The worm may have turned in the housing market, according to Quotable Value (QV).

"For the first time since July last year, the QV House Price Index (HPI) has shown a reduction in quarterly value growth from the previous month," QV said in its latest HPI report.

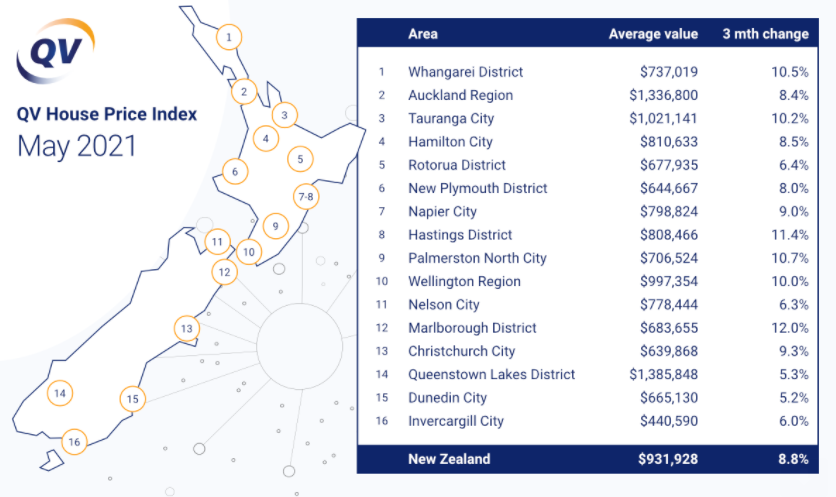

"The average value [of dwellings} increased 8.8% nationally over the past three month period to the end of May, down slightly from the 8.9% quarterly growth we saw in April, with the national average value now sitting at $931,928," the report said.

"This small reduction is particularly significant considering the QV HPI is a rolling average measure, which includes transactions from some of the most buoyant months earlier in the quarter," QV General manager David Nagel said.

"We can expect to see further reductions in the rate of growth as the impacts of the recent tax changes for investors and credit availability start to take effect."

However the changes in value growth were uneven throughout the country, with average value growth continuing to increase over the three months to May compared to the three months to April in the upper North Island, while average value growth declined in most of the rest of the country.

Of the 16 cities where value growth is measured by QV, value growth in May was up compared to April in Whangarei, Auckland, Tauranga and Hamilton, down in Rotorua, New Plymouth, Napier, Hastings, Palmerston North, Wellington, Marlborough, Christchurch, Queenstown-Lakes, Dunedin and Invercargill, and unchanged in Nelson.

The table below shows the average dwelling values in all 16 main urban centres and the value growth for the three months to the end of May.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

112 Comments

The moment of horror is when the US cannot handle its inflation and decides to raise its interest rate.

xingmowang - agree and the "herd mentality" of your average NZ Property Investor doesn't understand interest rates and are conditioned to them staying very low - ad infinitum ! But when (note I didn't say "if") they do rise, the Labour government will be happy, as they will save even more tax credits, on those soon-to-be defunct mortgage interest costs.

Plus the banks love it, as they hold the debt and get a greater return on that mortgage debt, so it's "buy low & sell high" ...... the bank always wins :)

But when (note I didn't say "if") they do rise, the Labour government will be happy, as they will save even more tax credits, on those soon-to-be defunct mortgage interest costs.

Except it doesn't work that way.

Right now if your rental revenue is $30,000 and your expenses, including mortgage are $20,000 you pay tax on $10,000, for most that will be $3,330.

If interest rates were to rise under the current rules, the expenses might increase to $25,000 and you'd pay tax on $5,000, which would be $1,665.

If the new rules applied in full today, then your expenses may be $5,000 and you'd pay tax on $25,000, for most that would be $8,250. If interest rates rose your deductible expenses under the new rules would still be $5,000 since the mortgage interest isn't included and you'd still pay $8,250 tax.

In other words under the new rules, it doesn't matter to the government what the interest rate is, it changing doesn't change how much tax they receive.

Under the current rules, it does matter. Labour will be happy they've implemented new rules, regardless of what interest rates do.

Yes, as I was looking at it from the IRD's point of view, as it's great for them (reduces credits to be deducted from your total tax bill to pay) and at the end of the day, any government would be happy with that, as it overall increases their tax take - but I wouldn't be surprised if National get in next time and scrap it ???

It may be a better idea to have the amount deductible linked to the official cash rate. Lower the official cash rate, the less that can be claimed. If interest rates rise a lot this policy may need to be scrapped or adjusted purely for financial stability reasons.

Things are pretty unstable now. I call 10% house price rises in a quarter unstable.

"The average value [of dwellings} increased 8.8% nationally over the past three month period to the end of May, down slightly from the 8.9% quarterly growth we saw in April, with the national average value now sitting at $931,928,"

Only 8.8% growth over a 3 month period....(bloody hell!)

And a national average value of nearly one million dollars....crazy.

Yet JB of Squirrel was mocked when he predicted at the end of 2019 that house prices NZ wide would reach $1 million within 5 years. It looks like we're getting there much sooner

If he was right, the government and central bank have really let down first home buyers as they should have taken his view on board, and intervened in the market to prevent this crazy level of price appreciation from happening (why? because it is very bad for the financial stability and prosperity of younger generations).

But instead they did the opposite. They created conditions to make it happen.

If the government is to claim credit for themselves in that the recent measures, removal of a tax rebate and bright line extension, are resulting in this apparent development as they foresaw, then why in heaven’s name were they not introduced earlier, much earlier?

then why in heaven’s name were they not introduced earlier, much earlier?

Because turkeys don't vote for christmas, and property owners don't vote for political parties that promise to materially impact their asset prices in the negative direction.

Of course you are exactly right. Would have been somewhat inspiriting if you hadn’t been though.

Property owner. Will vote for party that brings either houses down or incomes up to a reasonable ratio.

I will buy and sell in same market. It's irrelevant in that sense.

However I would like my children to be able to afford a house one day... and that is looking hard right now.

Regardless of price most young are commitment-phobes and dont want to buy a home. As for the not-so-young who had the same chances as others.... well?

Moving on to victim blaming before lunchtime has even rolled around?

Like if someone makes a choice saying the house is too expensive and chooses not to buy. Then later after the house increased in value they claim they are victims

#boomer #smashedAvocado

That's assuming they have a choice, many don't have the luxury of saying "oh house prices are pretty expensive I won't buy now I'll wait until they're on special".

Brock

Claims of “Victim blaming now before lunch”

Just tying to catch up, “Pitty me the victim” is in each and every day in the Breakfast Morning Report.

P.S. Have you solved that ad moan/gripe by becoming a financial subscriber of interest,co yet? Only 35 cents per day or still a believer in the free lunch? :)

The old whinging about other people whinging, but doing so from the high horse ;-p

Imagine being so bitter as P8.

" Neigh "

What moan / gripe?

Could you re-phrase please - I'm missing what you're trying to say.

Well youre on another planet so that is quite understandable

I have a friend in Wellington ( mid 30’s) with a $650knbudget to buy herself an apartment. She earns well and it’s intelligent. I’ve been following her house hunting journey over phone chats & listing shares via email. After 5 months she has given up ( she even got a group of buyers together to try buy a small 6 unit block) I find it sad and bewildering that a person like her will have to leave Wellington or buy a property elsewhere or stay flatting.

Plenty of people get mocked for predicting that NZ will be a banana republic within 5 years. It looks like we're getting there much sooner.

This data is really too old to give any reliable indication for what's happening in the RE now. REINZ data out next week is much more timely

Yes, and it's likely to show results as meaningless on a spectrum of more meaningless to less meaningless.

Really what happens now in terms of house prices is beside the point. They long ago decoupled from reality. For young people on average income it doesn't matter whether they go up 5% or 15%.

The only answer is for government to get off its ass and commence a massive house building programme.

My confidence in that being initiated AND being successfully implemented - close to zero...

So we are well into 'hopelessness' territory.

"Really what happens now in terms of house prices is beside the point"

Reading the comments on Interest you're forgiven for thinking most Kiwis are trying to buy their first house, in reality though, more than half the population own their own home and out of the 40% who don't only about half are wanting to buy, the others are happy to rent.

So where house prices go from here still matters to most

How do you know half are happy to rent?

@yvil, here is what I noticed last week in Hamilton. The market is still tight, not falling apart. The property we bought last week hard-won and not that special. Even properties with devlpmt potential in crap areas were strongly bid and fought over

What really blows my mind is that very few people seem to think ahead at what kind of place this country is going to be in the coming years and decades.

Not a pretty picture. But nobody cares.

The political system is simply out of date!!

just remind yourselves what Labour said when its in opposition and what it is saying now when it is in office. Same applies to National.

NZ is a country with no leadership.

Exceptionally poor leadership. Not as bad as Mao though (yet).

Taiwan is a country with fantastic leadership.

Brock Landers for new PM, he will do a much better job! Com'on Brock, stop complaining, make a difference if you think things are not right!

Brock Landers for new PM,

Not Ashley Church? I think many see him as the new deity.

AC..? A grandstanding self proclaimed expert with no property credentials

A failed Nat political candidate

Thanks for the vote of confidence Yves. It's a low bar to set, but you're right.

As an engineer I'm very skilled in solving actual problems and that's where my focus would be. The politician is focused on doing whatever it takes to be in power and paying lip service to solving actual problems.

I'd do a better job, but wouldn't make a good politician. Too honest.

Thanks Brock - hopefully you are following another fellow engineer Lyn Alden - one smart cookie!

https://www.lynalden.com/

Looks interesting.

"The major problem—one of the major problems, for there are several—one of the many major problems with governing people is that of whom you get to do it; or rather of who manages to get people to let them do it to them.

To summarize: it is a well-known fact that those people who must want to rule people are, ipso facto, those least suited to do it.

To summarize the summary: anyone who is capable of getting themselves made President should on no account be allowed to do the job."

That was always the interesting bit. STEM and medical people often found politics so ethically distasteful and soul destroying and would refuse to sell their ethics to go to be MPs. Yet how few MPs had solid STEM background, (worse if you consider the topics they are voting on), and even fewer with medical experience at the ground level even though they critically control medical health of the most vulnerable populace. At best all MPs have been playing on large investment incomes from day one and never stopped. Not one turned around and questioned why an unskilled backbencher has far more in hand with pension supports and perks than our most trained, experienced over hard worked nurses. The expensive branding merchants for MP campaigns must be creaming it.

Not PM more like Robin Hood.

Yes Taiwan appears a very well run country.

Xi of China is a poor leader - China's potential is declining under his reign, thanks to his arrogant, power-hungry, authoritarian mindset.

Where would we find an example of good leadership Xing?

Certainly nowhere near enough people care.

A very self centered country we have become.

why care when the government doesnt

The poor millennials, oh well they dont deserve a house anyway

People will only start caring once poverty and crime and general desperation reaches another level or two higher than now.

It's still not sufficiently in people's faces enough yet.

Even then what I have just said is questionable- the well off will deploy more security, and we will start transitioning to South Africa reality

Already there with He Puapua and the focus on reverse racism.

Labour is the new ANC and smilely is the new Zuma.

More hysteria from the right. There's no such thing as reverse racism btw, only racism.

Ok well I’ll call it racism then Mr know it all.

These figures are total nonsense.

An increase of 8.8% versus 8.9% is well within the margin of error

Any increase is calculated on the previous highest number so will still be a bigger number overall through the compounding factor

"The worm may have turned in the housing market says Quotable Value."

Greg N, check with FHB, what they feel. Does it help when price in Auckland is 1.332 Million and expect FHB to celebrate that now growth from 8.9% is 8.8% - BS.

Last year in begining, when it was approx $900000, it was suppose to be beyond and now when it has gone up by 40% to 50% to 1.3 million plus, this $#@& are justifying.

As mentioned earlier in Auckland Jacinda Arden supported by Robertson and Orr has killed FHB aspiration and hope.

FHB being extinct, if not already and the credit goes to Jacinda Arden and her Team -not of five million but her coterie of advisers.

The team of five million was marketing garbage, like most of the garbage out of the government.

Next time the government wants you to do something. Do the opposite.

Rumours of the death of FHBs have been greatly exaggerated.

https://www.interest.co.nz/property/110563/april-mortgage-borrowing-has…

Its more the paying back the debt which is the issue, not the buying of the house. Young people now basically buy with the expectation that the govt will devalue their debt over the next decade or so. If the govt doesn't meet these expectations they will not be happy.

(Some) People have stupid expectations, more news at 10...

To devalue the debt will require high inflation and if we have high inflation we need high interest rates.

The whole inflate the debt away is fine if its the 1980's and people haven't gone crazy by loading up with recorded breaking levels of debt relative to income. If wages don't increase at a rate higher than inflation, its a zero sum game that doesn't make any sense at all. And go and tell your boss or CFO that you want a pay rise higher than the increase in company revenue (i.e. relfective of the rate of inflation) and see what his or her response is like.

Young people now basically buy with the expectation that the govt will devalue their debt over the next decade or so.

This is the generally accepted 'cunning plan.' And the ruling elite still think it's their trump card. Only issue is that inflation of the money supply needs to flow into income. How this is going to happen is going to be most interesting. Furthermore, most people have little to no liquid savings. Now, this is also interesting. Benign income growth with a lifestyle of living paycheck to paycheck / robbing Peter to pay Paul creates all kinds of dilemma. Inflating the debt away is not necessarily as easy as it seems.

Exactly - we need wages to increase higher than inflation but I don't see how. Otherwise to me, that plan is a zero sum game given the quantity of debt in the system and the costs of servicing that in a higher inflation environment.

I added to my comment. Read it in all its glory.

The worm's derivative has turned ... maybe.

Absurd.

A slight decline in the *rate of growth*, when that rate is exponential, marks some kind of downturn?

At the current rate there's another $100k added to the asking price every few months. No one saving for a deposit can remotely keep up with that.

Absurd is possibly the best non-expletive word to describe this shambles.

$100k added to the value of an existing house every few months = equity that can be used as a deposit. Nobody saves for a deposit anymore, FHBer's just tap into their parent's equity for this deposit. Investors just tap into their own existing portfolio.

FHBers tap into their parents' equity... and young people not blessed with wealthy parents, tap out... (to Aus?)

Yes but tapping out to overseas has been the case for over a decade. Hence why thousands of engineers and nurses were leaving NZ shores every year for many countries with better healthcare coverage, better housing, better affordability of living costs, higher wages, better support structures and damn near anything but living in NZ and paying NZ housing costs on NZ wages. Staying in NZ is easier when employed by overseas companies but trying to afford NZ housing on NZ wages is long gone. We don't even have nursing accommodation anymore. Don't know how we will house the thousands extra nurses needed for the baby boom generation needing medical support in care and in their homes, especially now we are also removing the only transport option for many of nurses and elderly as well. We likely will and have been trending towards Japan's solution where literal prison is a better option than trying to get housing in NZ and since our prison populations are not getting significantly smaller I suspect that too has been a public housing outlet for a long time. Just commit a violent crime and you get housing, three meals a day, power, water, some heating, and education options. Better than the significant lack of housing support to disabled people who often do not even have bathroom access or any cooked meal prep support. Extrapolate to the growing weight of baby boomers without home ownership plus mental health deterioration and it is easy to see where we are heading.

Nothing has changed the market is still going nuts. That's a 3 month figure and the market would still be considered to be nuts if that was the 12 month growth rate. Even if it suddenly fell to 3% PA that's really the same as 5% PA anyway considering the recent massive gains. Nobody is going to panic until the market goes into reverse gear. The housing market is unstoppable and buyers know it. The very best anyone can hope for now with inflation going through the roof is still going to be like 4-5% PA increases. If your not already onboard, the gravy train has left the station.

The question one should be asking, is what happens when it eventually stops?

It doesn't Brock. We are now in an inflationary environment. Until inflation becomes a political issue expect don't expect change. 3 out of our 4 relevant political parties support this environment (Act, National & Labour). The party against it (the Greens) barely gets 10%. Young people saving for a house just got royally screwed by Jacinda & Co in 2020/2021. That's how this world works, it is a savage dog eat dog world. Look after yourself, your family & your friends forget wider society.

Sums up part of the problem we're facing though Donny...everyone is just thinking in terms of me and my family - not from a utilitarian view.

The view you show above, it the sign of a society in serious decline and usually prior to it breaking down.

Well why wouldn’t you? This govt doesn’t give a flying one about you and your family unless you can point to an indigenous ancestry.

Anyone who has built wealth is under siege by this govt and it doesn’t seem to matter how you attained it either.

Its look after your family first and foremost now.

Almost tempting to go register my Iwi.

Looks more like a stagflationary environment.

Incomes are not really increasing. To conclude that it will never stop is a dangerous folly.

That's my pick too.

I think FHBs are going to suffer -- not because of a price crash, which won't be allowed to any serious extent, but because they have 30 years to discover what a million dollars of debt really is in a stagnant economy. 30 years of handing over most income to the bank, no foreign holidays, no ability to take risks because there's a mortgage to pay... What for? A corner of Flat Bush or Wainuiomata that will be a pile of rotting Gib in 30 years, and probably worth the same as what they paid for it.

They may also discover what it's like to have the interest rates creep up as their loan balance reduces, keeping the interest dollar portion roughly the same for a good portion of the mortgage. Unlike historically where you'd see the interest portion reduce as the balance reduces and interest rates are dropped.

Maybe mortgage interest rates could be pegged to wage inflation, so any pay rises are consumed, and a 30 year mortgage will actually mean 30 years.

Great comment.

Remember kids its about serviceability, bring your own lube.

brisket, I'm sorry but this is really bad advice, you see given your own example, where in 30 years the house the FHB bought today is still worth only the same as what they paid for it today, they will have a mortgage free house, whereas the people who rented for these same 30 years have… well absolutely nothing. The unfortunate part is that the many people who gave you thumbs up, don't seem to realise this either.

PS, I'm not writing this to argue with you, I'm writing it purely to open some people's eyes because I was given the same terrible advice from my parents. They said you either pay the landlord or you pay the banks, it's all the same, you pay. Well they have been renting the same place for over 50 years!!! And what do they have to their name today… Absolutely nothing, zilch, rien, niente, nada, nichts. Had they gotten a mortgage they would no doubt at all have at leas CHF 1 million to their name today

Yes but in my example you have to live in Flat Bush

For 30 years

To conclude that it will never stop is a dangerous folly.

You have learnt well grasshopper.

The train never stops its called the Snowpiercer.

The ANZ-Corelogic price estimates have pretty much flatlined over the last 6-8 weeks on our place. If they reflect the general trend then it looks like the LVRs and the interest deductability change have done what they are supposed to, cooled the market.

My god, you view your property value weekly?! Sums up what is wrong with NZ now

It’s integrated into the ANZ app

Well then. That also "Sums up what is wrong with NZ now". Especially from a bank that could not get their testers to ensure Kiwisaver contributions we entered into the correct accounts or reading the right date from the database and pocketed much of the difference without reparations to the lost investment income of those kiwisavers.

I check it every few hours.

If you think the UK is your answer think again. Prices going up in Aussie also.

https://www.theguardian.com/money/2021/jun/07/uk-house-prices-rising-re…

... taking the average selling price to a record £261,743. Up a blistering £22k in a year.

Rookie numbers.

Greater London is £509k , 1mil NZD.

Average UK house size is 68sqm

UK's house price index is lower than NZs. Salaries are much higher too, especially if you want to use London as a comparison. House price rises there have compensated the removed stamp duty tax too. And there are other cities, such as Bristol, that are much cheaper and commutable to London (at just over an hour via train). There's also the benefits of living in a country that embraced work from home a lot more than NZ has. And this is ignoring life style choices. I'd recommend anyone skilled youth wanting to experience life try London.

Of course they should and we’ve all done it!

Im a citizen of both countries and I think when the time comes to raise a family NZ still has the edge, just. Though that’s changing by the day.

London is worth trying. It's a lot of fun. Don't stay too long though. If you are highly skilled, go work in finance, then bail out.

.. and yes, it does make Auckland look a bit silly with respect to housing and transport.

I recently returned from London.

Auckland is a sad clown show in comparison.

If you don't like it here, go back to where you think is better. Truely, why would you stay in a place you don't like since you have a choice?

That’s way too harsh Yvil.

There’s many reasons people come back and it’s not always that simple to just up and leave again.

It’s also totally understandable why many in that boat would be furious with what’s happened here also.

Despite the best efforts of the Brexit movement, London is still one of the great cities of the world with high incomes. Even public sector workers get a booster payment to live there compared to the rest of the country. Hardly comparable to anywhere in NZ.

My house in the UK is in a second tier city about the size of Christchurch. It's a 2 bed with a large garden in the suburbs. Cost 125k 10 years ago, now worth 175k - this is more representative of much of the UK.

The government is spending like a drunk sailor and the RBNZ has printed 100 billion dollars and rammed it into the bond markets. Money is devaluing, history is repeating. Asset price inflation will precede wage and consumer goods inflation which we are already starting to see.

This isn't about housing shortages or investors, this is about the flight of money to inflation stable assets and excess liquidity with low interest rates.

1) all asset markets have gone bullish - not just residential property markets. Commercial property yields are down, share market has gone crazy, people are throwing cash at crypto / etc.

2) there was a housing shortage when prices were going up by 3% under National with fiscal restraint - it should have dropped below 3% because immigration is way down, not escalated to near 9% like it has.

Winter is short before Spring invites you to Summer.

Be quick!

I stumbled upon this from Retired Poppy in March 2020:

"by Retired-Poppy | 16th Mar 20, 8:24am

Debt fuelled froth + complacency = debt driven deflation. Cheap money will not prevent what's coming next. All that was needed was a trigger to set it all in motion. NZ property prices and rents are destined for eye watering falls."

It had 37 upvotes lol

He used to be so proficient in his posts, he's gone very silent. I actually honestly wonder what he has done with his term deposits? That's part of the reason why assets inflate with such low interest rates, there's no return to be had by putting your money in the banks.

RP, if you're still here, what have you done with your term deposits ?

RP is not here because he has been busy digging holes in his back yard to bury all his money.

Lots of positives in those numbers. Where is your god now Mike Kirk and the DGMs??? Property gains to continue.

Worth getting your Auckland properties revalued you understand increased borrowing capacity. Purchased from a distressed owner pre COVID and seen more than 30% uptick. Exceeded even my own growth projections- very happy.

Heh, I bought in 2017 from a distressed Landlord. Have seen 250%+ gains since then.

For all we know the increase in prices could have been in March alone, the way it has been looking like in the past two months asking prices are down and we might as well be having falling prices in some segments of the market.

He called a big drop right as we got a huge rise. And the increses is price did not all occure in March, what are you talking about, almost all of the steep rise occured after March? Sure the market may now fall, but it doesnt change how hilariously upside down he called covid.

I believe we will see big increases over a lot of NZ including our area (Horowhenua) because;

Interest rates will only increase slowly if at all over the next 12 months. Demand is far outweighing supply. Many infrastructure projects are under way and more planned for our region. While slow at the moment due to Covid our population will grow significantly going forward as NZ is still seen a desirable country to settle in.

This tiny blip in avg house prices could be down to the season and some investors waiting for Labours next attack on them before committing.

There is no demand for the current prices, it is pretty obvious if you attend any open home. Lower rates have been already factored into the prices and raising rates will just help pushing prices lower.

I guess that depends where you are...we still have huge demand in Levin. Multi offers on average houses....Our avg house price still under $600k and will be 1 hour from Wellington one Transmission gully completed this year...plus Otaki to Levin now been signed off by Robertson so...we may buck the National averages if they were to drop in the coming 12 months perhaps?

Give it up b21 at least accept the facts as they stand right now. 50% are still selling at auction your don't need hoards of "Buyers" attending open homes you just need one serious buyer. The market is running hot in Rodney, I personally know of a recent sale and the open homes were mobbed with multiple offers put on paper. Prices still going up and my prediction is another +10% between now and Christmas.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.