There was clear downward drift in house prices in most districts in April, according to the Real Estate Institute of New Zealand's House Price Index .

The Index is considered a more reliable measure of price movements than median or average prices, because it factors in changes in the composition of sales each month, which can influence median and average selling prices even if there has been no underlying price movement.

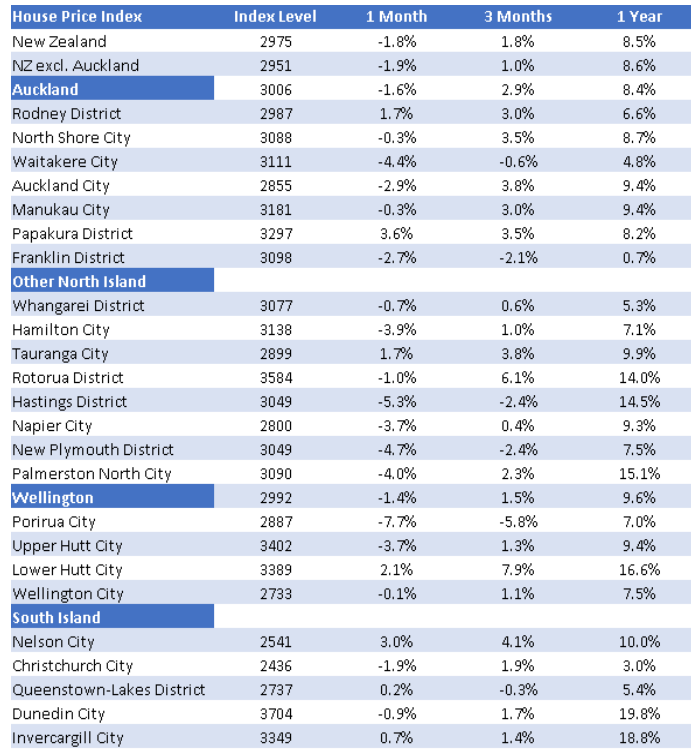

It shows that across the entire country prices declined 1.8% in April compared to March, but remained up 8.5% compared to April last year.

Of the 26 cities and districts measured by the Index, prices were down in 19 in April compared to March and up in seven.

The biggest monthly decline was in Porirua at -7.3%, followed by Hastings at -5.3%.

The biggest monthly increase was in Papakura in South Auckland at 3.6% followed by Nelson at 3.0%.

Within the Auckland region monthly price movements ranged from a decline of 4.4% in Waitakere to an increase of 3.6% in Papakura, with prices down 1.6% across the entire region.

On an annual basis prices were up across the entire country but there were big regional variations, with Christchurch posting the smallest annual gain at 3.0% and Dunedin posting the biggest at 19.8%.

In Auckland the annual gains were more subdued, ranging from 0.7% in Franklin to to 9.4% in Central Auckland and Manukau.

Seven districts posted double digit percentage price gains in the year to April (see table below for the full regional and district figures).

The comment stream on this story is now closed.

REINZ House Price Index April 2020

108 Comments

April figures are for entertainment purposes only. The whole country was shut down. Wait a few months. And we need to see where that unallocated $20billion ends up.

Entertainment purpose and also people/agencies in the business of providing data/analysis have to run their kitchen so the show must continue.

Early days and low volumes. To early to make any call with confidence on the extent of the drop.

We wait and see.

To early to make any call with confidence on the extent of the drop.

Yes. These indexes are constructs and not necessarily realistic indication of house prices at a single point in time. In times like this, these indexes are wholly unreliable.

For ex, the index suggests that house prices in Auckland only decreased 1.6% from March to April 2020. That doesn't mean that the aggregate market value fell by only 1.6%. It could be that the best price that an individual could get for their house is at a level 30-40% lower.

So when can you say with "confidence" that an index best represents reality? Directionally you can only do that when the number of sales transactions is high relative to other points in time. Right now, it could be that the sales volumes is the worst its even been since this particular index has been constructed.

Agree - price dips are trifling to date.

TTP

Not quite. You should say "the indices are trifling to date".

I read the comments section to get a handle on the data and to call multiple 50% declines over the last three years 'trifling' is a bit cheeky!

Here is an interesting take in situation from a property investment company that seems to be clued up to see what is coming unlike most in this industry.

https://www.propertyinvestorcentre.co.nz/deteriorating-world-markets-wi…

Not at all what I was expecting.

Refreshingly informed and realistic about the challenges we face.

Agreed. Logically stated argument. Clearly call vested interests.

Option to live further away from the city is the new norm after this pandemic. Let’s hope our city dwellers will move to regions in coming years. It’s not just Aussie, and is happening all around the world (US, India, Thailand and South East Asian countries). If this spreads to NZ means our biggest cities Auckland and Wellington will be affected too. Even people works in public service can work remotely, as no longer required to go every day maybe once in week or a month. The memo is issued to all google employees to work from home, and required to attend only meetings once in a month in physical office.

https://mobile.abc.net.au/news/2020-05-15/australians-seek-regional-aff…

https://www.google.co.nz/amp/s/www.latimes.com/business/technology/stor…

I think this trend is exaggerated.

You think? March was an all-time high, April is generally lower than March and it was indeed 1.8% lower this year and April 2020 is 8.5% higher than April 2019

You think? March was an all-time high, April is generally lower than March and it was indeed 1.8% lower this year and April 2020 is 8.5% higher than April 2019

This is where people are either foolish or duped by their laock of understanding. For ex, if comparing the month of April yoy, you might be comparing 100 sales with 1200 sales. The unreliability of the smaller sample size is important and most people don't have the chops to eestimate the extent of the unreliability. Statistically, what you point out would be disregarded.

I admire your attempts JC but I've come to accept this is ultimately tilting at windmills. The commenters who are going to get it already get it and the ones who don't never will. Some of the locals here have made it to their very advanced ages without ever understanding basic stats and data analytics, they are not going to have their come to Jesus moment in the Interest.co comments section now. Leave them to their delusions and malinvestment.

I think you are on a different planet. My response was relating to the trend of remote working / living...

And you will know your laid off when your remote access dosent fails one morning. It used to be when your BlackBerry went blank. Tech companies are known for ruthless exiting of staff.

After successfully proving working from home is achievable, my works now keen to get everyone back into the office as a show of strength to our (international) clients. "Look at well we handled covid, bring your work here."

It's a shame. Would love to be working further out, with those perks yet minus the commute.

Working from home isn't all it's cracked up to be. I don't see a massive move towards working from home coming out of Covid, although I do expect tolerance for occasional WFH days to increase.

Totally agree. I am totally over working from home 100% of the time.

As you say, we will likely see more WFH on a part of the week basis.

For me the ideal would be 3 days in the office, 2 days from home.

Surprised the headline wasn't "prices up 8.5% year on year despite Covid-19!" Guess we'll leave that to Bindi Norton.

Far too early to call anything from this. These were all deals that were agreed prior to the shutdown. I'd be gutted if I'd bought last month.

The family has a distressed auction coming up this Friday. It will be interesting to see how it goes ( Christchurch)

Sorry to hear that

Watchout for low ballers who wants to buy below market value.. I can name one or two on this site.

All the best.

Erm... Whatever it sells for will be 'market value'.

Exactly. Forced seller, and wary buyer. In a market considered by all to be over value thanks to central bank policies, look forward to feedback k on how it goes.

Well, yes and no. It is possible to buy a home that for whatever reason sells below what would reasonably be expected to be the market value of such a home. If NZ agents knew how to value property instead of just asking the buyers ‘well what do you reckon?’, that would help.

We are about to enter a period where properties will be seen as more of a commodity than before. This will be exacerbated if banks end up with a high volume of assets on their books. An agent worth their salt should be able to look at a home’s quality, size, age, location, special features, any deferred maintenance, and so on, and put a number on it, and banks will expect that. They don’t suffer from emotional attachment to real estate assets like owners (or buyers), and will want homes off their books as fast as possible.

Surprised the headline wasn't "prices up 8.5% year on year despite Covid-19!" Guess we'll leave that to Bindi Norton

Yes. This is how it works. And people will actually believe it.

A noticeable dip already, get ready for the landslide ahead

I’ve come to the conclusion that the only way I am ever going to believe statistics is if I would be happy to believe them if they said the complete opposite. I see too many people and even serious researchers that are happy to believe them when they match their narrative but not if they don’t.

Hardly a meaningful decline. It's too early to draw conclusions, in September/October (or when loan holidays cease, banks may try to "extend and pretend") we will see what pressures are applied to the property market.

There were comments on interest.co that Manukau house prices would underperform and suffer the most. Look again.

I thought there were comments that it was too early to early to use data to determine trends - or this an exception?

April was under lockdown so best is to wait - not even for may data (As most unconditional sale in the month of may will be those done earlier/Pre virus high price) but should wait till September/October though July /August data may indicate the direction that housing market may take (In all probability will be down but have to watch the speed and how deep the fall will be)

Also in today's scenario year to year comparison does not hold good as till February/Early March all asset class be it stock or property were all time high (may be would have continued) before hit by corona virus but after the accident of Corona Virus, economy is bedridden with no cure for now, so question of running does not arise as first it has to walk, will be happy with baby step.

".. best is to wait - not even for may data but should wait till September/October"

Does anyone have a white flag you could borrow?

Agree FHB (Provided jobs and earnings are secured) who have struggled / waited so long can now wait atleast few more months, if not more to take advantage of opportunity created by virus and save valuable $$$$$ and buy with more certainity of jobs or earning being not damaged in few months time and hopefully should also have more clear picture than today of future.

This data is pretty meaningless for Auckland. The majority of Barfoots 'sales' were simply contractual completions on apartments where deals were signed a few years ago to buy them.

As REINZ dont publish data for existing dwellings, new builds, apartments etc separately headline numbers are always going to be very difficult to interpret.

Auckland rental listings on Trademe right on the edge of breaking the 5000 barrier...supply is building, something will give

You first mentioned about breaking the 5000 rentals 3 weeks when there were over 4800 listings. Can I also add. Only those listings of 2 bedroom rental properties has increased, the number of auckland rentals in all other categories is unchanged from12 months ago. Too many apartments have been built and bought by investors so I expect to see some price pressure in that category in the suburbs where there is an oversupply. Some central suburbs including otahuhu have got very stable to falling rental vacancies, I cant see them being affected yet if at all.

Thanks for that. Sounds like you monitor the market very scientifically.

Let's see where things trend in the next couple of months. Hard not to see CBD listings rising.

Try and watch for trends in my spare time. Mine is one perspective only so it's good to be able to read the opinions of others but not so much the wild ungarnered assertions... those ones really piss me off :) apology for any bad comments I've made.

I think you mentioned you monitor these trends as part of your day job.

That's correct but still outside 9 to 5

Yep you're right Fritz, There's likely to be a lot of Airbnbs among those new listings as well as those relocating due to job losses. Of course the main flood of lot of holiday lets listings for sale will be in the provinces.

"There was s noticable dip in house prices in April" More specifically the house prices were up 8.5%. Say what??? Prices were UP 8.5%. Sorry Greg but your headline is totally misleading

Depends on if it's MoM or YoY your looking at.

I mean arguably, in real (deflation adjusted) terms instead of nominal, you could argue that perhaps housing rose in value last month despite prices falling. Without any inflation data (deflation data) it's hard to tell.

Statistics, eh!

You can make them say anything you want them to.

But the only statistic that matters is "What price did I get when I sold MY property?"

And a lot of New Zealanders will be looking at that statistic this week in a way they didn't 10 weeks ago....

Wow you still cannot see the trend developing Yvil ? better take off your welding helmet mate, its the wrong thing to use for riding a motorbike.

No I cannot Carlos, what "trend" do you see from these April figures?

Unfortunately, the reality of journalism and publishing in 2020 is that web traffic drives revenue and nothing drives web traffic like a sensational headline. If the public won't pay a subscription, then we can't complain. It's their business to run and the btl housing vitriol almost certainly increases the bottom line.

Prime house (not apartment) prices will fall between 7% to 12% in my opinion and very quickly, back to early 2019 levels. There will be exceptions of course, but we are already coming out the other side.

Those are very accurate predictions - where did you get your crystal ball?

How did the p-values and σ look when you ran the numbers?

(sorry sarcastic post)

Come on IO, I thought we'd moved on. That's my pick, put yours up and we can compare over the course of the year, sort of like a bit of fun. Otherwise, aren't we taking it all a bit seriously?

I'm not a fortune teller unfortunately! My range for the next few years is 0-50% falls. Add whatever weighting of probability to that range you see fit to fit your risk profile for such a leveraged investment!

You're familiar with Harry Dent IO? He's expecting big falls too

Watch "[PODCAST] Will the bubble burst or do we burst Harry’s Dent’s Bubble? | Interviews with Harry Dent" on YouTube

https://youtu.be/dfAPmlp6Tk4

Familiar with but don't follow so no thanks.

Probably very wise, his assertions of collapses are so wide of the mark... they get him a good headline to sell his books. The formula is a winner

Did you just say I'm wise...steady there Houseworks.

Un-wise, wise-guy. If the cap fits IO

That doesn't make much sense - but ok!

We as a country maybe coming out the other side of the health implications of Covid but the economic implications have only just begun and then there’s the little issue of what’s happening globally to add to the mix.

Wow suddenly a whole different looking house price table, who would have guessed ? Looks like anyone compiling this over the next few months is going to wear out the "-" button on their keyboard.

People like Carlos67 will once again be surprised just how resilient the NZ housing market is.....

A fall in median/average house prices, yes, but nowhere near the magnitude that the DGM yearn for.

As a general rule, it pays to be cautious of people who are rigidly pessimistic and resort to using emotive language. Typically, they don't have too much to show for it......

TTP

That has to be watched.... MAGNITUTE of fall.....

For a change, everyone in interest.co.nz be it experts or people commenting agree that market will fall and the only question remains - How much will it fall ? and how fast ?

Seeing the damage that virus has and is doing to the economy, result/answere seems to suggest that tbe fall will start from 10%......where it ends to be seen.

Some of the biggest gains come with an 'unexpected' fall in price.

Soros and sterling for instance or those who saw big department store JC Penny falling from $75 a share to today's 20 cents. (NB: Why did JC Penny fall? They refused to acknowledge their market had changed.)

It's all about magnitude ( as noted above) and time......not to be confused with timing.

And the worst falls of all? Those that drag on, and on, and on ....and keep proffering false hope of a return to the good ol' days.

Much better to get it out of the way "Early and Hard!" as they say. But that is unlikely in this case. So, on and on and on...it will be.

Yeah, the gains will be in other asset classes (property bros be like "what's 'other asset classes'?").

Gold.

So what drop in median value are you predicting Timothy...you’re quick to judge the so called DGMs but so far haven’t produced your own predictions. And no “covid will be a game changer” is not a prediction, rather stating the blinking obvious. It’s easy sitting on that fence son...

I'd personally be more weary of those who proclaim themselves to be offering "independent advice", while failing to disclose they have a vested interest in keeping property sales happening.

The new normal... whoops!

Description "The tenants have gone, the money dried up and due to financial stress our North Island owner desperately needs this property sold.

https://www.trademe.co.nz/a/property/residential/sale/listing/261376091…

"... our North Island owner desperately needs this property sold"

Thank you for sharing this example with us.

Property investor portfolios can have hidden fault lines and can affect property prices in seemingly unrelated locations.

This is a North Island based property investor, experiencing cashflow stress with property located in Christchurch (10 Atap Place, Belfast, Christchurch City, Canterbury)

This is also how a previously positive cashflow investment can become negative cashflow. (no rental income, whilst there is still costs of ownership such as rates, insurance and interest).

Wonder if TM2 is experiencing any vacancies or non payment of rental with any of their property portfolio given that their property is located in Christchurch?

Love the predicable 'Canerbry' chip about North Islanders.

"Ok. So where do I open the bidding?

Anyone? Come on, ladies and gentlemen! Don't be shy. We're all here to buy.

Ok. Well, I'll start with a vendors' bid of $250,000 to get things going. Now. Where do I go from here?

Anyone?

Come on! I know there are some savvy buyers out there amongst you. Who's going to pick up a bargain today?

Ok, I'll put in one last bid on behalf of the vendors at $450,000. Anymore?

Going, going......

Thank you, ladies and gentlemen, for your attendance today but the property is passed in. Please see Lance after the auction if you have an interest"

And the record will show "Passed in at $450,000." Disgraceful!

Vendor bid ... so no genuine bidders at the vendor's desired price level ...

If the vendor is unwilling to accept a lower price, perhaps the banks will in a mortgagee sale ..

Message from interested bidder to vendor bid

Good one! And although mine was hypothetical, you're right. Realistic offer prices should be attached. Because .....(as I'm sure you know)

Banks in Possession are legally bound to look for the best price on behalf of a defaulting borrower, and return any amount realised over what is owed to their customer.

Having an Auction is how banks show 'they tried'.

If a sale fails to reach the amount of the 'market price', the bank will add the property to an 'insider list' and it will be offered to them at a price to cover what the outstanding loan is. The last thing the banks want is distressed property sale prices being out in the open!

The trick is to be on that 'insiders list'. That's where the best buys are to be found.

Years ago, one of my dealers picked up a small island in Fiji that way and even got the selling bank to refinance the loan for him. (He subsequently found out, to his cost, why it was for sale.)

...trap for young players

Indeed.

And we all had much more expensive lessons yet to learn. Being caught the wrong way round with Sterling Futures on personal account when Sadam walked across the border into Kuwait still makes me shiver.

But none more expensive than the number one mistake - picking the wrong partner in life.

Have you ever met JK through your FX trading work. Last week you were on number 5 bw keep looking after her or she might take half of your millions

So how to get such an 'insiders list'?

Forgot the obligatory:

"if you're a savvy buyer you are best to get your bid in now, there are conditional parties interested in this property.

This is your chance to put your best foot forward ahead of them"

Matching headlines with the story is a tough gig these days. The English papers do it all the time. Mind you, so do the American ones, the Australian ones, the French ones, the Spanish ones, the Canadian ones....

Yeah time for the "Prices only ever go up" brigade to start making predictions on the magnitude of this fall or I can see the posts from a few months time already, things like yeah well it went up 50% over the last 5 years so whats only a 20% drop ? gee see prices only ever go up. That however depends entirely on when you enter or exit the market. If I'm wrong about a big drop then its cost me nothing at this point but an apology, but if I'm right then the difference is a saving of potentially hundreds of thousands of dollars.

Carlos

It will surprise you that picking market trends and the extent of the fall is not a guessing game as you seem to be fond of.

It needs to be said; those who have been calling bubble burst over the past year or so have based their assumptions on hopes (and often other emotions such as envy) unlike those who predicted the bottom and upturn of the Auckland market who have based their statements on factors such as the drivers and market trends and signals.

I note that you have posted that you expect a 30% drop and others 50%. One has to question on what basis you and the other posters arrive at such figures as it is not surprising they are unsubstantiated. I chuckle; bit like the bunnies at the races making claims about a horse based on a guess or their lucky number or favourite colour.

The extent of a number of drivers such as immigration (returning Kiwis), unemployment rate, and as we have been in lockdown - the first reliable auction results and trends, listings and sales data post the abnormal lock down are not yet known.

As one who often posts on the direction of the market (accurately since 2016) I will wait and see. I note two banks and RBNZ are ESTIMATING 9 to 12% but even they strongly qualify those estimates.

I talk often with an a couple of very experienced property investors with over thirty years experience each and they are very cagey about the extent. With historic low mortgage rates, a lack of LVRs, low cash rates and a volatile share market they are cashed up, just quietly waiting and watching - and they will be acting as they see potentially reasonable yields. They however are not guessing.

Another factor in predicting likely extent of price drop is who wins the election. I think Labour would like to see a moderate fall of say 10-15% but not much more. National probably reluctantly accept a 10% drop. Both wouldn't want to preside over a crash in prices, so they would pull the levers available to them to try and prevent that.

. . . oh and yeah, Carlos: as to the "Prices only ever go up brigade" that is not an apt description. In 2016/7 I was posting that the increase in Auckland prices were not sustainable, in November 2016 I saw Auckland prices peaking so it has never always been the 'prices only ever go up". Yes, during the winter of 2019 I was posting that the Auckland market seemed to be bottoming, and then in the September and October due to auction trends that there were signs of an upswing while the bubble burst likes of you were rubbishing me. My calls have all been correct - and not "prices always go up".

Quite possibly the difference between you and me, is that as well as prices increasing, I have also experienced downturns in the market. So no, I don't always see prices going up.

However, this probably doesn't fit with your wild and unsubstantiated statements.

So a bit of a long winded rant but still no predictions. By the way have made several posts going for 20% not 30%. The market is so uncertain if you really want to sell right now your going to need to cut 10% as buyers fear even bigger falls after they purchase. All the gains made over the last year are already gone in a matter of weeks.

No Carlos

I have seen you posting about the market 'tanking" - recall that?

Just one line - 20 to 30%. No reason, no justification, no rationale or no substantiating it. Just like the bunnies at the races - horse 10; why??????

Maybe rather than criticising me, I would love you show a bit of insight and take a little more time and justify your figure.

For me; no prediction at this stage as I am not into unsubstantiated guesses.

Cheers

I too find I’m far more accurate with my predictions after I hear the “bang” of the auctioneers hammer...

Why do people have to justify downside figures when bulls just draw a straight line on a chart? Seems a bit unfair.

IO and Carlos

IO: I never use straight lines - that is mikekirk's forte and not proved to be particularly accurate especially in either an up or down swing both of which the Auckland market has had in the past six months and currently. :)

Unsubstantiated posts especially if they are extreme leaves the poster open to challenge.

Cheers

Great to see you editing your original posts p8 so as to not be caught with mutually exclusive view points. Good stuff.

IO

Not editing other than immediate check on grammar. :)

What is going to happen to property prices?

A) The property price bull case (courtesy of Tony Alexander)

Well, what do you reckon happens to house prices in a downturn when:

i) one-third of properties have no mortgage,

ii) the home ownership rate is a low 62%,

iii) mortgage rates are at record lows,

iv) investors buying these past four years have needed a 30% deposit, and

v) the bulk of people likely to be made unemployed are young, do not own a house, and have not been able to buy because of a shortage of listings?

http://www.tonyalexander.nz/resources/TV%207%20May%202020.pdf

B) The rebuttal by the property price bears

Well, what do you reckon happens to house prices in a downturn when:

i) 40% of household debt is owed by 8% of households,

ii) the non owner occupier ownership rate is a high 38%,

iii) mortgage rates are at record lows, and many highly leveraged households may be unable to meet their debt service payments with significantly reduced income (due to unemployment, reduced hours for wage earners, salary cuts, etc)

iv) investors buying these past four years have been using equity release and deposit recycling financing techniques, and now may be credit constrained by tightened bank servicing calculations and criteria

v) the bulk of people likely to be made unemployed are young, do not own a house, and have not been able to buy because of a lack of affordability of house prices?

No need to try and justify my prediction really. Prices dropped by like 9% after the GFC and i didn't even notice it as being an event. Hands up who thinks that this is at least twice as bad as the GFC ? Sure as hell couldn't miss noticing this one. Anyone tracking the stats coming out of the USA can see its the worst in their history it dwarfs everything. The entire monetary system could collapse. Our property market has been a house of cards for over a decade and the biggest hurricane in history just made landfall.

I agree this makes the GFC look like a speed bump...you don’t have the largest economy in the world lose 32 million of their work force in a month (not to mention all the other global economies) and counting and not have major ramifications for the global economy.

Carlos

Good to see you provide some justification.

However, I wouldn't say it "dwarfs" the worst in the USA - most economists saying unemployment in the USA could possibly match the Great Depression and even that is seen an being on the worse case scenario side.

I would also be careful about drawing direct parallels between NZ and USA - e.g. NZ death rate 4/million and static whereas USA 271/million and still climbing at around 1500 per day.

Cheers

Death rate comparisons are irrelevant. We didn't have mortgages with banks in the USA in 2008 and yet our house prices got impacted. The entire world is now interconnected due to our modern lifestyle. What happens to the biggest economies in the world now just ripples through to us but the problem is that this is looking like a tsunami.

Correct, Printer8 just threw in a totally irrelevant red herring as his argument is floundering.

cmat

Not floundering at all. :)

Carlos

. . . and what was the consequences for housing (and equities) in the decade following the GFC in 2008?

Just saying.

So your argument is that it doesn't matter if there is a 20% or even a 30% or more housing market price crash right now because its going to recover and increase over the next 10 years anyway ? I think I already preempted that type of response just the other day, just scroll back up the page.

Hi Carlos

I am just waiting and watching.

Only indications so far are RBNZ (9%) and two banks (10 and 12%) and they have a little more nous and influence than you and I.

We wait and see. Certainly 20 or 30% short term drops would make yields look pretty attractive to many investors.

History would suggest that banks would have no idea what housing markets are going to do.

Yields on no-tenanted properties?

Yeah, super attractive.

That’s a shockingly poor response even by your standards sir.

Albert

Who do you refer to and what comment (time?)

If you refer to my comment post 2008, was the increase in property and equities not the most significant lasting impact of the GFC brought about by low interest rates, and QE?

Cheers

I read an interesting finance paper recently that. It showed that for the stock market as a whole, Eg the SP500, price elasticity was a myth. In fact if 1% of the market value in new funds flowed in, from bonds say, the market would rise by 5%.

Well if that's true, I wonder what the effect might be for famously illiquid markets like real estate? https://youtu.be/OQnHosZPuKQ

Can't wait for NZ's property "Minsky moment". When that puff of dust is visible at the bottom of the cliff and the present generation can buy a house intended as a shelter (and not as an investment or speculation), then our feet will back on the ground again.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.