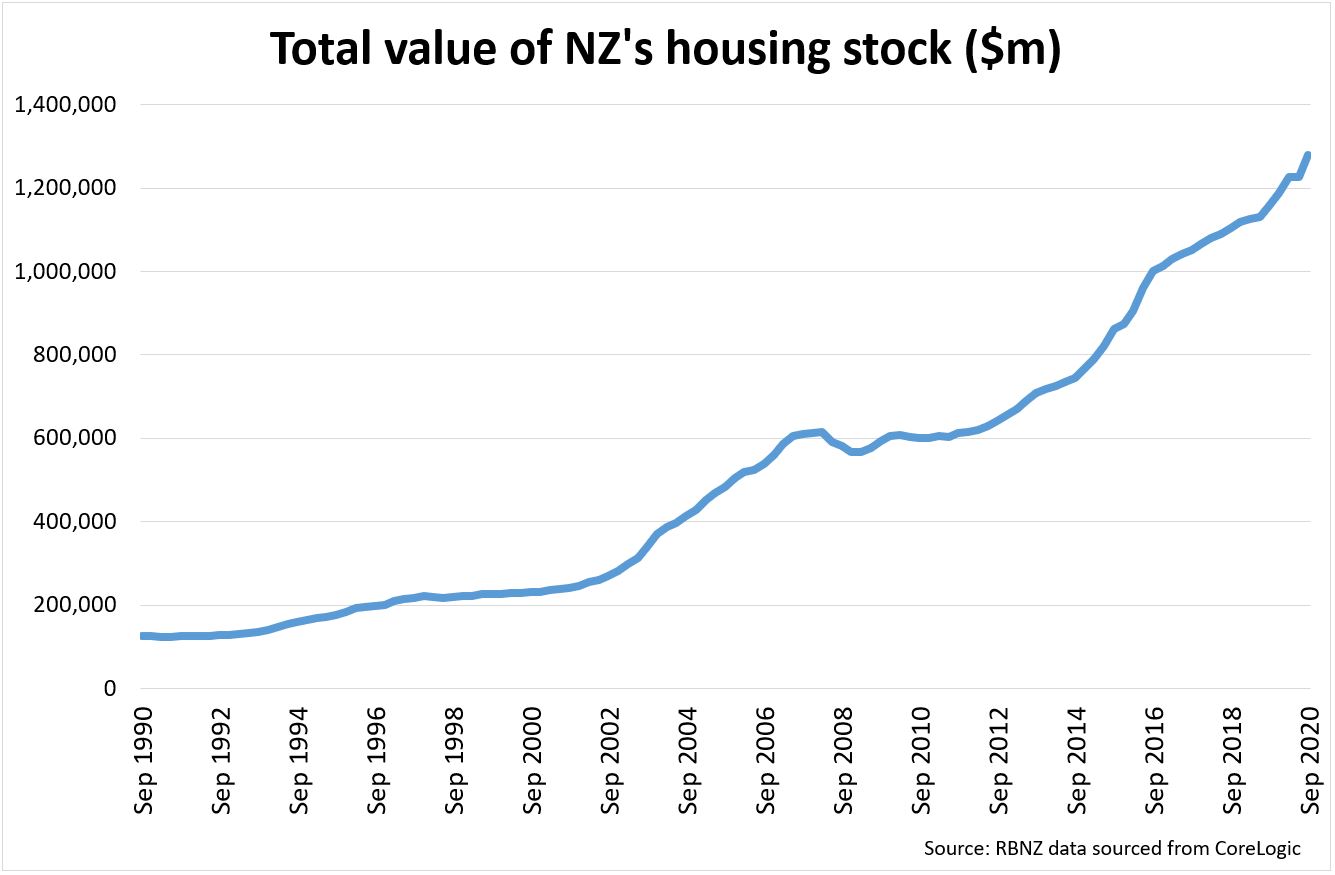

New Zealand’s housing stock is worth four times what the country’s economy produces in a year.

CoreLogic data, just published by the Reserve Bank, shows the value of New Zealand’s housing stock reached $1.28 trillion in the September 2020 quarter.

New Zealand’s annual Gross Domestic Product (GDP) is $321 billion.

The value of the country’s housing stock increased by 10.7%, or $123 billion, from the same period the previous year, and 4.3% from the June 2020 quarter.

Both the quarterly and annual increases are the largest since 2016.

The country’s ‘housing stock’ includes all private sector residential dwellings (detached houses, flats and apartments), lifestyle blocks (with a dwelling), detached houses converted to flats and ‘home and income' properties.

93 Comments

Is this responsible RBNZ regulatory oversight?:

Banks extend 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive, to do so.

Or this?:

RBNZ cutting OCR in half five times since July 2008, causing the rich to capitalise rising discounted present values of future unproductive asset cash flows.

{kind=link}

{kind=link}

And a third of landlords claim an average loss of $8000

I suppose a third break evan

What a wonderful investment our people have made in their future

Probably barely turn a profit over the duration of their ownership then claim they didn’t buy it for capital gain.

Buy investment properties problem solved

Don't invest in a problem or you become a vested interest in not fixing that problem. And you become a casualty when we do fix that problem.

Just basic tax evaders.

What type of strange statistic is that why are we picking 1/3rds what is the average loss/profit? not what is the average loss on your cherry picked set of landlords. Maybe 1/3 of landlords are new to the market and just go huge mortgages and will eventually turn a profit. The statistic shows nothing of value. I am so over people picking the statistic that strengthens their point instead of the most appropriate one.

You do realize money supply growth moves in line with nominal GDP growth, yes? Property market doesn't rise relative to GDP due to banks extending credit like you claim.

Fantastic news, no-one should ever need to work again!?!

Yip, let's crack a bottle of NZ's finest. Umm do you mind buying, I'm a bit short of coin this week.

Just borrow up to the value of your house, it's not like prices will ever fall.

I might, one day. All my coinage goes into a monster mortgage....not much left for the real economy, never mind, at least I’m supporting the property economy.

My, with these said gold plated assets, all NZ needs to do is start exporting houses. Otherwise what in reality is their actual value, beyond these shores or even as a current asset on the nation’s balance sheet?

We do

It’s called immigration

And in the next decades, a lifeboat for folk coming from overseas.

(Unless China or the USA invade / buy the place.)

.

But...if you do need to work, consider being a real estate agent

Does anyone know how that compares with other countries?

important, we need some context

A very quick Google and a small calculation suggests Australia is around the 4.2x GDP mark. YMMV.

I think this might be the first Ashley Church article that I have quite enjoyed and largely agree with:

https://www.oneroof.co.nz/news/38884

Although given it's Ashley we should always expect at least one stupid or misleading comment, and he doesn't disappoint as he suggests ANZ are expecting a 'painful correction'. They aren't- they acknowledge it as a possibility and a risk.

Seemed like the usual crap to me. By saying that governments cannot influence house prices he is saying that they would be the same with double the number of houses being built, interest rates at 10%, a 33% comprehensive CGT, a land tax, etc. I highly doubt that would be the case.

Seemed to me like his disclosure statement 'I know what I'm talking about... but... don't blame me if I get it wrong, it's just an opinion. Look ANZ get it wrong too'

Removing interest only loans would stuff the speculators

Let’s see if the government has that on the radar

Sorry to disappoint you but no it won't because those that can pay principal will just scoop up more property with less competition from those who can't.

Watch this video to see the difference between interest only and cap&i loans

Utter madness to allow interest only loans... I hope the govt stops them as they have in australia

Even with capital and interest you can always refinance once the your property value increases, to get that cash back.

Second the video mentions interest rates going up, I don't think this will happen unless the government magically grows some balls. Look at the historic interest rate graph here: https://tradingeconomics.com/new-zealand/interest-rate constantly going down. I don't think it is by chance either, imagine what would happen if interest rates almost double like he estimated, what would happen to all those people that that are just making ends meet and paying their mortgage, the government is stuck in an endless downward spiral of interest rates. There is no way back from this without some sever pain. The government has stated that they don't want house prices to drop, what do you think will happen if all those people mortgage costs effectively double.

There is also some valid cases for interest only like buying a house when you are planning to sell the other.

less competition among purchasers as some can no longer finance it = less demand.....

Well, I increasingly think governments *can't* exert much influence. So that's where I find general agreement with his view.

The international experience is that a CGT has little impact.

What governments clearly *can* do is build more housing for people at the bottom of the heap. That won't have any impact on house prices though.

Is there actually any hard facts about international experiences of a CGT? The only facts I seem to hear are that Australia have a half hearted CGT and still have high house prices. But no one knows how high they may be without a CGT.

It's a good question which I have asked before. I think a CGT might mitigate house price silliness but it certainly doesn't prevent it.

I do actually support it, but not so much from a house price perspective, more from fairness.

Similarly I think a land tax could take the edges off house price madness, but not avoid it.

As you allude to the level of these taxes would need to be very high to have an impact. And while theoretically possible, it doesn't seem politically tenable.

Something I find interesting about Anz's report is their almost total lack of mention of NZ's world beating levels of immigration.

Fritz... it is, at the very least, a huge contributing factor to the housing and rent problems but it is rare for any article to even mention it.

I can't can tell if it mitigates or doesn't or makes it worse, its very hard to tell economies are complicated things you would effectively need a parallel universe to do it in and see the difference. One way I could see making the situation worse if house prices dropped people with property will get money, and the government may be less likely make policies that reduce tax take. I really don't know, and I don't think anybody else really knows either. All anybody is really doing is speculation.

Even the fairness question is hard, sure if you are buy properties for capital gain then you should be taxed. That is what the actual tax law states it is but people avoid this. If on the other hand like me you own 1 property to hedge against the insane property market, and just want your kids to be able to have a house to live in, and don't see the government doing anything useful about it, why should I pay tax if they choose to live somewhere else, I am just exchanging one house for another. I would much prefer that all New Zealanders could reasonably buy a house, but my children are my first priority, and I don't know if capital gains tax will actually help anyone.

As a property investor I would love to see the value my houses half, it would only effect me on paper and I would worry less about my children, grandchildren, and the future generations in general ability to live.

Yeah fair. I mean Sydney and Melbourne are now cheaper than Auckland.... if all markets operated at perfect efficiency you would assume those cities would be more expensive... Perhaps it has made a difference. Obviously the main problem remains excessive land use regulation but a CGT does seem to have an impact

Thinking about it some more, yes perhaps a CGT can take the edges off the silliness.

It struck me just now that Nz actually has the 'perfect mix' of factors to cause this housing crisis, some of them are unchangeable things, others are changeable (ie. Through policy). This makes it more important to change the things that can be changed. The unchangeable things will always exist and still make it hard to solve the problem.

I don't think any other western country has this perfect storm like Nz.

Unchangeable factors:

Small population

Isolated

Generally a hilly country.

Highly susceptible to natural hazards.

Changeable factors:

High levels of immigration.

Lack of a CGT or land tax.

Generally Unresponsive planning rules.

Under provision of social housing.

What governments can do is allow councils to circumvent the district plan rules and not have to wait for the 5 yearly review or whatever which then takes another few years to complete. Thereby always creating a pent up demand to keep prices high.

The church can, like anyone, read the numbers, but he doesn't understand them or has the ability, or the thought to look at the data behind the numbers.

His conclusions are really pre Galileoian. He is at the center of his own universe.

It appears they now have Ashley Church's fellow village idiot writing a weekly column, too.

Tony Alexander and Ashley Church. What a line up.

nymad... yeah come on Tony and Ashley. Please publish or post an in depth history of your investments (esp property related) from day one to present. I am sure many people on this site would be very interested and grateful. Some good long-term numbers would only add subscribers to your readership bases and enhance your reputations.

Logic suggests they do ... Ashley has said already he is a longterm investor but I don't know if that means he still has any. He would want to be in this market I think.

FH... I believe that for most readers what Ashley and Tony now have is of little interest. However, of interest to me (and probably many others), is a specific property investment history ie bought house A for X amount in (date and area) and sold it in (date) for Y. Bought house B......

That way we could pretty accurately assess how much attention we should pay to their opinions and views.

Tony is often exceptionally bullish but he's definitely better than Ashley Church.

Ashley consistently says very very silly things with great conviction that frankly would be enough to make you unsuitable for entry level economics work.

If you said in an interview for an economics position in housing/property that the government couldn't influence house prices and took the outcome under particular policy settings for the last 40 years as your reasoning for why, you'd immediately be asked what you think would happen if x policy was implemented. If you said no effect, you'd not be given the job because you have demonstrated an inability to grasp the basics of supply and demand..

buyand hodl... yes, you would hope that Tony learnt a bit while doing his economics degree so he should "sound" knowledgeable. But as Einstein said;in theory, theory and practice are the same thing but in practice they are not" hence my wish to see details of Tony's real world practice.

My narcissistic side is claiming credit for Ashley now referring to the last 40 years, when prior to me sending him a personal email a few months back asking him to explain what happened to NZ property between 1974 and 1980, he always commented on the last 50 years. So we can now acknowledge he has learnt to (fairly) accurately "predict" the past.

And yes, what Ashley said about the Govt not being able to control house price was pretty silly on a number of levels.

Dale...well said. It seems to him that all that is required is to look at what has happened over the last 40 odd years, ie basing his opinions and thoughts on the very limited scope of what has happened since he has personally been involved in property. Wish it was really that easy.

Fritz.. a refreshing and unusually humble article by Ashleys' standards although he just couldn't help but mention the past 40 years as an indicator of the future. My one big problem with his articles is that they all seem to simplistically fixate on the very short term past and ignore everything else. If it were really that easy half of NZ could retire before 40.

As somebody who has not had to work since I was 32 (over 20 years ago) and has made my money solely by (usually) taking the right side of financial gambles, many in the NZ property market, I view the advice and opinions of somebody like Ashley Church with a serious amount of scepticism. He is older than me, has drawn at least reasonable salaries for the last 30 something years (when I never have), has seemingly placed money making as a priority and yet at his ripe old age it seems he still needs to devote a good amount of his time working for others and making money. If he could (and had) predict the future in relation to housing as accurately as he often claims, he simply wouldn't be wasting his time (and lowering himself) writing for One Roof. Correctly assessing the value of peoples words and opinions is a valuable skill.

Looks like hard working is not the way to go, owning real estate is, just realised it has been so throughout human history..

"New Zealand’s housing stock is worth four times what the country’s economy produces in a year."

No it's not.

There are a lot of folk who act like lemmings, who don't understand what debt is, and who have been trained to think numbers mean wealth.

This is going to be interesting; we're well beyond the inflection.......

Your correct PDK, your personal wealth is the DIFFERNCE between what you can actually sell your house for and your mortgage on it. What we have out there is massive debt. We all had better hope the music doesn't stop because there are nowhere near enough chairs.

Or houses...

Carlos67.. yes technically your personal wealth (or part of) is the equity in your home but IMO the real definition of personal wealth is this.

Living in a comfortable home with enough money to do what you want without having to sell ANY OF your time for money. Once you attain that you have achieved personal wealth regardless of the amount of your assets or money. If you end up moving from your multi million dollar Akld home to a rest home at 75 or 80 (which so many do) then your personal wealth is no more than worthless numbers on a piece of paper.

Isn't the expansion of money supply (ie growth) predicated on the issuance of ever increasing levels of debt? That's the absurdity that is our economic model is it not? That's why we're pricing out all future generations from home ownership and completely re-writing the socioeconomic treaty for years to come? Debt = growth? The more debt issued against housing = more value in housing stock. No. Not a ponzi.

Stop talking about so called property value and use term foreign debt.. that what the Kiwis are taking on.

Houses are our economy now, productivity is so gauche.

I would like to see banks devote a miniscule fraction of the profane profits they make from every loan payment to go towards various business development, social enterprise, science research, community stuff and the like.

I'm talking like 2c of every dollar paid on every mortgage by every Kiwi. How much would that add up to and banks won't even notice it... hell can't they claim it as an expense? Imagine the good it could achieve.

Like jewellery made of shells and recycled bottle caps and stuff like that?

Yes! If you like.

Can't blame the banks when even our elected representatives have zero interest in taking a chunk out of speculative gains in housing.

Foxes subsidising the henhouse.

Hmm - the Space Shuttle. Fine on the way up, but I recall a couple of crash and burns...

Jenee

A question for you how does “$1.28 trillion - four times that of the country's annual GDP” do NZ numbers stand out with contemporary country’s ?

This illustrates better than anything I have recently seen of house price madness. A new 2 bed 70 square meter box in Mangere for 860k. Doubt it will sell at that price.

Bonkers.

https://developments.mikegreerhomes.co.nz/mangere-3?utm_source=facebook…

That is nuts. Other packages have e.g. 3 bedrooms and 3 bathrooms for $950. Why 3 bathrooms? That just pushes the price up and steals square metre-age

Yeah 3 bathrooms odd, although I assume the third might be a WC

What this really means is one 1/3 to 1/2 of the value of NZ housing stock is non-value added, ie it only exists because of monopoly restrictions forcing up the price above its actual true amenity cost.

Otherway of looking at this is that is what we call waste and could be taken out of the system without affecting the product, but that others by manipulation have been able to leverage and to them is revenue, but they have added no value.

All this waste cost is tied up in the debt to the banks when you take out a mortgage and in a downturn the purchaser is still liable for this "Ghost Equity' and the bank's security is on the real remaining value added costs.

That is the main difference between other jurisdictions where house prices are that much lower, ie simply housing policy decisions by their politicians.

This is what good housing policy gets you:

Dallas, Texas.

25yr old Teacher on $58,000, just bought a three-bedroom home for $155,000 (median income to house multiple of 2.67)

Interest rates at approx. 2.3%

https://www.cnbc.com/video/2020/12/17/58k-a-year-dallas-millennial-money...

Do these stats for average house price increase also account for the increased numbers of houses during this time? If the stock numbers increased, as well as the prices, the average increase per house wouldn't be as high as it is implying IMO.

If interest rates rose next month, then house prices would have to drop, as first home buyers wouldn't be able to spend as much buying a house, as the maximum amount they can afford to service is tied to the interest rates. It is interest rates, along with a lack of supply, that are a big reasons for this massive house price inflation. This graph does show that for a good number of years after the GFC prices went sideways. We are in the middle of a pandemic so I wonder how things are going to be coming out of it over the next 5 years.

Our housing stock is not *worth* 1.28 trillion, it *cost* 1.28 trillion.

I would even go further, "it *steals* 1.28 trillion".

See my comment above, but in summary approx. 1/3 to 1/2 of that value is 'Ghost Equity' with the remainder being the true cost of production if the market was not restricted.

The majority of, or all of, a mortgage is on the Ghost Equity which you pay interest on.

IE you are paying interest on something that only exists because of bad Govt. policy.

If anyone does not mind that, I have some second-hand Emperors clothes for sale, like new, hardly worn.

Ghost equity being used as a down payment for more mortgages backed ghost equity. Self feeding ponzi, where everyone with enough ghost equity piles into additional property purchases, then prices increase and more ghost equity is formed.

NZ is aim to post more than just 4x, it's expected to be around 10x IMHO, as the first in the world to show 'how future sustainable' of Finance, Insurance & Real Estate to govern the rest of economic activity. Thumbs up & be kind.

Well....why be surprised. MAJOR economy in NZ was housing and Now ONLY economy in NZ is housing...Am aware so many businesses people who have either shut down their business or putting it on silent mode to concentrate on buying and selling and development- speculation in housing market as no where can one make so easy and fast money and cannot blame them as also is tax free many a times.

In other countries also house price have gone up but have industries and other business unlike NZ. Narrow and Short term thinking of politicians and ignorance of current government is leading NZ to a path of destruction.

Immediate question - how does this compare internationally?

Quick and dirty search suggests:

US housing stock valued at $34 trillion (in Jan), US GDP $20 trillion. So approx 1.7x ratio, as opposed to our 4x.

UK: GBP 7.4 trillion, GDP 2.2 trillion. Much closer to ours (population density?)

The reason we are closer to the UK number is, guess where we learnt our bad housing habits?

As a commonwealth country, we use many of the same legislative type systems, including taking our housing lead from the UK Town and Country Planning Act.

But we can proudly say that the student has succeeded the master in housing unaffordability.

The USA homeowner only has about 35% of the net worth tied up in housing, whereas in NZ we are 75% plus.

UBI is the way to stop the lunacy, they know it, but they won't use it. Why?

Because it would just go to landlords, whom would also receive their own UBI on top of that, then buy more ghost homes? lol

Nothing will work in NZ while the housing market is the way it is.

Labour want house prices to increase, so your UBI suggestion is implausible under this government. Though much better than the current welfare system (WINZ Classic). At this point a UBI would just act as a band-aid and give latitude to increase rents and bid up housing - much like 'Accommodation Supplements', expect landlords get to have their UBI and eat yours too.

I know this article is trying to make a point about the value of NZ's housing stock but comparisons like this are pretty meaningless. GDP is a measure of what a country produces in a year whereas the housing stock has been built up over many years. It's like those articles that claim Bill Gates is wealthier than . Except it's not true because Bill Gates has built up his wealth over 40+ years so those articles should actually be comparing to 40 years of GDP.

Given "NZ" cant sell its housing stock on mass, its a meaningless statistic in terms of "wealth" - more accurately it reflects the amount of leverage / debt burden in the system

The trouble being we can add debt with a keystroke, but the underlying energy/resources to service this additional debt don't change

Which reflects how fiat currency is ultimately being devalued to nothing ... a system where wages and savings cant buy you anything ...

So the question is, what comes after Capitalism

Exactly - the end of the debt cycle.

Capitalism largely stopped years ago, and was replaced with crony corporatism.

After crony corporatism, ramped up entitlements, then deleveraging, and off we go again.

And all that will really have changed through the cycle, by another chunk, are the climate, resource availability and automation of work.

Did they remove the mortgages?

House is not yours til its paid.

"Worth" is not in hands fo "owner" til its paid.

love how cynical these comments have become. people are so over the property bubble and the inequality it has created.

I'm often surprised how comfortable wealthy kiwis are with this new inequality. NZ is no longer the same country I immigrated to 22 years ago. It's becoming more like Brazil or South Africa with a dissipating middle class. New Zealand is now rentiers and serfs - little else

We have become a very self centered nation.

I agree saw a guy today at the lights in Newmarket begging all the range rovers and Mercedes for some coins. He was filthy a proper homeless guy who looked sick. I gave him all the coins I had and I thought to myself these poor people are everywhere now. What the hell has happened.

Very true.

And we are decaying from a free-market and entrepreneurial nation into a degenerate and zombified environment where parasitic, unproductive and socially destructive housing speculation is promoted by the authorities at the expense of capital formation, productive expansion and productivity improvement. This is an environment where massive landlord welfare and unfair tax advantages and a shortsighted and highly damaging ultra-loose monetary policy completely skew and make the whole investment market utterly meaningless.

Hey, I thought foreigners are responsible for the runaway house prices! Where's Phil Twyford? We need a new racial list of scapegoats! How about the Yankees, Aussies and Sinkies this round?

The source of the housing problems remains letting in a net 500k people in the last decade. That is why we have gone from a country where pretty much everyone had a place to live to one where people are living in cars, garages, motels, moving back with parents, sleeping in the lounge etc. So you are right, foreigners are in fact the cause of the problem. Not their fault though as they are just trying to improve their own lives. The fault lies with the politicians of both main parties who allowed mass immigration.

Yoy net migration is - 59.5K and Mom is -900 but house prices are still rising relentlessly.

Nevermind the disconnect and facts, let us continue the story, "it's the foreigners fault"!

https://www.stats.govt.nz/information-releases/international-migration-…

That's a disingenious argument. The past year has been an outlier.

Not many people say it's all because of immigration. It's one factor.

CWBW you must be one of the daftest people to be born in the last two thousand years. You mention facts and provide a URL link to support your argument. But you clearly dont understand the numbers. Net migration in the last 12 months is positive 59k not minus 59k and in the last month is positive 900 not negative 900. You have confused the dash sign for a negative sign. A silly mistake to make because it gives yoy departures at 58k and arrivals at 117k so simple arithmetic would confirm the net migration was a net inflow. The housing shortage is not entirely due to migration in the last 12 months - the excess demand due to migration has been building up for years.

and of course the effects of lower immigration take time. If it stays low in 2021 I think we will see some major effects.

NZ housing stock - the most inflated bubble in modern world economic history.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.