The residential real estate market appears to have gone into hibernation over winter, with property website Realestate,co.nz reporting the lowest number of new listings in the month of June since it began recording the data in 2007.

Realestate.co.nz received 7545 new listings throughout the country in June, down 7.3% compared to June last year and down 16.4% compared to June 2017.

The highest number of new listings received in the month of June was in 2007 when 13,430 were received.

The downturn affected most of the country, with record low new listings for the month of June in 12 of the Realestate.co.nz's 19 sales regions - Northland, Auckland, Coromandel, Bay of Plenty, Gisborne, Taranaki, Manawatu/Whanganui, Wellington, West Coast, Central Otago/Lakes, Otago and Southland.

In the critical Auckland market, new listings in June were down 12.7% compared to June last year and down 25% compared to June 2017.

In the remaining seven regions - Waikato, Hawke's Bay, Wairarapa, Central North Island, Nelson/Bays, Marlborough and Canterbury, new listings in June were at generally low levels but not record lows.

However buyers will still have plenty of choice because although new listings were down in June, the total number of homes available for sale on Realestate.co,.nz was up compared to a year ago.

At the end of June 23,519 residential properties were available for sale on the website, up 4.0% compared to June last year

In Auckland stock levels were up 8.7% at the end of June compared to June last year.

Average asking prices were less volatile, but generally weaker, with the national average asking price dropping to $653,812 in June from $662,810 in May, putting it almost to where it was a year earlier when it was $645,113.

The all time high national average asking price was $704,002 set in October last year.

However record high asking prices were set in four regions in June - Manawatu/Whanganui, Wellington, Canterbury and Southland.

In Auckland the average asking price increased from $873,445 in May to $898,259 in June, with May and June being the only months where the average asking price has been below $900,000 since August 2016.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

110 Comments

stock up (currently listed for sale and a ship load on its way), winter in.. patience will be tested..

Listings down, stock up is a really bad outcome from a bull perspective. It means people are withholding their supply because they are pessimistic but that there is so much on the market relative to sales that inventory is still increasing.

Although the "days to sell" measure can be distorted, both the National and Auckland "days to sell 'metric have both turned up. On a 6 month rolling basis , the number of days to sell an Auckland home is now higher, than at any time other than the start of the century. The Auckland metric shows no sign of improving .

"The Auckland metric shows no sign of improving ", an ailing market cannot resurrect itself when there is more poison (debt/global downturn) than remediation (sudden surge in global sentiment)

I would like to sell one of my properties, but if I had put it on the market a few months ago it would have been the 5th place up for sale in my tiny street. So I've decided to wait them out. 3 months later those properties have either been sold or withdrawn from the market. So I'm good to go once we move into the spring selling season, maybe a bit earlier to beat the rush.

This is no fun Auckland

Where are the endless posts from the DGZ & Zachary types ?

How much equity have they lost in this depreciating market ?

So much for portfolio management

Luckily Auckland turning Asian has helped prop up the market but at huge cost overburdening local infrastructure & public services

Low New Listings are a classic symptom of a correction. To give you an example consider Auckland.

Approximately 500,000 rooftops,

2015 - 30,883 sales

2016 - 25,987 sales

2017 - 20,172 sales

2018 - 21,447 sales

That’s 98,489 sales over a 4 year period. Or nearly 20% of the total stock where owners, if they wanted to sell would be selling for less than (2016,2017,2018 purchases) or equal to (2015 purchases). Either way the likelihood is that after transaction costs to sell most won’t have enough equity to trade. Unless circumstances force a sale, these people are stuck, either through not wanting to sell at a loss, or just being stuck by their equity position. Generally very little is paid off the capital in the first 5-10 years so reality is that volumes of sales are going to be low for a very long time ahead and this is going to have an effect on credit growth at some point in the near future.

JW: You say "if they wanted to sell would be selling for less than (2016,2017,2018 purchases) or equal to (2015 purchases)" Certainly, each year there were less sales but how do you conclude that people would be selling for less (implied lower price) from your numbers? You are getting number of houses sold mixed up with sale prices, very different indeed.

What was allowing people to move before was an increase in their equity (we can talk causes of that until the cows come home, or chickens perhaps?)

Eg a FHB bought a shed for 500k in 2013. 100k deposit 400k mortgage. By 2016 shed was worth 800k, mortgage 372k, lots more equity. 428k allowed owner to trade to $1,000,000 (now has mortgage of 628k and is tapped out).

Person that bought original shed for 800k in 2016) and mortgage of 650k is likely already tapped out. They have not seen any move in price (HPI is lower) but if price has flatlined (best case) mortgage is now 615k and equity 185k not being enough to trade to 1,000,000 upsize with another 200k debt.. that and they’re tapped out anyway. Result. They don’t list again as soon as the guy did who got the boom. The guy at 1,000,000 also won’t be moving for a while

Low new listings is the result unless they want to sell for a loss but for many that will hammer the equity they have and moves up won’t be achieved by doing that. Like Ireland and many other nations before us we too have successfully hamstrung the mobility of a generation through reckless credit growth.

I think that understates the difficulties recent FHB will have trading up - as the "Equity" held in the property is often not 100% theirs. A huge proportion of FHB's have relied on third parties (parents, family members) to provide some of their deposit. In some scenarios its a gift, but often its a low interest loan.

If that equity needs to be repaid it will make it even more difficult to trade up while prices are flat/falling.

And very often it will have come from a re-mortgage of the parents family home. Where the parent will want to sell up to clear the debt before retirement, but top end sales this year have stumbled into an itsy bitsy gully.

You show me where you found the evidence that FHB try to buy 'up' within a few years... Sounds completely made up to me. Just a property bear's version of romantic fiction.

Corelogic. Average holding times attached it has gone up a bit. Remembering that that's the average and that many boomers etc have sat in the family home for decades, then the flipping merri-go-round was very popular to lower that average to 5-7 years over the last decade. No Romantic fiction, just factual data that is available to the public.

https://www.corelogic.co.nz/news/how-long-do-owners-hold-their-properti…

JW, the link that you provided shows average tenure of houses at 7.4 years, sooo that would indeed contradict your original post of Joe Average buying in 2013 then "trading up" in 2016

We are truly lost!

Many here will have parents that have lived in the same house for more than a couple of decades before they sell, so what drops the average tenure to 7 years? Yep, Lots of others moving a lot quicker than the seven year itch.

So even when confronted by facts, your own facts, you find a way to manipulate them to suit your point… we are lost indeed

Yvil, think about what an average is and then re-read this thread.

An average is what JW will quote when it suits him but if it doesn't he will say "look at the data below/above said average. (choose what's most suitable to personal opinion)

Why would they not try to trade up within a few years?

I'm currently at the age & stage where I'm able to trade up.

Most of my friends bought their first house in the past 3-4 years (following their OEs):

- They bought where they could afford in Auckland;

- Now most of them have 2 kids under 3 and they're thinking about schools;

- Their FB was in a rubbish school zone because i) schools weren't high on their priority list at the time they purchased; & ii) they just "needed" to get into the market wherever they could.

Appreciate that's anecdotal, but I don't know why it's a strange concept that a lot of FHBs would seek to trade up within 5 years out of necessity.

cmat, you're in a privileged position, being a multi millionaire

I am in a privileged position.

Multi-millionaire is a big stretch.

That doesn't mean I can't appreciate the challenges that are being faced by others, and those people being challenged will ultimately come back and bite me.

We're talking about people who are extremely well qualified professionals, on very good salaries, that can't move into family homes and send their kids to good schools.

There is a lot of talk about 'entitlement', but if these are not the people who should afford these homes, then who is and where are they going to come from??

it's not good for society.

Read "Rich dad Poor dad" you will get the answer to your question

I've read it thanks.

Suggest you read 'The Intelligent Investor' by Benjamin Graham.

Then try applying that in today's world... you'll understand why the world is riding for a fall.

Value and yield are dead concepts.

That is not a good thing.

It's hard to believe you have read "Rich dad, Poor dad" and you still ask the question:

"if these are not the people (qualified professionals) who should afford these homes, then who is and where are they going to come from??"

Read "Rich dad Poor dad"

that explains everything (eye roll)

And when you’ve read that you can move onto the Janet and John books!

Fritz, indeed it explains very well why I have done so much better out of business and property rather then my very good degree in Architecture.

(although I do realise your post was condescending)

Well it hasn't done so well the the Author. https://thecollegeinvestor.com/4726/ultimate-hypocrite-robert-kiyosaki-…

A colleague was showing me various properties they were looking to buy to "get onto the property ladder". All of them 2 bedroom. They plan to have kids in the next 5 years. The amazing thing, was looking at these properties they had all been bought and sold at least 5 times over the past 14 years. Some as often as every 2 years.

When affordability is reasonable people will obviously try and buy that dream house. When affordability is stretched, as it is now, people will settle for less due to fear of missing out.

That link is broken.

Thanks Pragmatist, what a beautiful up trending line : )

In a world where nothing else changes the median will tick up with wage inflation.

In a world with wage inflation and lowering interest rates the median will tick up a bit faster.

What the median doesn't show is that the top end of the market is collapsing.

Which is why it's a great stat for the real estate industry to quote ~ its calm and steady and naturally increases over time.

Which is why you never rely on one statistic :)

I'll help you out a bit - your figures are a tad out; CoreLogic data suggests approx. 5-10% more properties sold than your data.

Additionally, they report these sales on ~85k unique properties in the Auckland region. If your ~500k dwellings in the Auckland region is to be believed, thats only ~17% of total dwelling stock that may or may not be subject to negative equity based on this criteria. This doesn't immediately suggest a dire situation of the likes that other markets have seen...

Yes, it will have lock-in effects. However, to call this a symptom of imminent correction is jumping the gun. An imminent sign of correction arises when these people cannot service the mortgage.

I’m not talking about negative equity.. just not enough equity to trade again.

Either way the likelihood is that after transaction costs to sell most won’t have enough equity to trade.

Okay. Tomato, tomato.

Negative equity ~ 'equity to trade' (a JW original?) if you are talking about a lock in effect.

Yep, that’s why the duputy governor wants to relax LVR’s again. The lock in effect is reducing mobility and the opportunity for debt growth that the country needs to keep going.

Corelogic figures last month also talk of first home buyers making up 23% of the monthly purchases in May. Which sounds near right to me, but the loans issued to first home buyers were 2700 (RBNZ C31) or the equivalent of 38% of the 7200 transactions if one loan equates to one purchase recorded by REINZ for May. That doesn’t sound right with only 17.8% of the new debt issues at $416,666 average.

So much of the data provided by the industry has holes in it. NB Blackrock and Vanguard are major shareholders in corelogic along with other US investment houses and the banks no doubt pay for and fund a lot of the information, disclosure that corelogic release.

I have used REINZ figures for the year on year Auckland sales.

My view is that the RBNZ should get a real handle on what total household exposure is first (aggregate of loans per mortgage) against transaction levels before making a call on LVR’s as at present First Home Buyers are still able to offer themselves up for sacrifice without any further assistance from the RBNZ.

Really?

LVRs being relaxed is due to their dynamic relationships - i.e. they are symmetric in nature. If a positive impulse to house prices results in them increasing, then by symmetry they must also reduce as a result of a negative shock in order to minimise long run variance in economic outcomes. It doesn't matter if they are endogenised or, as in this case, forced exogenous. You don't get a free lunch here, Wilkes. Bascand advocates changes on the basis of this.

That C31 data doesn't sound right because you have no idea about the distribution of it. You are making assumptions based on your world view and trying to make that stick to data for which you don't know any of the distributional characteristics of. That is plain statistical bias.

Plus, the data characteristics and the periodic nature are completely different. You can't really compare sales in one month with mortgage draw downs in the same month. I would say at least quarterly data is required to make any meaningful comparisons there.

My view is that the RBNZ should get a real handle on what total household exposure is first

Again. Trust me. The RBNZ has a pretty good idea of what mortgage exposure is in New Zealand.

Look at FHB loan numbers in the C31 release data (remember FHB loans are by definition for a transaction ‘buyer’ being the operative word) then compare to REINZ transaction numbers for any month over the last several years and you will see the discrepancy for yourself.

But that's my point. You can't look at the monthly data - it's never going to correspond. You'll always be finding anomalies that disappear over longer time horizons. Show me matched quarterly series.

Do REINZ or CoreLogic define 'First Home Buyers the same as the RBNZ?

Does a "finalised offer of mortgage lending" correspond exactly with the transaction date of a property?

I doubt it. What I don't doubt is that it is a classic case of making the data fit your narrative.

Is 12 months data enough?

REINZ SALES FIGURES - C31 Number of First Home Buyer (Loans)

MAY 2019 - 7263 2760

April 2019 - 5800 2300

Mar 2019 - 6938 2457

Feb 2019 - 5954 2089

Jan 2019 - 4372 1771

Dec 2018 - 5330 2295

Nov 2018 - 7286 2599

Oct 2018 - 6791 2365

Sep 2018 - 5506 2157

Aug 2018 - 6216 2201

July 2018 - 5661 2306

Jun 2018 - 6034 2306

TOTAL - 67197 24740 (36.8%) if number of loans were a true reflection of number of purchases.

Okay.

Now tell us how the definitions of First home buyers differ between the two datasets.

One data set refers to total transactions each month across the country (REINZ). The other data set is the published data for the number of loans written to a set of buyers in the market each month (RBNZ). The REINZ are not talking about the proportion of sales to first home buyers and the RBNZ are not looking at the total number of sales being made when they publish the figures on number of first home buyer loans that the banks give them.

Therein lies the problem. No one’s been looking at the two datasets together!

They are quite different things.

Not having the equity to trade has a big impact on liquidity, which is what we're seeing now (lower sales volumes, particularly in the mid-upper price brackets where prospective purchasers are largely reliant upon prior accumulation of equity).

That lower liquidity will have to bite at some stage.

Marginal sellers will be forced into accepting lower prices and thus setting new, lower, price watermarks.

No they aren't.

Not having equity to trade (wtf that is?) is, effectively, the negative equity trap.

No. It's not.

i) Negative equity is *negative* equity.

i.e. Your bank debt is greater than the fair value of your home.

i.e. A disaster.

ii) Not having the equity to trade means your equity position limits you to the home you're currently in.

e.g. You purchased a $1m home in 2016 with $200k (20%) deposit. Since then you may have paid down some equity due to P&I payments, but the flat market means that, if you sold, transaction costs would at least take you back to square one ($200k equity).

So, your equity is *positive* (i.e. NOT *negative*) but you can not move to the next rung on the property ladder - say $1.5m for that extra bedroom / better school zone... which would require an additional $100k of equity for a 20% deposit.

JW was talking about the lock-in effect.

Both negative equity and 'tradeable equity' (wtf) has the same lock-in effect.

Thu, we are talking about the same mechanism; the inability to move as a result of a lack of usable equity.

I have tried to illustrate it as simply as I can.

Yes. And what you have described is the 'lock-in' effect, which I highlight.

What it all means is that, by and large, property owners won't sell unless they get their price. Or, put simply, when the quantity of houses demanded weakens, so too does the quantity supplied (i.e. listed for sale).

So the market is slower (with fewer listings) but prices remain steady enough - which is exactly what we've been witnessing.

Not so long ago, the DGM was trying to run the line that supply (i.e. house listings) had reached record HIGH levels in Auckland and that was a sure sign that things were bleak - but things weren't bleak at all.........

Now the DGM is trying to run the line that supply has reached record LOW levels in Auckland and that's a sure sign that things are bleak - but things aren't bleak at all.

Clearly, the DGM has got it wrong - twice!

In reality, the housing market has self-stabilising mechanisms and they're actually working pretty well - despite being tested by the boom of 2013 - 2016 (and despite the humiliation of the DGM).

TTP

"What it all means is that, by and large, property owners won't sell unless they get their price. Or, put simply, when the quantity of houses demanded weakens, so too does the quantity supplied (i.e. listed for sale)."

That is not at all how it works. People will hold off selling, but only if they believe they can get a higher price within the time-frame they need to sell. If people believe prices are going up, they may hold. If they believe prices will fall further, they may feel forced to sell.

Last time I checked their is a large demographic bulge (boomers) approaching the point they need to unlock all of that equity to fund retirement. Would they be willing to wait out a downturn? Interesting hypothetical, particularly when you consider 1/3 of homeowners over 65's still have a mortgage.

Quite right.

A lot of sellers will hold off.

BUT there will be sellers that, for whatever reason (retirement, deceased, relocation etc), need to sell.

These marginal sellers will accept lower prices, because they must given their circumstances, and end up setting lower prices in the market.

If it's anything like what I've heard from the horses' mouths (anecdotally, of course), some have removed their houses from the market because buyers are "just trying it on" and "putting in cheeky lowball offers". At least, compared to what they could have gotten pre-China capital outflows being shut down.

How dare they.

Haven't they heard that they need to offer more for houses that's just not sporting, goes against the rules of property prices only goes up. Well in NZ anyway.

The Kiwisaver statistics support the boomer need for retirement cash. In 2018 about 130,000 accounts were closed due to retirement. That figure is only for those exiting the scheme, but when you need cash, a car, or to pay down debt it's the easy option.

https://www.kiwisaver.govt.nz/statistics/annual/exiting/

Excellent point. Crux of this is that there is a big mismatch between boomers desire to sell and availability of 40-47 year olds able to afford price boomers think it is worth. Next surge in the 40-47s in Auckland is not due til 2023-25. So, prices will have to fall or transactions will crater.

And (generally speaking) those 40-47 year olds bought their first houses/started their families/paid off their student debt later in life as well, so probably have less ability to buy the boomer mansions as well.

For a home owner with small or no mortgage, the best time to trade up is in a declining market. Bring it on...great news for the financially conservative and the fhb's. Bad news for the greedy.

TTP, I think you are a bit confused. "New listings" is not the same as supply. Read the article.

"In Auckland stock levels were up 8.7% at the end of June compared to June last year."

Stock is up, despite that low number of new listings. Which means vendors have been trying to sell for a long time, with no success.

Clearly, you have got it wrong.

REA-TTP, you say "what it all means is that, by and large, property owners won't sell unless they get their price"

Property wise, I think we are entering the "denial" phase of this cycle. Over time, denial could prove costly for many when eventually owners re-list come spring. Words like "panic" have been used to describe what's occurring in Sydney and Melbourne. The thirteen stages are;

Euphoria - Complacency - Anxiety - (denial) - Panic - Capitulation - Anger - Depression - Disbelief - Hope - Optimism - Belief - Thrill

If this is "foreign" to you then you're also in denial.

Yes, great reference to the cycle words! Mostly denied nowadays unfortunately.

What sellers do not want to take on board right now is that they will have to chase market price down as in 4 months it will be lower than now.

Reality is that "investors" have gone largely and a large slab of them were illegitimate foreign buyers distorting prices and sales numbers and sale frequency. This distortion fed into asset inflation and velocity of money, which is now flagging badly, meaning less GDP growth and economic activity generally. Government and most commentators have no clue about velocity.

Take a look how much RE NZ listings for houses drop in first 3 days of a month (ie now). That is people pulling listings coming up for contract renewal.

Crux of all this is it is deflationary to the economy.

If the oldsters do not sell, then less velocity of money.

Inflation will keep falling as will interest rates.

Then, just as everyone thinks inflation is dead, it will surge due to inflation due to abysmal harvest approaching in USA and food dependency on that harvest of 15% of world population.

If the US has an abysmal harvest, then demand for our produce internationally will increase.

Inflation of import prices worldwide will follow I believe

" In reality, the housing market has self-stabilising mechanisms "

I couldnt disagree more....

In Akld new listings are falling, and stock is RISING, HPI is falling. I dont see any of that magic self stabilizing dust you speak of. looks like the pressure is rising and you can see prices dropping in most places.

The interesting thing also is that as more and more people are stuck (renting or unable to sell), economic mobility drops further and further. Which further drags economic performance and productivity. This makes the next crisis worse as the economy is less advanced and less flexible to be able to handle a down turn.

And sales in 2019 running at 20,000 pa rate.

The level of house price in NZ is set from average of 300k to 400k to 500k to 600k.

Once the level is set, there is no turning back.

"Once the level is set, there is no turning back." until it does

Expectations and reality are often two very different things if you’ve ever worked through a housing correction.

Yeah, its impossible for thing to go backward like it did in lots of other places, irrational pricing will continue forever..

LOL

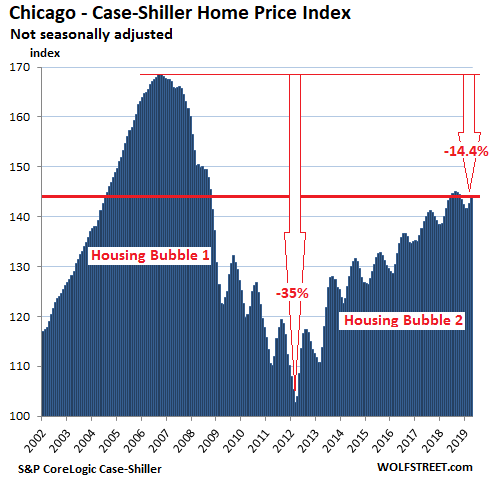

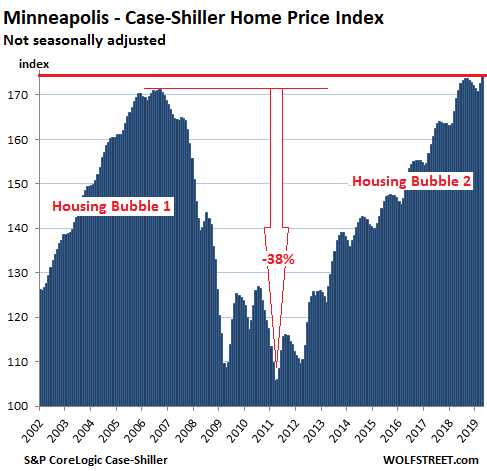

For your reference, proof that housing markets do go up AND Down.

https://wolfstreet.com/wp-content/uploads/2019/06/US-Housing-2Case-Shil…

https://wolfstreet.com/wp-content/uploads/2019/06/US-Housing-2Case-Shil…

{kind=link}

{kind=link}

proof that xingmowang has not witnessed a property downturn

What does that even mean?

House prices always go up!

...except when they don't. See https://en.wikipedia.org/wiki/Real_estate_bubble#Recent_real_estate_bub…

Yeah but some fanatics of the 'housing religion' think those kind of slumps could never happen in New Zealand.

It's a bizarre and irrational belief.

"The level of house price in NZ is set from average of 300k to 400k to 500k to 600k.

Once the level is set, there is no turning back."

Yeah, what does this even mean?. When the level is set?.

dp

https://www.youtube.com/watch?v=3dGhsRsHXP8

About "going back" lifestyle wise for women & sexually for men, Chris Rock, just watch it : )))

Great clip, it's got nothing to do with house prices though.

Yvil would no doubt argue that it somehow does ;-)

Thanks Ocelot, it was in reply to Xingmowang's post:

"Once the level is set, there is no turning back"

"chuckle"

If Auckland June listings were down 12.7% compared to June 2018 this just provides further evidence that property flipping is slowly dying a death in the city.

What's interesting to me is the quantity of new builds coming to the market. Most of them (* he said generalizing) seem to have no real outside space and look pretty cookie cutter ~ wooden frame, heat pumps, open plan kitchen and the ubiquitous grey carpet !

Will be interesting to see how these sell and at what level as there is a ton to choice right now and new places are being released like the baker putting out fresh loaves each morning.

Really, you also have to look at WHAT is listed.

Currently Auckland as about 6500 houses and townhouses listed.

About 1900 apartments.

In Hibiscus Coast there are meant to be 523 houses and townhouses OTM.

BUT 80 of them are duplicate listings on same property and a further 25% are not actually a building but the promise of one - ie house and land package etc. So, all is not what it seems.

When you deduct those falsehoods, you see that HC OTM for houses and townhouses is in fact 40% lower than it looks on surface, before we start digging. If you did same exercise for Auckland as a whole, it might be the same. Thus, there is nowhere near the "choice" that people continue to refer to.

Then, look at what is selling.

Sales are running about 25% below the first 5m of 2017, itself not a good year.

Buyers: higher the price the more buyers have exited: 43% above $2m, then 28% over $1.2m.

What this means is that buyers do not have " lots to choose from" and there are fewer buyers interested.

The parts of the market only down 7-10% on transactions are 3 beds priced $600-800k and 4 bed priced $800-1.2m, in respect to most of Auckland and Rodney.

Listings are down because people are pulling properties early due to Agents telling them the harsh truth that the market has changed and its not worth what it was 2 years ago.

Owner occupier buying and borrowing is barely moving and investors is 25% down on 2 years ago.

FHB are catching a falling knife and are borrowing far more than RBNZ figures indicate because those figures only show 1 loan and do not add up to the % of market FHB are taking now.

Mike, where are you seeing top end transaction prices in Auckland vs historic levels. Anecdotally it seems to me that perhaps we are about 2015 levels at the moment ? Any data or thoughts ? Thanks G.

That would be approximately consistent with what the HPI index suggests.

Hi

Price data would take longer than sales. However expensive stuff over 1.5m is either taking 7-8 or even 12 m to sell and amount of cut can be substantial to get a sale. Reduction in buyers up there not sunk in with many sellers yet but expect substantial adjustment in awareness in the Spring when agents restart education!

Hi Glitzy

Find me on LinkedIn to connect?

Did a post yesterday giving reasons sales and prices will go on falling for a while yet.

2003-4 Auckland sold 56,000.

This year it will be 20,000

Cycle is 18 years, so bottom nowhere near in sight - will be 2022.

Then, no increase in 40-47s to boost market until 2025 and Australian and China housing markets both due for wrenching recession, which I do not believe CCP in China can "manage".

2012-17 was an aberration. RBNZ wanted to stop it and did LVR.

Government killed it with OBB and AML. RIP I say. Just a shame all FHB after 2016 are falling into the greater fools Ponzi trap.

IMHO you use a lot of abbrevs. LMFAO.

Where do you get the idea of an 18 year cycle? Increase in 40-47s?

You mean 40 to 47 year old people? Why is that important?

"You mean 40 to 47 year old people? Why is that important?"

Maybe some weird extrapolation from incomes, cost of living etc, and he's determined this is the age most will actually be able to save a decent deposit for a credit wary bank? *shrug*

I assume 2025 is when the big demographic wave of baby boomer's children start to enter that age group, en masse

It is when Chinese and Indian immig reach age with enough income for buying

Lots of agents recog the 18 year cycle and an Aus wrote a book on it. Basically a proper pullback is 4 years peak to trough. 40-47 year olds have highest disposable incomes. In USA they peaked in 2008.

Don Brash back in 2016 "If you could hold house prices static for half a century and have nominal incomes growing at say 3 per cent, you might get back to a reasonable relationship over half a century.

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11672584

Of course 2012-2017 was an aberration and the correction has just begun. The OBB, AML, rental loss ring fencing and boomers cashing up their rental investments will accelerate the process and thats a good thing. Much better than waiting half a century.

2012 - 2017 was a smaller increase than 2002 - 2007 in % terms, but few on here seem to know this.

That is true however the relationship between house prices and household income was reasonable during that period. The same cant be said for the period 2012 - 2017.

Indeed. And peak sales in Auckland was 2003-4 at 56000. This year headed for 21000 max

With the introduction of deposit insurance along with increased discussions on negative OCR and increasing NZ Bank capital by $20 billion to guard against a one in 200 year event, is as much real as insurers contingency against losses on coastal property associated with rising sea levels. Both are significant potential threats that should be taken seriously.

First time buyers need to take these new risks into consideration and what impact it could have on property values in the near future.

Savings will provide security whereas the same can't be said after buying into these still toppy valuations, borrowing 1/2 million over 30-years and raiding the Kiwisaver. There's no hurry.

Reality is that house market has fallen and is falling :)

Like it or not, as anyone trying to prove otherwise is actually trying to convince oneself of otherwise as even they knows that the market is gone for a toss for few years and are actually not convincing others but themselves.

Reality is that house values are up and will keep going up :)

Like it or not, as anyone trying to prove otherwise is actually trying to convince oneself of otherwise as even they knows that the market is going up for few years and are actually not convincing others but themselves.

Wow, I can make wild unsubstantiated posts too, it must real LOL

Good reflecting back mate

We could be more specific and say Auckland is falling with the top end leading the way. The ripple to smaller towns (bar Wellington) hasn't yet really started yet.

Some interesting points here. I'm personally watching the market very closely as after 13 years in the UK looking at moving back to NZ with family in tow with Auckland the likely location.

You will like it back here. The property is like the UK in 1985 ;)

My brother is a builder and quantity surveyor and would be checking out any property I would consider buying. I would be in no rush as the market will fall further.

Really good quality cardboard houses here in New Zealand

Agreed build quality, insulation lack of central heating is shocking in NZ. I'm not naive lived in NZ for 29 yrs owned 2 rentals and have brought 4 properties and sold 3 in UK since I've been here so my eyes are wide open.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.