The housing market remained robust in February, with the Real Estate Institute of New Zealand's House Price Index (HPI) showing a significant jump in prices in most parts of the country..

The HPI allows for differences in the composition of sales by property type from month to month, so is a more reliable indicator of overall movements in residential property prices than averages or medians, although the REINZ's median prices in February were also firm.

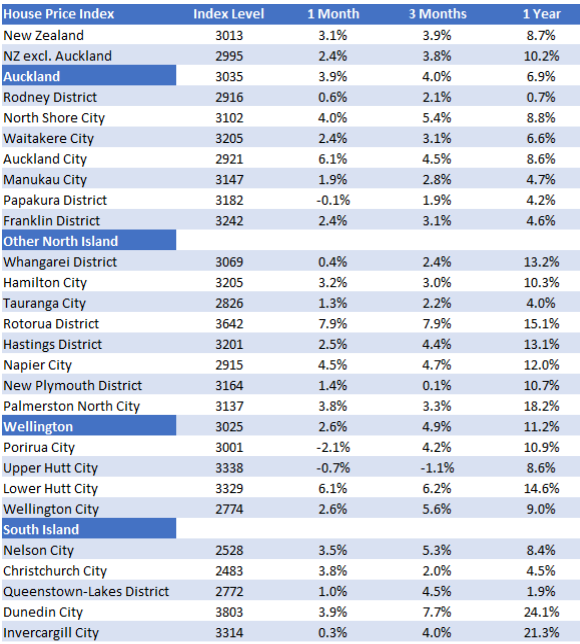

The HPI for the whole of New Zealand was up 3.1% in February compared to January, which means it's now 8.7% ahead of where it was 12 months ago.

The figures also suggest that the Auckland market has shaken off its recent lethargy, with the HPI for Auckland up 3.9% in February compared to January, while the HPI for the rest of the country excluding Auckland was up just 2.4%.

The strongest price gains in Auckland were in its two most expensive districts, the North Shore where the HPI was up 4.0% compared to January, and Auckland Central which includes upmarket suburbs such as Remuera, St Heliers, Parnell, Epsom, Mt Eden, Ponsonby, and Herne Bay, where the HPI was up 6.1% compared to January.

The price rise was more modest in the more affordable districts, with the HPI up 1.9% in Manukau in February, while Papakura was the only district in Auckland to record a decline with the HPI down just 0.1%.

There were also very strong price rises in Rotorua where the HPI was up 7.9% in February compared to January, and in Lower Hutt where it was up 6.1%.

Apart from Papakura, the only districts to records falls in the HPI in February compared to January were Porirua down 2.1%, and Upper Hutt down 0.7%. (See the HPI movements for all districts in the table below).

However the world's financial markets are changing rapidly and it would be naive to think that the property market will remain immune to a significant economic downturn.

It is still too early to say how badly it may be affected but for the time being at least, the current data suggests that while the share market may be feeling the ill-effects of coronavirus, the property market remains in rude good health.

The comment stream on this story is now closed.

REINZ House Price Index - February 2020

75 Comments

Gosh, these latest house price increases are nothing short of remarkable - even Auckland!

But, as I've been cautioning for several weeks now, the housing market does seem likely to slow down a bit on the back of the dastardly Covid-19 virus.

I reckon we're now in for a period of uncertainty - of unknown length......

Health (personal and public) will be people's main concern - with housing taking a back seat for a while.

Those whose asset portfolios are weighted toward property and away from shares will be feeling relieved........

Let's hope the banks won't be tested too much - because that's where my (meagre) savings are deposited. (-;

TTP

Doesn't surprise me TTP that you are overweight in NZD. Good luck to you.

TTP, you've been pretty bullish on NZ property during the past year and before. The virus, and the crash in oil, are only catalysts for what's now going on in international markets, not the cause. Amazing that the Fed has been injecting hundreds of billions into the system to try to keep it afloat and money flowing, and they'll do a lot more. But it's not working now. Watch for a likely credit crunch. I think a reckoning is coming for the NZ property market, much bigger than you think...

1500 billion actually. The house always wins.

It seems unlikely to me that house prices will continue to rise through all this uncertainty. The big difference is, we won't know for a month or two (or longer) whether property is affected. A fantastic asset class for those who want to stick their fingers in their ears and say 'la-la-la' and hope that things blow over.

"Unlikely"

At least you arent one of those who stubbornly claims the sky is falling. There is hope

If you could stop claiming to be Nostradamus that would be really great.

You reckon we're in for a period of uncertainty?

You reckon?

Well done you, takes a real savant to make that prediction.

You've spent years discounting global macro risks.

Here they are, in a big way, all at once.

And even now you still think this thing will be contained to liquid markets and your tiny little illiquid leveraged market will get away unscathed.

You're deluded.

Most people in NZ are unaware of the financial linkages of global macro developments on NZ and the NZ residential real estate market.

Given that property prices have been a lot less volatile (and mainly going in one direction for the last 50 years) compared to share prices, many property buyers remain confident that property prices will not fall by much. Many have taken on high levels of debt to finance their property purchases, and may be vulnerable to a credit crunch or recession.

cmat

"If you could stop claiming to be Nostradamus that would be really great."

A little bit of bitterness there cmat?

So what is it that you want? Do you want this site simply left to those who have made the majority of posts claiming bubble burst over the past year.

Land in good locations appears to be replacing Gold as the new inflation hedge.

No, I really doubt this be the case in the coming year. It'll be no hedge if you've bought in the past 5 or more years in NZ. Perhaps in a couple of years though, they'll be some bargains!

QE releases money into the world effectively devaluing money, making things look more expensive if you express their value using money. When money is rapidly losing value you don’t really want to hold a lot of it, so you look for hedge options :)

You do, but the optionality of cash is also important in times when asset prices are dropping significantly. If the share market drops 40-50% for instance, and or the other assets drop to bargain levels, cash is what you want! Buy low sell high is a saying for a reason, but so few people actually do that.

Good point, but is the option of cash worth taking a hit on your real estate if you can not get a good price for it? Unlikely. You may be able to get a valuation now (as a hedge against them going lower in the next few months) and release equity via a loan (revolving credit?) to buy other asset classes whilst they are down.

Add to your debt in an economy with a massive debt problem... yeah not me mate.

It is no longer about inflation hedges or growth. The game has been about capital preservation for a while now as in how do you limit your losses?

Gold is not insurance against deflation, neither are debt-backed property prices. The only protection against deflation is the (US) dollar as it goes up in value. That's why you don't want a negative amount (debt) of it.

I am surprised to observe that so many have issues with grasping these financial definitions. Isn't investing taught in NZ schools or something?

Insufficient factorial analysis has been applied to the data in these make-news pieces to make it a valuable tool for the likes of myself. Surely REINZ can give us more detailed analyses as to types of house (e.g. units separated from houses, more localised areas). They're only giving us broad sweeps which are subject to distortion e.g. 2 houses sold in a particular area for $10,000,000 can lift the value of the whole area artificially.

This leads me to conclude that housing statistics mentioned on news media are subject to manipulation....especially those from the REINZ.

Also data is applied to February results...........with the pandemic-induced economic implosion they are now at least two weeks out of date. Two weeks is 'an age' under the circumstances. It's about time the REINZ got with the 21st century and supplied statistics 'as they happen' so to speak....think 'sports streaming'. It's about time someone 'disrupted' the current Real Estate model once and for all. But all the current players seem to be too entangled with their entrenched business models and their cozy relationship with establishment politicians, for this to happen unless our society throws up a genius disrupter.

I collect this data personally for all house sales in NZ, but what you are asking isn't possible within the current system. Two weeks is probably the minimum time needed for the actual sale of the house to go through and the council to be notified and update their systems - which is where REINZ and everyone else gets the authoritative sales price data.

If the data doesn't suit your bias, just rubbish the data LOL

REINZ HPI is an hedonic index, it is already adjusted for those things - Unit vs House, $10m vs $1m property etc. I agree that it would be nice to see segmented data because more information is always better, but the data isn't inherently untrustworthy - just limited.

Hard not to consider leverage as almost free. Well done sellers banking their gain. With all the covid19 noise, will be interesting to watch the next couple of auctions to see if there is any impact or not.

Hi Averageman,

With all due respect, it will take more than the "next couple of auctions" to determine any impact......

TTP

Interesting when you put it that way. A lot of folk selling expensive properties over the last month in Remuera (& central) and the North Shore?

For prices to go up, like REINZ say they have, you need more buyers willing to buy, not more sellers

We're talking about where people have been buying and selling.

Now...volumes have an influence on price, you now say?

Would have to think that Air BnB property's will be in for some tough times, especially is the upcoming announcement this weekend regarding travel restrictions/ban is negative/very negative.

So the FED gods issued $300 billion in the repo market last night. They are also undertaking a $1.5 trillion dollar asset purchase program to keep the markets alive. Bloodbath in the US and European markets. NZX50 7.83% down. NZX20 8.21% down and 8.48% down at 11:15 today. Share prices affect how businesses operate and make decision. It affects how people spend if they are invested in the stockmarket. It affects how people spend their money if their hours are reduced, or they notice that the phone isn’t ringing, the orders are not coming through and customers are not walking in. We are going to see further heavy falls. This will have a trickle down effect into our economy. It will affect all asset classes including real estate. Once people realise what is happening in the markets and the effect of the coronavirus there will be serious implications for everyone in New Zealand. Having witnessed and commented on the breakfast show on TV this morning I believe that most of our fellow citizens simply haven’t got a clue. Thankyou to the Interest contributors, you are keeping us well informed, but a big thankyou to my fellow commentators, we may not agree, but we are aware of whats going on and can share our knowledge. I wish you all well

Re "trickle down effect". I think this is going to be a lot more than a trickle down effect for the NZ and Aust property markets. The obvious overvaluations will reverse and the construction industry will be hit hard.

There will be a few traders suffering from the 'trickle down effect' this week. Let's hope everyone has spare pants.

You mean it could be more like a waterfall than a trickle.

"my fellow commentators, we may not agree, but we are aware of whats going on and can share our knowledge"

Great to share knowledge, observations, and anecdotal examples. Note that not all regular commentators on interest.co.nz are aware of what's going on.

"I believe that most of our fellow citizens simply haven’t got a clue."

Some of these fellow citizens are regular commentators on interest.co.nz as they're unaware of the linkage between financial markets and real estate prices.

Also some other examples:

1) have a relative who is employed in one of the big 4 banks in NZ. They are fully unaware of the linkage, as they have no interest in financial markets, or macroeconomics. They spend the majority of their time watching sports on television (such as rugby, netball, etc), exercising and socialising with friends. They would be the typical family in NZ.

2) have a few close friends who are partners in accounting firms. They work with some of the largest companies in New Zealand, yet they are also unaware of the financial linkages, and have little interest in financial markets or macroeconomics. They are focused on their daily job activities (which do not involve financial markets). They spend the majority of their time with their families, watching sports on television (such as rugby, netball, etc), and socialising with friends.

Prediction: House prices will be down 20% by October.

Maybe October 2021. I reckon it's gonna take more than a year to actually have the full effect of the collapse ripple through the economy.

Perhaps it depends on the region. Queenstown for example relies on tourism and it's suffering right now.

There's houses, apartments and hotels going up everywhere so I suspect the housing correction will start in Queenstown later this year.

I think the total impact on the NZ property market will take some time to be fully felt. As a rough prediction i suspect we will see:

1. Global financial credit crunch (of some sort) impacting banks ability/willingness to lend (short term)

2. Immediate impact of slowing economy impacting decision making (short/medium term)

3. Rising unemployment -> Reduced immigration -> falling demand (medium term)

At this point its inevitable the measures required to contain the spread of COVID-19 will have a big impact on the economy. I just hope we can contain the spread sufficiently that we reduce the chance of any further (more dangerous) mutations occur, as happened with the 1918 spanish flu.

Rising unemployment and loss of income already being experienced in:

1) tourism sector

2) logging sector

Some of the people have large mortgages (and high debt service ratios before the loss of income) that they will be unable to continue servicing.

There might be a whole lot of these people become self employed drivers on Uber ...

I think I will depend on how many developers go to the wall. If there are fire sales on sections, houses, or as happened after the GFC, entire developments then the market could be flooded with property.

Also I'm sure there will be a few mortgagee sales thrown in there. As other have said we are really in uncharted territory so it's anyone's guess really.

That what many people miss when they believe that land prices don't fall and only rise. They think that there is a limited underlying supply of sections, and there is growing underlying demand for sections.

Land prices fall when there are financially distressed sellers such as highly leveraged land bankers / speculators, high leveraged land developers. This is effective supply to the market and potentially causes the imbalance between effective supply and effective demand.

Many people have a fundamental misunderstanding about supply and demand which drives their future price expectations:

1) underlying demand vs underlying supply

2) effective demand vs effective supply.

Unless you expect construction costs to drop in a similar proportion, this is very likely to result in an extremely illiquid market where there are very few properties for sale (probably by those who are forced to sell: bankruptcies, divorces, death etc). What are your expectation about future prices of building material, wages, food and commodity prices, etc. If you expect these to drop too, then there will be a real deflation of house prices. But if the cost of all other inputs are increasing, the deflation of asset prices can ever go low so much. In other words, if your expected outlook is CPI inflation due to intervention and QE, then the drop will not be as significant (which is important for mortgage holders! they will earn more money and pay off debt on something that at least worth them paying off debt), if you expect a general deflation outlook, then there will be total crazy town. House prices can crash so much as you are much better off to go bankrupt and stop paying mortgage than continuing to pay.

For this reason, i expect the Central Banks will try to inflate CPIs and stop deflating asset prices directly. I do not know how they will do that. But this is the response that makes sense. A miracle for sure if they want to do that without increasing interest rates.

Congratulations to all the sellers. I hope the buyers had a very healthy deposit (40%+) and have stable jobs, preferably not in hospitality.

AKL up 7% YoY now. Can we get to minus 7% YoY by the end of the year? This DGM thinks so.

You forgot Tourism, Logging/timber industry, Construction, Accountancy, IT, Sales, Retail, Legal, Street sweeper and concrete layer.

Now let's talk about bankers.

Everyone is going to feel the effects of this major correction of the share market!

It has been badly overpriced for a long time and was well overdue for a correction.

The Banks have been under pressure to lend responsibly and all this is going to do is make it even harder to borrow money if you were marginal before.

The sharemarket has a way to fall yet I would say as who is prepared to buy when there is no real value.

Everyone who has put their money into the so-called productive sector are going to wish they were solely into positively geared property

Until your tenants lose their jobs and can no longer afford the rent of course.

Best have the government arrange for a rental shortage so that you have spare tenants ready to apply as soon as you need to remove the old ones :) once all the “spare” tenants and a decent chunk of existing ones have lost their jobs and exhausted their savings, landlords will start to feel the squeeze. Hopefully by the time it gets to that point government relief will be making its way through the economy so that the pain isn’t too bad.

TM2 won't kick out the tenants he said he's always looking after his tenants.. they are so lucky to have such understanding landlord!

You could be right that tenants lose their jobs.

Fortunately personally we are able to wear that without much of a problem

you could open the door of your own home for those being kicked out by the rouge landlords..

... and then there are those properties being rented out on Airbnb, which are now vacant due to lack of tourists, and not covering their mortgage costs. If they are vacant for a long time, then some of these could be listed in the long term rental market, causing more supply for accommodation. And potential downward pressure on rental prices.

So in the long term rental market

1) fewer tenants (lower effective demand) due to unemployment and

2) more potential properties in the long term rental market (effective supply)

I studied the great depression a few years ago ,an interesting thing that was presented to students was that landlords assumed they were safe and people had to still live somewhere ,what happened was that families and relatives started to live together or congregate to save costs due to security concerns,unemployment or in fear of unemployment.

There was 30% unemployment if i recall correctly ;but,some people who were employed had to accept lower wages than prior to the depreciate,also asset values drop significantly and people in some cases almost sold everything in their homes to meet their financial commitments..

Lets hope for an improvement.

You understand this will feed through to property, rents, landbwankers, landlords, roofers and REagents (sorry ttp)... so many asset bubbles, so little time

Landbwankers? Just made me laugh! Presuming it’s a typo! Don’t edit though, it may bring a smile to others too.

Was talking to someone in the finance industry earlier this week. They are looking for a house in the central Auckland city suburbs. Good Housing selling 10% over CV because the buyers are happy to overpay because the bank economists have said House prices will rise 7% this year. The worrying part though is the the bank has offered to lend them far more than they can afford. Still working to extremely outdated HEM measures. What could possibly go wrong.

The cognitive dissidence is astounding.

I can see this hitting us in the film industry too in Wellington. There's enough coming through post production right now, but give it 6-12 months when there might be a huge gap to fill from the pushed out films. I doubt most the people I know will hang about in NZ if that's the case.

Strong economy, strong job market, strong housing sector.. it only takes a bowl of bat soup to kick start it !!

Long term monthly chart for NZD has $US0.40 firmly in its sights. Imop. 2000 doesn't seem so long ago to me ;).

Eating bats - Ozzy has a lot to be blamed for for sure.

To be fair, a pandemic like this would have made economic life very difficult any time it would have happened. It is hugely disruptive. To me this just shows how difficult (or futile) economic risk assessment can be as it is impossible to properly weigh the likelihood (and impact) of so many possible outcomes. Yet, that is exactly the basis of our decision making.

Many were fooled last month when had similar reporting : Stock Market All Time High despite corona virus and uncertainty.

TODAY after just 3 weeks stock market has crashed and the process is still on with no sight of end for NOW.

Question to be asked : Will Housing market remain immune when everything near around is falling/Crashing ?

OR

TODAY Housing market is where stock market was about a month back so Can housing market be in a month from now where stock market is today (Definitely will not crash like stock but still have an impact and fall).

In this uncertainty and chaos ( Not witnessed before) - Not sure how many business may have to wind up and how many lose their jobs or hours of working reduced - Definitely story is not yet over for housing market. Wait and Watch : All speculators and so called new developers with no deep pockets.

For those of us that remember ‘87 it’s déjà vu. The leveraged will be tested, the over leveraged will go under. Those with cash :) will wait patiently. The perverse thing with downturns is that few can take advantage unless cashed up. Credit will dry up. Every generation needs a good recession to focus them.

Yep, I remembered it well.. lost 4K on BNZ Shares

Indeed. Many of the sub 45 workforce have no memory of it, and the sub 30 have only really seen think go up and up.

Any thoughts on when to buy in EE?

at the bottom, duh! :)

From the REINZ report:

"The HPI for New Zealand excluding Auckland increased 10.2% from February 2019 to 2,995 another new record high.

The Auckland HPI increased by 6.9% year-on-year to 3,035 – the highest annual percentage increase in 35 months and the first time the Auckland region crossed the 3,000 mark"

I rest my case for predicting in September 2019, new all time high values by March 2020

Weren't you predicting a record high median price, specifically?

Excellent!

Well, I never .......

"The strongest price gains in Auckland were in its two most expensive districts, the North Shore where the HPI was up 4.0% compared to January, and Auckland Central which includes upmarket suburbs such as Remuera, St Heliers, Parnell, Epsom, Mt Eden, Ponsonby, and Herne Bay, where the HPI was up 6.1% compared to January."

Of course this would happen, the more well healed of the Auckland population have only cottoned on to what John Key did a year or so ago ....sell up !

They realise apart from their own home, to get the "next sucker" in the PPP (Property Ponzi Party) to buy any property "surplus to requirements" and get the cash out while they can. They have finally realised, as some of us here knew all along, what a crazy market it was, pumped up by the banks and media etc

Just hope your banker mates have the chequebook open for the next sucker to buy ?

PPP stands for Private Public Partnership. It always has and always will CH.

Semantics.......

"However the world's financial markets are changing rapidly and it would be naive to think that the property market will remain immune to a significant economic downturn.

It is still too early to say how badly it may be affected but for the time being at least, the current data suggests that while the share market may be feeling the ill-effects of coronavirus, the property market remains in rude good health."

Balanced reporting thanks Greg

If the current situation continues and no solution is found should see the effect in housing market by April / May and at that time blame will be on winter.

a comment above by "very interested"

"So the FED gods issued $300 billion in the repo market last night. They are also undertaking a $1.5 trillion dollar asset purchase program to keep the markets alive. "

To put a meaningful support the under the current stock market will require heaps more then $1.5 trillon. not a lot was written in AUG/SEPT 2019 when a support of $400 Billion was applied which caused a slight bleep in stock prices only as it was thought the need for the stimulus at the time came about from the effects of US/China trade war. The front on Trade war is all but silenced by the current blow we are in. Who will want to buy stocks when they are overvalued to start with. Why go on with the printing of money to support an overvalued asset/stock. Wait till the institutions dump stocks, thats when the punters who got in after each time the market went down in March 2020 will get a fright. Or may be they wont still, until it sinks to where it should sink to i.e P/E that makes sense.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.