The latest figures from property website Realestate.co.nz suggest Auckland may lead the housing market down as it eventually starts to cool.

March is traditionally the busiest month of the year for the residential property market, meaning February is usually the busiest month for new listings.

Realestate.co.nz received 10,736 new listings in February. That was up 1.8% compared to February last year, and the highest number of new listings for the month of February since 2018.

But at the end of February, Realestate.co.nz had just 15,829 residential listings in total on its site, down 24.2% compared to February 2020.

That was the lowest number of residential properties available for sale on the website in the month of February since its records began in 2007.

The fact that new listings were up while total stock was at a record low, reflects the buoyancy of the current market and the tightness of supply.

However a closer look reveals significant differences between Auckland and the rest of the country.

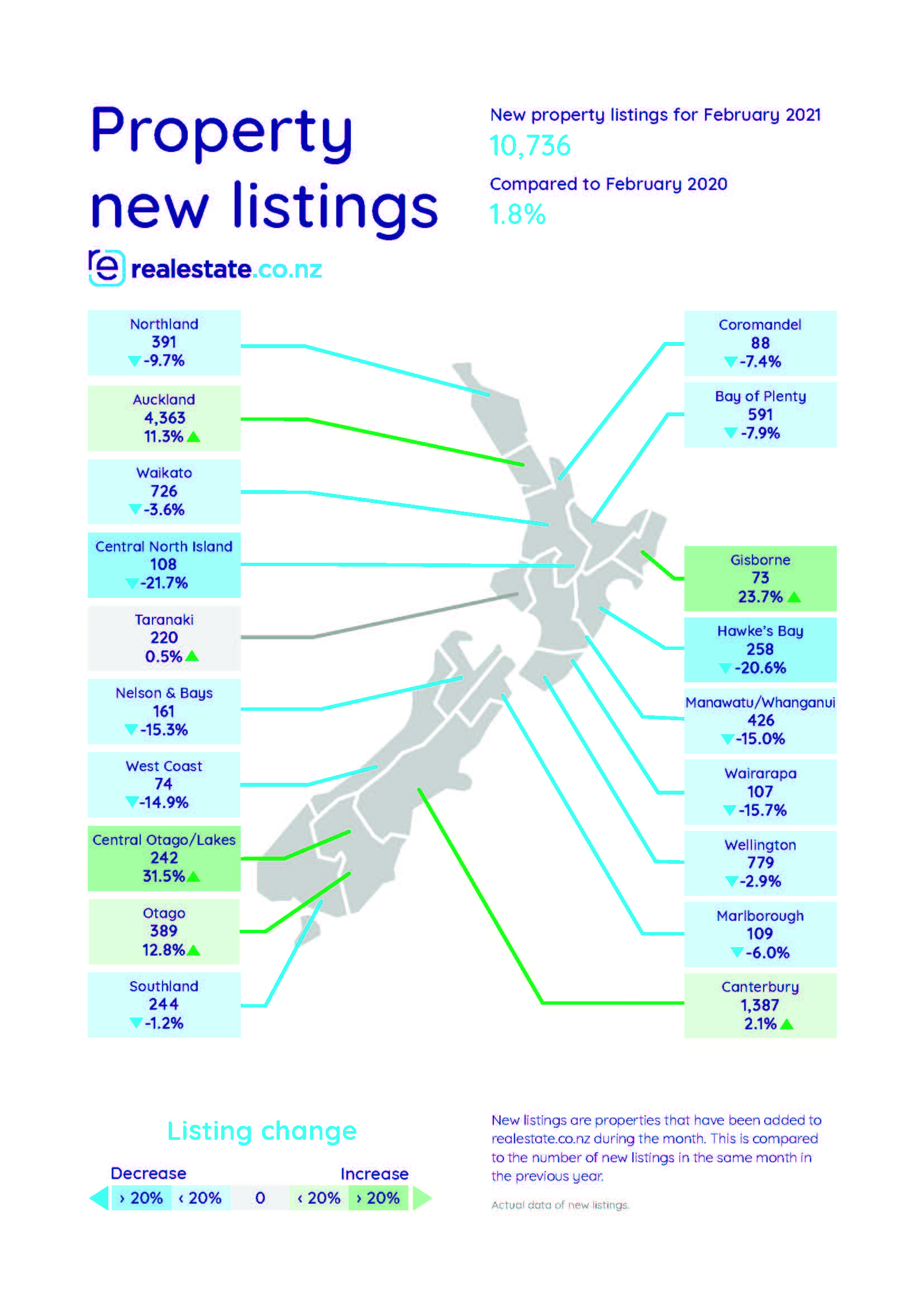

Realestate.co.nz received 4363 new listings from the Auckland region in February, up 11.3% compared to February last year (see the first chart below for the full regional figures).

That was the highest number of new Auckland listings for the month of February since 2012.

However new listings from the rest of the country (excluding Auckland) were down by 3.7% in February compared to a year earlier. That's the lowest they have ever been for the month of February.

Looking across all regions, the trends are that new listings have been growing quite strongly in Auckland, Otago/Central Otago and Gisborne, but are largely flat or showing declines everywhere else.

And in the areas that have shown growth, the numbers are quite small.

So almost all of the growth in new listings is coming out of the Auckland region.

There are similar differences between Auckland and the rest of the country in the total amount of stock available for sale on the website.

There were 7196 Auckland properties available for sale on Realestate.co.nz at the end of February, down 9.2% compared to February last year (see the second chart below for the full regional figures).

That compares to 8633 for the rest of New Zealand (excluding Auckland), which was down by exactly a third compared to February last year.

It also means Auckland accounted for 45% of all the residential properties available for sale on Realestate.co.nz at the end of February.

Those figures suggest that while the supply of properties for sale in Auckland may still be on the tight side, it is a lot less tight than in the rest of the country.

And supply is a lot closer to catching up with demand in Auckland than it is in the rest of New Zealand, something that was also suggested by recent Statistics NZ figures showing strong growth in residential building consents was mainly being driven by activity in Auckland.

With loan-to-value ratio mortgage lending restrictions once again a feature of the housing market and many forecasters picking upward pressure on interest rates to eventually start kicking in, a market cooling may well be on the horizon.

And when it does arrive, it may well land in Auckland first.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

130 Comments

Not before time.

Don't worry, widespread zoning to higher density later this year will give values in Auckland another nudge higher!

Is this happening, or just a prediction? Isn't the new unitary plan in place with the higher density zoning already set?

Yes it's going to happen. I can't believe how little media coverage there has been, and how little awareness there is.

The National Policy Statement - Urban Development mandates that ALL of the bigger cities in NZ rezone land within walking distance of train stations and centers to enable 6 storey apartment development. It also mandates the removal of parking requirements.

So in Auckland the amount of high density zoned land will have to increase massively, probably trebled or quadrupled. That affects tens of thousands of properties. Many will go from 2 or 3 storey height limits to 6 storeys.

I think plan changes need to be notified by the end of this year.

All things being equal this will generate significant property inflation.

Hi Fritz, what am I missing? Won’t more dwellings reduce prices?

It should, but it will be gamed so it won't. Also getting a house half the size for 3/4 the price of what was available prior is not really getting it cheaper.

It depends if you are talking land or dwelling prices. With intensification land prices could go up but dwelling prices come down. Lots of ifs and buts though.

That is the experience of Tokyo compared to London. Tokyo has the higher land price yet has lower apartment prices. As you Sherwood. Lots of ifs and buts though.

Fritz... developers had a good idea all this was going to happen over 5 years ago. I sold 2 houses next to each other in Mt Roskill with about 900SQM of land on the front (not including land the houses were on or the back yards). Developers knew what was going to happen way back in 2015 and were clambering to get there dirty little hands on it.

That was the Unitary plan. This is Unitary Plan mark II...

Fritz,, OK thx.

"clambering to get there dirty little hands on it."

No that's just a filthy comment. And 2021 prices are far higher than 2015 so maybe you're also filthy about it

FH... not filthy at all. Did not need to sell it. I chose to do so to avoid all the stress I would no doubt have suffered in dealing with the council in relation to subdivision. IMO once you have enough money where you will never run out then you should avoid any risk or stress related to making more money. Why would you bother?.

Also, if you check out what has happened to the NZX50 in the last few years (where most of the proceeds of the sale went) you will see that it has outperformed the NZ property market quite handily. Not that it really matters to me anyway. I live a cheap lifestyle, have all the money I need and if I(for some weird turn of events) ran out of money fortunately I have the skills required to make more money quickly and easily if I needed to do so.

I hope you didn't lose on the covid downturn ... a lot of investors sold during the plunge or switched to low risk

FH...I did actually. Sold down a fair bit of NZ stock last year, most of it at the absolute bottom. Still I guess I was lucky I bought a house in Feb last year about 3 weeks before lock down.

Possibly, but with demo. and amalgamation costs, full apartment specs, lifts, fire, structural, etc. plus buyers maxing out, possible interest rate rises, and the number size of the zoning, all these costs, would/should come off the land price.

A price rise, yes, but significant across the zone? Will be interesting to watch.

THAB zoned sites with the right characteristics - 700 sq m plus, flat etc - have been going for crazy prices.

The easy low hanging fruit in this brief hyped market, plus developed before all the views go due to the others being develooped.

Also because you are in the industry, when I hear you saying crazy prices, then we both know that is a red flag.

Yes, it's definitely happening.

I've got family members who bought a house 20 years ago in a now gentrified suburb walking distance to everything, shops, transport, schools, medical, etc. Lots of million plus character villas on leafy sections in the area.

They can now get approval to build a 6-storey building on their 809sq m block immediately next to the next door single level villa.

Firstly the AUP already does a fair decent job of managing density in Auckland. Secondly the increase in value of land due to allowing something closer to what the market wants is unfortunately the price for affordable housing and increased density. If you don’t want to have to fit more people in the same amount of space and deal with the above I suggest we vote to at least half immigration.

Whilst it may manage density, it leaves some home owners sandwiched between multi storey up to the boundary developments and no ability to be able to afford to move.

Also basic infrastructure is already stuffed and this just adds.

Ever wonder why so many developments have pressurized sewage systems in the front yard? Simply the reticulation cant cope or gravity is too expensive. Roading is gridlock and were still on water restrictions.

With the Government printing money with abandon its best hope for fixing the Housing Crisis in Auckland is to "go out". Rather than over density in inner Auckland do as the region did in the 60's when faced with baby boomer generation needing houses-expand out and massive new residential land produced. North of Albany and east of Helensville tens of thousands of normal sized residential sections could be produced at affordable section prices if done large as in the 60's. Back then motorway created to link the city to new South Auckland region. 60 years later a new harbour crossing carrying Light Rail from the near north down the current bus lane would link the near north to the CBD. But a Ministry of Transportation $4 Billion annual budget doesn't get it done--needs to expand exponentially. Massive new builds on cheap land no farther away than 20k from the CBD is the prescription needed to allow 1st Home buyers a place to live in the Auckland region--other than shoe box apartments in the CBD. It would be a ray of hope to keep the 30 year olds from fleeing the country. This is what I would call a "Think Big" project.

Price for affordable housing? Show me 'affordable' apartments in Auckland.

Btw my comment was not passing judgement on the merits of intensification- I actually favour it. But unless the government gets much more involved and we look much more seriously at shared equity, we won't see affordable apartments and townhouses in Auckland...

We need this correction, they need to come back down 20%. FHB and investors will loose their 20%+ deposits if buying in this market. Funny how the banks demand a sizeable deposit now...they know what’s coming and they’re not putting their money on the line.

20%? And the rest mate.

If human psychology remains to what it has in past markets, at 20% fall will be followed by another 20% fall - especially if the central bank is out of ammo and can't push even cheaper credit into the market (which it appears is where we are at).

At some point I think (and have thought this for a while but get laughed at) there will be a deleveraging event where we see mass defaults on debts. Its a natural part of the long term debt cycle - its just that it hasn't happened in most peoples lives so it isn't believed that it can happen.

The central banks can't own all of the bad debts in the system - despite the Fed buying up junk bonds last year to keep a failing system alive!

This is when I started getting really worried about it all: when the Fed started buying junk bonds. Bad, really bad.

Yeah but its happened now and nobody seems to care nor think its abnormal when its actually pretty crazy - its the state keeping dead companies on life support and making their balance sheets look 'ok' instead of what they really are which is insolvent (i.e. nobody else would be willing to hold their debt with that level of return given the market or company risk).

Theyre not putting their depositors money on the line.

If house prices went down 20% I don't see the problem. After all they have gone up 20% in a very short time so it's only getting back to prices of last year.

Sure some have bought recently but only a small percentage of the whole housing stock. Those new home owners might look hurt on paper, but it's the same loan they took out and they are living in the same place. So no problem really.

"Investors" ( or call them speculators if capital gain was the game plan ) still also have the same loan and continue to own the house. A chunk out of their equity, but that's the business they are in, so again, no problem.

Exactly. The Auckland median was 830k just 8 months ago. Less than 1% of Auckland houses are involved.

So March 2020 during the first lockdown, economists predicted a fall in house prices. RBNZ panicked and loosened LVR restrictions to ensure there were enough people to purchase houses during the expected mass sell-off. Said sell-off didn't happen, so loosening LVR backfired, and prices went UP instead of down (or even flat). Talk about a massive backfire.

A year later, LVRs are back on, which means less buyers, and interest rates are picked to go up, which will mean more sellers. It really feels like they gave the Smart Money time to sell last year, and now the ones left holding the bag will be those who jumped in late due to FOMO.

How far down are we talking about,because they could fall 20/30 %,imo,and they would still be out of reach.

House prices need to come down not only because of unaffordability but also to help our economy shed some of the deadweight from unproductive jobs and investments in the enormous real estate sector.

Our GDP is clearly overinflated by real estate commissions, house lending margins, brokerage, solicitor fees, etc. from the numerous housing swaps that happen each year.

IMO about 40% to 50% to get to a point where a hard working capable couple can afford to get married and start a family in Auckland (Universal Child Benefit would help too). Until house prices drop by a third to a half the most productive young Kiwis will look to leave Auckland and frequently that means moving overseas. Productive Kiwis include IT programmers and technicians, builders, plumbers, teachers, doctors, etc.

This is a heartfelt comment because we are supporting by paying the rent for two daughters with good jobs, loving working partners and young children. By the time they spend on the necessities [vehicle, pre-school fees, taxes, food] they have no money for rent or holidays. It wasn't like this when we were their age - we never depended on the bank of Mum & Dad.

Thats very very good of you... I think its a hand to mouth existence though and if at all possible you should help them into their own places. How much is it costing you?

Graeme Wheeler wrote and presented a paper when he introduced the LVRs.

In it talks about the return to long term mean of 3*income when real interest rates rise.

So you are actually looking at up to 70% price fall or more if we had a crash and rates jump up.

Can't happen without a knock on through labour rates which are going up thanks to Labour and the industries on the supply side taking a big hit on the cost of what they make and sell

Even if land and materials were free, the labour alone in a new build is more than 3x income.

In fact on my most recent build because of the contour of the land and its location, costs (building & resource consent, infrastructure growth charge, intensification levy, engineering work, etc) were over 3x the median income before any work even started.

Because some houses get torn down every year if the cost of building exceeded the value of the house, building will stop and housing supply will constrict.

With regulatory and labour costs each over 3x the median income there is little prospect of prices ever being lower than 6x median income especially if you end up needing to pay for the land and/ or materials.

You need the cost of labour and regulation to drop for house prices to drop.

That is so true. Also, the cost of labour and compliance needed to build infrastructure is capitalized in the land prices.

As you raise the minimum wage and labour costs go up the labour already capitalised into the house goes up in value as well (because it would cost more to do the same now). Add to this the fact that council costs go up when min wage costs go up, and this causes the capitalised value of the regulatory work that goes into housing to go up (because it would cost more to get the same approval now).

It rapidly start to look like the problem is that the median wage is too close to the minimum wage. It would be interesting to see an analysis of house prices relative to minimum wages around the world / across history. The correlation may be better.

All that you say is true, under the present system BUT that is because the input cost order is back to front. When supply can meet demand (especially fewer land restrictions), the demand, ie the buyers have slightly more choice so the suppliers have to compete for the buyer. Part of the competitiveness is to be good value and cheaper than your competitor. This caps what price developers can pay for the likes of land and because they can buy land more freely, then they can generally buy above its next best economic use, eg if buying farmland, the farmland price.

This offsets any increase in income to a far greater extent than income causes what you describe, so getting to a lower multiple is easily possible. After all, that is what happens in jurisdictions that don't have restrictions to supply, especially the supply of land.

All that you say is true, under the present system BUT that is because the input cost order is back to front. When supply can meet demand (especially fewer land restrictions), the demand, ie the buyers have slightly more choice so the suppliers have to compete for the buyer. Part of the competitiveness is to be good value and cheaper than your competitor. This caps what price developers can pay for the likes of land and because they can buy land more freely, then they can generally buy above its next best economic use, eg if buying farmland, the farmland price.

This offsets any increase in income to a far greater extent than income causes what you describe, so getting to a lower multiple is easily possible. After all, that is what happens in jurisdictions that don't have restrictions to supply, especially the supply of land.

Don't panic Auckland homeowners. The borders will soon be open and South Africa, India and China will come to your rescue.

Yes then we can finally see some really big gains..

Some Hong Kong evacuees?

KK....Don't panic (South) Auckland landlords. The borders will soon be open and Samoa, Fiji and Tonga will come to your rescue.

I think the rescue ships are likely to bring more lifetime renters for Auckland landlords.

Advisor... NZs own Windrush people, and weren't they a net positive on British society.

High immigration won’t be possible if we have a crash and high unemployment.

gnx... you are presuming the Govt would not throw our lower-socio unemployed under the bus in favour of global inclusivity and virtue signalling. They have already shown how little they care for our struggling kiwis by allowing 300 000 temporary visa holders to currently be here competing with them for much needed housing and (largely) low (or no) skilled jobs. That number could have been 400 000+ by now had it not been for Covid.

It is not just the Kiwi lower-socio who suffer; it is the low paid immigrants too. In 2016 Prof Stringer produced a report into worker exploitation; the Herald's headline was "No Sex, no visa" - a remark made by an employer to a 31 year old female immigrant from India. Prof Stringer's report detailed many cases of exploitation - she said everyone in her sample of recent immigrants claimed to know of a case of exploitation. Prof Stringer's remarked that she was not surprised that exploitation occurred but she was by how common it was. That was an authorative report and both National and Labour governments have effectivly ignored it.

Lapun...there is a very easy and sensible way to ensure no more immigrants are abused on NZ soil again. And without knowing the details of the specific case you mention, I would bet the abuser was a "new NZ net negative immigrant" , originally from the same country as the abused. Our first mistake in your whole sorry story was probably to grant the abuser PR in the first place.

As I have said before there are certain nationalities who are in the business of selling NZ PR and citizenship. And as your story illustrates money is not always the only price. If we only accepted wealthy students and genuinely highly skilled people into NZ on long term visas this would massively reduce the chances of this type of situation occurring. It is rumoured that even the odd Member of Parliament is impartial to a bit of sex for visa action. My lips are sealed (as David Hartnell says) but apparently this MPs are often not.

I get your point

It is important to not get a feeling that stock and house prices are one way street - up as many are borrowing in extreme under FOMO and buying not only houses but even stocks left right and centre, which is good if doing within limit and for long term - holding capacity even if it falls but many are borrowing in extreme and leveraging everything with no tolerance of even slight correction and for them will be doomsday which will have domino effect snowballing into biggest disaster of the century. So one should allow healthy correction for long term.

Disagree . The full effects of the current lower OCR/ mortgage rates and resets has not passed fully thru. Auckland currently accounts for 37.7 percent of national real estate sales up from 28.3 percent a year ago, having turned upwards only from last July and remains well below past peaks. It is Auckland in "catchup" Inventory as stated is at historical lows , Auckland included, yet apparently unadjusted for growth in stock. The current situation where it is now "cheaper' to own than rent does not gel with a message that a storm is rapidly approaching, as most homeowners have been afforded the opportunity, if required, to anchor in a quiet bay for the foreseeable future. ,

yes. unfortunate that when people make comparisons, they do not do so on consistent data.

Housing stock up about 13% in Auckland since 2013.

So, % of stock sold pa is never quoted.

Auckland council has v vague idea of how many OO dwellings there are in its City for instance and Census was not v helpful on this either as 500,000 people in NZ did not answer the question fully.

Speculators heading for the exit. If inside the bright line test (soon to be extended again...?) you have get out before the income tax change hike as well.

Now all talking about doom, suddenly. Can sentiment change in a day or two from positive to negative suddenly or is it something to do with what government being forced is planning to do to control speculative demand - spook them and this government is most spooked as it is.

Tipping Point by Malcolm Gladwell gives a good insight this if you haven't read. Small changes that spread rapidly through society and can quickly change the sentiment of large populations. Witnessed it first hand in the US when their property bubble burst - just noticed week by week more people start to become fearful and before you know if you're past the tipping point and everyone has gone from bulls to bears.

The bigger the Ponzi, the more prone to sudden implosion. Once some specuvestors start heading for the exit, there is no way anybody can predict how quickly the whole thing unfolds. But it could well be very fast.

The problem with over-inflated bubbles is that the tiniest of wobble can wreak havoc.

Could be quite an apt photo given this mornings events.

The housing market can't crash. Dave Chaston pointed out weeks ago that banks are awash with customer deposits. Those deposits put in the bank by customers is then used to lend out.

Banks don't lend out customer deposits, these are held in their reserve accounts at the reserve bank and nor does QE give the banks money to lend out. Banks create new money when they lend as the reserve bank explains on its website here. https://www.rbnz.govt.nz/research-and-publications/videos/money-creatio…

No No treadlightly

You are incorrect. Dave Chaston has said that it's the money deposited by customers that is used to lend out. He also said if banks could create money they wouldn't need bailing out.

Haha yeah but banks need credit worthy people and companies to lend to and that doesn't work if they're already at peak debt...and stuck in a liquidity trap.

Yep even if it's free people won't borrow...

He is incorrect, listen to the video that I have linked. The Reserve Bank and The Bank Of England cannot both be wrong. Economist Bill Mitchell has an excellent article on banking here which also supports this. http://bilbo.economicoutlook.net/blog/?p=14620

No all money is existing and banks are financial intermediary institutions who only lend what customers deposit...

I have provided sufficient evidence from reliable sources, where is your evidence? Here is the full article here from The Bank of England. https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

My evidence is interest editorial. Dave Chaston is correct and you are incorrect...

You do not understand how our banking system works. New lending creates deposits. Provided people chose to leave that newly created money in the banking system, the only thing holding back banks from creating infinite amounts of money is:

1. Willing and able borrowers

2. Capital reserves

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Wrong

Dave Chaston said banks take money from depositors and that is lent out for mortgages etc. And as dave said banks are awash with customer deposits. Which means mum's and dad's are putting all their hard earned money into the banks which is lent out.

Miguel is correct

Banks have to retain specific ratios of capital for their assets (lending)

Ever heard of the credit multiplier function?

Ever heard of the credit multiplier function?

Do you mean this:.

As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements for all depository institutions. Link

Not that it mattered much for decades for the larger non-regional banks - FED-sweep-ACs.pdf

I have never seen an RBNZ statistics entry detailing a domestic reserve ratio or any tally of required reserves.

Well this may enlighten you https://www.rbnz.govt.nz/-/media/reservebank/files/oias/2019/response-t…

About what?

Banks create money to lend out. Customer’s money once deposited becomes the property of the bank which is used by them to do whatever they want.

Banks don't lend out customer deposits, these are held in their reserve accounts at the reserve bank

Bust a gut and point to them in the following links:

https://www.rbnz.govt.nz/markets-and-payments/our-balance-sheet-at-work

https://www.rbnz.govt.nz/statistics/r1

https://www.rbnz.govt.nz/statistics/r2

https://www.rbnz.govt.nz/statistics/r3

Deposit levels are falling monthly

Personally, I took advantage of the current strength of the Kiwi dollar and got my deposits out of NZ a few months back. It's not like I was going to get any interest anyway, so I may as well park it somewhere with deposit guarantees.

Where ?

ponzikiwi... Don't bet your house on it.

You obviously don't understand how fractional lending works.

B21

Fractional reserve banking is a myth. Prof richard werner proved it. Banks are creaters of the money supply and are not reserve constraint.

Ah,,, another conspiracy theorist I see

This may well correlate with sales in NZ excl Auckland falling in January by 10% compared to prev January.

I was recently reading an article about an American couple who were accused of defrauding the court system and profiteering for years. An aspersion of guilt was having a palatial home worth less than the average Auckland house.

Here is is what really happened today

https://www.zerohedge.com/markets/stocks-bonds-are-plunging-powell-fail…

Hilarious. These click bait article popping up again as they were back in 2016 and all the desperados are all at it again willing it on and convincing themselves they are all suddenly going to pick up some bargains.

If there is any sort of correction it will be single digits and then in a few years time start an upward trajectory again as normal.

20, 30, 50% declines please...so many dreamers on here it’s incredible

In a free market they would have already.

But we are in an extreme market manipulation state.

You picking they won't decline is a relevant as someone saying they will. You are effectively calling yourself out.

LD... yeah I mean look at the last FOUR ten year cycles. You would have to be a complete fool to think that things might change and nothing lasts for ever. Nothing in the past points towards anything changing. Why can't these dreamers spend a few minutes looking at the "evidence of the last 40 years" instead of moaning and being negative.

A financial crisis will bring it down

Fritz

Just like a global pandemic?

Don`t want to be the doomsayer but perhaps there`s more on the market in Auckland now because they`re sick of the Covid shit there and are heading for the hills which if anyone had seen the cars last Sat night leaving on the highways you might understand.

If prices start to fall the herd narrative will be along the lines of “well in the GFC house prices only dropped 10% so we aren’t too worried”

But this time, as house prices are falling interest rates would be going up. It will be global not just in NZ.... George Gammon has just made a youtube video explaining how interest rates could go up significantly through the actions of the FED.

Breaking News

Leading real estate agency, Barefeet and Tomtom, have just reported a huge influx of new listings of coastal properties this morning. Listing prices smashing all-time lows; some properties listed at 50% discount to current levels. Great opportunity for FHBs.

streetwise... no doubt they have doubled their (% based) commissions so their income is not affected?

NZ Insurance company report huge increase in profits insuring these properties

The RB and Trading banks knew in 2019 that there had to be a correction. But when covid came along it was not good timing. So they threw out the rule book and pumped in cheap money and loose lending. They over cooked it a bit. Now covid is under control and vaccines have the end in sight. They need to force the over leveraged to unwind their positions. Its called a pump and dump. The insiders run the game and they never loose.

Love the DGM article and picture- didn't know trans-geographical flow can be that turbulent.

How apt we are getting an earthquake and lost count on the prophets of Ahab.

Forgot to mention that the huge number of rental apartment vacancies is increasing availability which will compete with units and other lower segment homes, effectively pushing the prices from the end of the market down.

Very good article Greg

"The latest figures from property website Realestate.co.nz suggest Auckland may lead the housing market down as it eventually starts to cool."

A lot of commenters on here interpret this opening sentence as "the values of houses are going to go down" and some even put % number of falls in value. Personally, I don't think that's what Greg meant, in my opinion he means the RE market will go down from it current giddy heights, with fewer sales and lower value increases to be expected.

Agreed. The DGMs come out and get excited at the prospect of house prices falling. Doubt it will happen.

the heat might come off for a year or so. But we will be in the same position next year.

Anybody except housing market cheerleaders would be excited of falling house prices, it is something positive for the future of our country. The rampant hyperinflation we had over the last few years needs to be reverted as soon as we can.

I expect house prices to keep rising as banks are awash with customer deposits which they can lend out..

By how much? -30 -40% Everything is about offer and demand and leaving aside the recent past trend was an unsustainable spike conditions are changing and the pool of people that could afford a deposit with the current prices is getting smaller and smaller every day.

PonziKiwi is being facetious.

The only word in the English language with all five vowels in a row.

Eventually people will get sick of looking and buying property all day everyday, once overseas travel reopens people will spend massively on overseas trips and property market will slow down a bit.....until then.

Waiting for house prices to drop has been a consistently losing strategy for quite a while now. There are a lot of forces working against you if you play that game so it is a very brave, more like foolhardy, approach.

I don't think it is sensible to give too much thought to apocalyptic or 'black swan' scenarios. Yeah it could happen but it is out of the ordinary and rare. The modern world, especially the West, has the status quo as a primary focus. Everything is designed to keep things stable, the two party political system, property rights, the cult of individualism.

Ah and yet we find ourselves in the predicament from the very same mentioned rare event.... black swan (COVID)

Was GFC also not a event that arose from the very same naysayers who couldn’t see that main-stream thinking’ could be wrong...

Go ahead and put your money on whatever gamble you think is best. I'm just saying the wheel is weighted in favour of those that play.

Look who is talking :

Forcing investors into new construction is a good idea. Delivers new insulated rental product, and leaves the older stock for fhb'ers, to get into the ladder.

He believes DTI restrictions and higher rates won't have an impact on the market? Delusional as always. Remember this was the guy offering special BNZ rates to all attendees to a conference. Sound banking strategy.

I saw this NZ herald article this morning. Rupert Gough claims that young kiwi buyers are still in the market because of the wages increases they got last year. His explanation was that to afford another 100K on top of the purchase price - the couple needed to earn just $5 more an hour - which BTW equates to $10 400 more in income per annum.

I suspect Mr Gough is delusional - I earn $150K a year and my total increase last year was $3000 - most people got less than a 2% increase. I'd love to know what industry all these young house buyers are in where there bosses are giving them 5-10% pay increases. The last time I got an increase that big was 2004.

I thought take home pay dropped last year? Not increased. And that younger people (FHB) were more impacted by this than older folks in management positions?

Exactly - it shows how delusional the MSM have become with this housing market and worse still they are perpetuating price increases in both sellers and buyers mind - the sellers think - its okay everybody got $10 500 pay rises last year they can afford another 100K for my house and buyers think - I only need to earn $5 more an hour and I can afford a house.

More so it explains where housing prices will go next- given interest rates are likely at the bottom- house price increase now become dependent on peoples wage increase - if most couples are only taking home an extra 5K a year than-that means prices will only go up by 50K a year - which is roughly the 4-5% everybody is predicting - assuming interest rates dont go up. If interest rates rise- than that 5K wage increase will be used just to pay existing mortgages, there will be 0 chance of borrowing more.

A $5 wage increase is massive though if applied across the board and would indicate that there was severe inflation in the last 12 months (even if not measured in the general price level). If it was say $30 per hour, a $5 increase would be approx a 15% rise in wages. So does that imply we had real inflation of 15% last year? (as opposed to the fudged make-belive CPI numbers?)

If you look at M3 money supply - it increased by around that....15%

And it alwasy amuses me when you look at M3 money supply and its strong correlation with house price growth in NZ. And money supply was a historic measure of inflation. So in theory it would be possible to say we're currently experiencing and have done so over the last 20 years - incredibly high inflation. Its just that we don't talk about it because its not the measurement that central banks want to use at present.

Imagine if at some point that quantity of money flows is reflected in commodity prices as opposed to asset prices....the whole financial world will be thrown upside now (i.e. people want cash so they all try to sell assets at once).

Auckland has probably had an easy ride in terms of property price inflation. If/when the borders reopen I suspect it will remain the preferred destination for migrants. Consequently I doubt LVR limits will be able to reduce Auckland house prices for long.

Also Reserve Bank Guv' Orr seems pretty trigger happy, it won't take much to push him into negative rates or extending other programs (e.g. LSAP.)

Most migrants (if there are any in the next years) are usually not able to purchase their own home as they arrive, let alone have +200K deposit available right away. Regarding rates, since the trend setter is the US and they are likely to raise them (banks are already doing so) it is unlikely the rates will go lower anytime soon.

Market has peaked and housing and shares are boomer money chasing gain totally unrelated to real yield. Prices vs wages cannot double again. More chance of rates moving back in the direction of long term average.

Tonight, there are 1429 properties available in the Auckland City Centre on Trademe.

That number has been very steady for the last 4-5 weeks. Normally it would have dropped significantly in the last two weeks, with mass arrival of students including from overseas.

Will be interesting to see where rents head to from here, probably down.

interesting ive been tracking rental properties in the hutt valley since the beginning of the year - around one in 3 are having to discount the property to rent it - average discount has been $48 a week before they have tenanted the property

Recent govt & RBNZ gestures is just that, only a gesture a bit like shushing hungry feral cats, just to give them a pause, in order to get some sort of PR feeling of control in public eyes, but nothing concrete.. the hungry pack are now gathering watching & waiting, as more stimulus should be roll out soon now for Insurance backing.

Even the recent E/quakes justification cards for action are all undergone preparation right now.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.