Although the December sales for Auckland realtor Barfoot & Thompson came in substantially above those for the same month a year ago, it has been a challenging year for the market leader in the Queen City.

They sold 779 properties in December, taking the 2019 total to 9323. That compares with just 504 sold in December 2018 but 9659 in all of 2018. That is an annual dip of -4.4%.

Prices dipped too. Their median December 2019 price was $865,000, down -1.1% from the same month a year ago when it was $875,000. Their average December 2019 price was $949,100 and that was down from $950,300 in December 2018.

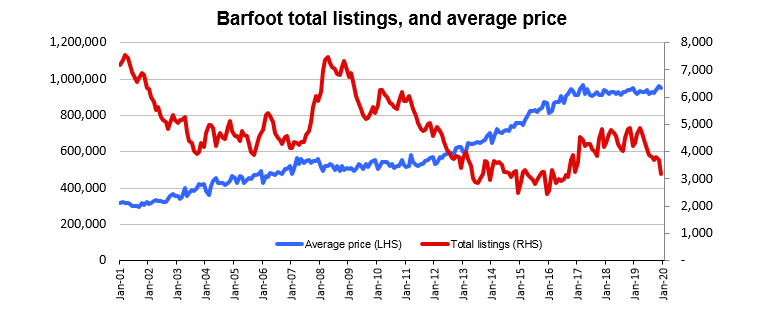

This comes as listings in their network fell by more than -1000 from 4194 at the start of the year to 3191 at the end. It seems tight supply didn't raise prices in Auckland.

If there is a silver lining it is that the stable median prices from January to October of $831,000 jumped to $891,000 in November and only fell back to $865,000 in December. Perhaps the market is turning, although it would be a brave prediction to make on so little and spotty evidence.

Average and median prices have been stuck at unchanged levels now for three full years. And that is despite the shortage of listings for sale.

Their average 2019 drop-out rate was just under 13% whereas their average in 2018 was just over 13%. Low listing levels didn't improve sales success. You need to go back to the 2010 to 2012 period to find average drop-out rates down to about 10%. (The dropout rate measures how many listings didn't sell at all and were withdrawn at the agency. It is a crude metric however.)

Like all other Auckland realtors they will be hoping the new year brings more sellers into the market, improving the options for buyers who have been holding back. Listing portal data doesn't indicate that yet.

Here is what Barfoot & Thompson say about the December sales result. It is more upbeat than this article.

Barfoot Auckland

Select chart tabs

32 Comments

Apologies. Comments were unintentionally closed earlier. They are open now.

And we all thought Interest .co had a new years resolution of no comments on housing articles.

Great idea, let the numbers do the talking.

I think that’s a good idea

Don’t speak the dirty word housing

Sums up the situation nicely: “Average and median prices have been stuck at unchanged levels now for three full years. And that is despite the shortage of listings for sale.”

The discussion centres on: why?

Simple answer: the market is overvalued, and there’s perhaps not quite the shortage that continues to be reported.

VOR

. . . and over that three years of stability we have had continued postings regarding imminent a crash or at least slowly leaking bubble.

If the building boom continues at the pace it is but the demand is not really there, a decline in prices could still happen (to meet demand at a lower price level). We’ll have to see. Certainly I don’t see a reason for prices to go up much in Auckland, and wherever else there’s a boom in building without much demand at the asking prices. I own property outright in Auckland so happy to see prices go up more for my own situation. Just don’t see it happening much for years, but will be fine in the long run.

VOR

I agree that we are unlikely to see prices increase substantially in Auckland.

With immigration continuing at 55,000pa, and new house builds somewhere around the 14,000pa, and a lack of any seemingly effective government policy on either immigration or housing to address these, I don't see current housing shortage being significantly addressed anytime soon.

As the current drivers are still present and seem fairly consistent, my feeling that economic factors and RBNZ actions will have greater influence on the Auckland housing market.

My feeling is that RBNZ will be reluctant to make any further cuts to OCR as a figure of or less than 0% (while possible) is a level that has lots of associated reactions and implications. What little "powder" they have left they will be wanting to maintain for a relatively dire situation. The NZ economy and exporters seem to be trucking along OK so no apparent need for any cut currently.

As for LVRs; RBNZ won't want to be see Auckland prices rising rapidly with the associated economic stability risks. Orr has previously commented that he would be comfortable with 2 to 3% increases. Anymore and I think that we could see a tightening of LVRs. Given the current state of both the Auckland and the provincial markets, I see more likelihood of tightening rather than loosening of LVRs over the next year. A regional variation of LVRs - as previously - is always possible.

Note that RBNZ has no mandate regarding housing affordability - just economic stability.

In the event of any significant impact from a global event affecting the wider economy and housing, I would see RBNZ more likely looking at loosening LVRs over cutting OCR further.

Bottom line; despite affordability issues, I see the likelihood of Auckland market as continuing to be firm with ideally some possible growth of 2 to 3%. The housing boom from 2012 to 2017 will go down in economic folklore.

I think an economic and or political shock from outside NZ is quite likely over the short to medium term, as probabilities go. To me, a likely scenario is that sharemarkets take quite a big hit, after a very long bull run (over 10 years now). Predicting exactly when is impossible, but it is very likely. The question is, what would the RBNZ do in that situation, as it would start to impact the overall economy, including the property market? There’s very little commentary on this. People have forgotten about the impact of the sharemarket.

VOR

I agree with your sentiment.

The share market has had a great run fueled by cheap money; it also seems that central banks are continuing to provide ongoing cheaper money. By historical measures the share market is over heated but then that cheap money has got to go somewhere.

Had a quick look at the NZSX50 this morning; over the past six months it has gone up 9.6% so locally money will - if not already - be moving from cash, term deposits and conservative/cash KiwiSavers to exposure to shares and providing support for the share market.

One good thing about property market over the share market - it tends to be a lot less volatile in negative periods,

Yes, and the S&P 500 has had a 373% gain since March 2009, and 30% in the past year. The decade run is bigger in percentage terms than from 1990-2000, and way bigger than the run leading to the GFC. A significant drawdown seems increasingly likely, and NZ would follow. No doubt central banks would lower already very low rates, and provide other stimulus.

VOR

Again a valid point and one I actually agree with. Yes, there is some - note "some" - degree of heightened risk.

For this reason I am hedging my bets. As I am able to access my KiwiSaver funds which I intend doing so progressively over the next few years (travel, new car etc), given the situation you describe, I am currently comfortable in a moderate fund with 35% exposure to equities.

Personally, for my situation this risk level is fine for me given that term deposit rates and conservative/cash KiwiSaver are returning next to nothing. I would not be looking at at a KiwiSaver growth fund in my situation for the risk you describe.

....Aaaand the gold price is spiking again on the predictable idiocy of war. Gold has been a good hedge for over a year now. It may only be getting started.

Gold has the longest proven history of any hedge so its no surprise despite its detracters

No one can deny that last 3 or 4 months have been very positive and house price specially in Auckland has jumped liked never before (Never before as have have from already high price) specially in high end properties. It is surprising but truth.

If this trend continues, FHB can say good bye to their dream of owning a house in Auckland - where they work but YES can own pigeon hole apartments for a premium.

All the data/ article published today, is of past perfomance which has been very good and can be felt in the market besides the data that supports the rising housing market not only in Auckland but also in Canada and Australia . What has to be watched is, will this trend which started from September/October continue or fizzilen out (See no reason of it fizzling out just as was seeing no reason of boom in October but it happened). Only factor was low interest rate but now with Low interest rate being the norm, does 0.2% or 0.4% fall justify this quantum of jump in house price and what happens to law of diminishing return.

So is wait and watch from here on.

House price should stable, if not fall for FHB (Housing market has been turned into casino by all government) but should jump/move up for tons of first time mom and dad new builders/property developers who have entered the market now for quick buck (many switiching over their business) - if have deep pockets would be fine but many who are entering with intenetion to sell as soon as get approval at plan level is worrying and for that the housing pozi has to continue.

Reversion to the historical mean can always been counted on (and overshooting it in both directions). The present situation is not a new normal - for high price-to-income, or ultra low interest rates.

The present situation is not a new normal - for high price-to-income, or ultra low interest rates.

The current situation is unprecedented in economic history. The ruling elite is wholly focused on the "new normal" because they're terrified of what will occur if it were any different. Any kind of reversion to mean spells wholesale destruction of people's wealth and self worth.

Only those with lots of debt relative with insecure income. Secure income, medical and utilities.

If New Zealand, Canada, and Australia saw a correlated mini boom that would be worthy of analysis.

You mean like over the past decade in these countries? It’s already happened, without the decline many other markets had during the GFC.

Yep this article highlighted the situation very accurately: Better Dwelling: China’s Massive International Real Estate Buying Spree Is Officially Dead.

https://betterdwelling.com/chinas-massive-international-real-estate-buy…

Indeed. Quite different markets but all negatively impacted at the same time, from the domestic tax paying potential owners perspective. Flip side is a massive boon for domestic property owners with debt leverage not interested in yield. Those two camps cover more that half the post on here.

Comparing Auckland to Toronto Vancouver or Montreal is laughable

For example the 401 freeway take a look online

Canada is the 2nd largest country with a pop 7X NZs

We take 75% of what Canada exports here into USA

NZ is perhaps comparable to the other Hicksville AUS

Listings heading towards zero. I wonder how long it will be before someone buys the last house? And who?

Could be April or May, but who knows, could be as early as the end of summer.

Valuations are going to go sky, propety the next bitcoin. Better get in quick or be locked out forever.

Well it just goes to show how much Auckland was so very dependent on all that lovely dodgy overseas money. Still mortgage rates will probably slip lower to keep the property ponzi scheme going for the next year or so.

Plenty of cities around the world but notably in Europe have seen price rises just like Auckland. Some of them even with falling populations. Within our own country, I would point to Dunedin and its soaring prices. The major factor in all this has always been central bank policy, not foreign money.

"Europe have seen price rises just like Auckland" Europe is still recovering from the 2008 Global Financial Crisis where most of their housing markets have been a lot more restrained in price rises since then. Dunedin is only soaring since mortgage rates dropped allowing people to borrow more. Ask yourself this; Have you seen any major business investment in Dunedin recently, do you have your own Silicon Valley? If the answer is no, then it's just a credit bubble.

"Lovely overseas money" gone

Notice that Barfoot's top 30 sales people from 5 years ago have all gone too

https://www.barfoot.co.nz/find-us/find-a-salesperson

Not one of them still around

Fair-weather friends weren't they

Barfoots showing median going nowhere for 3 years. Contradicting REINZ a bit. Notice 2019 sales increases only in periphery if Auckland where new cheaper builds going in. Economic shock to come will give market push to bottom in 2021

Agreed "Economic shock" looks more than a likely an out come especially for Auckland. I keep asking myself, how long can the price growth last for NZ without real business investment and wages increase? We've even out stripped London in overinflated property markets where at least their wages are much higher and better able to support property prices. Currently the London average property price is £458,363 ($902,970) and Auckland's city average based on the recent QV data is: $1,244,959 (£632,265). And we have much smaller wages, crazy isn't it.

Here's a link to the UK's average house prices for Q4 2019: https://www.thisismoney.co.uk/money/mortgageshome/article-7864225/House…

How can it be a minus in Auckland property values ?

I was told here property only goes up up up

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.