the regulatory control of the government’s amendments to the CCCFA.

“A number of new products have been introduced into the credit markets in recent years that have features of consumer credit contracts but fall outside the strict definition in the CCCFA," MBIE said.

"These include interest-free ‘buy now pay later’ products such as Afterpay, PartPay, Laybuy and Oxipay. Consumer advocates and some lenders have raised concerns about these products, although there is very limited evidence of harm from them to date. We have not considered bringing them within scope of the CCCFA at this time, however this could be reconsidered if variants of these products emerged that were shown to cause consumer harm."

Rapid rise: Australian Securities and Investments Commission graph showing the exponential growth of buy now pay later transactions in Australia since 2016.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

14 Comments

I have known a few of my friends/colleagues that started off buying 1 thing on these system, got the instant gratification and now have 3-4 purchases over the past 6 months that they are paying off. While I understand that this does solve a niche market, overall I think its a millennials + financial illiterates trap.

I do this for appliances. 60 months interest free for a fridge. Cash price was only 2% lower. Pay off to avoid interest.

I don't dispute your statement; yes I have seen such deals advertised plenty of times including for far more expensive items such as new cars.

However, it is interesting how a retailer in your case can essentially offer credit - with all the risk factors associated with offering credit and especially with a rapidly depreciating item - over a 5 year period for 2% which probably works out at an effective rate of about 0.7%pa.

For me, the "If it is too good to be true, it probably isn't" alarm is set off.

The obvious questions

- Was there any booking or credit fee?

- Was an "extended warranty" mandatory?

- Where there any other additional costs including delivery fees?

P8 - no real alarms here.

GE Card is $60PA.

No extended warranty.

Delivery was $80, incl installation and take away cardboard/wrapping.

I can afford to pay cash if I wanted too, but I won't miss the monthly payment of $75 or so.

Great.

We used to call it HP. No other option then. No credit cards. No bank personal lending. Taught most of us to be prudent about what we did with our money.

Sooner rather than later, we will be forced to acknowledge the limits to forward betting. This is a good move - pity there's nobody in the media capable of - or willing to - ask the hard follow-on questions. The process was just the inevitable expression of insatiable exponential growth, getting inevitably ahead of itself. The trouble is that you can only get ahead per time, once per time unit. Then you have to consolidate, or trend towards '20 years before you pay anything'.

The planet can no longer support physically-based economic growth (and most borrowing is to purchase physical parts of the planet) even real-time, let alone betting on future continuance. Sooner we retreat to real-time payment (including for housing) the better.

Nature will sort it out PDK, economic darwinism will cull out the parasites and earth will be left with only the humans most fit for survival. You can pretend idealism, but the reality is that current economic arrangements are incapable of change because exponential growth is also a law of nature.

This tone is getting a bit extreme - ranting like you're superior to other people? Unsure if you're being sarcastic or not? I hope so.

In what way extreme? on the probability that some can see us going extinct as a species? If "superior" is this ability to see and warn, I' m all for some superiority over stupidity every time.

Haha you need to be certain that its not your ego speaking which is what a lot of this thread appearst to be.

The last I recall, a certain Austrian/German decided he was superior as well and need to eliminate parasites - things didn't work out so well..

All I"m saying is the direction skudiv is taking is a very dangerous one and it doesn't work out well for anyone involved.

You are wrong on so many levels,''

a) There is no "guarantee" like this in darwinism. The parasites know how to survive so its often the innocents that will get destroyed and not the bad guys (and girls).

b) PDK is taking about real nature, economics has nothing to do with nature with short termism.

"exponential growth is also a law of nature." now this is an interesting one though. You would think as an "intelligent" species we'd figure this out, when if fact there are too many "intelligent" humans working against this in their own short term self interest.

ergo you may well be right on this one, which means of course we go well extinct within 200 years.

While not a supporter of the current government, I applaud them on their moves regarding their moves to address long-standing and well known issues associated with those who have preyed on fellow Kiwis unfairly.

The practices of loan sharks and truck shop operators, were at best only marginally little better than dishonest con-men.

"Churning" of insurance policies by brokers has been a long established practice that has preyed on the vulnerable. I know of a working solo mother who for the security of her children, bought life insurance that she could ill-afford for the security of her children. The scum-bag agent would be around every second year over a considerable period to supposedly "up-grade" her policy. After eventually learning of the consequences of this she complained to the insurance company who dismissed her concerns.

Retailers offering "extended warranties" especially when they become mandatory and offer no more than the CGA are again little more than mafia-extortionists.

While these credit policies may be relatively new and seemingly OK, it is only going to be time before they are manipulated by scum-bags to be exploitative. Sadly these scum-bags tend to masquerade as reputable companies.

Such practices are not open and honest and contrary to having pride in being a fellow Kiwi.

I'm glad the government is taking care of the sheeple. The wolves want to slaughter the old and weak, or the young lambs. The good shepherd will fight the wolf because he also wants to slaughter the sheep, especially the prime lambs. The little sheeple are just to stupid to look after themselves.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.