By Greg Ninness

The latest house price figures make startling reading for potential first home buyers.

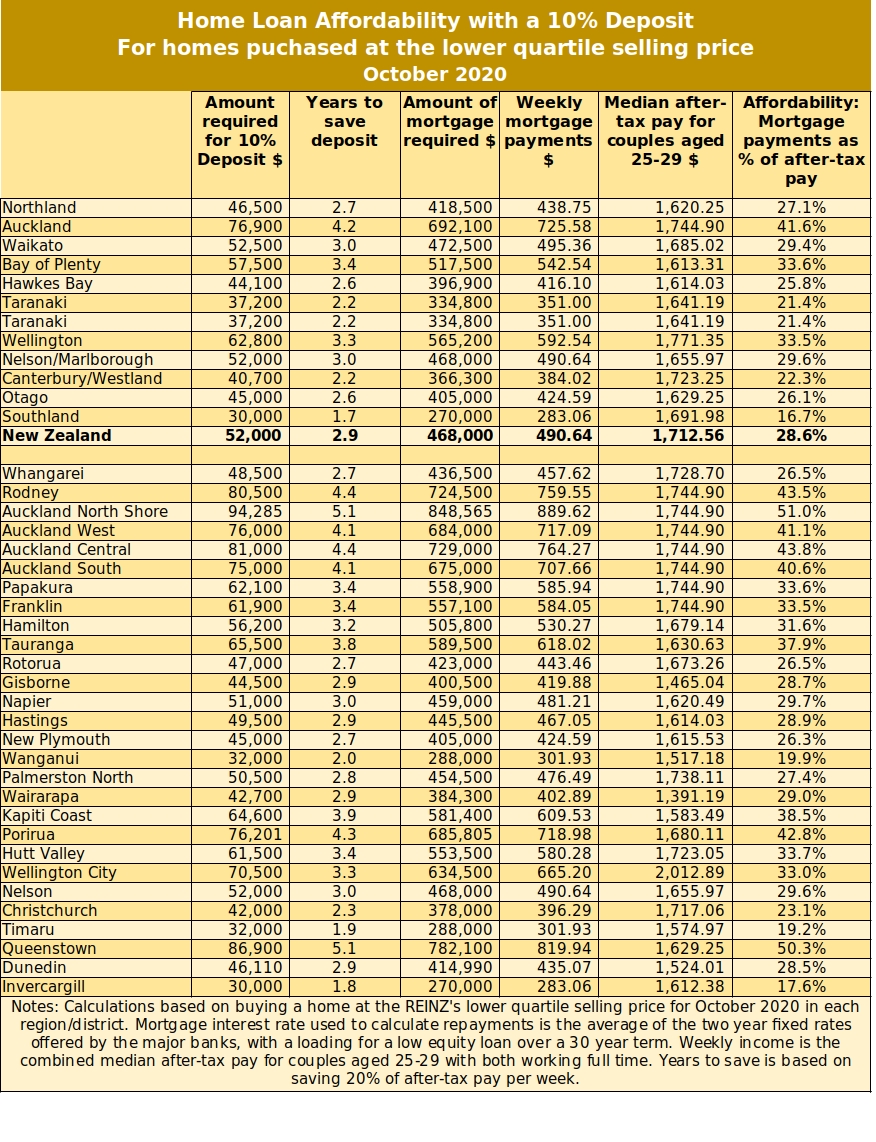

According to the Real Estate Institute of New Zealand, the national lower quartile house price was $520,000 in October.

That means it has increased by $85,000* (+19.5%) since October last year, and by $157,000 (+43.3%) since October 2017.

That's an average increase of $1000 a week over the last three years for homes at the most affordable end of the market (the lower quartile price is the price point where 75% of sales are above and 25% are below).

In Auckland, where prices are the most expensive in the country, the lower quartile price has increased from $654,000 in October 2017 to $769,000 in October this year.

That's an increase of $31,500 over the last 12 months and $115,000 over the last three years.

That means a 10% deposit on a home at the national lower quartile price would have increased from $36,300 in October 2017 to $52,000 in October 2020. The size of the mortgage needed to go with that would have increased from $326,700 to $468,000 over the same period.

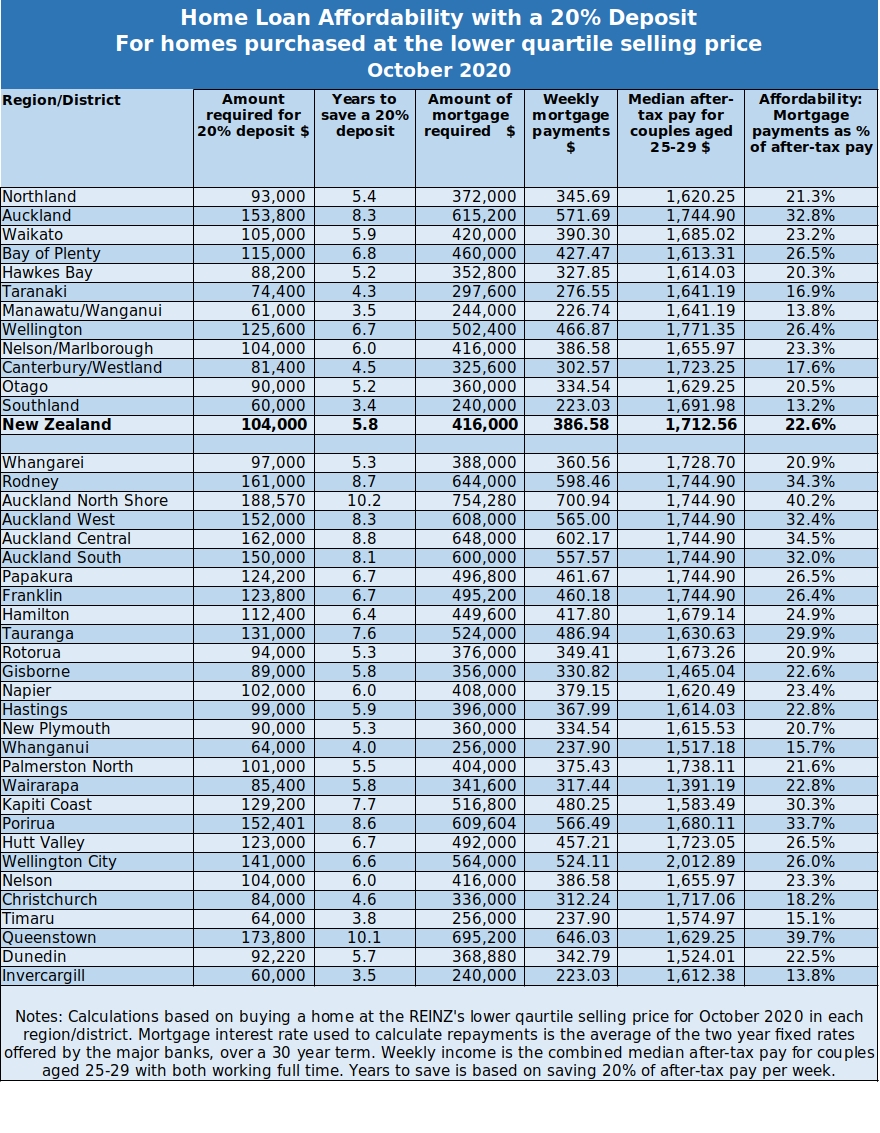

A 20% deposit for the same property would have increased $72,600 to $104,000 over the same three years, while the size of mortgage to go with that would have increased from $290,400 to $416,000.

Those are pretty steep increases, especially when you consider what has happened with wages over the same period.

If you the take the national median rate of pay for couples (male and female) throughout New Zealand aged 25-29, and assume they are working full time, that would give them combined after-tax pay of $1713 a week in October this year.

That's an increase of $34.14 a week (+2.0%) compared to October last year, and an increase of $129.91 a week (+8.2%) compared to October 2017.

So, over the last three years, the cost of homes in the part of the market likely to be of most interest to first home buyers has increased 43.3%, while the take home pay for typical first home buyers on the median rate of pay has increased by just 8.2.%

That suggests lower quartile house prices have risen at more than five times the rate of after-tax wages for typical first home buyers over the last three years. But to get a complete picture of the pressure faced by first home buyers, we also need to look at what has happened to mortgage interest rates over the same period. In October 2017 the average of the two year fixed mortgage rates offered by the major banks was 4.70%. It fell almost continuously from there to 2.65% in October this year.

That decline had a huge impact on mortgage payments.

If you had purchased a home at the October 2017 national lower quartile price of $363,000 with a 10% deposit, which would have required a mortgage of $326,700, the mortgage payments would have gobbled up about $446.71 a week, or just over 28% of the take home pay of a typical first home buying couple.

If the same property had been purchased with a 20% deposit, which would have required a mortgage of $290,400, the payments would have been about $347.19 a week, or just under 22% of a typical first home buyer's take home pay.

At the October 2020 lower quartile price, the mortgage required with a 10% deposit would have increased to $468,000, which would have pushed up the mortgage by $43.93 a week even after allowing for the drop in interest rates.

However the after-tax pay of typical first home buyers would also have increased by about $142 a week over the same period, more than making up for the increase in mortgage payments.

Measuring mortgage payments as a percentage of after-tax pay in the above examples, shows that the figures have remained remarkably stable at around 28% over the last three years for buyers with a 10% deposit, and 22% for buyers with a 20% deposit.

So as far as mortgage affordability is concerned, there has been almost no change over the last three years, with lower interest rates more or less cancelling out the effects of rising prices on mortgage payments.

Higher prices make it harder to cobble together a deposit

Where rising prices will have made it harder for first home buyers is in raising a deposit.

The rise in the national lower quartile price since October 2017 has pushed a 10% deposit up from $36,300 to $52,000, and the amount needed for a 20% deposit from $72,600 to $104,000.

If couples at the median wage rates outlined above were able to save 20% of their after tax pay each week to put towards a deposit, it would take them 2.8 years to get enough for a 10% deposit on a home at the national lower quartile price (up from 2.1 years three years ago). A 20% deposit would take 5.8 years to save (up from 4.2 years three years ago).

So looking at the overall picture, mortgage payments have generally become easier for typical first home buyers over the last three years, but raising a deposit would have become more difficult.

That is particularly true in Auckland, where lower quartile prices are significantly higher than in other parts of the country.

You would need $76,900 for a 10% deposit on a house at Auckland's October 2020 lower quartile price of $769,000, while a 20% deposit would set you back $153,800.

With a 20% deposit you would need a $615,200 mortgage and the payments on that would be about $572 a week.

That would take up just under a third of a typical first home buying couples' take home pay, which should be reasonably affordable.

But if they only had a 10% deposit, the mortgage payments would jump up to $725 a week, eating up almost 42% of their take home pay.

At that point their weekly cash flow would be starting to get tight and it would mean that housing in Auckland is starting to get into unaffordable territory for people on average wages without a substantial deposit.

The tables below summarise the main affordability measures for buying homes at the current lower quartile prices in all main regions and districts throughout the country, with both 10% and 20% deposits.

* Note. This figure has been corrected. When the article was first published the annual increase figure was misstated as $40,000.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers on Friday. See here for more details and how to subscribe.

239 Comments

Hi Greg, Let us talk about about last few Months. Prices have gone up bu 25% to 50% plus and government and RBNZ is a silent spectator doing nothing.

Time chart of hose price in Pakuranga :, A house with CV of 950 pre lockdown was going for 900 to 950 and in June between 950 to to million, in August between million to 1050, In september 1.1 million, in October between 1.1 million to 1.2 million and now in November between 1.2 million to 1.35 million.

So on average from 900 to 1.3 million and still going on. Government, RBNZ and RE industry all have have joined together fir the push. Even website like Oneroof, propertyvalue.... adding by giving high valuation... So something is at play or how does one justify house prices moving 40% or 50% during such uncertain time.

Stabilizing or supporting price is one thing and understand but all went to push price higher and higher and all this has lead to creating bigger FOMO.

Justified by low interest rates expected to go lower and keep lower plus temporary relaxation of LVR rules pushing investors into FOMO

it's the history of all bubbles, sometimes nothing changes. From what I have read bubbles always go way higher than common sense would say is possible, then when they burst they wipe out many, debt forbearance if never a good thing, just creates more pressure in the system.

Have been hearing this that bubble burst but in last many years have not witnessed any. In fact is going from one high to another, with no sign of going burst.

Can RBNZ or government now afford to let it burst. Have doubts and for the same reason both RBNZ as well as government will do anything and everything to support the ponzi and this is what is exactly happening now and will continue.

Bless RBNZ and Government for screwing FHB and supporting housing ponzi thereby creating social unrest along with economy inequality.

it's not if RBNZ and Gov't can afford to let it bust but if they have the power to stop it going bust. Underpinning a bubble by lowering borrowing costs may seem an unwise move when they write the history of these times.

I don't think any government in any bubble wants to let it burst. It will cost them votes for decades, plus they are usually making money out of it somehow, both as a government, and personally....

At least in most countries housing profits are taxed highly so society gets infrastructure as a side benefit of the bubble and speculative buying and selling. We're not even getting that here.

How low can the government afford to drop the OCR? When they run out of gas there, or something globally drops employment significantly, it will pop. Until then it's getting worse and worse.

I don't think it's in anyones interest for the bubble to burst but it is for the bubble to stop being inflated.

For those who don’t yet own, who are young or have been prudent, then a bubble burst is exactly what is needed.

A year of unemployment to reduce the required deposit and mortgage by hundreds of thousands of dollars will be a blessing for many younger people who need to be given a fair shot at home ownership in this country.

If you're young and have been prudent saving for a deposit - unemployment after a housing bubble burst isn't going to do you any favours. Kiss your savings good bye, have a difficult time getting employment, low wages if you get employment, and likely the inability to be able to take on a mortgage to purchase that cheaper home.

I’ve talked to many people who were young in the 1930’s - they did just fine (in the long term)

1930's? - how old were they then and how old are they now?

Dead...

So you're advocating for a depression? yeah.. that'll work well. NZ needs to deflate the housing bubble, not implode it.

What if:

- collectively as a nation, as a people, in need of the basics (housing...), refuse to work unless we're paid a wage that will allow us to afford the basics

- vote out a Government that refuses to ensure we have the basics at an affordable level....

I don’t think you can have both - we need to think long term. Living beyond our means to deny the economic reality we find ourselves in, isn’t living. Especially when one group benefits and another is punished. It’s a recipe for economic and social disorder.

I don't disagree. However maybe it's the demographic that you're trying to help (in a decent percentage) that's contributing to the problem. If people just decided "F@#k it - I'm just going to rent" perhaps that in itself would stabilize prices and may even reduce them. Other jurisdictions (especially EU) often held as comparisons to NZ don't actually have the same obsession with house ownership. Perhaps NZ needs to reassess it's road to prosperity.

But RENTING is unaffordable, Hook. And therein lies the problem.

And you're clearly better off buying if you can.

ARE you though Nifty1? It's been drilled into people that that is the case but has it ever actually been dispassionately challenged? Offshore examples would tend to challenge the idea that ownership is the be all and end all.

In NZ at the moment it is a no brainer, hence the FOMO. You're massively disadvantaged renting. No asset wealth appreciation, no ability to leverage off & accumulate equity, no ability to reduce rent temporarily (mortgage holiday/interest only), no stability in rent payments, no guarantee on living arrangement, no freedom to have pets, decorate etc...the list goes on.

I don't disagree Nifty1, all I'm saying is that in other parts of the world people happily live without house ownership, perhaps NZ is approaching a rubicon. Is a long term lease something that should be investigated?

House ownership is deadweight dragging on your options for at least 5 years - and can be unexpectedly expensive. Renting does have an element of freedom.

Owning is dragging on your options for 5 years? Why 5 years? Not sure if renting offers more freedom - Renting if you leave you have to give 21 days notice, Owning you can currently sell in the same time or less, alternatively you can rent it out immediately. More certainly offered to renters along with better conditions would be a good thing in making renting more attractive.

It takes at least 5 years to start making a dent in the Principle with Table Mortgages. Renting is a clean break after 21 days - selling may take longer and you have "Open Homes" inspections, etc. Going from an owner to a Landlord may not suit all people and there's PM fees and arrangements.

Depends, you can increase your loan repayments or make lump sum loan repayments when you want. After 5 years even if you haven't dented the principal, you've accumulated equity - so if you sell you have made profit. If you don't sell you can leverage the equity. Renting you're making a dent on nothing, just helping the landlord keep things ticking over. When you give the landlord notice you're leaving, they dictate the open homes (with notice) and have people look through the property with all your belongings there. Likewise photos will be taken. You have next to zero control in a renting situation.

Yes, there is research that points to people getting locked into homeownership too early and thus limiting mobility to take advantage of more opportunities and thus resulting in less productivity.

In Germany for example it is not uncommon for people to wait until they are in their 50's before they buy their forever home, as there is no financial disadvantage in buying a house later, but it does give them the advantage of location flexibility for jobs.

There's also a stack of research that evidences the benefits of owning a home - which includes more wealth, better health, better security & in general better outcomes.

Not in the context of the German model there is not.

The point is if the system is set up right, then you get all the benefits of renting, ie not being tied to one spot which is very important when you are young so you can move to take advantage of opportunities that you might be afforded if you could not move, and then all the benefits, as you point out, of owning.

The system that is set up to make this happen, like Germany, also has more stable house prices, so you are not buying to make any speculative gain.

Yeah, we're not living in Germany though.

But it's not like it is some intangible law of the universe that we must have high house prices.

It's all about individual countries making policy decisions about how they want their housing to be like.

If we wanted more affordable housing, and not paying up to 50% of our 'equity' as non-valued added costs, all we need to do is make the right policy decisions, like other countries do, to achieve that.

We have already taken on MMP from Germany, and there are many other jurisdictions that have very stable low house prices which we could follow.

I wonder if maybe Germany is a settled economy whereas NZ is still a growing economy?

Kate there is no empirical evidence of that, that I'm aware of, but feel free to post a link to educate me

Here you go;

https://www.stats.govt.nz/information-releases/household-income-and-hou….

Renters were about twice as likely as homeowners to spend 40 percent or more of their household income on housing costs. For the June 2019 year, just over 1 in 4 (27.9 percent) renting households spent 40 percent or more of their household income on rent and other housing costs. In contrast, about 1 in 8 (12.6 percent) of people who owned, or partly owned, their own home spent 40 percent or more of their household income on housing costs.

And the metric will have deteriorated since then (for the renters that is).

Or, plug into this one;

https://www.calculate.co.nz/rent-affordability-calculator.php

Using NZ's median household income (before tax) of $102,000 - an affordable weekly rent is $490.00.

Thanks for the links. They unfortunately don't show that rent is unaffordable, the calculator especially is subjective. However even if I accepted the calculators results the after tax median HH income would be about 75K. My partner and I can quite happily live with our two dogs (large ones) for less than $600/week including fuel and alcohol. That leaves roughly 40K /yr. I don't know what the average rent is in places like Auckland but even at $650/wk it still seems affordable, although I grant you at $800/wk it gets tight.

We rented out a 4 bedroom plus big office which could be another bedroom. 650 pw. To a 30 something couple with no kids and also no flatmates. The PM said they can easily afford the rent and dont need flatmates.

Thanks HW2 - I'd have to say "what the hell does a DINK couple need a 4/5 bedroom home for?" Air BnB? Gotta say $650 seems reasonable - is that market?

Premium hamilton location with views, possibly a bit lower than what it could be, the tenants are a quiet couple just returned from europe and they love the home, I hope they stay for a long time but probably they will buy their own house. Goodness knows why they need such a big home but the PM reassured us they're genuine and we have met them

They'll need a combined pre-tax income of $170,000 for that price to be affordable according to the calculator.

Is that my place you're talking about.... I think the more you earn the greater disposable income available. Your figures dont add up sorry to say

Yes, based on the rent affordability calculator linked to above.

Dp

You are quite hilarious. Even when provided the proof - you're in denial. The calculator isn't subjective - it's pointing out that based on the 2019 median household income;

https://www.stats.govt.nz/information-releases/household-income-and-hou…)%20was%20%2445%2C744

Weekly rental of $490.00 is affordable.

And as per the link above:

31 percent of households spent 30 percent or more of their income on housing costs. Meaning nearly a third of all households in NZ are living in unaffordable housing.

And if that were not the case - then there would be no need for an accommodation supplement!

Affordability is a subjective measure Kate. If you want to base your opinion on a subjective calculator go ahead. Who said 30% is unaffordable? It's clearly not unaffordable or they'd be homeless. If the Accommodation Supplement didn't exist, nor the WFF payment perhaps rents would be lower. The Calculator IS subjective you just choose to not accept it. Successive Govt subsidies of rent by various means has absolutely driven increases. I personally spent nearly 20 yrs paying significantly more than 30% of my income on housing costs (mortgages), clearly it was affordable because I wasn't foreclosed on, and that was without Accom.Sup. or WFF subsidy.

"Everyone else may describe it as unaffordable but I do declare it affordable!"

Interest.co.nz has a chart for you to look up median rents nationwide;

https://www.interest.co.nz/charts/real-estate/rents-median

According to that chart vs your calculator vs the median wage it seems that rents are indeed "affordable" nationwide.

The thing is Kate there are many people who choose to waste money on "retail therapy" and then claim hardship. There is also a segment of the community who will NEVER own a house. It's been like that since mankind started fixed communities. Upending NZs entire ownership paradigm to serve a limited number just won't gain traction.

Sorry, how do you get that? When the calculator tells us for the median household income of $102,000 (before tax) a rental cost of $490.00 per week is affordable. For the three bed rental from the interest.co.nz chart, we have:

Auckland = $680/week.

Wellington = $675/week

Christchurch = $450/week.

So I only get CHCH as being an affordable rental market based on the median household income.

And it's hardly a "limited number" of NZers in accommodation cost stress. According to the earlier post;

For the June 2019 year, just over 1 in 4 (27.9 percent) renting households spent 40 percent or more of their household income on rent and other housing costs.

That's the thing Kate.. it's your subjective judgement that 40% is unaffordable. It's high, I agree but nowhere does it say empirically that it's unaffordable. They might be under stress but that doesn't make it unaffordable. If 28% of renting households found the rent unaffordable we would have 100's of 1000s homeless - clearly that isn't the case. Auckland and Wellington's figures may be high but they are obviously not unaffordable - people are paying it.

Clearly that is the case - but they're not homeless - they are state sponsored into their accommodation either in state housing; or in temporary housing or on the accommodation supplement;

Here are stats from 2018 for temporary accommodation or shared accommodation (41,644 when added up);

https://www.hud.govt.nz/news-and-resources/statistics-and-research/2018…

And as at 2018, the number of people receiving the accommodation supplement was 279,283;

https://www.msd.govt.nz/documents/about-msd-and-our-work/publications-r…

And we have approximately 70,000 state houses;

https://en.wikipedia.org/wiki/State_housing

So, how's that? Does that satisfy your 100s of 1000s?

I'm not disputing the state sponsorship effect, in fact I personally believe it's a contributor. Let's face the cold hard facts - people in temporary accommodation, shared accommodation or living in garages are highly unlikely to be aspiring to home ownership or if they are it's well out of their reach. That unsavoury fact hasn't changed for decades. I was brought up in a single parent home and we rented all my parent's life (she was a teacher). We lived quite happily, although I vowed never to be in the same situation.

You're right - homeownership will always be out of reach for many - all the more reason why we need a functional rental housing market - as it likely was in your childhood days.

Kate I can assure of one thing - it wasn't easy and wasn't that functional. You need to quit with the hard done by downtrodden crusader mentality. When people can't pay rent - rent will fall, when people can't afford housing - prices will fall. Until then the merry-go-round will continue

Nope, when people can't afford rent, the accommodation supplement kicks in. When people can't afford rental housing (even given the level of accommodation supplement), they go on the state house waiting list.

State housing rental pricing is based on no more than 25% of household income paid in rent. You don't qualify to register on the list unless you can't find anything in the market at 25% of your household income.

Hook sometimes it’s best to just stop digging.

Hook sometimes it’s best to just stop digging.

I will NEVER give ground to disinformation or out of context posts. Kate is so far out of contact with reality it's a disgrace.. that others can't (or won't) accept that is on them. She is an intellectual who hasn't obviously been at the coalface.. doesn't make her wrong but it does make her out of touch

LOL - I'm the one backing up my points with evidence from StatsNZ etc. Where's your evidence?

Crusader Kate is anti-investor therefore rent of virtually any amount is unaffordable.

Your reading comprehension skills require work. 25% of pre-tax income is affordable, over 40% is unaffordable.

Very petty its pretty obvious to a blind person where you stand

Your socialist preconceptions finally reveal themselves. Who made you the arbiter of what is affordable and what isn't?? If people are meeting their outgoings then those outgoings are affordable. Just accept it.

* NEWSFLASH * Boomer hates facts.......calls people who states facts socialist...

**FACTS** Millennial believes what's posted as empirical evidence and can't think for itself. Fails to accept contrarian opinion.

HAHAHAH Newsflash - i'm not a millennial but someone who is sick of the sheer lunacy and societal problems that this country (which i love) is facing from the disconnect caused by ****ing houses being treated as 'investments'. However your 'i'm alright Jack' attitude is admirable. As you were chief.....

I just want to see how narrow the comments thread can get... dont mind me haha

Hahaha good

Anything less than 100% of gross wages for rent is socialism. Altho I love the "I paid more than that in mortgages!" comments that totally ignore the massive financial advantage having your equity growing at the same time that you repaid your mortgages gives you. It effectively becomes a deferred savings account.

Definitions are important. There are a number of officially recognized definitions and Kate is quoting one of them.

But what is not a definition of 'affordable' is paying for something you must have (like a roof over your head) and the expense of other needs, like food, health, etc.

And the increased numbers of homeless, health problems, etc. all point to a systems failure.

"socialist preconceptions"

Swearing off your pension, are you? Or are young Kiwis still expected to fund that socialist blessing?

The 279K works out to about 15% of the total households in NZ - hardly a catastrophic number.

After reading the comments, I am glad that you rent and therefore are poor, Hook.

Not burst and stabilizing is fine and can do but pumping it to new high on a weekly basis is not.

Unfortunately in democratic set up, once anyone is voted bexome the ruler - side affect and NZ earlier thought of labour but JA is national leader in labour.

Most commentators overlooking the fact - if it's a bubble it WILL burst. Otherwise is is not a bubble.

It won't burst until credit lines get more expensive, or hard to achieve. When it looks like that might happen, that's when things will get interesting.

Why do many commentators and experts forget that in last few weeks JUMP was expected as Mr Orr wanted by announcement of LVR from March as many will rush and pay wjatever to enter before

"Mortgage payments are just as affordable for first home buyers as they were three years ago, thanks to falling interest rates"

I think this shows that interest rates are the sole driver of prices. Other factors are just smoke and mirrors.

*i left off higher wages from your headline - how is wages growing slower than prices helping

With house prices going at 5 times wages, wages still have 10 times leverage with a 10% deposit. Percentage wise housing has become more affordable, however deposits are paid in dollars not percentages.

RBNZ is obsessed with pushing interest rates lower. It's a matter of how much this can be pushed until the population breaks.

Well RBNZ has made it clear that it wants the house price keep moving up as the only solution with them but rising up 5% or 10% on a monthly basis is madness and they do not understand that in their zeal have gone overboard. If they want to reduce interest rate, Can do but could have some measure/tools in place to control jumping housing house price like LVR, DTI or some other.

JA and her team is silent as suits them and election is over.

She’s hinted at relaxing the home start grant criteria...as if that’s going to improve affordability *hand palm*...this neglected issue that’s been highlighted again so early in her term threatens to remove considerable shine.

"JA and her team is silent as suits them and election is over." - they're silent because their last effort was an abject failure and they're scared of getting burnt again. The only thing saving them is the "other lot" don't have a clue either. Building more infrastructure to allow expansion (3 Waters, coms and power systems and roading) and then leasing it back to councils might help. Grandiose projects like CRL, Transmission Gully and Light Rail are a waste of money imv

Transmission Gully was approved in 2012 by the National government;

In November 2012, the Cabinet gave the Transport Agency approval to finance and build the Transmission Gully highway using a PPP. The Transport Agency was also given approval to borrow up to the estimated costs of traditional procurement as part of the PPP.

Not disputing who approved it Kate.. given the loose contract and the cost blowout, and now the recent squabble over costs increases what I said was - these types of projects are a complete waste of money. And I stand by that statement.

For a roadway - agreed. For public transport - don't agree.

The billions spent on these projects should have been funnelled into LG loans/leases to facilitate infrastructure repair and builds. Wellington Wastewater and Auckland Watercare spring to mind but there are a myriad of other projects needing funds

Interest rates only have an effect if supply cannot keep pace with demand. There are numerous jurisdictions where interest rates are lower, but because they are allowed to build at the rate of demand, house prices have not gone up.

Even within NZ, Christchurch is an example, where, due to the earthquakes, supply was allowed to meet demand, and there was a great demand, yet prices by NZ standards were relatively affordable.

Lack of supply is what ignites the property fuel price rises. Things like interest rates are accelerants which only work if the fuel is ignited. If supply equals demand, then interest rates have little effect.

It’s actually the change (positive) in volume of credit being lent..you can have interest rates at zero but if banks don’t lend it then you aren’t going to get house price growth.

"Mortgage payments are just as affordable for first home buyers as they were three years ago, thanks to falling interest rates"

But hand in hand with that, you will have fewer debt free years in the latter part of your life than the previous generation.

Life expectancy for the “previous” generation was 68 ish? Most paid off their 25 year mortgages by about 50 ish? Leaving 18 debt free years at the end.

Gen Z have just over 100 year life expectancies ( https://www.futuretimeline.net/forum/topic/17874-how-long-will-generati… ). Assuming they save a deposit by 40 and pay it off by 70. That still leaves 30 debt free years at the end?

I see that other media is now just waking up to the implications of all this money being issued. They are now posting unflattering pics of Jacinda Arden. They are now posting screenshots of some of her old tweets which can be interpreted that she has flexible positions regarding housing. Calls for her to do something, anything instead of looking concerned. Too late, this market has become a bubble in an environment that should be slowing. Ridiculous prices pushed by the RE industry with agent's laughing all the way to the bank. I'm now seriously considering whether my decision to relocate to NZ was the correct choice.

Yeah finally seeing the main stream media having a go at Cindy and the general public getting concerned with what's happening. Even the wealthy seem to be complaining now, poor Hosking wrote an article how he's struggling to buy a home. The pressures on. I'm sure Labour's counting down to Christmas, hoping that this all goes away over the break.

One of those figures (either percentage or value) is incorrect for lower quartile national increase over a year

Thanks Albert. The figures have been corrected. Well spotted.

What about the opportunity cost of locking away cash for 8+ years in a low to zero interest account whilst saving for a house deposit in Auckland?

easy solution... save faster. If its taking you 8 plus years you will find the market has moved again and you'll need more deposit

That’s a pretty simplistic response. Have you seen what housing/living costs have done over that time period? Not all FHBs will have the luxury to fly back to the nest to save their pennies

The problem is everyone is saving faster to try and keep up (be it to save for a house or retirement) all the while removing money from the goods and services economy and slowing the velocity of money. Hence the reserve bank now finds itself in a classic "red queens race".

Lmfao yeah save faster.... what a disingenuous comment but thanks for that.

The tables are calculated on a couple saving approx 350pw. Way back in the 90s we saved 500pw and our incomes were low for the time. It wasnt that hard instead of going on overseas skiing jaunts we went to turoa and whakapapa. We also owned a tinny and had a good time. That decision has been worth those small sacrifices and now we are doing ok

What percentage of income went on rent?

Probably 90 lol

Oh haha... it was about 25 actually

Watch this Albert:

Watch "[PODCAST] Here are 2 proven ways to get rich | Rich Habits, Poor Habits Podcast with Tom Corley" on YouTube

https://youtu.be/VsxDQGQqGRk

Two proven ways to get rich - other people's money, other people's time. End of story. Always has been - always will be.

Have either of those worked for u Hook? Yardney makes it clear that a person's habits and thinking are decisive, you can earn millions but if you frivolously waste it then you are no better off. Also did you forget to mention the internet

Actually HW2 the "other people's money " theory has worked for me. Having said that, investing in the stock market is not without its risks but I've done OK

I could have bought a few rentals but I can't be bothered with the headaches and I hate salespeople (RE agents). In the Hare and Tortoise race I'm more of a tortoise

I am risk averse and actually happy with zero capital gain so long as it's high yield... but the nz property market keeps giving and giving lol

Certainly is generous. Have gone from 25% equity to 60% in 3 years in our first home (according to Core Logic mid range value). If I were to base the valuation on the asking price of an almost identical property (1 less bedroom than ours) then it'd be 75%.

Prices rising 40k from 480 to 520 equates to 8.3 percent only not 19.5 percent as stated in the article. Still high

Thanks Flying High. The 19.5% figure was correct. The annual increase was $85,000, not $40,000 as originally stated. Well spotted.

Flip thats high... and higher than the other quartiles I assume. I certainly did not expect 19.5 percent increase it really shows the level of demand is not being met

The amount of debt people are required to get themselves into a home is crazy. All well and good that rates are low now but as we know the life of a homeloan for alot of these borrowers is 30 years. I hate to think what's going to happen if these rates increase as quick as they've dropped or property values drop as quick as they've increased.

The RBNZ will not let interest rates increase quickly because of that very reason, unless wage inflation also takes off. House prices falling.. why would that happen unless there is an absolute flood of properties onto the market?

Like King Canute?

How much longer can RBNZ manipulate the market, it's not sustainable. QE programme is already mounting to 128 billion & OCR can now only be taken into negative territory. The RBNZ's actions are coming under increased scrutiny with the consequences it's having on society as a whole.

I can guarantee whilst mortgage payments as a percentage of income might be stable, rates, insurance and maintenance costs certainly haven’t been.

Thats right and in some parts of the country insurance costs are becoming ridiculous.

Unfortunately many FHBs would have followed the comments on this site, the bank economists, etc that said house prices have to come down and waited. They might be waiting for the rest of their life now. Just goes to prove that no one can predict the future, I would suggest the opposite of popular opinion seems more likely to be right. Almost everyone is starting to think house prices will only ever go up now, maybe it is now time for the crash. Seems unlikely though with all that boomer cash sloshing around.

Anyone remember the comments when Westpac dared to predict a 7% increase. Turns out that was too low.

Westpac not long ago was also predicting a drop in house prices.

Housing is increasingly New Zealands economy, if house (and other asset) prices don't perpetually increase we would have to face the reality of declining productivity. That's a brutal reality for voters.

Immigration and selling land and houses to immigrants has been New Zealand's economy since 1840. Everything else is just peripheral.

I mean its all speculation at the end of the day isn't it. I personally didn't foresee the RBNZ going full retard but here we are.

Might be an unpopular view, but house prices are demonstrably at the right level for the economic conditions. I can still buy apartments and houses and rent them out at a low (but reasonable) yield across the country, and there are enough buyers with stored equity and a decent credit rating to keep the market buoyant. It will take a change in economic or policy conditions to cool the market - higher interest rates, credit constraints, landlord licensing / property tax etc. Supply is relatively inelastic and is a convenient distraction IMHO.

You won't be popular (who actually cares anyway, popularity is overrated) but you're 100% correct.

RBNZ needs to bring in a 5% deposit requirement for FHBs with good serviceability and a 50% LVR for investors

I think a 5% OCR would be a better move.

RBNZ should allow NZ citizens to create bank accounts directly with them cutting out the AUSI banks. These accounts should be paid Y/Y increases in nominal gdp on a monthly basis. This will give Kiwis a govt guranteed bank account option guaranteed to be protected from real inflation

So FHBs can end up underwater if house prices slip even a fraction? Thankfully our banks aren't that silly.

There are degrees of silliness.

The banks will have cross security against other property (like parents' house) against the potential for any downside.

There are far more people that would look sillier first should a correction come.

The only thing that might happen for the banks is they feel slightly embarrassed they didn't make a record profit this year.

"FHBs can end up underwater if house prices slip even a fraction"

Did you make this claim last year ... yes!

Chirrrp Chirrrp pragmatist goes quiet

That adds so much to the conversation - very deep

No Hook you don't get it. Permabear Pragmist sits there throwing little quips that the market is over-priced and will/might fall. Its just that in his opinion it has "always" been that way which does not make a lot of sense. Stop trying to defend the indefensible.

Oh, is this incarnation #4 now? BLSH, DD and the last one lasted so short a time I can't even recall it.

And your reading comphrension sucks, go back and read what I actually wrote.

Sorry, on holiday down the west coast, Internet coverage is still shit down these ways.

Gee paranoid... you *need* a holiday ... he may be FH but are you FHB

Tillers, a 5% deposit is extremely risky regardless of current serviceability. A job loss, accident or pregnancy could suddenly reverse that ability, plus a 5% downward movement in prices (granted presently that looks unlikely) could easily tip the buyer into negative equity. Maybe a 30% cash deposit requirement across the board would slow things down, but that would be very unpopular and unlikely to happen.

I’m in my 30s and luckily we bought a house in 2014 based off contributing 8% to KS as soon as I started working . My boss is mid 40s and was telling me he bought his first home in Auckland at 105% lending in 2006. 105% lending!!! The bank lent him money for lawyers and moving costs etc. He weathered the GFC and his house has appreciated to the point he has been able to use his equity to buy another 2 properties. What’s keeping people out of the market now is access to that 20% deposit- if you don’t have parents to help then you’re effectively locked out!

And the current financial settings which encourage your boss to grab two houses off potential home owners.

So FHBs can end up underwater if house prices slip even a fraction? Thankfully our banks aren't that silly.

Sorry, pressed report button by accident while scrolling.

The median take home pay is incorrect. The rates of student debt in the 25-29 population are near 25%-33%. Banks will lower the borrowing power markedly based on this and the median couple with student loans would have a weekly take home pay $170 less.

Good point - although I think buying a first home tends to be more like 30yo.

I wonder if a lot of the FHB demand has come from young people who were going to go on OE but now can’t and have decided to get a house instead? Or maybe those waiting for the crash and have realised it ain’t happening. Or maybe it’s just low interest rates.

I know of one example that concurs with your first point

Can anyone honestly claim RBNZ monetary actions are achieving the aims embedded in this statement?.:

“The importance of monetary policy as a tool to support the real, productive, economy has been evolving and will be recognised in New Zealand law by adding employment outcomes alongside price stability as a dual mandate for the Reserve Bank, as seen in countries like the United States, Australia and Norway link

There are feedback effects, very positive ones that in the end leave interest rates moving higher; to the extent that the initial policy actually does stimulate investment and spending, it will also mean rising incomes and liquidity preferences, maybe even the price level (inflation), all of which should combine to pressure interest rates into going only upward.

The result of successful stimulus is higher rates. As back then, today everyone including central bankers seem unaware of the multistage processing. Or they are insidiously disingenuous; they know higher interest rates would confirm their success with monetary policies but in their absence keep calling low interest rates “stimulus” so as to stave off questions about their performance. Link

Scaringly unintelligent statements.

Hmmmm...

Westpac New Zealand extended 62% of loans to housing to record a $3.727 billion increase from last year, while lending to all other categories combined fell. Link - page 22 (27 of 145)

Who needs a productive economy huh?

This really is shaping up as the perfect storm

This whole house affordability thing when actually prices for dumps are sky high makes Buy Now Pay Later look positively financially prudent.

Just because it's "affordable" does not make it a good buy.

But I would know Jack. I'm one of those who didn't see this coming and fair to presume I'll never own again.

My solutions

1. Lock away horticulture land from being concreted over, NOW. I don't care that it can't be sold to developers and that steps on someone's "freedom", we need productive land to feed ourselves. In my humble opinion, concreting over your food basket is about as crazy as it gets.

2. Start from the bottom and work up, build for those in the most need, build appropriate. There are hundreds of large sections with old state houses, some still serving as state houses, it is this land that should be targeted first for increasing density with smaller homes for the most needy among us. It must be acknowledged that some people using these homes will need them long term, some for their lifetime, they should be able to think of even these as "home"

3. Shred our tenancy laws and rewrite them to include leasing more in line with Europe or our own commercial leases, even transferable. Co-operative ownership and shareholding even by tenants themselves could be included. Landlords can still offer houses under laws such as they are now, they will just have the leftovers and less long term among tenants. Too bad.

4. Tax etc laws to favour home ownership rather than investor ownership.

5. Limit immigration to that which we actually need, the last however many years of mass immigration has done nothing for this country in real terms. It is time to acknowledge growth is a limited thing.

Sorry if my ideas encroach on this whole business of every man and his dog seeking to be landlord, that culture's time has got to be over.

We now have one sixth of all housing in this country being owned by people who own more than 20 houses and with more than one third owned by "mum and dad" investors, that is far, far too much of our housing in the hands of investors and we must work toward change.

To me the current tax laws are back to front. If you buy a house, do it up, and make a profit you pay brightline tax. But if you buy it and rent it out and make a profit over a number of years then you don’t. To me it’s the second category that are the real parasites that need to be taxed.

Looks like we need a new political party to promise a capital gains tax so we can then elect them and have them change their minds when the herald does a negative write up.

The second category of people will also slowly over time improve there property in a capital way but disguise the costs as repairs & maintenance to claim the tax deduction & lower income taxes. They then get paid out on these capital improvements when they sell their property.

R & M must be like for like. Remember also losses are ring fenced. If an owner tries to push the envelope too hard their accountant will push back and capitalize the expenses which can't be depreciated. I see the IRD is aware of a large number of people dodging the "Brightline" imposition so it'll be starting to watch that more closely too. If I was a landlord I'd make sure my accounts were squeaky clean for the next while.

Actually the repairs are a legal requirement, leftwing stirrers and rabble rousers decided that it would be better for houses to be improved despite many tenants saying they did not want it. As a result my rent for a furnished house went from 380pw to over 500pw for an unfurnished one. Now we have a PM to do the work for us and its carefree for us.

How about setting 50% LVR for investors and 10% for FHBs?

How about no mortgages available on existing homes for new investors. They are only squeezing out owner occupiers.

The RB cannot dictate to trading banks how they lend or who to. They can only set risk limits, so it's left to the banks to manage the risk as they see fit. Something that seems to be missed in all the noise around the FLP is that perhaps businesses don't actually want to borrow. Housing is a safe bet for the banks - low risk and high return, so they will continue their merry way.

LVRs dictate to banks as would DTIs.

True but those are risk mitigators. They don't dictate who the money goes to (Investors vs FHBs vs Businesses). Besides LVRs etc haven't had much of a dampening effect when they were on

What’s happened since their removal would suggest otherwise

I think it's more the drop in interest rates personally. Prior to the LVR removal there was already anecdotal murmurings about banks being a bit more circumspect about lending. Cheap wholesale money opened the floodgates.

"According to REINZ"

"the national lower quartile house price increased by +19.5% since October 2019, and by +43.3% since October 2017"

Mathematics says prices increased 23.8% over the preceding 2 years October 2017 through October 2019

Momentum was increasing even then

That was the first 2 years of the Ardern Labour Government Stewardship

What on earth did they think was happening

Actually that is not what mathematics says. 1.201 times 1.193 equals 1.433. Mathematics says prices increased 20.1% over the preceding 2 years.

Politicians be reading this article thinking

"So it sounds like the size of the deposit needed will be a key constraint for prices continuing to rise. Think we need to do some work around removing that blocker"

https://www.nzherald.co.nz/nz/pm-jacinda-ardern-hints-at-lifeline-for-f…

Haha.. yeah saw her jibberjabbering about that yesterday. Let's remove the hurdles to the ability of people to pay more and more for a house. A true lightbulb moment.

Careful now. Some people on this website get very upset if you point out that Jacinda is a bit dim.

I think political/regulatory consideration ought to shift focus from housing affordability/house prices to rent affordability/rent prices.

Add a column to the above table with the rental price alongside the weekly mortgage repayment - and you'll see the cost to rent being higher than the cost to service the mortgage.

The government needs to further regulate the rental market by way of price controls - perhaps a formula based around the property's RV - and the price control being renewed every three years in accordance with changes to RV.

We put price controls on the carbon market - why not the rental accommodation market? Quite simple and do-able tomorrow.

https://www.mfe.govt.nz/reforming-nzets-price-controls

The government are gutless.

The trouble is Kate the RV has no relation to sale price and rises with the increase in prices anyway albeit with a lag. A control mechanism would be extremely cumbersome, regional based, open to abuse and evasion, and very complex. Reading some of the comments here from landlords there is already a form of rent control now - the market

The ‘free’ market eh..

All I'm saying IO is that there is a limit landlords can charge - going by landlords comments. I didn't say it was capped. Also if landlords don't provide rentals then what?

Property ownership as a percentage of the population grows. But more to the point, there will always be rentals as not every landlord purchased during the bubble. Only those that have got into the racket lately would need to sell.

"the racket"

Your choice of words belie you Kat

Glad you got it.

Having that biased attitude makes you no better than the other ravers here. Long term it does you no good as you're blinded to effective solutions and the solutions you propose are simply bandaids that produce distortions. Do you get it, No!

Do tell - what's your effective solution?

FH owns multiple properties (significantly more than the typical kiwi apparently). So his views will likely be ‘more of the same please’ as opposed to any type of utilitarian view that might be beneficial for the most people in the future.

I could not have expected anything better from IO...U should really work on your retorts. If you actually want to know I would say to give development the green light and heaps of it. This will please the RBNZ that now has a mandate to maximize employment and also contribute to general inflation then Orr will ease up on interest rate cuts and that will please the govt

give development the green light and heaps of it.

Given new builds will always end up more costly than existing housing, I'm not sure a supply side argument addresses the core problem of accommodation costs for those renting, unless the government regulates such that the state housing metric of 25% of household income be applied to all new rental stock.

This example of a new build/new rental having been linked to earlier;

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

Kate your solutions have been tried and always failed... do you know that in the 1960/1970s there was a massive building boom following high immigration and all the units and houses built then sustained us for decades after. During which the green lobby were slowly strangulating supply. The problems we have now are the result of those who want to regulate every aspect of our lives so please don't promote that as a solution. You also need to consider the effect the new rbnz mandate is having.

FH - have you heard the story about the ant that lived on the bonnet of a Ferrari who thought the whole world was red?

lol in your opinion who is which

Well if you're the successful landlord you probably own the ferrari.

It perhaps becomes a question of transcendence.

Thank you but no, I am more practical.

Then what?

The whole world will end and thousands will be sleeping in the streets...(not)

Exactly. Do nothing about rental pricing and thousands are/will be sleeping in the streets.

Such a mess that we’ve put ourselves in this situation - ignorance and greed basically (in my view)

Keep egging on the govt to take a hard edged approach go on... part of the reason for the current mess is the govts recent law changes which were in response to the activists. I see that private investors who previously self-managed their own properties have been switching to using professional managers... that is having a flow on effect to the tenants through higher rent. Nice moves Kate and others

This is true. Professional managers don't show any mercy, it's all just business. They will arrange to enter the properties regularly and photograph everything which an old school self managed landlord likely wouldn't do.

Managers wont really develop a relationship with a tenant like a landlord would either. If the government wants things done properly then properly they shall be done.

What landlords overlook is that any capital growth above the rate of inflation is a form of yield. If you make this adjustment then landlords get more than enough return on their property, which we know they can draw down on (and do).

Another way of running the numbers is if you take out the non-valued added costs of building a property, which is at least a third of the value of a property.

If you do this, then you can build and own houses for a lot less and the rent can be less but still, return a greater yield. The numbers work well for both landlords and renters.

The

No there isn't a functioning market - at all.

Many, perhaps most, renters are paying 50%+ RTI ratios. That's unsustainable.

Secondly, the government intervenes to the tune of $2billion and rising per year by way of subsidising the market.

In a properly functioning market with no taxation on either realised or unrealised capital gains, the cost to rent ought to be below the cost to own. It isn't all that long ago in NZ when that was the case. And so it should be.

In a properly functioning market with no taxation on either realised or unrealised capital gains, the cost to rent ought to be below the cost to own

I agree Kate. But this is an epic property bubble. You know when it is when the ruling elite don't want to utter the words.

No kidding - epic.

Here's an example of the type of buy-to-let going on in the Hutt Valley.

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

According to this calculator - a household income of $190,000 before tax needed for that level of rent to be affordable.

Not saying no one would be able to afford that - but with that kind of income, they'd likely be buying their own anyway.

You'll probably find these will become emergency accom.. the govt is paying over 200 per night plus gst to house the untouchables. Yes there are plenty of families and individuals who are too troublesome for a standard rental and that was before the 90 day notice provision was removed.

So set the control on some other measure then - perhaps Rent-to-Income ratio. Landlords will need to reduce their prices based on that formula then. Many ways to skin a cat, Hook :-)!

Having the State meddling in a commercial relationship is a dangerous road to go down Kate, once embarked on there is no turning back. We've all seen what happens when the State sets payrates - Teachers, Nurses, ECE teachers, lots of grief there

WFF. Accommodation supplement.

Agreed. Both those have contributed. As has raiding KiwiSaver and Home Start grants. Short term electorate bribery fanning the flames. To reduce prices the ability to buy needs to be reduced not enhanced. Unpopular but essential.

Muldoon did it. We can do it again

On the first oil shock Muldoon introduced price controls on everything and established a Price Control Tribunal. Products were categorised as either Category "A" for large businesses such as Fletchers who were subjected to margin controls and returns on capital. Category "B" were all the small businesses who could raise prices only to the extent they had incurred increased costs. They could not increases their margins. If Landlords were subjected to such controls today they would have problems if they were negatively geared because most of them have had the benefit of substantial reductions in their largest cost - interest on mortgages. Fairly sure if Muldoon was still around today he would institute such a rent control - and do it retrospectively - rents would fall immediately. Strange thing is, the digital world has no record of it

Oh for goodness sake - appropriately regulating a dysfunctional market is hardly meddling in a commercial relationship, Hook.

Just say it Hook... she’s a raving socialist

So, MLSmith, you'd rather see tax transfers over proper regulation as the means to sort out the rental market failure?

I do get such a kick out of crony capitalists that label anyone against crony capitalism as a socialist.

‘The government are gutless’

And in a democracy they are just a reflection of society. We’ve had ample opportunity to do the right thing/s the last 10 years. We haven’t...each opportunity we’ve decided to take the easy road and the destination of the easy road is hard times. It’s a common theme throughout history.

To my mind, there isn't an easy road as compared to rental price controls. The only other viable solution is to build state houses at a faster rate - FOREVER - to convert folks from unaffordable private rentals to affordable state rentals where rent price is based on a ratio to income. And given the need is never ending as wages continue to lag house price inflation and more and more become unemployed, the state also has to continually increase the amount of subsidy into the private rental market.

That's pure madness in a resource constrained world.

Yip agree - build away I say and now and for a long period of time.

I've got an even better idea - restrict immigration to 0 and restrict family size to 1 offspring only - problem solved. Oh wait.. that's been tried elsewhere and didn't work well.

One day, some time in the future, when the dust is settled, and the pain is over -

NZ will regret forever its immigration program of the last 20 years

Thomas Sowell wrote a book Basic Economics in it he goes in to great detail about price controls and why they don't work. I thought rent control would be a good idea untill I read this book.

One missed metric: total repayable capital.

With wages not nearly matching house price rises it will take years longer to repay debt. Meaning lots more leveraged debt available to banks who class debt as an asset.

Interesting: no comments on this article from the buy

Now regardless set

Probably too busy at open homes getting in before the LVR restrictions

More like.. too busy meeting agents and listing their slumlord rental properties, desperately trying to dump them on unsuspecting Newby investors who don't realize how strict the new healthy homes standards are.

Or, just maybe those buying are that little bit smarter than those commenting here? Who has a track record here that would warrant me paying any attention?

I have a healthy distrust of politicians and corporate leaders and it has served me well. The fiat currency's of the west are being debased at an alarming rate, so all the talk above of DTI, debt, returning capital is completely missing the point - which is that you are putting all your faith in a piece of paper.

Adrian Orr and Jacinda have decided that it is preferential that a millionaire who owns 20 properties gets a tax free capital gain of $200k x 20 = $4 million in less than a year when a renter gets nothing except for a rent rise?

The naïve and the greedy who get excited about a $200k rise and only own one home benefit only partially but seem to feel that this rise makes them somehow "better" than your average renter.

The only actual winners are the investors and speculators. I wish the ordinary home owner could see how their own greed is being manipulated by the real winners.

The whole arsenal needs to be thrown at this situation. Prices need to come down so that people can see that houses are not bulletproof. The invincibility lie that Orr has pushed is a big cause of this hyper bubble. We need a crash and we need it now.

The greedy investors and speculators will shout how this will harm everyone but what it will really do is level the playing field and everyone will have an equal chance. It is analogous to a small sapling trying to grow in a tall forest. The Big trees block out the sun and prevent the sapling from growing. However, if all the trees are felled, every sapling gets its time in the sun. Equality can prevail !!!!!

There are a lot of wolves in sheep’s clothing here in Nz

100% correct..... and some of those wolves have really nice smiles and are ever so good at looking concerned.

nailed it

{kind=link}

"However, if all the trees are felled, every sapling gets its time in the sun. " - haha.. yeah right! Ever seen a clear felled block? It's a barren wasteland. When the big tree falls it crushes every sapling in its path. Selectively removing the big trees helps but how can that be done?

What a lot of the HAVES like yourself don't realize is, that if you continuously lock people out of the benefits that the HAVES keep on getting then the HAVE-NOTS have got nothing to lose and do not care if the system collapses. In fact if it does collapse they have a better chance of improving their lot.

Yip the French Revolution keeps coming to mind when I look at where we find ourselves. Ignorant wealthy people promoting their own interests and expecting the poor to keep playing along. History would suggest they won’t

Right - I think property owners forget that they only own (have control over) property because of the acquiescence of non-property owners to a system which protects property rights. If enough people stop respecting that system, you no longer really own anything. Put it this way: if one tenant stops paying rent, and refuses to leave, you can evict them. But if every rent payer does? There aren't the resources to evict all of them.

Adrian Orr and Jacinda have decided that it is preferential that a millionaire who owns 20 properties gets a tax free capital gain of $200k x 20 = $4 million in less than a year when a renter gets nothing except for a rent rise?

Remember when the investors of South Canterbury Finance were bailed out when the Blue Chip and Hanover punters were thrown to the lions? Do you know the difference between the investors of SCF and BC / H?

Interesting. Who are left supporters going to blame this time? Indian sounding names???

Boomer sounding names this time

Leader should not have ego. If can take U turn for something that you strongly feel and politucal opposistion did not allow, WHY cannot take U turn again and do what ine believes unless thinking has changed and now like John Key - housing crisis is a good crisis.

Rise and show leadership by doing what is just and required :

https://i.stuff.co.nz/business/opinion-analysis/123456016/ardern-should…

Speculators paradise. It is interesting to see rule alone Labour continue to do nothing, and increasingly screw over its core voting base. Perhaps they are rental property investors like National.

It's a bit like winston calling out immigration at no more than 10000 per year. Where is he now?

Affordable? Not what I've seen. In Christchurch, properties with a RV of $530000 are selling for $720000. No bank would agree to loan you the funds to purchase a property that over-priced. Certainly not with only a 10% deposit.

If you think they might, you got to pay them $600 for a "special valuation". You take a good look at the property, and you'll find it's just not worth $720000, but that's what you got to pay nowadays to secure it in this very heated and competitive housing market. Same with every other house price out there at the moment. You're just paying through the nose.

It's like buying a second-hand car for $10000, only to have the insurance company tell you the replacement value is $8000, but you can give it a good clean, take down the fluffy dice, replace the floor mats, repaint the bumpers, and sell it next year to some other muppet for $12000. Only to have their insurance company tells them its worth $7000.

It's crazy and it's got to stop.

Chch is still flat from what I can see- houses still selling at GV and you can still buy a 4/2 house 10 mts away in Rolleston for $549k

Does anyone know any recently returned Kiwis who are leaving again? I came over 3 months ago with the intention of buying a home but these house prices, actually, not just the house prices but the total contempt shown by Adrian Orr and Jacinda and the greed of the investors has made me feel quite sick and I don't want to be here anymore. I think I have gone off kiwis. Listening to all that team of 5 million BS and then seeing a large number of those 5 million try and shaft the very people who gave up, on many occasions, their jobs and futures has shown me a darker side of NZ.

As I say above, NZ is all about wolves in sheep’s clothing. We think we are very nice, but appear blind to our dark side personality/character traits.

Out of interest what country are you thinking about moving to? Seems that most western nations are seeing similar trends. In Aussie its somewhat masked as apartment prices are stagnating, house prices are going crazy. Perth/ Brisbane are relatively affordable compared w Auckland, but Sydney/ Melb are off the charts.

I am heading to Ozzy first. Gold Coast has amazing houses for great prices so will look at buying there or maybe even give Perth a go, its so cheap over there too and plenty of work. These prices are just unjustifiable in NZ and the houses are so crap. What u can get for $500k in NZ would cost $50k in the Gold Coast, thats if it would even be legal to sell such junk over there?

I have two friends who are returned Kiwis who decided against sticking around. One is an expat Kiwi who worked in and is now retired with a base in Singapore. He came back here but doesn't like what he is seeing and will return to Singapore in late summer with a view to relocating to Thailand. The other was based in Hong Kong. Who is an early retiree who was messing around sort of biding his time there. He came back, lasted 3 months and has headed for Singapore and is biding his time for somewhere else in Asia to open up. They each had their reasons for leaving and it was a combination of things.

EarlyRiser.. I was based in Thailand for 22 years till a year ago. Met so many Westerners who had come for a holiday years ago and never left. All the big things are great. Wonderful friendly people (but don't marry one), amazing food, never cold, great beaches, very cheap and easy lifestyle and best of all almost total freedom to do almost whatever you want. Very safe too (except on the roads).

It is a dirty, polluted, overcrowded (in many places) inequitable dictatorship where foreigners can't buy a house but for most men these are minor negatives. Beats anywhere else in Asia hands down.

Most men?

Pocket Aces.. yes there are some things that, as a generalization, are high priority or maybe more to the point upsetting to women but often of much less importance to most men. Some good examples would be the open sexism, the very unPC jokes, dirtiness and pollution, animal cruelty and of course prostitution. If those things are going to seriously upset you living there would be the nut low. There is some fantastic high stakes poker though.

interesting perspective.

Spent 20 minutes in two open homes today. Not even one other viewer and nobody on sign in sheet. High end houses and was raining, but still.

Thank goodness, nicely summoned article, low record OCR and will still go to negative, our wages increases by subsidy factor and FHB deposit help from govt. - there could never be a good time to buy the RE to settle down for the newly graduate workforce specific quota numbers, for some though it's better off across the ditch.

Mortgages the same price but existing homeowners get a free wealth boost. No downsides confirmed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.