There was a substantial increase in the number of homes being listed for sale in October, with many potential vendors deciding the time is right to sell.

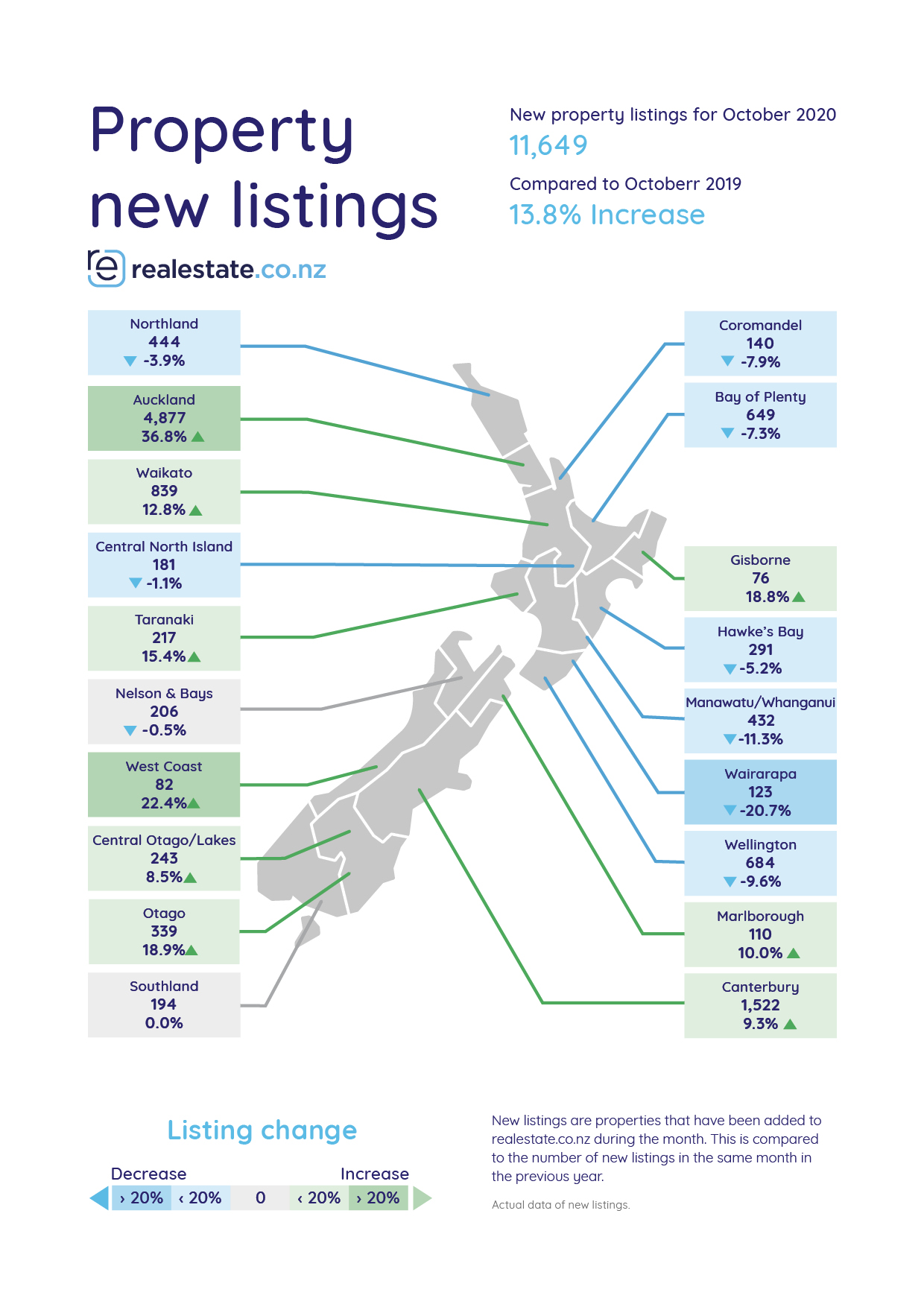

Property website Realestate.co.nz received 11,649 new residential listings in October, up 13.8% compared to October.

The Auckland market was particularly strong, with 4877 Auckland properties being newly listed on the website in October which was up a whopping 36.8% compared to October last year.

That was the highest number of Auckland properties newly listed for sale on the website in any month of the year for more than 12 years.

Other regions where new listings were up strongly compared to October last year were Waikato +12.8%, Taranaki +15.4%, Gisborne +18.8%, Marlborough +10.0%, Canterbury +9.3%, West Coast +22.4%, Otago +18.9% and Central Otago/Lakes +8.5%.

However, new listings in several regions were down compared to a year ago including Wellington -9.6%, Wairarapa -20.7% and Manawatu/Whanganui -11.3% (see chart below).

Realestate.co.nz spokesperson Vanessa Taylor said buyers would be buoyed by the fact they had more properties to choose from than they did at this time last year, and if the increase in new listings continued, this could affect prices in some regions.

"Typically, we see an increase in Kiwis looking to sell during the summer months with a drop off over the Christmas season," Taylor said.

"However, the impact of the nationwide lockdown earlier this year and the changes that many Kiwis are experiencing as a result of COVID-19 mean it's anyone's guess when new listings will peak this season," she said.

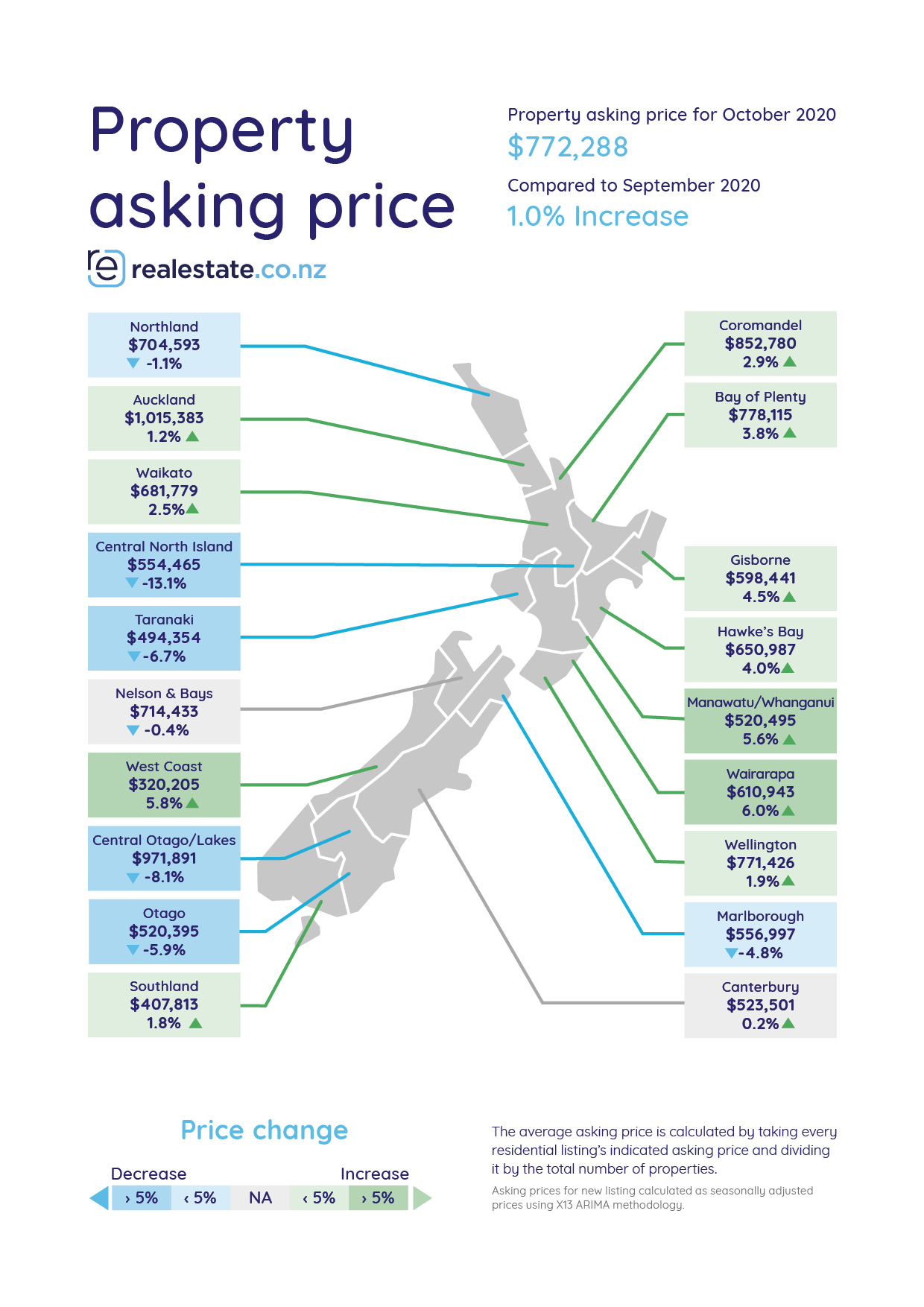

Vendors are obviously being encouraged to sell by the buoyant state of the market and that is being reflected in strong average asking prices.

The national average asking price (not seasonally adjusted) was $772,288 in October, still well below the record of $858,432 set in April and still slightly below the August average of $824,702.

However record asking prices were set in six regions - Auckland, Waikato, Bay of Plenty, Hawke's Bay, Wairarapa and Manawatu/Whanganui (see the second chart below for the full regional figures).

The biggest decline in asking prices was in the central North Island where it was down 13.1% compared to October last year, followed by Queenstown-Lakes -8.1%.

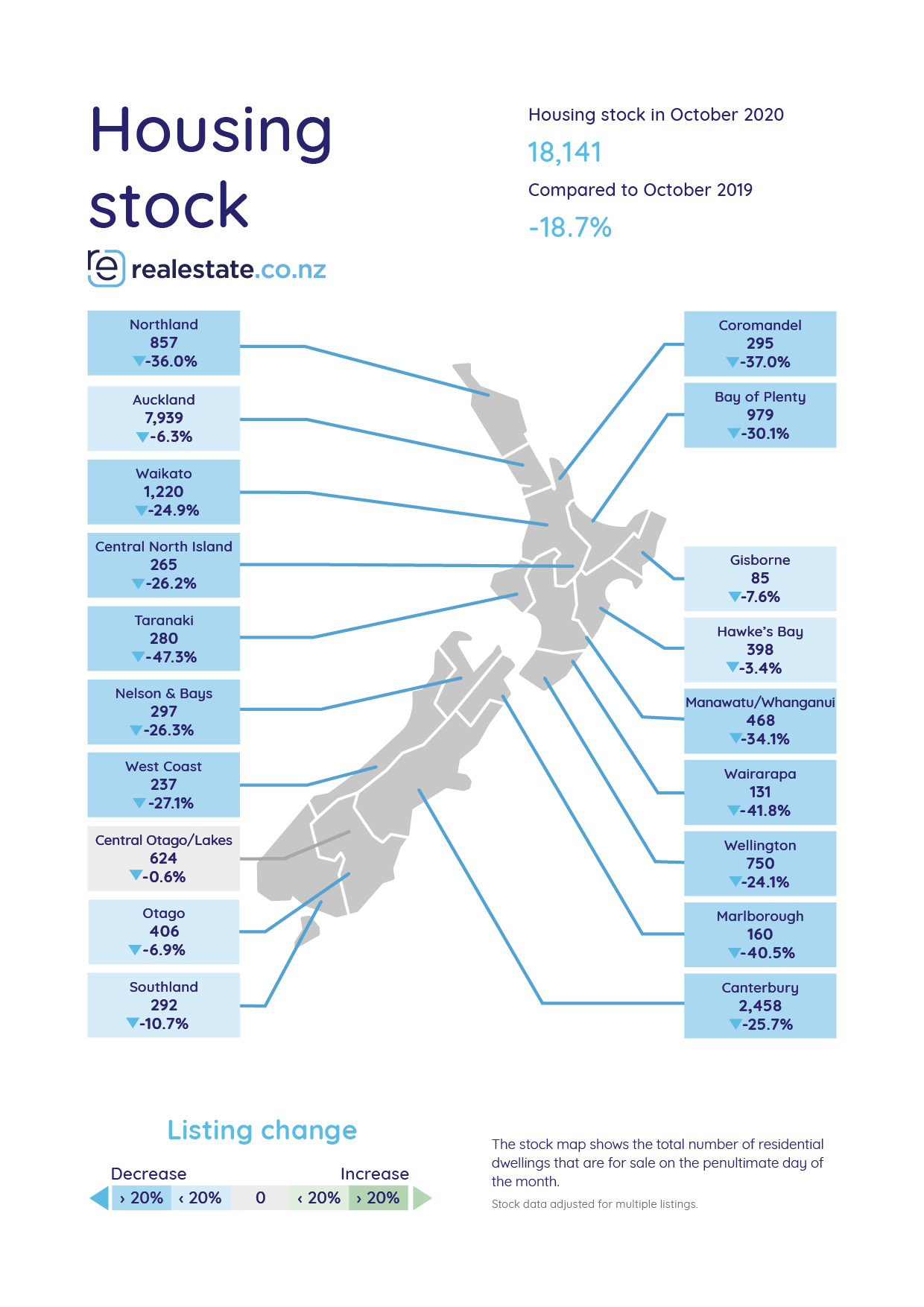

However, although the number of new listings picked up significantly in October, total stock levels remain relatively tight.

Realestate.co.nz had a total of 18,141 residential properties available for sale at the end of October, up 3.21% compared to September but still down 18.7% compared to October last year.

In Auckland the strong surge in new listings meant total stock increased by 6.98% compared to September but remained down by 6.3% compared to October last year (see the third chart below for the full regional figures).

Overall, the latest figures suggest the buoyant market that has been evident over spring looks set to continue into the summer months.

The comment stream on this story is now closed.

58 Comments

Ultimately what matters is the stock for sale and this is still down in every region in NZ despite the much higher listings. Combined with the low interest rates, this means prices will keep rising

"what matters is the stock for sale" - I disagree. As demonstrated in the past few months, fundamentals don't matter at all since this is no longer a market. Credit availability is the name of the game.

Prices now completely depend on RBNZ action (since no fiscal policies targeting housing are to be expected anytime soon).

Yvil is correct. There are far more credit approved buyers than property on the market, which is why prices are rising. It may be tougher for some segments of the market to get credit, but overall the market is not credit constrained.

Agree that stock is still very low. Surprised to see that listings are up.

New listings may have risen, classic supply side response to rising prices, but overall inventory levels are still way below this time last year. Look at Coromandel, prices up 3% in a month and 37% lower stock than a year ago. Prices rises haven't finished yet.

Agree that stock is still very low. Surprised to see that listings are up.

So people list their properties for sale, but they're not actually intending to sell. Why do this? In the chance of being offered a king's ransom? I think I know a few people doing this but the homes are probably north of $2 mio.

Plenty multiple units being completed on one site in the tron. They advertise ONE when 8+ are on the site.

Plenty of BS going on.

But pile on in...msm and their advertises know the market.

Getting credit is not very hard... Check with any finance broker.

CourtJester makes a good point though.

It doesn't matter if the stock doubled, with so much demand and silly money around.

Although supply is of course very relevant, it's the RBNZ's actions affecting the demand side that is the key factor.

Agreed, this is market economics 101.

A very silly time to be buying. An excellent time to be liquidating.

These listing increases are off a very low base....... but at least a move in the right direction.

There's been a dire shortage of listings in Auckland, Wellington and many other centres for months.

TTP

I flew to Wellington in the weekend and we were diverted to Palmy. Boy is that a dump. Makes the tron look nice.

Just interested....

1: Where are buyers living now? If renting then rental house will become available, be sold or owner will move back in.

2: What are the sellers doing? Trading up, Trading down, Renting for a while, selling their rental, moving overseas, moving in with parents, Relocating. If you take the headlines in the media it would appear everyone is trading up or it’s first time buyers entering the market.

FOMO created by rising housing price in Auckland, being supported by government and RBNZ, if stops will prove to be disastor as have witnessed units in Auckland going at 40% to 50% their market value - 9000000 being sold for 1.2 million or 1.3 million plus ( no land or view) and this is not in Epsom or Remuera.

Any free standing house wether subdivideable or not is getting premium and if sub division possible going at 100% to 200% above market value. Agree by subdividing, supply may increase but by paying ridicluse high premium for land, cost increase much more than before the government tried to help by freeing up housing zone for construction.

RBNZ and Government fueling housing ponzi and now can they act, even if they want to by creating a monster. No word from Jacinda Arden on housing crisis but when question with straight face comes with supply completing ignoring speculative demand - forget that economy is Supply as well as demand and by ignoring any one situation cannot be solved.

So even governments help is more towards speculators than FHB and what may actually help FHB Luke CGT, LVR...is ignored by RBNZ as well as government and are talking only about Supply side problem ignoring the problem and controlling speculative demand.

"Any free standing house wether subdivideable or not is getting premium and if sub division possible going at 100% to 200% above market value

This is incorrect. A property may sell for 100% more than you think it is worth, but the market value is the sale price. What you think it is worth is not "market value".

This is incorrect. A property may sell for 100% more than you think it is worth, but the market value is the sale price. What you think it is worth is not "market value".

OK, does that mean if a national price index goes up by 1% that the housing stock value has not increased by a propotionate amount? The ruling elite, media, and general public tend to think differently.

I feel she got away from this because of Covid 19. If this happened last year, she would've got bashed by Media's questions. But these issues wont disappear by themselves. One day, she will be facing these questions. I don't think she will be ready.

She's turning into Aunty Helen. A pragmatic and conservative centrist. A master politician, but one with limited vision and legacy. A love of incrementalism.

Aunty Helen loved the property boom of the 2000s. They all do, whether left or right!!!

Clarke: FU, Got mine!

Key: FU, Got mine!

English: FU, Got mine!

Ardern: FU, Got mine!

Ha!

FU, got mine! Plus it's great for my popularity! :)

It pains me to say it, because I live in a physically attractive (currently) inner suburb of Auckland, but: *this* part of the bubble is a good thing.

We need more density. The loosening restrictions *should* lead to a premium for subdividable sections, and those sections should be developed. I just wish there was more will and capacity to build attractive, solid multi-storey dwellings, rather than *another* set of mushroom-grey townhouses slapped together with GIB and waxed paper.

Sort of, although it's a bit of a false narrative because the townhouses or apartments that are built will inevitably be expensive. Especially townhouses, if the land value component of the selling price has doubled. Less of an issue for apartments.

The problem with the current developments is that the new townhouses cost almost as much as a standalone house + section in the same area. In my area, developments usually looks like this: developer buys 3 adjacent sections for about $2 million each -> Builds a dozen units -> Sells units for $1.5 - 1.8 million each. Density goes up, but price per unit remains pretty much the same.

New homes are worth more than tired old houses. But do the math, when there is demand and limited supply the developers can charge whatever and buyers will pay. When supply increases there is more buyer choice and developers will compete harder for your dollar

Have you not been paying attention?

A contributor here has been drawing everyone's attention to 1000 sqm sections with old or dated villas being sold for land value only. Properties within a 10 km radius of AKL CBD. In the last 3 months the land value per sqm has increased by 17% in just 3 months. In some cases more. Developers going gangbusters buying anything with multi-unit potential and paying knock-out prices individual homeowners can't match

Vendor FOMO is here, this spike in offer on top of the more than likely removal of LVR will likely cause the end of the current trend, hopefully affordability will improve as a result of it.

RBNZ has no intent or even if firced to introduce will give 6 to 12 months window for speculatirs to play unlike earlier when had fear of house price came out as soon as to help by removing LVR and mortagee defferal til next year.

RBNZ will act and will act fast to support the ponzi and not to stop or disrupt it.

This is not the impression they gave given their recent declarations.

Lack of tourism already hitting the prime AirBnB locations. Let's see how unemployment will look after the Summer season. Can kiwis make up for the lack of international tourism? I've seen somewhere that the money spent by international tourists in NZ in an average year is about twice as much as kiwis spend abroad.

Income?

pfft

who needs it

we can trade houses with each other and let real estate agents keep the cafes afloat

That is the one. Rockstar economy.

But will it turn out like a typical rockstar?.. soaring high while the stimulants are flowing freely then passed out for 3 days after the party is over?

Ha, nice!

Who knows

Someone on here noted the resemblance to a 'blow-off top' last week. I prefer to call it The Spike before the Big Chuck...but whatever. It could be that others, all over the place, see similar?

The word is out among Sydney’s prestige homeowners: sell now in what is a surprisingly strong high-end market....Stockbroker Rob Fiani has heard the call, with preparations underway to launch his grand Bellevue Hill mansion this week for more than $20 million...

https://www.afr.com/property/residential/stockbroker-lists-sydney-house…

[ removed ]

That wouldn't surprise me. But I guess we'll know on Saturday morning!

Nobody knows but the S&P500 is up 47% from its low on 23 March.

So 20% drop is only taking the S&P500 back to about mid April so it wont be a great disaster.

Tech can fall along way and not have much impact as the rest of the market is still so far down including the big US banks

[ removed ]

Are you just plucking any random number for drops, putinbot? Or is this based on anything?

All I do is invest in US Equities full time on my own account so know nothing of France.

But chances of a 50% drop in the US S&P500 are zero. Now 20% of the market are Apple, Amazon, Facebook and Microsoft who are making so much cash its not even funny.

History Doesn't Repeat Itself, but It Often Rhymes.....see largest drops in history here https://en.wikipedia.org/wiki/List_of_largest_daily_changes_in_the_S%26…

Not surprised, it's just couple days before US election. People sell to avoid risk of US election result.

I don't think someone would sell their mansion just to lock in capital gains. The guy is a stock broker though, so I might be mistaken. We've seen another of his kind sell his $20 million+ mansion just to cash out a few years ago...

It was a ridiculous example. The person in the article just paid $34m for a house and is now selling his old place, I know what I would deduce from that.

Wouldn't you keep it if you thought it would appreciate? (NB: At that level, liquidity; getting a(nother) mortgage, isn't a problem at these % rates)

We all have to live somewhere, and if it's a $34 million place, so much the better!

“Better three hours too soon than a minute too late.”

Of course listings are up, up, up !! ......tons of places onto the market, as Air BNB's etc now producing no income. ......extremely cheap interest rates and MAY get cheaper !! .....wealthy returning NZ residents returning from overseas..... c'mon Kiwi's get with the program and "buy, buy, buy" ! .......bye bye

PS - I just ask one thing .....IF (note I didn't say 'when') it all comes tumbling down, for any reason whatsoever, please keep your hands out of the bank depositors and taxpayers pockets and FINALLY let the market "run it's course"..... as this is NOT a free market, in it's present form.

Governmant and RBNZ has created a monster that is beyond their control and have twingled themselves in a sutuation where tbey cannot afford to go back infact will be blackmailed now more to provude more and more stimulus or tgeir will be bloodbath on the street.

All the central banks are playing the exact same game. It is not unique to NZ. Get the people to take on massive debt - because it’s cheap then watch them squeal when the market turns the other way. Desperate people will take what’s offered. Enter Central Bank Digital Currencies. Enter the brave new world where you will own nothing as outlined by the World Economic Forum last week. This quote from Jeff Booth sums up the effects of governments kicking the can down the road for decades. “Governments prevented creative destruction in the free market, and by doing so - creative destruction is moving to currencies and governments instead.”

Hope lives eternal. There is no ways the RBNZ will block an OBR event and hence depositors will be fleeced. It'll be up to the govt to decide whether there should be a taxpayer bailout and I'm not so sure they will. Any fund holding deposits with a bank will also get done. The fund won't care as all that'll happen is the value of your fund will depreciate and the fund manager will say its a govt problem, not theirs.

We currently have an environment where almost nobody is forced to sell. However, in Akld the number of new listings was at a 12 year high. Does the fact that more people are now trying to exit the market than at any other time since 2008 concern anybody? I think it should.

I find it hard to square. What are all those sellers intending to do with the proceeds? Investors de-leveraging makes sense, but many of the usual rationale for (discretionary) sales are not very tempting. Travel? no. Retirement village? no. Overpriced shares? er. TD at ~0%? hrm.

I do wonder a little about the listings and stock mix. Could be that there are a lot of new listings for airbnbs and student flats, but things are tight for places that kiwi families actually want to live? That could give you listings being up, but a tight market for homes.

Just looked at Trademe, in Auckland only about 26% of listings are for 1 or 2 beddies which is quite typical. Doesn't look like a massive flood of these types of properties.

I imagine plenty of these listings are from vendors who want to upgrade with the bargain basement mortgage rates on offer.

Please tell me that "image" at the head of this article is not an example of terraced housing anywhere in Auckland

Nah, in Auckland it's either white & gray or black & woodgrain

Google lens suggests Houston, TX.

Looks better than hobonsville point tbh

As usual devil is in detail (which we do not have but perhaps RE NZ does ?)

First query: WHO is selling and second, WHAT are they selling?

That is: are investors selling some of it/their portfolio and if so why?

Are owner occupiers selling because they are pleased to see sale prices exceed CV for first time in 3 years?

Are developers selling loads more than usual per month, as investors are hoovering up stuff off the plan? ie a lot more than were doing a year ago? Guess is: most of the above. RE NZ does not tell us.

The stock on RE NZ in Auckland that has been OTM over 3m has fallen from about 27% a year ago, to 17% now (I checked then and now, personally) So, inventory is falling as sales sell faster than new listings added.

In October that probably levelled out.

Sales in June were up 14% on 2019

In July it was 36%

In August it was 47% and Sept it was 53%

An interesting stat might be the ratio of increased listings to increased sales in following month.

I expect October sales to come in about 2995 (about 44% up)

After that I expect sales to taper off for next 5m at around 25% up on previous year.

After February sales will only equal 2019 figures and comparison will become less flattering with jan-march 2020

How many houses in NZ have been taken out of the NZ stock by investors sitting on them, or using them as Air BNB etc. I really wonder if we do have a realy lack of stock, or people just not wanting to rent them out, when the capital gains are so much better. Dealing with tenants can be a nightmare compared to the relatively small amount you can get, vs the capital gains you get from just sitting on a ghost house. No need to worry about the house being trashed by tenants. Just hook up some cameras and alarm to keep it monitored and empty. I am seriously considering doing this myself, and surprised there is no tax preventing me not just sitting on a house like this.

Covid19 has presented the unthinkable industries sudden profit demise/dip & jobs specially in those airlines, airport, tourism, cruise ships, hospitality, restaurants, educational exports etc. - But at the same time? we also witness the 'replacement unlimited money supply' by every world CBs into those sudden lost of income, the very essence of these bail out/subsidy? is to prevent those Banks with large loan book into specific asset lending as means of year in/out of extracting profit from collapsing. A lot of Kiwis opt to be in denial when being presented with terminal illness diagnosis, but over the time? after time delay.. then the inevitable result

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.