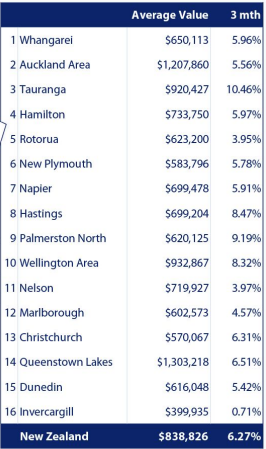

The average value of all New Zealand homes was $838,826 at the end of January, according to Quotable Value.

The QV House Price Index shows that the national average value increased by 6.27% over the three months to the end of January and had increased by 15.11% over the previous 12 months.

The strongest growth over the three months to the end of January was in Tauranga (+10.46%), followed by Palmerston North (+9.19%) and Hastings (+8.47%).

Wellington recorded the fastest growth of the main centres with the average value up 8.32% over the three months to the end of January, followed by Christchurch +6.31%, Auckland +5.56 and Dunedin +5.42%.

Property values were also surprisingly strong in Queenstown-Lakes, where they increased by 6.51% over the three months to January, making the district the most expensive in the country with an average value of $1,303,218, eclipsing Auckland where the average value was $1,207,860.

The smallest increase in average value was in Invercargill where it was up just 0.71% over the last three months (refer to the table below for the breakdown in all major centres).

However, QV General Manager David Nagel said the market could start to cool later this year.

"With the return of LVR speed limits in March this year, we may see a gradual cooling of the market in the second half of 2021, particularly in the entry-level locations as property investors reach their credit limits and first home buyers struggle to raise a deposit.

"But with the long term forecast for housing demand in New Zealand looking positive, it is difficult to see the market take a significant turn for the worse anytime soon," he said.

You can read QV's full House Price Index Report here.

The comment stream on this story is now closed.

QV House Price Index

Three months to January 2021

- You can have articles like this delivered directly to you inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

32 Comments

I expect Invercargill property prices will start moving up with a bit more certainty.

Clearly, it's not just the main centres (Wellington and Auckland) that are racing ahead - but also provincial growth areas like Palmerston North.

I expect that all three of the above will witness further strong increases in property values.

TTP

It is the early stages of white flight. It has happened in many other countries. Aucklanders feeling like foreigners in their own city are moving to the provinces and taking advantage of the house price differences while they are at it.

Wow so glad I bought here in Tauranga in September 2020. The problem is that nothing is going to change this rampant house price increase without some major changes in interest rates and this government are just sitting on their hands. If they don't do something immediately the average house price in Tauranga will most certainly be $1mil by the end of this year. There simply will be no "Cooling off" without some major intervention.

Prices have gone up in Tauranga 25 per cent in less than two years. But you know, it's a great place to raise a family. Just don't expect to ever see them as you work '$10 Tauranga' jobs to pay for it...

The increase in people down here is almost exclusively cashed up Aucklanders like me. Garages are full of "Toys" and a huge number of people either work from home or don't work at all. If the increases in house prices here are not immediately sorted, Tauranga is just going to turn into one giant retirement village.

Once you've been here for awhile you'll realise that all those toys aren't very representative of real wealth at all, which is really worrying if there's any kind of correction.

I thought Tauranga was a giant retirement village already. Funeral directors paradise there.

Carlos67....you may well be right but you really really really should read The Black Swan to help you understand risk and how it is impossible to be (correctly) as certain about the future as you seem to be. Please try to make the effort to read it. It will be time very well spent.

Nothing in the future is set in stone Karl, however you can take a punt using the information gathered first hand and by pure experience over time. At the end of the day you go with your gut feeling and then it doesn't really matter if your right or your wrong because you can live with it because you cannot blame anyone else. Pretty happy to make the prediction about Tauranga if nothing is directly done to change it and the current situation continues unchecked. Sure something totally unexpected could happen to cool house prices but if we keep on just cruising in the current "Do nothing and lets see what happens" mode the outcome is a certainty. The average house price in Tauranga will be $1mil by Christmas.

So to summarise, your prediction is: If nothing changes, everything will stay the same.

Carlos.I've got a three bedder rental in papamoa.just wondering if prices are going up there also?thanks☺

Carlos67... I understand where you are coming from and (being a gambler myself) especially the taking a punt and only having yourself to blame if it doesn't work out. But since you have a lot of free time why wouldn't you want to read The Black Swan? It is an entertaining and very informative read and I feel it would change your perspective on risk in a positive manner. There are no certain outcomes in investment (even in NZ property) and I believe taking a few hours to read The Black Swan would help you to see that. You might enjoy reading it so much you will read all of Talebs books.

Thanks, Karl, for the book tip (and your comments in general, which I enjoy) - I will read it.

Table of Contents - "Empty suits" - ah, so that's where that comes from...

RR... enjoy the book. All his books are very good but if you enjoy The Black Swan then Antifragile is probably the next best. I especially admire him as he is a doer ie takes risks with his own money and stands on his own merits rather than risking other peoples money without "skin in the game" (another good Taleb title) like those empty suits (bankers, economists, politicians etc) he so clearly despises.

Can anyone find or source the annual change?

Property price increases (asset appreciation) are a sign of a AILING financial system

The system requires debt growth

If it cant get it in real productive output, it must rob the balance sheet and load up on capital appreciation

You cant kid floundering income growth & weak commercial activity indefinitely

With the impending obstacle facing the FHBs, the investor should consider turning this great opportunity into a multiplier for your portfolios. Investors who currently hold high end estates should seriously consider a swap strategy especially if it is a 2 for 1 opportunity.

With the escalating house price momentum, the rate of returns on assets with higher valuations falls; well those with lower valuations accelerates rapidly. It only makes sense that you should invest on the assets that generate higher returns.

Therefore, investors should now strongly focus on the entry level properties as part of their portfolio regeneration.

Wishing all a prosperous year ahead!

"Wishing all a prosperous year ahead"

Except you dont

Just those who can game more of the fat for themselves

To think NZ use to frown at this sort of attitude

CWBW... if you think I'm gunna swap my 300sqm home on 2000sqm of land in Shelter Grove for even 3 of your Marfell Block rentals you must have been smoking those green cigarettes again.

Nah mate. I'm not interested in Taranaki. That place is on track to become the New Bennydale anyway. Just waiting on Todd energy and the port to wind down. Prospectus had never been that bleak. Maybe they should start making batteries and brand them 'Hardcore'. haha

CWBW... A rental in Waitara would be right up your alley. You could be the star of Taranaki Hard, Season 2 (adults only). You and Paddy Gower could have a meeting of the minds down the Waitara RSA every Sat nite. LOL. Bleak prospects don't pose any problems for rich (ex) property magnates like myself. And BTW, show some respect, it is Ngati Benneydale now.

Annual figures (year on year) in link in full report above :

https://www.interest.co.nz/sites/default/files/embedded_images/House%20…

15% over all NZ.

Palmy +23% yoy leading the way over that term, Welly +21% yoy close behind as is HB.

Easiest $$$ I ever made. Thanks to all the support i have received from interest.co.nz commentators over the years agreeing that Palmy really was severely underpriced 2012-2017 when I had been hoovering up stock. The suicide capital now the capital gains capital. Who'd have thought it...

Cheers Robbo and Orr. What a dream team. Cindy certainly has been kind. That horsey smile's really growing on me.

Simon I presume you have sold them otherwise just paper profits. Nothing is certain until the cash hits the bank account.

We have discussed this before on interest.co but it is worth repeating. Simon's houses are superior to cash in the bank. They likely yield much more than term deposits and they at least keep up with inflation. If Simon had cashed up the money would be depreciating in the bank. If he had sold up a year or more ago he certainly wouldn't be a happy chappy. Realizing your "paper gains" is like killing the goose that laid the golden egg. To think that wealth is only cash in the bank and not the current value of all your assets is the wrong way to think about these things. Simon has purchased money generators with positive cash flow which money in term deposits certainly isn't.

Reminds me of that old joke that started in 2006 about the rich Irishman with "his superior houses" and a big mortgage. 15 years later everybody is still laughing except him. Don't be that Irishman.

If the Irishman had cash flow positive houses and retained them he would still be rich today. You are also imagining a worst case scenario where the mythical Irishmen bought all his properties at the apex of the market.

It's like saying, what about all those investors who bought rental properties in Hiroshima in early 1945? Or in Pompeii an AD78?

Zach...If the Irishman had bought his first house in say 2003, a second in 2006 and a third one in 2009 he would still, almost 20 years later probably be in negative equity and that is if he is lucky. I couldn't find stats on what happened to rents in Ireland but I'm guessing they dropped as house prices dropped making positive cashflow (for most) pretty unlikely and forced sales for many (at low prices) inevitable.

It is probably not feasible to plan for Hiroshima-like events (although giants of risk analysis like Taleb suggest we do), however it seems sensible to me that we examine global property markets over the last century or two (especially those that have many similarities to NZ, (such as Ireland) to see the outcomes that are very possible and (with some financial common sense and responsible investment strategies) we can all but eliminate the risk of ruin.

As long as NZ investors understand that if they purchased their 3 houses around 2015, 2018 and 2021 and we have an Irish type correction then they will probably still be in negative equity in 2035. If you are OK with that possibility then take a punt. More likely by 2035 you will end up rich but it is far from certain. Hope you get as lucky as I did (between 1988 and 2015).

Somewhat agree although I think Ireland is a bit of a special case and governments have learned a thing or to after what happened there.

Not really its better than cash, hence the whole problem of silly gains to start with. Cash is just paper and people are pouring into hard assets like houses.

Agreed, cash is no longer the king. I've suggested those young single medical specialist no longer asking for worthless 6 digits salary, ask the payment towards land/housing.

Likewise to all those poor fresh produce/distributors, should all leveraged .. asking their business transaction to be back into bartering mode.. with land/housing. Not in worthless numbers, remember at anytime RBNZ & govt can just make more of it to the point of land/house, to be swapped with those things so super important to support life.

You've given me an idea Pusheen. The government should create a type of crypto that has units that are always worth one millionth of an average Auckland house. People could elect to be paid at least partially with these units instead of dollars.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.