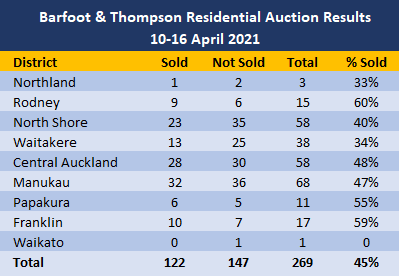

The sales rate at Barfoot & Thompson's auctions dipped below 50% last week (10-16 April), which meant more properties were passed in than were sold under the hammer.

There were more properties offered at auction by Barfoot by last week, rising from 236 in the week of April 3-9, to 269 in the week of April 10-16.

But the number sold was almost unchanged at 122 compared to 121 the previous week.

That meant that more properties were passed in (147) at the auctions last week compared to 115 the previous week and the overall sales rate declined from 51% to 45%.

Around the districts the sales rate was highest in Rodney at 60% and lowest in Northland at 33% (see the table below for the district-by-district breakdown).

Overall, the number of auctions taking place suggest the market remains reasonably active, however it is normal for sales activity to start to decline at this time of year as the market comes down from its March peak and heads towards the winter season.

However, the overall sales rates at Barfoot & Thompson's auctions have now declined for five weeks in a row, suggesting buyers could be being more cautious on price, or affordability issues are becoming more of an issue.

That may crimp the price expectations of some vendors.

Details of the individual properties offered and the results achieved at the auctions monitored by interest.co.nz are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

88 Comments

I'd expect there to be very very small growth if any going forward. Perhaps a small pullback of no more than 2%-3% in prices. However, you'd be mad to by an existing investment property at these values at this moment in time.

If you absolutely have to buy, then put in an offer 20% below asking and be prepared to walk away. Don’t let your emotions rule over the fundamentals.

I reckon about 40% below asking.

Even a 10% reduction on current asking would compensate an investor for 10 to 15 years of the additional tax on the property. You are in total denial as usual.

Denial of what, exactly?

That you are going to buy a house for 40% less than it's value pre interest deductibility announcement. That wasn't clear?

I feel sorry for all the real estate agents.

They may soon have trouble putting petrol in their new BMWs and Mercedes.

60% or I'll walk.... back to my rental

... that the silly landlord is running at a loss

Only the landlords leveraged highly in low yielding properties. Makes no difference if you have little to no debt.

As a side question Brock.. did you buy a house when they were 30% cheaper 2yrs ago, or were you wanting them cheaper then also?

Great question FP!

Could everyone buy an overpriced house 2 years ago with higher interest rates?

Or did people have enough deposit? There’s so many factors. Making assumptions just makes you look like an a..

I think FP makes a very valid point, it's often not about the money but about the mentality one has, some talk forever and never take action, then they're full of regret later on and make excuses, point fingers at others and complain endlessly

Whilst others are easily influenced, sell their property in haste only to watch said property gain another 20% in capital and then complain that they shouldn’t have listened to others.

hahaha, classic Albert. I wish I knew who you were talking about.

The only person who says "it's not about the money" is a person with money. Albert, my reply was to Yvil. In wrong thread.

Fair call Yvill.

Good on you for being able to see both sides of an argument, this open-mindedness will serve you well

Mentality does not buy you a house. Typical neoliberal narrative that helps nobody but those with the money to do so already.

Oh b21 really - it worked in the 60s!

Rob, neoliberalism as we know it started in the 80s, so I doubt it had any effect 20 years before that.

You are so wrong b21, the positive, proactive mentality has to come first, then the money will follow

American positivity

Golden rule

All it takes is positive thinking

Drivel

True, a positive mindframe by itself won't achieve anything, a positive mind and taking action will though. Also a negative mindframe will definitely not achieve anything at all!

OMG the Deepak Chopra brigade is alive and well. Must be because they have reversed their ageing.

A less-heated, winter market is a good time to buy......

TTP

"ANYTIME" is a great time to buy, ay TTP ;)

When is a good time to sell TTP? Is it summer? So that means I'll have to wait for almost a year?

C of H ....TPP is looking after his own "vested" interests ....I wouldn't take any notice, in fact his posts should come with a disclaimer, that they are an "Advertorial" for the RE industry...."Caveat Venditor" :)

So should the FHB write the same caveat, because they want house prices to be lower, because they want to buy?

Are you implicitly confirming that you guys get paid by the lobby for posting their message on interest.co.nz?

What's your fixation with people who have differing opinions to yours? You post that "they" must be in a "lobby group" or "paid by the post" or "RE agents". People lead different lives b21 and are allowed to have different opinions, it doesn't mean they work for some kind of "evil group"

My "fixation" would immediately go away if you would answer to the question, which funnily enough always avoid to do.

It is pretty obvious there is no evil side here, just interested sides. The problem you lack to grasp because of the life you were so lucky to have is that because of the interest of some, many are suffering a life of poor housing conditions and will never be able to afford a home of their own.

I wasn't lucky to have a privileged life, my parents never owned a house and they are still renting today. I grew up with the same narrow minded, negative mentality as you, what changed me was my wife who had a mentally of "we can" "let's do it" whereas I was always scared the worst will happen. IT'S ALL ATTITUDE & MENTALITY, the money comes afterwards, not the other way around!

Still didn't answer the question.

You always tell those that don't agree with your narrative they are narrow minded and negative, when it is actually those that wish things would get better and fight for it, and you the one that thinks that the same solutions must work for everybody since they worked out pretty well for you apparently, totally oblivious to the concept of equity. 25 years investing in housing and your parents are still renting...

Come on b21, why on earth should Yvil help his parents out? It is their own fault for not thinking positive thoughts.

Yet another comment sponsored by B&T?

I really question these numbers.

I was at the auction on the Northshore on Thursday and there was only about 6 sold out of 38 under the Hammer.

I looked at the B&T website the next day and there was still 6 show as sold.

Sorry but I don't trust the realestate industry or the Australia Banks any more.

They really want this fear of missing out and the Ponzi scheme to continue.

Wake up New Zealanders all stop buying let the market crash so we can fix this and start again.

Does anyone have insights into the market for studio and one-bedroom apartments in central Auckland?

TradeMe shows a lot for rent, with some ads offering a week rent free - which just never used to happen. But I don't think prices have really dropped yet.

Who, in their right mind, would by a rental grade studio after the recent tax changes...

A good time to buy is when everybody else thinks it's a bad time to buy.

Looks like the party is OVER. Hearing last week there is now a new trend in property FOMO is no longer an issue but FOPTM (Fear of Paying too Much) is alive and well. Lots of people standing on the sidelines waiting to see what happens next.

FOOP* Fear of Over Paying. This I CAN totally relate to.

EDIT to fix auto correct from can’t you CAN! We are going to an auction Thursday and I have no idea if we are going to bid or not or if we should just wait a little longer. Oh the joys.

What ever you do, don't bid against yourself. B&T seem to think this is normal and it isn't.

Whatever house you bought in NZ in the past 5 years you would have been overpaying so I understand the fear must be real.

Sarah, I hope you don't mind me giving you some advice (I have bought and sold properties for over 25 years). Before you attend the auction, have a firm figure in mind of what you are prepared to pay for the house and stick to it, there will be another house for you. The auctioneers wants to create a frenzied atmosphere where rationale goes out the window, stick to your budget. Don't bid early, never make the first bid and if you are the only bidder, don't bid at all, the agent will contact you after the auction (since you have registered) and you will be in a stronger position to negotiate. Good luck!

Hi Yvil,

Wise words. I always value your comments on this site appreciate that you took the time to tap this one out.

I don’t think FHBs can get “too much” advice at the moment. Well, so long as the advice is of from someone with experience and one whose position is somewhere you want to be or something that you admire.

Thank you. I’ll let ya know how we go. I’m sure there will be a property spin happening on interest on Thursday so I’ll see you in the comments :)

Excellent advice. Also will like to add that should not fall for multi offer trap and under FOMO, pay more as Yvil you rightly said have a firm figure in mind of what you want to pay or their will be another house.

Couple of suggestions further to those of Yvil's

Firstly regarding the comment "The auctioneers wants to create a frenzied atmosphere where rationale goes out the window . . . "

Make sure that you don't contribute to that by bidding quickly especially when it gets down to two of you.

Quickly putting in a following bid will often encourage the other bidder to be frenzied causing them to over-bid their proposed ceiling. Take your time, let them think about what they are bidding . . . maybe only when they take time and confer with someone else and get hesitant that you can be strong and quick as that doubles their time of uncertainty for them but if they come back quickly, then slow down and let them them stew a bit. In this connection sit towards the back of the room so that you can see who is opposing you - you can then see their body language and how they are reacting such as conferring and with whom. Remember that they are in competition with you, so be aware of your opposition and mind games are fair.

This raises the second point. Always take someone - other than a partner - with you. At best they will keep the agent away from you and trying to influence you (sit on the wall side of them so your support person acts as a physical barrier and also engages them) and they will provide information in your best interest. However, quite often that person (often mum of dad) will be conservative and not fully appreciate the market as you will, so prior to the auction let them know you want their support but that you will be deciding and doing the bidding. The best value in having someone else there is prior to the auction to be able to talk about things other than the auction and hence help you remain calm.

Best wishes for the auction Sarah.

What you're saying makes sense on the face of it, but let's not forget that the vast majority of us were thinking the same 12 months ago re property, shares the economy etc...look what happened there. There should certainly be opportunities out there now and into the short term but what happens beyond that is anybody's guess. Keep an eagle eye on what's happening, assess your situation and general affordability and if the numbers stack up, don your best negotiating hat and see what you can carve out. Getting on the property ladder is a very long term investment decision, so don't get too hung up on the possibility that prices may drop another 10% or whatever over a given period of time. If history is anything to go by, there's considerable risk they won't. Be greedy and try strike that deal with the fearful vendor sooner rather than later, while interest rates are on your side. In 2 years time, the likely worst case is that there'll have been give or take no capital gain, but you'll be 2 years into paying off that mortgage rather than lining a landlord's pockets and thinking coulda, shoulda, woulda. Much of the uplift we've seen in prices is simply a correction to reflect serviceability due to plunging interest rates...people need to get over it and accept it's the new norm. There will be wise old cashed up investors looking for opportunities atm too...those that don't need to borrow stand to make the most of the situation the government and RBNZ have presented. Just my 2c.

Hi OnTick

Thank you for your comment and the time you put into replying and giving your thoughts.

That’s how we feel. It will be our home for sometime and somewhere for the kids. We have our “happy figure” so hopefully we have a shot. At this stage the agent says we’re well ahead of the game buuuut she’s an agent. We shall know Thursday evening. It’s an ex rental and the soon to be ex landlord wants out ASAP so we shall see :)

Best of luck! If it falls over, there'll be others ;-) And don'trust an agent as far as you can throw them!

Hi Sarah, OnTick's advice is spot on, I'm sure he's not trying to trick you , he's not an agent or whatever some commenters try to make out. Listen to his advice it's 10/10. Good luck with your purchase and as OnTick says, if it falls over, there will be another house for you. Just please, for your own good, ignore the many negative comments and do end up buying a house that's great for you. Good luck

Has the percentage of so called investors buying dropped substantially as houses that are been sold in Auction are going at premium and if houses that are sold immediately after are also selling at premium so not much of a help to FHB but may be hope if RBNZ goes after speculators in their may announcement.

https://www.stuff.co.nz/business/opinion-analysis/300280371/residential…

As long as it was investment was fine but it has turned into housing ponzi supported and promoted by government and RBNZ resulting in FOMO like never seen before, where FHB under FOMO are borrowing beyond limits and taking big risk, so DTI if implimented may help FHB in avoid making irrational decession, which many may repent later as not having a house is frustrating but buying one beyond means and than having problem will be a disaster.

As the Prime minister believes in fairness - reason for doing tax changes, sh should immediately stop Interest Only Loan as this too give undue advantage to speculators in auction room by multiplying their purchasing power over FHB and also many speculators are able to speculate, only because of interest only loan and pay a premium resulting in 10% increase in a month.

Even if a breather for now as going into winter season but like tax changes, IO Loan has to go as it will not be long before jumps again.

Agree that the only way to kill FOMO : Greed generated from fast and easy money has to stop at the same time fear that house price can also fall is must to bring some sort of sanity in the housing market.

Government and reserve bank who can act to kill FOMO instead add to it by their statement and inaction / perception like when it comes to support housing market from falling they acted and acted overnight / threw everything as believe in policy of 'least regret' and in contrast when house prices are running away to new heights every week their policy is to ' wait and Watch'.

This sums up.

Government has done some announcement and now is the turn of RBNZ to walk with government and target speculative demand but will they ?

Have doubts as everyone knows that not only Mr Orr but everyone working in and with RBNZ has vested interest to support the ponzi.

Even Jacinda Arden is surrounded by people with vested interest and only see and hear what they want her to believe as it took an open home near her house to highlight the plight of housing market, which probably is the first time she experienced and saw something without her YES MEN and was immune till now, to all the buzz, since so many months where house price ran by as much as 50%.

Has she learnt her lesson to look beyond or is she still.......

I think we may have just experienced a “melt up.” The stock market is probably next. Could we be witnessing the final stages in the 80 year or so debt cycle?

To be honest, I don't think stock market has that much bubble especially when interest rate is so low at the moment. It really depends on which stocks you are looking at. With less investors in housing market, more investors might start shifting their money into stock now.

Watching MEL at the moment after the Blackrock forced ETF selloff of 1 billion after market last Friday. Im not buying the $6.05, games afoot I think. Will be watching closely.

I was just about to say that too. There are some amazing companies on the NZX. I said last week, keep your eyes open. We bought Tilt in early 2017. Now up 256%. Takeover action will see us forced to sell out after a great run. A lot of people who have had a one track property lens are going to have to think differently now. Good. FHB may just be able to get on with their lives, and society will be the better for it.

Dividends are pretty good too. Spark just paid out 12.5c per share, at a share price of $4.3 that's 5.8% per annum. Roughly 8x better than term deposits.

And you can deduct interest cost of money borrowed to invest.

US stock market has massive leverage in play and fantasy PE ratios as a result. Again its all about cheap debt fueled speculative capital gain. NZ is probably the opposite. Our property market however...

This is just about Auckland. Other regions may have some mania to go. Although I note Wellington City prices stood still in March.

Winter is coming...

It's all about the tax rules. I'm curtailing spending this year to repay loans faster and I'm hugely cf positive. Lord knows what others will do. Tourism businesses didn't need my money anyway.

Me too. Although I'm not a landlord, that tax change was a shock and made me pull a bunch of money out of property related shares (rest home sector) and throw it at the mortgage instead, plus I've gone and ramped up the repayments on the mortgage. If plenty of people take that kind of action, it's potentially going to be damaging to the economy as that mortgage repayment money effectively gets cancelled out of the system. It's the complete opposite of what the RB did last year by effectively boosting the value of property and subsequent wealth effect encouraging people to borrow and speed.

With a possible announcement regarding interest only and/or DTi coming in early May, you would be mad not to wait for that. Whats another two weeks in a world of overwhelming FIAT debt enslavement.

The script of the announcement that he will be doing in May is already drafted and his approach will definitely not be least regret - to act on interest only and DTI but will be wait and watch as he has already hinted in his last two appearance before the media.

May be the number of sale has declined but when looking at house price, they seem to be touching new height ( houses that are been successful) and to have any meaningful result, action by RBNZ is must but can vouch that will come up with data, reason and excuses to avoid or delay.

https://www.interest.co.nz/property/residential-auction-results?region=…-

Typically if the number of houses sales retreats prices follow after

I feel fairly certain that May announcement will underwhelm. Robertson philosophically against DTI's.

I'm not sure how much of this is seasonal and how much is the tax changes but both are at play - that's my first observation. Secondly Robertson cannot afford the financial instability of a dramatic (15% ish at a guess) drop in house prices over the next year, but has to balance this against the growing political pressure to be more aggressive with more deflationary measures.

A correction is needed and although those posting on here wanting a rapid, and massive reduction have blamed parasitic investors for hurting the average kiwi FHB, I find it interesting those same people are wishing financial ruin on fellow FHB's who have managed to buy in the last 1-2 years so they can become a home owner. It's confronting to run with hounds, then hunt with the wolves and continue to maintain the high morale high ground.

Agree that annualised fall will be very bad but if something shoots from 100 to 140 or 150 and than it corrects to 140 or 130 or even 125, is that bad or good fundamentally and economically also.

Even if house price fall by 15% ( though doubtfull) but still if it falls, it will be at where house price we're two months back - January 2021. Though few FHB who managed to buy in last two months will feel bad BUT as in for long time will not be affected if have bought sensible and able to service the debt as are in for long term as compare to them only people who may be hit are greedy speculators who are in to flip and may lose but again even in them those ( which are many) will not be that badly affected who are in buying and have flipped number of time, so even if get stuck in the last deal have made fortunes earlier.

So even if it falls now, will still be 20% to 25% up from last year.

Exactly. Only a miniscule % of housing stock has sold in the last 4 months. A correction of 10% would barely be noticed.

If you bought a house to live in the next few years it doesn’t matter what your capital value really is. My mortgage is far less than my market rent and looks set to stay that way.

"however it is normal for sales activity to start to decline at this time of year as the market comes down from its March peak and heads towards the winter season."

So it's "change in the weather" not "change in Government tax rules" that has cooled off the auction sales???

Article on this site only 4 days ago, attracts 299 comments “Housing market heading for the stratosphere as prices and sales volumes rocket up” …..then when this article comes out today “The overall sales rate at Barfoot & Thompson's auction has declined for five weeks in a row” only 23 comments ???

This says to me the “sheeple” are ONLY interested in positive news and will ignore anything against the narrative that “NZ property can only go in one direction – and that’s up”…. primarily because all their life savings and debt servicing are in residential property.

Crazy situation ! - do any of these people do any homework at all ? ….and have heard of the word “Diversify”?

Sit tight FHB’s - with interest on mortgages for investors now not being tax deductible, DTI’s in May, inflation around the corner with stagnant wage and salary increases, higher building costs (not to mention compliance costs !) etc I can not see any room for house price increases, in fact for them to stay at this current level, I would not put my “house” on it !

PS ...as for the "myth" that low interest rates are here to stay - I am very sceptical about that too.....why you ask ? Well in western economies, the lower the interest rate the worse shape an economy is in.

PPS ......not a "DGM" ...just a realist.

Europe and the UK economies are basket cases. The US is printing its way out. Which economies do you see starting to raise their interest rates? The kiwi economy is too reliant on exports to unilaterally change so as much as I'd like to see interest rates normalise I don't see the evidence. Despite the economical stimulation here we have a declining GDP so the best I see is things staying the same for 12 months. Outside that who knows - we may be back in lockdown with a new variant if we don't get our vaccine programme sped up.

CitM .....OK interest rates may stay low for a further 12 months, which would help the NZ economy etc at this stage - but watch out for inflation or worse still "stagflation". As a salaried employee, I think costs are going to keep increasing (as they have done already) while salary and wages will remain "stagnant" , so we will definitely not keep up with "true" inflation and NOT the RB's "version" which is completely "doctored" to a band that suits their agenda.

Seeing significant inflation already, electricity and gas providers have told me both putting up prices 20%, my work has raised prices significantly..

Worth shopping around - I got an e-mail from my powerco this week saying they are reducing my prices by ~3%. This is Electric Kiwi in Christchurch, could be a regional change but it's a pleasant surprise.

Oh it definitely is regional. I got the same email except my rates are going up - it's the second increase within 12 months. I'm in Auckland.

They won’t have a choice if inflation hits. All these supply pressures are building together to exert inflationary pressure

Did anyone see this?

Global financial ratings agency Standard and Poor's believes New Zealand house prices come down in the next two years. https://www.stuff.co.nz/business/124851267/standard--poors-predicts-an-…

Has Interest.co.nz posted an article on it?

Don't need to have a PhD to predict that house prices will fall, whoever is telling you the opposite is usually trying to create fear for their own interested purposes. BTW, S&P was predicting the opposite would happen not even 2 months ago, so it may seem they do not want the government to introduce further measeures

Another even more awful week to sell by auction. Agents should get the message and stop pushing sellers into auctions where they are wasting their time and money.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.