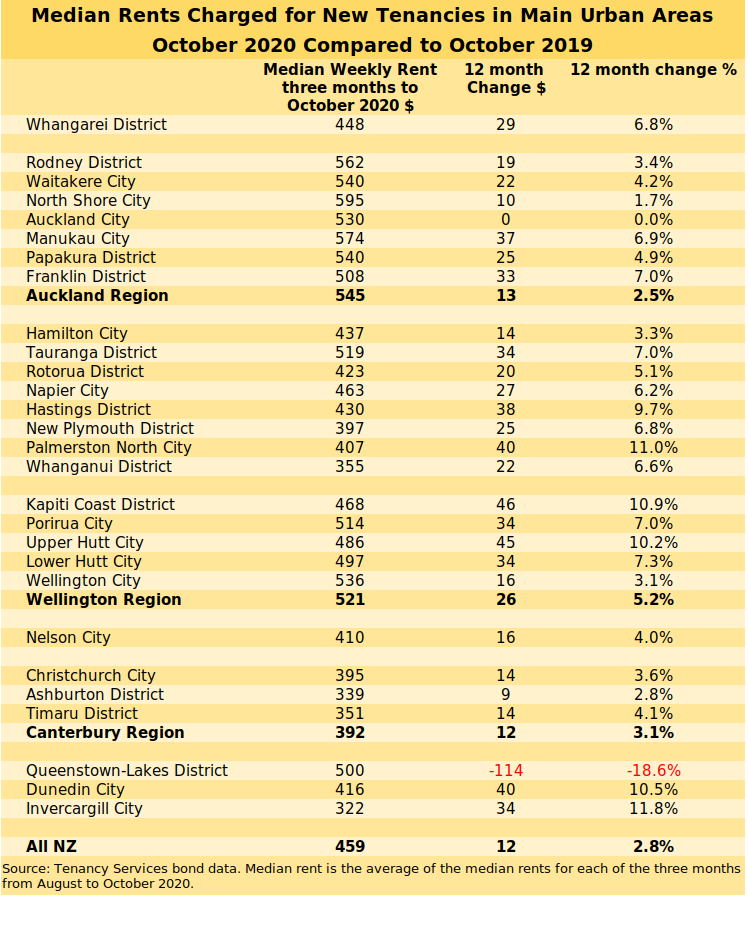

The median rent for newly tenanted residential properties throughout the country increased by $12 a week over the last year, according to the latest bond data from Tenancy Services.

The median rent for all bonds received by Tenancy Services over the three months from August to October was $459 a week, up $12 from the same period of last year, giving an annual increase of 2.8%.

However there were some significant regional variations, with five districts having double digit percentage increases - Palmerston North, Kapiti Coast, Upper Hutt, Dunedin and Invercargill.

Only one district showed a decline in rent over that period but it was a substantial one.

The median rent in Queenstown-Lakes declined by $114 a week, from $614 over the three months to October last year to $500 in the same period of this year. That's down 18.6% compared to a year earlier.

There was also only one area where the median rent was unchanged from a year earlier, - Auckland Central which includes the city's CBD and leafy inner suburbs, where the median was unchanged on $530 a week, most likely reflecting weakness in the apartment market.

Rental growth in the main centres was weakest in the Auckland Region at 2.5%, compared to 5.2% in the Wellington Region, 3.6% in Christchurch and 10.5% in Dunedin.

Of the main urban areas, the most expensive rent was in Auckland's North Shore at $595 a week, while the cheapest was in Invercargill at $322 (see the table below for the changes in all main urban areas).

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

58 Comments

Well that won't cover for hyperinflation in property prices, I can see many investors getting out since wages won't cover for their investments to make any profits.

b21

Note: B21 edited his post slightly since I wrote this.

Not a valid conclusion: no reason for investors to get out at all.

With increase in rents their yield on their initial capital investment has just got a little better.

They will be also be very happy knowing that not only over time will their yield on their initial investment be increasing, but also that initial capital investment. And its looks like Orr's actions are pretty bullish as to housing.

So every reason to stay with it; and no purpose in cashing up - such as putting it in term deposits - where one's capital is fixed and the returns likely to show some downside.

Your comment seems probably been driven a hint of envy rather than rational thinking. ;)

I did not, I finished editing it before there was any answer to it and not in any meaningful way that would change the message. The timestamp is there to confirm what I say since it gets updated after every edition. Stop lying.

Hi b21,

Advice to you: "When you're in a hole; quit digging."

TTP

TTP? Forgot switching accounts? Again? :)

I think he has multiple accounts so he can uptick his own posts (because nobody else wants to). And this is from TTP who is always changing his posts after people reply to him! The hypocrisy...

b21

Not a problem. While writing my comment you edited it to include reference to wages.

However, as said; no problem.

But as you now include mention of wages; those renting are (unfortunately) currently facing increasing rents while those recent FHB are likely currently experiencing falling mortgage interest rates as well as capital gains.

Bottom line, contrary to your assertion, the reality is that things are positive for both landlords and recent FHB will be pleased. The reality is that sadly, renters are finding increasing rents and getting further behind with house price inflation. You can't put any other spin on it such as you are trying to do. ;)

Haha coz what you wrote before was pretty much saying there is no need for LVR :D

Not true either. Just for the record this was the original message:

"Well that won't cover for hyperinflation in property prices, I can see many investors getting out."

Stev-O

Not sure who your comment refers to.

If me, I support and see urgent need for LVRs along with other measures to cool the housing market; I see this as a need in conjunction with other things including targeting FLP for businesses only, no OCR cuts, and as posted numerous times, a need for a CGT.

What I have recently said is that LVRs for investors are seemingly less effective than both other factors and what many think.

Introduction of LVRs affecting FHB - even at a considerable lesser rate than for investors- would have considerable impact on that group.

I presume peoples wages will be going up a comparable amount (2.8%) for the year too?

Nah. Most employers use CPI when negotiating wage increases in NZ, not just housing costs.

Such an increase in the housing cost component of CPI will be offset by cheaper electronics, fuel and apparels due to higher NZD/USD.

I know quite a few companies that did not give employees their annual increase due to covid - despite not being in danger of any decrease in revenue, citing solidarity with the rest of the country. They have no plans to take this in to account at their next annual wage review. I am more concerned about people truly struggling in far worse situations than this, but I do think it is very unfair, when you look at the effect this often has on their lifetime earnings, particularly those in lower paid positions and still renting, facing the brunt of increased living costs.

Seems like the too much effort in the employment sector goes into looking for reasons to not pay proper wages.

Parties on both side of our political spectrum support our businesses in their wage suppression tactics.

Even virtue-signaling Cindy ran a campaign on fair pay and representation for local workers, while her agencies were quietly chugging out thousands of 'skilled' visas to low-value migrant workers in the middle of a recession.

Net rental yields nearing zero (if there's a mortgage on the house). Capital gains or bust for many retirees.

CourtJester

Despite your glee - another fallacious comment. :)

Not sure how you calculate rental yields nearing zero for retirees. Most retirees have long got rid of the mortgage - or after a number of years it wold be very small and with falling interest rates repayments will be a lot less - on their investment property.

The reality is those retirees looking at funding their retirement with an investment property will be now looking at considerable yields on their initial investment - plus considerable capital gains to boot.

Likewise those investors who have purchased over the last few years; they have seen increasing rents, improving yields on their initial investment, and considerable (tax free) capital gains.

You won’t like it, but both retiree and more recent investors have probably been to leverage for another property.

So the reality is that both retirees and landlords are very, very happy so no need for you to be concerned at all.

Whether one likes it or not; the reality is that those with property have done exceptionally well and especially including during Covid while those renting have seen continuing rent increases and homeownership getting further out of reach.

Like B21, your comment I seems driven by envy.

However, as you have previously posted you could afford to buy a home; you haven’t, that was your choice, so the consequences are reality of life.

Cheers :)

I'm talking about people who retired recently. I'm not arguing that people who bought years ago made a lot of money - yet you keep bringing this up.

CJ

Much appreciate your concerns but most retiring recently bought sometime ago.

Even if they bought recently (especially just a year or two back) they would have looked at yields on the property when they purchased it.. Since then the only thing that has happened that is going to affect their capital invested is that rents have gone up and mortgage rates down - so their initial yields have improved. You need to look at returns on your initial investment - is much like a long term term deposit with the only difference is that one’s capital has unlike a term deposit increased considerably.

Honestly, currently no need to get yourself upset about recent retirees or other investors and the outlook seems bright with increasing rents, downside to interest rates, and given Orr’s attitude, likely increasing capital gains.

To argue otherwise is denial of reality.

Cheers :)

I guess the question is what can people who have retired recently do to get more yield on their money?. Term deposits are fairly abysmal. Buying a rental property may be an option.

If you had 400k to invest you could buy an 800K property with 400k interest only mortgage and rent it out at $550 a week and get about 2-3% on your 400k after expenses. The total asset of 800k should keep up with inflation as well.

You may get similar returns with index funds. I'm going to try this as have been and done property.

What would have been interesting is the 6 month and 3 month changes - as my observation here in the WGN area is that both those would likely be 10% plus and rising.

What the stats above do tell us though is that the worse of the rises are coming off the lowest base; i.e., the areas traditionally suited to the lowest quartile wage earners.

Get in there quickly Kate, this one won’t last long.

https://www.nzherald.co.nz/nz/wellington-flat-labelled-an-800-dungeon/M…

Thanks for the link - I rest my case :-).

What a sad little country we have become.

We can blame consecutive governments, but we get the governments we deserve....

Could do with a lick of paint...

But it's an investment! You're not supposed to spend money on it!

Almost word-to-word quote from a wannabe landlord when I asked if he'd get that ugly patch on the wall painted before I rent his place.

Correct, its pretty sad seeing the poorer areas being hit the hardest, all in the name of better yields.

Can anyone think of any major negative impacts of a long-term rent freeze? Would assist people who need it most, much of the rent saved would go back into the real economy instead of to investors, many of whom use the rent increases to purchase more property. Govt saves on accommodation supplement too.

And before anyone says some landlords would just leave properties empty reducing supply just implement an unoccupied property tax too. Together with slashing immigration these measures would make huge inroads towards solving the problem. Why not??

Because those with the power to do anything at a policy level, do not care to. It will most likely come down to the people most affected, finally getting fed up enough to band together and refuse to play by such unfair rules any longer. I hope we relearn the importance of Civil Disobedience here and change our course peacefully. Because if nothing is done about the disgusting inequality in this country, it will be the landlords getting put on ice soon enough.

Rob Muldoon would have been a fan. Could do the same with food, petrol, electricity, etc too.

But aren't we trying to encourage inflation!

Market rents at the moment are unaffordable for many - it's why we have such a rapidly growing state housing wait list. State house rentals are set based on being set at no more than 25% of the household income. And many if not most on the waiting list are working families. So, what you really need is to set a weekly rent maxima formula for private sector rentals that works to around a 30% of household income at the lower quartile of household incomes.

Based on median household incomes, as at 2019, 31 percent of households spent 30 percent or more of their income on housing costs. It is this end of the spectrum that regulatory measures need to target. A rent 'freeze' simply locks these households into difficult situations - hence the need for food parcels; emergency payments from WINZ, etc.

I do think we need to focus regulatory policy on lowering the cost-of-living in this big-ticket area, as opposed to increasing benefits/social assistance.

Why state should set prices for private sector? the only argument the state can have is to show private sector that it can do what they cannot: offer housing at an affordable price. They (the government) already have the formula too. The income of tenant determines the rent a tenant pay.

They must ramp up their state housing supply. This will both controls market rent prices (it will surely bring it down) and also will create a platform for building cheaper houses for aspiring FHBs. But no, that would require the government, with the crazy amount of power and money that it has, to actually prove that private sector prices are wrong.

Why state should set prices for private sector?

Because it provides an accommodation supplement to private sector landlords. I suppose we could exempt landlords who whose tenants are not subsidised. It's a good thought..

No one forces them to pay subsidies. This a flawed argument. As mentioned, government can justify significant involvement in supplying rental housing to the market, as private sector is leaving many behind. The way to do this is to increase their housing stock. Not to tell others what to pay. No one forces government to pay subsidies. they chose to do it.

Why stop at rent freeze? if you can tell people how much they have to take for what they offer, this should apply to anything. Why should we not freeze dentist fees? surely having healthy teeth is very important. Why we cannot "freeze" price of healthy meat and vegetables? surely cheap healthy food is vital for people who need it most and will help us having a healthier economy. Why we do not freeze energy prices?

Please do not get me wrong. Expensive housing is an undeniable and very strong pressure for many many people. I feel the same for healthy teeth and healthy food. I think given the inability of private sector to provide these essentials to many at an affordable price, NZ government can step up and compete in offering them at an affordable price. But to tell everyone what is the price they have to accept for their services is mad.

We did freeze dentists fees along with everything else in 1982 because the Govt felt it was best for NZ as a whole. Surely it is now best for NZ as a whole for the Govt to freeze rents for a significant amount of time. What is mad about it? I personally had Akld properties for 25 years and never increased the rent on a tenant once. Of course many stayed several years, hardly bothered me and almost always paid on time. Many (but not all) landlords now seem to lack any empathy and compassion towards tenants.

A rent freeze only is best because the property situation is causing a massive divide in society. The cost of dentists and other things is not.

The cost of dentists is not? Mate, get back to the real world.

Pragmatist.. if you think the cost of dentists is creating a social divide between the haves and have nots YOU are certainly not in the real world. The majority of people do not even need to visit a dentist once a year. Not even sure why I bothered to respond to you TBH.

So in a way this is good news right? We want inflation and this should have reasonable impact on the CPI shouldn't it (with housing being such a major part of people's spending)? Maybe we won't need any more rate cuts...

Sorry to burst your bubble but I’ve just bought a rental with a 30% mortgage and the net yield is 4.5%

Just curious, are you accounting for insurance, rates, maintenance and vacant periods in that calculation? How about opportunity costs on the deposit? Starts getting skinny when you put everything in.

B21. Where will people with spare money go? Property is the only investment with some sort of hope of yield at present. it staggers me that there are still some people who cannot see this. Old people still remember the '87 crash, when absolutely everyone in NZ got burnt by Alan, Rod, Bruce, Bob, Ron and a few of their mates, and so are reticent about going near shares again. The Aussie owned banks give us a really crap return, and shovel all our fees back to Australia quicker than a croc going for a Pommie backpacker swimming. The shortage of rental houses has never been sorted for donkeys' years, so in we all go. There is literally nowhere else.

If people expect property investors to derive their return from income yield and not capital gains, then rents are going to have to go up a lot more than that.

Tell you what I am expecting, and that is measures are taken to see to it that housing is returned to what it is supposed to be, homes for people, not a never losing casino for speculators and investors.

Residential Property investing seriously needs to become a thing of the past, beyond specific, permanent leasehold properties and a few short term rentals for those who need them.

Massive state house build to remove the people needing much more affordable living from the predator market is the best start imho

Well said. They should be homes for people, not a form of investment. We need a high rate of home ownership, easily accessible to all who are not specifically wanting to rent - which would no doubt be far less people if the pathway to ownership were not so difficult for so many.

More and more people are starting to expect property investors to stop leeching off others and start investing in something productive.

And if people cannot afford the increases, they will sell and homebuyers (owner-occupiers) do not need the capital gains.

I don't see a problem.

Two ways to square that circle - either rents can rise or house prices can fall until the yield is respectable.

What a co-incidence. The PM just sent me an email about the Government's three priorities and closed by saying:

"Do let me know what you think - as ever, I’ll make time to ensure I read as many of your replies as possible.

So I replied with my #rentcontrolnow suggestions. Last time I wrote to two Ministers during the election campaign and the next day, Labour came out with an announcement that partially addressed my concerns.

So, here's hoping!

Might as well make it public!

Dear Prime Minister

On the issue of housing, I believe the regulatory initiative/focus should not be on lowering the price of houses per se, but rather on lowering (and stabilizing) the cost of rent, with a particular target for policy effectiveness at the rental market for lower quartile household incomes. The regulatory initiative would be to set rent price controls (not a rent freeze), as a weekly rent maxima formula that is applied universally to

all rented properties, both existing tenanted properties and new-to-market rental properties.The easiest formula to apply could be to base a rent price maxima on Rateable Value (RV). My cursory look at it, suggests that a universal formula might be, RV/1000 = weekly rent price maxima.

It may need to be tailored differently on a regional basis given RVs are reviewed three-yearly. My consideration has focused on the Wellington market where the RVs were updated in 2019. As RVs are reviewed every three years, CPI could be applied as a rent increase maxima during the intervening years. Such a universal maxima would specifically target regulatory relief to lower quartile income households, who typically rent the lower quartile residential dwellings (this is where I am seeing the greatest percentage increases at the moment). Many upper quartile residential rentals presently charge less than the maxima – as these prices at the higher end are more aligned to the market’s ability to pay.

It is the lower quartile that is most affected by inability-to-pay, and hence unaffordability (i.e., rents equating to more than 30% of household income). According to your Government’s studies;

“At a national level, the share of renter households spending over 30 percent of their income on housing costs remained fairly constant at 31.0 percent in December 2018 (31.3 percent in December 2017).”

https://www.hud.govt.nz/news-and-resources/statistics-and-research/hous…That data is before y-o-y data on average rental cost increases for 2019/20 has been taken into account;

https://www.interest.co.nz/property/108127/rents-auckland-13-week-compa…A rent maxima based on a formula associated with RV, has the following benefits:

• A formulaic approach that can be calculated based on already publicly available information.

• Lower quartile properties may become less attractive to property investors, hence taking the ‘heat’ out of the low interest rate housing market, and subsequently giving first-home-buyers (FHBs) less need to compete against the tax advantages afforded to investors.

• Lower rents allow renters the opportunity to save more for a home deposit.

• Should property investors in the lower quartile end of the market exit those businesses, the Government might want to instruct Kāinga Ora to purchase more private homes for State house stocks, in a manner that ensures that it does no displace or compete against FHBs or downsizers. (A number of days-on-the-market might be a metric for such purchases).

• The government need only review Accommodation Supplement maxima (which I believe is set regionally) every 3 years with the corresponding RV reviews.

• No tax changes are required to implement.

• The initiative would be welcomed by NGOs working in the area of inequality/poverty.

• House prices in the lower quartile should remain static, or possibly decrease with the introduction of the rent maxima.

• New builds should not be affected, as the market for new builds has largely been targeted at individual homeowners in the mid-upper income quartile (one of the problems with new development: the private sector is not interested in low-income housing as the profitability is lower).There might also be a need to concurrently review QVs methodology of residential valuation for the purposes of rating (RV) which is presently based largely on market price paid in the surrounding area. With market prices spiralling out-of-control, every property, whether prior sold or not, has its rating valuation lifted. I have always preferred a rating methodology that recognises, not market prices (dollar value), but instead on the value of public amenities in the neighbourhood area and the proximity of the property to centres of employment and/or public transport services. A number (i.e., points, not dollar) scale would be far preferable to a dollar value scale. The dollar value scale simply fuels property price inflation.

Some good points there Kate and I happen to agree with you on your maximum rent formula. But if the PM has time to read that, I will be surprised.

Thanks for your comment! One of my grand daughters drew a lovely picture about plastic pollution in our oceans a couple of years back. I suggested she write some words around the drawing and send it to the PM to tell her about her concerns - which she did and we posted it off.

The reply letter from the PM was amazing - directly commenting on the drawing and explaining she shared those concerns and what her government intended to do about it. Language perfect for a 9 year old to read/comprehend. It's a prized possession of hers now. We laminated it and she took it to school - the teachers too were amazed.

She grew a lot of fans with the gesture :-)!

If you did your homework rather than just pushing your wheelbarrow you would know that rent control basically decimates the new build market. No new investor wants to pay to build (or buy) a house that is then subject to rent control. You can kiss goodbye to all those property developers who build for property investors, particularly those using foreign money. No one will invest in housing in NZ. The result of no new investment is to make rental property scarce, which is fine for those already tucked up in rent controlled houses but for anyone who is looking to leave their parents home or have arrived from overseas - finding a property to rent is impossible.

And if you want to see real life rent control markets in action - go watch HGTV and one of the House Hunters International shows. Time after time, episodes filmed in places like Sweden show just how difficult it is to get a rental property. I remember one episode where the RE agent basically advised them that the only way they would find a place is if they know someone personally who is looking to rent out their property, as empty houses only to go to friends and family.

https://www.austriancenter.com/rent-control-has-failed-in-sweden/

And another side effect, as this article shows, a roaring black market in subletting at humungous rents to desperate people develops. If you think cramming 8 people into a house is bad, wait until its 8 people per bedroom.

All depends on the design of the regulation;

https://www.ft.com/content/efe1f74c-3c1d-11e9-9988-28303f70fcff

(and where you do your homework).

Q/town soon will lead as a good example, pre covid, average rental is $750/wk, covid hit bang! to $600/wk, subsidy arrive, bang! is up back to $700/wk - now variant above of down $114/wk is relative to flexi-subsidy stutter. The RE lobbyist soon able to ask govt. for more permanent flexi-subsidy anticipating the vaccine roll out, removal of bright-line test, keep away in the box that LVR (banks are prudent enough..wink, wink), negative OCR and special FLPs flexi door opening for Q/town housing investor, and more QEs. Remember, NZ economic wealth barometer for North Island is AKL and for South Island? is Q/Town (used to be Chch tho)

People here calling for rent freezes are surely on the wrong web site. Please toddle off to a place where your comments will be appreciated.

Readers want to read about good returns on our investments, be they rental properties, shares, bitcoin, businesses etc.

Your head must be stuck up some dark place. The comment section here is constantly full of people who are calling for and discussing ways to make returns on property investment less profitable for the good of our society. Judging by the amount of comments and the upvotes they receive, many readers want discussion around this and not just information on good returns. Do you speak for Interest.co.nz? If this website does not want us here, they can tell us directly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.