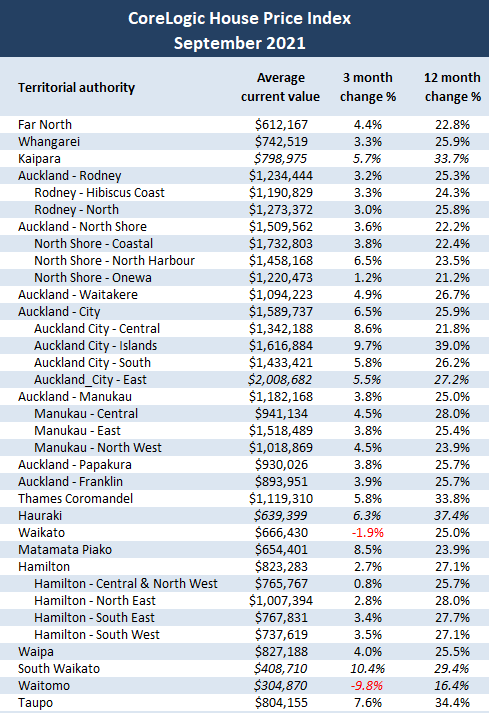

The average value of New Zealand homes increased by just over $13,000 last month, according to the CoreLogic House Price Index (HPI).

It shows that the average value of New Zealand dwellings increased from $937,148 at the end of August to $950,229 at the end of September - with both figures based on sales in the previous three months.

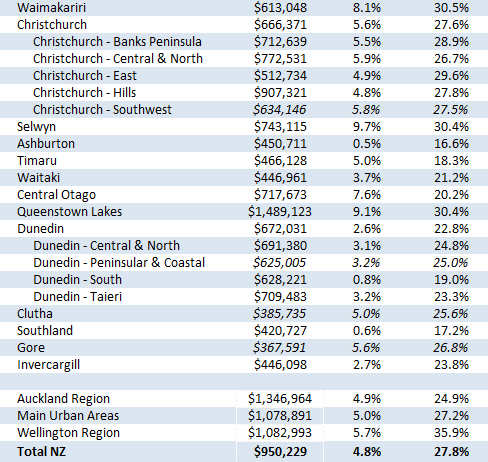

In the Auckland region the average dwelling value increased more than $9,000 to $1,346,964 in September from $1,337,648 in August. In the Wellington region it increased from $1,065,224 to $1,082,993, and in Christchurch it rose from $654,198 in August to $666,371 in September.

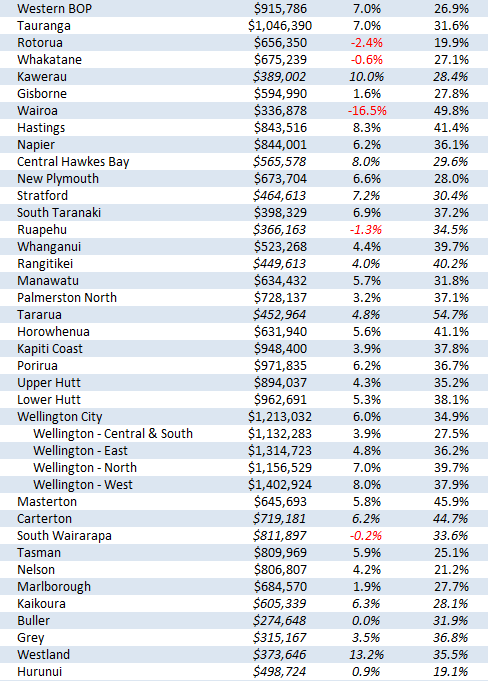

Although all of the main urban districts posted a rise in average dwelling values in August, average values declined in 21 of 97 districts monitored by CoreLogic.

The areas where average values declined were Far North, Kaipara, Hibiscus Coast, Central Auckland's southern suburbs, rural Waikato, Waitomo, Kawerau, Gisborne, Hastings, Ruapehu, Rangitikei, Horowhenua, South Wairarapa, Buller, Grey, Christchurch Hills, Dunedin overall and particularly the Peninsula and southern suburbs, Southland and Gore.

Most of the declines were fairly small.

However CoreLogic noted that although average housing values were continuing to rise, their rate of growth was slowing.

Average values increased by 1.4% in September, down from 1.6% in August.

September was the fifth consecutive month that the rate of growth had declined.

Although September's $13,000 increase was still substantial, it was down compared to the almost $15,000 increase in average values in August.

"The outlook for property values is for growth to continue to slow through 2021 and into 2022," CoreLogic said in the HPI report.

A key driver of this is increasing interest rates, but local factors will play a part to different degrees across the country.

"These factors include investor appeal, affordability constraints, the health of the local economy and borrowers' debt management behaviour."

The comment stream on this story is now closed.

137 Comments

House price up by appox $3200 per week and still government and RBNZ approach is WAIT AND WATCH.

https://www.theguardian.com/world/2021/sep/30/haves-and-have-nots-how-t…

Since pandemic is up by more than $10000 per week. Still no concern is raised.

I long gave up contributing on house price increases, however this one caught my eye - a knockdown 21km from CBD with glimpses of mangroves and mudflats for $4m. https://www.oneroof.co.nz/news/40222

Extraordinary, no other words for it.

Now, 165,000 new NZ residents visa holders and their family member will try to buy houses from the next year.

Nonsense, they have rights to buy houses today or on any day since arrival.

If you had a temporary visa would you want to buy a house?

If you then became a permanent residence would you want to buy a house?

'Wants' and 'Means' are very different things.

Using should/would approach is generally not a good idea when analysing data, in this case, the "scary new demand" of 165,000 people.

Think from your perspective, if you'd decide to move to a more developed place than NZ (say Belgium, Switzerland or Singapore), would you assume that you can build your life there, get a job, house, family one day, or would you move under the assumption that you'd be a forever renter and can be kicked out at any moment?

So my sense is that the moment we issue a work visa it's fair to assume that the person has an intention of building a life here. 165,000 isn't a new number btw (in fact we have a way larger number of newcomers).

Now for me personally, I know people who bought houses being on temporary visas, my neighbours actually, and I know people who waited for residency. I don't think that's relevant.

Mmmm, I don't think you can buy a house on a work visa. Needs to be a residence visa, permanent residence visa or citizenship.

Oh, I think you're right: https://www.newzealandnow.govt.nz/live-in-new-zealand/housing/buying-or…

That was different in the past for sure! Come work here for a few years, slave, don't you dare to stay longer, loving it.

It changed around 2016 or thereabouts but prior to that you could be on a temporary-class visa, e.g., work visa, and purchase property.

LOL you've got to be kidding me. Do you really think these new arrivals have hundreds of thousands of dollars saved up? Also, they've already been living *somewhere*, so this wouldn't affect demand by any significant amount.

Special grants and low deposit loans. I see some banks have 5% equity for new first home owners,. Think there are lots of different schemes available to help some people.

Try is the operative word, some here dont even try.

And kodus to them if they buy, they don't moan, just get on with jobs , life. They work hard, get on with things even at barely just above minimum wages while others complain.

I know where I would rather be for the same $$$$ NZD v USD ....... https://www.zillow.com/homedetails/577-Anapuni-Loop-Lahaina-HI-96761/68…?

This just getting absolutely ridiculous - the more these Auckland house prices go up, the greater the price "correction" will be ......but the sheeple still drink the koolaid !!!

And I don't think the renters are going to be able to "keep the pace" with their rents and the capital value of these properties......unless the Govt. forks out even more accommodation supplement, courtesy of the taxpayer :)

Someone in this NZ scenario is laughing all the way to the "bank" .......oh that's right, they don't need to laugh - they are already there !!

What irks me a lot, and something that not many people are touching on, is that Real Estate agents are now enjoying massive pay rises. Maybe it's time that they lowered their already over inflated commission rates, thus giving FHBs a bit more leverage. Selling million dollar houses in a matter of days, with far far less effort than in days gone by, they're just laughing all the way down to their nearest Audi dealership... again.

Does seeing other people do well irk you? Are they overpaid? Undoubtedly, but it's a free market so either sign-up as an agent or start your own Agency if it's so easy. Barriers to entry are low, so why don't more do it? Because it's a cut-throat, ruthless industry where you need the hide of a buffalo and only a few make the big $'s. You can expense the Audi as well.

Yes, barriers to entry are low, and being a largely unregulated industry, although minimal, it certainly can and does attract a number of unscrupulous and unethical 'agents', who are cleaver enough to jump in and seize the ability to manipulate buyers and seller alike, in order to 'legally' make a much bigger and often dishonest buck. Just saying..

The top real estate agents are really very skilled, but not that in the way traditional metrics like iq capture. The people I know that got wealthy (like $20m - $100m+) have no better than average iq but very high eq and drive and discipline.

Good on 'em ozzzy2 .....the RE agents can charge as much as they like ! ....as if you are paying these huge amounts of money for a property, you should have enough "smarts" to bargain their fees down .....I know I would bargain their fees down, as they are so friggen' greedy, as in reality they would do it for a third of the price !

Why do Kiwis think just because the fees are on some glossy brochure, it's "set in stone" .....I have always "shopped around" for an agent and go for the one who can provide me with the recent sales figures to back up their "blurb" !

It’s not that easy at all trust me. My wife’s good friend is one. She makes 300k+ a year but she has no time at all. It’s a 7 day a week job. Whenever we see her she just can’t get away from her phone. She said she will keep going until the cycle ends and then take some time out with maternity as she’s almost completely burnt out. It’s all hustle.

Doesn’t mean much if one only owns one property.

And yet the government mouthpiece that is RNZ focuses on a drop in the growth rate of 0.2%

Same with Stuff. Weirdly portrayed as a cooling, declining market. The wording would have you believe house prices are going down.

Nothing to see here folks. No action necessary.

Yeah you don't see other media posting the values listed like this, it's definitely sobering and would be a wake up to the masses...

Media suffering from Stockholm syndrome with government and central banks.

More likely profiting from advertising revenue from RE companies / banks etc.

They use the same wording with different meanings.

They really should say growth is decelerating, although not by much.

House owners/investors enjoy yet another windfall gain.

But are landlords ignoring the tenants who are making them wealthy?

Come on landlords. How about spending a bit of dosh on upgrading your cash-cow rental slums……

TTP

Only if I can deduct the interest as an expense.

Just look at all the old run down 'cash cow' student villas in Dunedin. They rake in $100+ per week per room for decades, and still wont spend a cent on them.

Hi ozzzy2,

What you say is undoubtedly true. It's downright disgraceful - and goes on in all university cities.

I'd llke to publicly name and shame some of these slum-lords.

TTP

Just shows the absolute greed of many (not all) landlords here in NZ .....I have seen so many cases in AKL, of usually young families, living in hovels with very young children, paying crazy rents with no maintenance done in any way shape or form.

House owners that live in the home don't benefit. Infact it makes it even more expensive to upgrade in the future. Many people who own their house are becoming accidental cash poor millionaires.

What a mess...

its no longer a correction on the horizon its going to be a complete crash

I honestly can't see it happening within the next 5 years unless real interest rates were to rise quite significantly.

Cobolt24 .......do you EVER look at what is happening overseas ? ..... to make a statement that in the next 5 years financial matters etc in NZ are just going to "meander along" with Reserve Banks and Governments (including NZ) dishing out money like "lolly water" (which all has to be paid back) is not going to have ANY long term economic effect ?

I bet you think these current prices are "completely" within the realm of "normal".

Oh, I'm usually quite bearish, I just think central banks are going to not raise rates very much as they know what will happen. Even the Fed is ignoring current inflation as 'transitory' and should it carry on long term, will instead raise the inflation target.

Never has such a bull market (of this scale) in property happened before globally. Typically large upswings end in large downfalls.

It could crash 50% and I don’t think many of us would care. I certainly wouldn’t, no plan to sell any time soon.

The trouble is many small businesses have their houses as collateral for their business loans. This with Covid would only need a small fall in house prices for businesses to start to close for banks to toughening up lending across the board.

If this results in job losses, then all bets are off.

But yes they are overvalued by approx. 50%.

Yes.

But the crash is going be the value of money.

Fortunately for the criminals who set monetary policy the crash will be "transitory" so they will excuse themselves from doing anything about it.

You guys still talking about the crash?

Greg Ninness, highlighting the data is just copying and informing but should one be not highlighting its effect on the society- both ways rich getting richer and poor getting screwed.

More than highlighting the data, would make more sense to raise valid concern and ask RBNZ and Government to hold them accountable and responsible for the mess that they have created and still not 7nderstanding - either not aware and playing dumb or ignoring to suit their vested biased narrative.

Have seen only one journalist - Jennee asking and raising some valid question though even she too does it in a limited way as a result does not help much in awareness and allowing RBNZ and politician to get away with smirk on their face with a feeling that they have got away with their response/bluff.

Highlighting data to inform people is good but agree, what are they doing to highlight the effect of ever growing house price on average Kiwi and what they as a journalist are doing to hold government and RBNZ accountable, which they should be being fourth pillar of democracy.

Guess everyone is here to be a part of the farce to make money so why disturb the people in power, Corruption

That's a tough ask - on the one hand, one of the media's jobs is to investigate the government's claims but on the other hand, it is also the media's job is to inform impartially.

It really should be the people's job to hold government to account, and the people do that by electing (or NOT electing) people into office that they feel are up to the task of looking after the people's interests.

So in this case, it's inferred from this factual report and others that the government is not doing a good job of keeping housing affordable. Is it Greg's job to question the government and drag them over the coals? Or the opposition's and the people's?

As someone on TV once said, "Just the facts, ma'am, just the facts."

House price not value*

Was listening to George Gammon and Martin North last night.

George thinks the media and society are suffering from Stockholm syndrome in the relationship they have with the central banks and with governments.

I mostly agree. At what other point in recent history could a government and a state institution (Fed or RBNZ) shaft such a high proportion (poor/non-asst owning) of society without being absolutely chewed up by the media or protest?

Then you realise they been mentally hijacked and incapable of clear thought because they actually believe the words coming out of Orrs, Adern and Robersons mouths. The level of either intentional or unintentional deception is quite high and doesn’t bode well for the future stability of society.

Scary times.

I watched that last night too. Martin and George are getting more exacerbated recently, their styles slowly heading further into rant territory.

Even Robert Kiyosaki is saying stuff like "Everything they do just makes rich guys like me richer".

I just refreshed my memory on the crash of 1929:

https://en.wikipedia.org/wiki/Wall_Street_Crash_of_1929

"The "Roaring Twenties"...was a time of wealth and excess."

Something for our reserve bank to consider

Mo nga waahine, Mo te whenua, Ka mate nga tangata.

More like the education system and its profit-focused institutions that have failed society - journalists (and the fewer and fewer young people joining the profession) are not taught as much to question and to dig for facts and truth. "Click bait" I think is the term more commonly associated with news styles these days...

More often they're taught how to write and how to present. And many media these days prefer to regurgitate rather than investigate - partly because they haven't got the time to fact-check or they don't have the skills/training.

You mean an article containing the phrase "According to his Facebook page..." isn't a sign of good journalism?

Better than "according to (anonymous aka unidentified aka unverified aka made-up) sources"...

So sick of those, especially in American media.

It is no surprise, govt is doing what they have said, it was clearly told by Robertson price will go up & you can see 5% decline in 2023.

You can expect this increase each month in summer & ahead. Now for those who are expecting crash, it is not going to happen till labour in power. Also don't expect anything from media they are sold out like property & there will be no protest because every one is happy in there home (if not owned than rented or govt provided).

Why PM take action as she is still favourite in recent polls (44%).

While i agree neither national or labour will proactively do anything to address affordable housing, its silly to think they have the means to keep a bubble inflated indefinitely.

Almost every economic shock in NZ is caused by external factors (we are such a small cog in the wheel). Labour and National have chosen to not address the issue on their own terms, so a correction will be "forced" upon us when the prevailing winds change. Sad but true, our political class care only about re-election and care little for the wellbeing and success of the country.

Well done again Ardern/Orr you guys are really competent.

What will you do next ? Hit investors again and worsen the rental shortage or just smile and remind us of the wonderful job you are doing looking after us with Lockdowns !

Oh well at least your portfolio will have gone up again significantly this month Shoreman.

Nothing to worry about.

There will be only two type of people living in this country in next 20 years. The ultra rich and the very very poor. NZ will be bach house of the ultra rich of the world and very very poor in the country to do their menial jobs. Everyone else will just move to countries where it's affordable to live.

At which point democracy has failed and the country will have to be run by a corrupt autocracy.

Think of the voting power of the poor which are making up a higher and higher % of society.

Labour are getting away with it at the moment because they promise the poor welfare and the rich policies to make them richer (ie having it both ways). But that doesn’t work long term. Eventually someone has to pay the bills. The middleclass is being destroyed.

I think it could work long term. Humans are pretty easily entertained and bought off. As long as there are plenty of machines delivering stuff, and the bulk of the population (the poor) are getting food and entertainment most of us will be pacified most of the time.

But the spanner in the works is resource depletion, and the stuff hose being crimped to the poor but still open to the rich. If life keeps getting more expensive and the birthrate continues it's collapse then that could be handled

Obviously my views are dystopian. I try not to confuse what I want with what I think will happen.

There will be only two type of people living in this country in next 20 years. The ultra rich and the very very poor

Very sad and scary, because someone once said society is in trouble if there are too many sad and lonely people, because they will have nothing to do, nothing to contribute and nothing to lose...

I predict the green party is required to form a government after the 2023 election. A tax will be put on property which will end the party.

Evergrande missed another interest payment yesterday.

Mr Orr will be using them as an excuse for holding the OCR, plus the likely extension of level 3 in Auckland. Mr Orr has had a really good comfortable job over the last 18 months thanks to COVID and general global issues.

How can Mr Orr use Evergrande missing another interest payment as an excuse for holding the OCR? Could you explain it in more details?

Well he could use the uncertainty around Evergrande PLUS the effects of a very long lockdown as a reason to hold for now.

2IC Hawksby was on 'red radio' yesterday stating categorically that Te Putea Matua will be be raising shortly

What is Putea Matua?

A mythical Maori deity that punishes the Maori people by forcing them into abject poverty through raising living costs, material hardship and/or making obtaining shelter impossible. Putea Matua tried to take control of Aotearoa shortly after Maui fished it up. Legend has it Maui had to defeat Putea Matua to originally free his people from slavery. It was prophesized that the ghost of Putea Matua would rise again in the future to try and impoverish Aotearoa again.

The reserve bank.

Putea is money (as in put it 'ere!) - just kidding that's my description. Matua is like authority/ wise figure. Hard to translate it.

Translation for tax is very appropriate - "take" (pronounced as two syllables not one).

While I agree that rolling news and internet allows central bankers to live in permanent crisis, there is no way he can use Evergrande as an excuse to stand pat. If anything, it would still be Covid.

Based on Auntys comments yesterday, we will have pubs open in auckland next week, you just wont be able to leave. Go the team of 1.5 million, beers ahoy.

They were about to raise the OCR several weeks back, but the very day before, we got a new case, and went into lockdown. I often wonder what would have happened if it were a day later..

It's a joke, isn't!

The only people who think this is marvellous are the ones with multiple properties.

For others it means not having the opportunity of a more secure life and perhaps deciding they can't have children.

A re-modelling of society for the worst.

I've been involved in property for many years and my observations are that it ascends like a soaring lark - and descends like a brick. This is because the market is extremely leveraged and just a tiny fraction of houses actually sell monthly. When it sinks the market locks up entirely.

It's hard to see prices continuing at this rate given the headwinds being faced

Many said that last year, and the year before, and so on.

Interest rates have been declining for many years. For the first time since the GFC, we are seeing a sharp rise (already up +60 bps from the bottom).

So, rates are back to where they were a year ago. Don't hold your breath.

I've been in since 1990 (before it was trendy) been a few cycles since then. I wouldn't say NZ property has ever 'crashed' but there have been slumps. Going long means you'll have good and bad times. The new entrants haven't been through a full cycle yet. The key is to hold on, and hold on some more. Don't sell, even if you feel you have to. Dig in and tough it out. I suspect this current cycle, (the biggest I've yet seen) still has between 25 to 50% more gain to be had. Given the unusual circumstances and unrelenting momentum. A good slump is in the pipeline, but not for a while yet. But even this coming slump won't roll back the previous five years.

Another point I'd like to make is the media's involvement here. Property articles have dominated the our media for the last ten years, entrenching the FOMO in the publics mind. Which has definitely added to the present madness.

You say:

'I wouldn't say NZ property has ever 'crashed' but there have been slumps. The key is to hold on and hold on some more. Don't sell, even if you feel you have to. Dig in and tough it out.'

And thus probably don't see the logical flaw in these two sentences. Most people don't.

The very reason you don't see much of a drop is that people feed the debt from other income sources. This 'toughening it out' does not show up anywhere in the housing stats. The money that goes into covering this is less money for health, savings, kids' education etc.

If this hidden money could somehow be recorded, it would show quite a large housing financial slump.

Do you have any actual published stats to back this up?

Yes, all those millennials who have bought over the past few years - despite contrary to the comments on this site arguing otherwise - will be pleased that they did.

Now enjoying the intrinsic and financial benefits of homeownership.

Really pleasing to see FHB over the past year at highest levels since RBNZ first published data in 2014 (numbers up 60%).

They are certainly braver than me.

It's good, but it's a small window.

Those numbers will drop away with rising interest rates and build costs.

It was a small window which will shut tight the minute interest rates rise. The problem is the longer the window stays open the worse off many will be. Its now out of control and the RBNZ doesn't know what to do, they are like a possum in the headlights, no movement no change just hoping by some miracle the market will come right by itself.

Exactly

HouseMouse

Yes, you just keep focussing on those “negative waves”. Likely no more difficult than over the past few years as the market is likely to flatten or even see a slight dip of a few percentage.

P.S. You missed the bit about the impending bubble burst.

You don't get it.

A large proportion of FHBs, at least in Auckland, have been buying new build townhouses. Due to soaring land and construction costs, the prices of those townhouses have been soaring.

So, it's typically 2 bed townhouses in low value locations selling for circa 750-770k.

There's very little chance that those prices will come down - land and construction costs won't come down.

With interest rates increasing, the pool of FHBs able to afford those townhouses will shrink.

Unless the gov gets creative to keep the prices up, a few ideas:

- negative rates

- lowering deposit (50-100k grant/loan)

- kiwi build model - buy using tax payers money/sell at the loss

There's very little chance that those prices will come down - land and construction costs won't come down.

They might be empty then if the punters can't afford them.

We were lucky - in the right time, right place - to be in that window. As FHBs we bought our 3 bed, new townhouse 1.5 years ago for 750k. We were lucky to get in before things went really mad. And we got a good mortgage rate of 2.3%.

Our townhouse is probably worth circa 900k now. We wouldn't have been able to afford that price.

Really empathize with FHBs.

HouseMouse

Well, you clearly did not listen to and take the advice of the prolific posters on this site at that time then. :)

A good thing about this forum is it's diversity of views.

Ultimately people make their own calls.

Question other's views, as well as your own. And then make a call.

HM

Agreed.

As an aside, one should also do this with bank economists . . . unfortunately many don’t understand this.

Two or three years ago I thought there was a good chance prices would crash. At least partly from hearing views such as your own, I changed my view. So thanks for that.

Doesn't mean I agree with everything you say!

But hey there would not be much value or interest in forums like this if we all agreed.

HM

Agreed one is not always right . . . the key is critically looking at a range of views and most importantly the rationale supporting that view and coming to one’s own conclusion. That definitely increases one’s chances of sound decision making.

I have four (two step) millennial-sons whom I have great pride in, and that has been my consistent advice to them. All four have their own homes - one reduced their rental portfolio last year and one son (single and living a great lifestyle) has a home and rental and looking at a further investment. They have all done that without financial support from me but making their own informed and critically made decisions.

People confuse basic economics about supply and demand, with Gamblers Fallacy https://en.wikipedia.org/wiki/Gambler%27s_fallacy

They confuse why housing will increase under our present housing policy (until we reach the tipping point), with either the Gamblers fallacy of, 'if I get a head, then the next flip has a greater chance of being a head', or the reverse fallacy, 'if its a head the next one must be a tail.'

Neither is true.

Our townhouse is probably worth circa 900k now.

How do you know it's worth $900K? Did Granny Herald say so? What if its value hasn't changed but the purchasing power of the currency you bought with has been decimated?

A couple of the nearby townhouses, same type and design, recently sold for a touch over 900k. I would suggest that's a pretty good gauge.

And that's pretty consistent with the general level of price movement over the last 1.5 years, slightly lower given they are townhouses.

It doesn't answer the question. A higher price can simply mean the purchasing power of your currency has weakened.

Bitcoin has messed up your head. House prices have gone up 30% in a year, pretty much everything else has not gone up anything close to that. So if Bitcoin goes up 30% in a year has it got weaker ? on the other hand if you intended to buy a house with your Bitcoin then your Bitcoin just got 30% weaker in 12 months.

1 Bitcoin is 1 Bitcoin. Just because its price has increased 320% in USD over the past 12 months doesn't change that. The purchasing power of the USD has decreased relative to BTC.

Could be but the 20% rise in constructions costs and labour/material shortages are good examples don't you think ?

Nice job.

Though someone who got an old stand-alone 60s weatherboard for about 100k more at that time would now likely have something worth 1.2+

Freehold stand-alones always go up more.

The experts all agree, problematic that the experts are all economists, the OCR will rise next week according to latest Reuters poll

https://www.nasdaq.com/articles/poll-rbnz-to-hike-rates-for-first-time-…

Hmmm. I just bought a house in central Wellington. I paid a lot lower than the estimate sites suggested and I genuinely think I was the only bidder. It’s patchy out there said the agent. I think falls in October..: solely because I’m usually buying at the top of the market!

Not in Auckland. It’s going nuts again all pre auction offers and auctions brought forward. Everything on my watch list is disappearing.

It actually beggars belief considering the levels it’s coming off but it’s a dog fight again out there.

Yeah almost seems worse than prelockdown, FOMO is through the roof.

Every time they say "it can't keep going on like this" it seems to get even worse. We look headed back to 19th century levels of inequality, with a small number of land-owning elites owning nearly everything, and the rest of the population forced to work in squalor.

Unless the RBNZ and government take their finger off the scale (whether by choice or forced to), I don't see things changing anytime soon, as much as I want them to.

There are only 4 ways to keep the ponzi going at this point, that I can think of

Take interest rates lower - not with current raging inflation

Significant wage increases - unlikely based on the last 30 years

Foreign money, through rich immigrants or overseas "investors"

Extending mortgage lengths (40+ years)

Heinberg lists six ways of resolving this debt:

1. Increase GDP growth - unlikely, reduced resources available, mass immigration becoming increasing politically difficult.

2. Reduce interest rates - nearly as low as they can go already.

3. Offer bailouts. Guess this could happen.

4. Reductions in benefits and standards of living - happening already...

5. Inject more money into the economy - inflation happening already.

6. Accept defaults, debt jubilee - seems like this coming closer and closer.

Maybe we should do what California does and give ability to hand the keys to the bank with no liability when there is no equity left in the property

For 15 years the comment stream here has been like a frequently uncivil civil war between the doomers and the spruikers. It now seems an uneasy truce has transpired wherein the doomers concede that prices did keep rising to dizzy heights, and the spruikers accept that this is not good for equality of opportunity or social cohesion.

Both agree that successive governments efforts to maintain price stability for housing have ranged from ineffective to clearly insane.

exactly its not a real estate "Market" as much as a socialised ponzi

What did Jacinda call it? Sustained moderation or something, I think. Classic.

Anything uttered by her or her inner circle of incompetent ministers is sustained bull****.

Is that a euphemism for Managed Decline?

Wairoa down 16.5%! Might have to go buy a Bach.

Cannot be long now before the price of 98 petrol in Auckland breaks the $3 a liter barrier for the first time. Getting to that cheap Bach could get pretty expensive.

I only go through 25l/100km around town, fill your boots.

Maybe the way money is created might be the problem? Most new credit (debt) goes into unproductive and speculative investments. Oh hang on, we’re not allowed to debate monetary reform. Ok let’s carry on with the left wing - right wing paradigm. Rearrange a few more deck chair while the Titanic sinks.

We can’t fix out current problems with the same level of thinking that created them.

This central banking system has clearly failed at it’s task so it’s time to go back to the drawing board and start over.

I’m tired of hearing the same arguments from the left or right about how each side has failed when it’s clearly a problem higher up the pyramid. Turn off the supply of credit and watch this house of cards come crashing down.

A healthy economy has a balance between savings and careful investment in productive business. Expensive houses isn’t wealth, it’s stupidity. Extremely low interest rates and easy money for everyone seems like a dumb idea to the average person but these clowns at the central bank can’t see that?

We’ve tried central banking and it failed, so maybe decentralised banking would be better? And remove the ‘fractional reserve’ component of the system as well. That doesn’t make any sense. Gold and silver worked for much longer as a medium of exchange than this crazy mess of a system. 97% of money is debt. If we payed all of our debt off only 3% would be left in circulation.

Every attempt at a fiat currency has failed in the past. Why? Because it’s too easy for the rulers to just create more money. It’s like a magic trick that they hope we don’t ever figure out. And so inflation is this ongoing illusion that we’re making progress.

It would help if this stuff was taught at school. Wow what an idea. Teaching stuff at school about how the world really works. That sounds dangerous.

There's still room for upward valuation.

Be quick.

This is the bull**** that's been stopping me from pursuing that next step in my career. What would be the point of a 20k raise, especially if it comes with more stress? Why should I improve my skills and create more value for a net 10k per year while house prices increase by more in one month?

Instead I've been doing the opposite now: putting in the absolute bare minimum, as I don't even care about my annual review. A 5% raise wouldn't mean anything. It has pretty much zero value when I'm looking at my goals in life. Nihilism hitting hard. And I'm sure I'm not the only one in my generation who feels this way.

This country is destroying itself at an accelerating pace. Cannibalising its core productive workforce just to feed the rich who are greedier than ever.

How many people here wanted multiple rental properties 20 years ago? Nowadays the size of your property 'portfolio' (god I hate that word now) is everything that matters. Yet it's the young that get sh** for wanting to travel once a year or buy a $1000 phone. But they should accept without question that rent increases by more than that amount every single year. Just how much more twisted can this 'economy' get?

Much as I loathe their racist surveillance state, the CCP gets it right sometimes.

Xi has formally stated that the CCP distinguishes between productive and unproductive economic growth, and they've started to crack down on housing speculation and fraudulent tech bubbles. (Of course, this is *after* blowing the world's most insane housing bubble, but you've gotta start somewhere).

Meanwhile, here and elsewhere in the West we're unwilling to concede that there is any difference, much less take steps to encourage 'real' economic activity instead of rentierism and bubbles. We're governed by children.

I think he might have left it a bit late, but he does have the ability to change course more easily than our 'leaders' can or want to.

The latest estimate I saw puts Chinese total assets tied up in property at 76%, and NZ is approx. 74%. USA it's about 35%.

If you study hard, get a good job, save money and invest wisely, we'll tax you harder."

That's why number of people gave up and now depending on state hand out's. Because they accept that by putting effort they cannot match up with increasing house prices and inflation.

So why to wake up early and slog, when you know it's not worth in this economic set up.

“In this present crisis, government is not the solution to our problem; government is the problem.” - Ronald Reagan, 40ᵗʰ president of the United States.

Good comment Court jester. My adult children tell me the same story. There is a real sense of hopelessness out there for young people with good jobs.

Yes, great comment - the incentives have degenerated to a point where behaviour seems bizarre by past standards.

I feel the same way, and I'm a renter pushing 60 (an empty portfolio - ha!), so this is not just about you kids. I was contacted yesterday about an IT job I could easily get making 2.2 times the money after tax and I'm like "Nah, it's not worth it". I won't even tell my Dad. At least the struggle is over.

China has this "lying flat" cultural thing going on - even Chinese kids are not bothering:

https://www.abc.net.au/news/2021-09-23/tang-ping-lying-flat-generation-…

Hey there. I hear your circumstances, feel for those, and thought to share a bit of my story.

This is the same bull**** that has had a great impact on me stepping down from my career path and starting a company. In my case, both I and my partner are professionals who were on 6 digit paychecks so our circumstances are not as tough as they might be for the average family. But it's hard to see the bright future for my kids in this country unless I'll manage to buy them a house each. Even then, there is a good chance they'd emigrate unless things change.

Did that decision serve me well? We're 9 people now, keep growing bit by bit, and honestly, we're yet to see if that was worth it. Certainly experiencing more stress. But I think you do control things in your life to some degree and doing nothing while becoming "average" in your career, even if everyone around you is "average", is not necessarily a good option to choose.

A mate of mine accepts low paid jobs in horticulture precisely because it's low stress and plants don't talk back. Having minimal stress at work is worth more than $ to her.

House prices goes down or up are just a number now for FHB particularly in Auckland as this government led by Jacinda Arden has killed the dream and aspiration of many.

Many have given up and the way it is continuing supported by likes of Orr's and Robertson, many will give up soon, if not already unless ready to pay a million PLUS for pigeon holes.

God save the country !

A bit of info shocked me today.

Labour have allowed interest deductibility if you rent your property out to a social housing provider.

Its fairly obvious the extent of ramifications this will have for the private renter who will find an even smaller pool of private rentals to compete for. I wonder when they will just raise their hands and go onto the emergency housing waitlist.

So essentially old houses will be rented to HNZ tenants and new to private rentals. Once again Jacinda and her bunch of misfits rearrange the deck chairs while the titanic sinks.

Renters United should be aware of this and the media must report it.

It is interesting why, if they think this is a good idea, ie allowed interest deductibility if you rent your property out to a social housing provider., that they won't allow the private sector to do it as well.

They give themselves benefits, eg not having to comply with the healthy house act, that they won't allow anyone else.

It's state control by stealth.

Exactly right.

A 1,613m² section sold for $2.43m in Wanaka this week.

https://rwwanaka.co.nz/properties/sold-residential/queenstown-lakes-dis…

It is funny that it is only a year ago since the PM said that property prices just can't keep going up this much, and so quickly. Yet it has only gotten worse.

Waiting for DTI to come in, and interest rates to rise.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.