This month's House Price Index (HPI) figures from the Real Estate Institute of New Zealand make for eye watering reading.

The HPI figures give a better indication of overall price movements in the housing market than either median or average prices, because they take into account changes in the mix of properties sold each month.

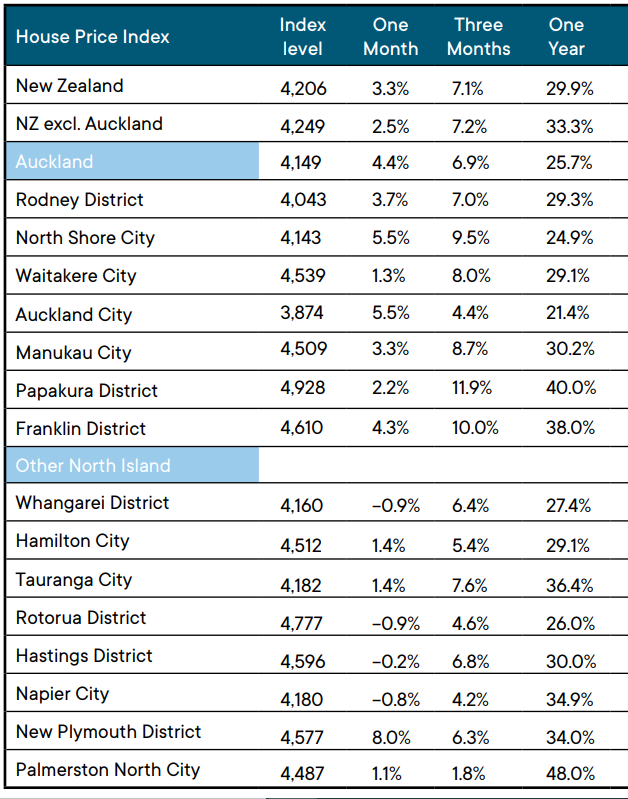

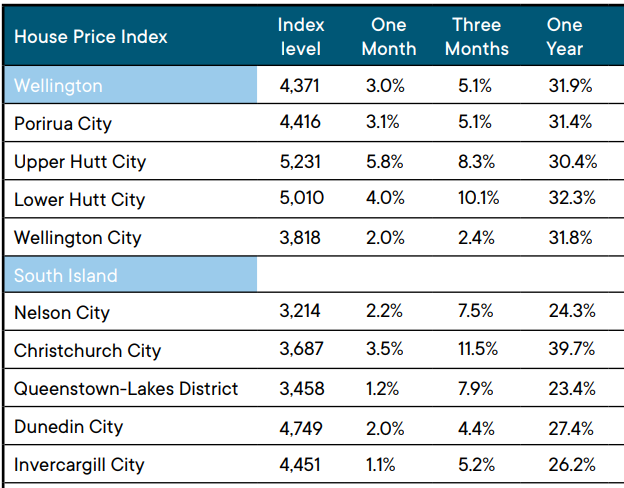

The most startling figures are those showing the price changes over the 12 months to October, with annual price growth hitting the 40% mark in a couple of places.

Palmerston North led the way with truly astonishing price growth of 48% over the last year, followed by Papakura on Auckland's southern flank at 40%. Not far behind were Christchurch at 39.7% and Franklin, also on Auckland's southern boundary, at 38%.

The average annual price growth for the whole country over the 12 months to the end of October was 29.9% and nowhere had annual price growth below 20% (see the table below for the full figures).

The main fuel for this bonfire of irrational exuberance has been microscopically low interest rates and the enthusiasm with which banks have been willing to lend people ever larger amounts of money.

If you have needed money to buy a home in the last year or so the banks have practically been giving it away.

However the drivers of the market are slowly changing.

Interest rates are starting to rise and lending criteria are tightening.

Supply and demand for housing are much more in balance as border closures have brought migration-driven population growth to a halt and developers continue to pump out the supply of new homes at a great pace, particularly in our biggest housing market, Auckland.

So are we at the peak of the current housing price cycle?

Unfortunately predicting house price movements is a bit like trying to read tea leaves after too many gins.

Over the last few months there have been plenty of commentators pointing out that while prices have continued to increase, their rate of growth has slowed, suggesting price pressures are starting to ease.

Then along came October's price figures and Boom!

The REINZ HPI shows prices in Auckland increased by 4.4% for the month and nationally they were up 3.3%.

True, the HPI posted declines for the month in Whangarei, Rotorua, Napier and Hastings. But apart from that, it was pedal to the metal for house prices in the rest of the country in October.

However prices can't remain detached from the market's underlying fundamentals forever.

If we are not at the peak of the current price cycle it's likely that we are not far off it, which is going to make for an interesting summer.

What remains to be seen is whether the peak will be followed by a price flattening, a modest decline or a sharp drop.

And the answer to that, I'm afraid, is written in the gin and tea leaves.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register (it's free) and when approved you can select any of our free email newsletters.

REINZ House Price Index October 2021

176 Comments

Its hard to see where this will all end, even with interest rates going up that hasn't seemed to slow. I have probably joined the group that Tony Alexander describes as old white men predicting some level of crash. However I am probably wrong. I personally saw the massive slump in houses in the Sacramento Area during the GFC. The price chart doesn't show the real extent of individual house price falls. I saw houses go from $400K to $150K. Families renting moved in 4 Families to a house to save rent. So at the margins is was extreme, until Blackrock moved into town around 2010 and brought up houses big time. Now they are back to boom time.

https://fred.stlouisfed.org/series/ATNHPIUS40900Q

However knowing the housing market has reached the point of extreme Irrational Exuberance it is still supported by many factors. The Reserve Bank, Banks wanting higher profits & market share, subsidies for rents from the Government, the immigration tap likely to be turned on, High Build prices, slow council infrastructure.

To push down house prices would probably take a large Black Swan event outside of New Zealand's control. What would our policy response be to such a situation? QE and low interest rates. Increased Immigration. A repeat of our policy to the GFC.

So I now assume that house prices will remain high until we reach a point where QE no long has an impact as it has been to over used, like some Antibiotics.

As on older guy watching this I find it sad for young people, the social implications of high house prices are detrimental to the wellbeing of most kiwis.

Steven Joyce in the Herald this morning well worth a read. I don't normally agree with his views, but today he is spot on.

Life is a competition. It starts from the time the sperms race each other to get to the egg. With a dose of help from the MAD bank, my two sons recently each became homeowners. Even though the bull run in prices has largely past, it's not too late in my opinion. They need homes and there is a lot to learn about ownership and rental investment that you dont get from reading textbooks. You will always have young people but the young still need to grow, learn and mature.

Your kids are going to be forever soft with that bank of mum and dad help. Unable to fend for themselves in the real world.

Au contraire BL. They have to toughen up fast, one is using his as an investment and the rental investment environment and regulation in 2021 is ridiculous.

And that's the reason for the uptick in new listings. Smart landlords are exiting.

Researched figures please not vague assertions

Sure, https://youtu.be/vl1ewsQVuMQ. Update From Lowe & Co. Straight up facts and opinion.

That is Wellington, if you are not going to bother spending your time to note the figures why should I

From Barfoot and thompson the new 2012 residential listings for october compares to 2119 last year and 2335 last November. Further, the 3041 properties they have on hand is the lowest october number for 20 years .. not the floodgates opening but probably closer to the pearly gates than anything

I have done some personal research over the last 2 years based on Wellington Market only - not the whole of NZ and based on trademe listings (total I dont seperate land/ townhouses or houses- just total listings)

Nov 2019 - total Listins was

Lower hutt : 243

Upper Hutt: 156

Kapiti Coast 213

Porirua 116

Wellington 606

June 2020 - so first month after lockdown and start of the boom

Lower Hutt :239

Upper Hutt: 131

Kapiti coast : 230

Porirua : 130

Wellington :453

I also took at that time Queesntown = 453 and North Shore Auckland 1256

As of today

Lower Hutt : 360

Upper hutt : 135

Porirua : 125

Kapiti coast :203

Wellington 569

North shore :1179

Queenstown : 279

so at the moment - Lower Hutt has its highest listings in 2 years (its actually the highest in 5 years- based off other data sources) Wellington and upper hutt are about 10% down on same time 2 years ago and porirua and Kapiti coast have similar listings to 2 years ago and also in line with June 2020.

Another way of also looking at stock is to take number houses sold on the REINZ reports and divide by number listings ie Lower hutt sells between 35-40 listing a week - 140-160 listings a month so Lower hutt has roughly 9-10 weeks stock for sale. MEaning housing listed today could take until Late Jan to sell.

Wellington sells roughly 60-70 houses a week so there are 8-9 weeks stock on hand. Upper hutt sells 15-20 houses a week so there is 6-8 weeks stock on the market.

Agent in Hamilton told me recently they usually have about 1000+ homes available to sell, recently they are down to about 300. Just no one selling except for the new builds. And there are actually quite a few going up around the place. This in-full housing is great to see.

Older property's are waiting their 10 tax free time to be up.

There is no uptick in listings there is a shortage of listings. What planet have you been on.

Why are your comments always so aggressive?

it’s like listening to the bully at school

Its banter tomjones04

It makes you sound like an arrogant twat though

This is true of residential but whoa Nelly have the rural listings blown up. I was starving to find land of any interest over the past 6 months and now there is a veritable smorgasbord and the chef is busy serving up more to my table every day.

Mountie

"uptick in new listings...investors exiting"

You can't be living in a nice suburb just outside the double grammar zone. For the first time in well over 15 years in both my area and my sister's a kilometre or so away there are no real estate agents' signs. Perhaps you're living in an area where all those gang shootings have been happening.

I admit there could be an upsurge in listings of all those blocks of penitentiaries, sorry, apartments, being built.

Unlikely mate, most smart land lords are set up for very long term ownership. What we may well see is high risk portfolios, or shorter terms positions, liquidate. No indeed, smart landlords have seen the tide come and go, and prices on any particular day are not of much interest to them. Why? Because smart land lords run profitable businesses. Remember that if you sell rental property because you expect capital prices to change, then you are not a landlord, and you will need to pay tax even without a bright line test.

Rubbish Brock, "Soft" or not comes down to the persons personality. "Soft" is where the next generation cannot even be bothered to go to work, live at home, sponge off the parents and friends and have no plans or direction in life and are dreamers. You can give the right kid with the right attitude a helping start and they will triple that early investment in them. I got given a helping hand and that $125K turned into $1.2m and totally changed my life.

You're only worth 1.2M at your advanced age?

Sounds like they gave that money to the wrong kid.

LOL I'm in the top 5% of the NZ population.

Top in what Carlos..being wrong on many things?

You're in the bottom 5% of the NZ population for IQ.

You wrote: "You have a couple of really fatal flaws Brock that are stopping you dead in your tracks."

Imagine how hilarious it would be if the person you were trying to mock had more wealth than that by his late thirties without ever getting a handout or owning a house.

You're an embarrassment gramps, perhaps soft is a family trait.

That's so funny Brock, you got the 5% correct but at 125 I'm in the top 5%. I'm sure there are people in their 30's with way more wealth, good on them I'm not here to tear them down. I could have gone for the next million but called time when you come to the realisation that enough is enough, why not leave an opportunity for the next person.

So why do you try to tear people like me down?

B L,

Is there any chance you could be persuaded to move to Australia? If you crowdfund for the fare, i will certainly contribute. Unusually, this will raise the IQ here, while lowering it in Oz.

Hi linklater01,

If you would like to contribute towards relocation overseas you are more than welcome. Shall I provide a bitcoin address for your donations? Let's consider the size of your donation the measure of your wealth and success.

Casual racism (even to Australians) is very out of fashion these days so just on the down low I would keep that one to yourself next time. It only makes you seem clever to dropkicks. Perhaps you are just trying to impress your peers?

It does appear to be the case that the more intelligent and ambitious kiwis do move abroad for better opportunities. As an observation after being away from New Zealand for some time, there is a very pervasive culture of tall poppy syndrome and nasty bullying here that you don't encounter so much when abroad. Dumb people here really seem to get a kick out of when they think they are punching down. We see it plenty with some of the toxic pieces of shit on this forum.

Something doesn't add up in this story. $21/hr, $180/week rent and they are both saving $333/week after tax, Kiwisaver etc.

Would that have not left them with <$50/ week for food and bills?

Only took 15 months to save $75k...

More than min wage at a supermarket yeah right

Also selling meth

I got the impression they were living at home and had to pay $180 rent but their parents covered the household expenses.

Dreams are just forward planning for some.

Brock landers,

Just another of your ignorant and objectionable comments. My older son is one of hardest workers I know, both physically and mentally. With a young family he went back to University in his early 40s to do a teaching degree. That was tough. He could not have got into the market many years ago without our financial help.

If you, and others like you, didn't provide handouts to your soft children there would be a much more level playing field and much less of a problem with house prices for everybody else in this country.

I am sorry if you find that objectionable, but this country used to pride itself on its egalitarianism, not hereditary handouts to your runts that are incapable of standing on their own two feet.

At least your schoolteacher son wont be able to afford to corrupt your grandchildren in the same way. God bless them.

There is a lot of bitterness in there brock, too much to be healthy. Some have an easier path in life financially and genetically. It's what we do with what we have that counts. Maybe you didn't have much of a hand up, but I can promise you there are many with less.

What we do with what we have doesn't actually count for anything and thats the crux of the problem.

What counts is who got on the rungs of the property pyramid at the earliest date. That's all that counts anymore.

The poor sod doing amazingly with what they have hasnt got a hope in hell against housing costs going up 300k in a year.

"Hard work" is a myth.

That's a victim mentality. You complain that "boomers" have had this huge advantage, yet there has never been a time in history when the young have made so much money so quickly. Tech, crypto and social media have been rivers of gold for young entrepreneurs. What is happening in NZ is no different to what is happening in sydney and brisbane. Yes, prices have shot up and it makes it harder, if you want to buy a house in a central Auckland suburb you are going to have to take some risk with your career and investments, no different to London or NY.

Oh mate, look at the data, please.

Every millennial has made a mil on crypto and tech, right? You’re talking about a small minority of people who has become wealthy vs generation who feeds by policies that screw the youth.

Auckland & NY is 🍎 to 🍊, same as comparing Auckland to Hamilton.

PS: not trying to complain here just prefer people who strive to be objective.

Given that even a lousy townhouse under the high voltage lines at Westgate is now asking 1.62 million, I would float the hypothesis that Auckland is the problem rather than young people just not trying hard enough or not taking risks with their investments and career.

Young people are going to leave New Zealand in droves. Keep your central Auckland suburbs they hold zero appeal to young entrepreneurs.

Wow, is that what they are going for? Madness

How about 1.7M.

https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

It's a clown show.

2.7 million plus for a townhouse in pt chev, times 4 homes on The Block. $2.25m profit is out of this world and shows the executive home market is doing well.

Yep and Pt Chev is not even that great. Full of narrow streets with wall to wall parked cars and housing NZ properties scattered about it.

Market is still very hot no matter how many emotional posters on here are trying to tell themselves.

"but I can promise you there are many with less."

There alway are. Even people in the slums of Nairobi could say that, It doesn't mean you can't critique the current situation. Young (and not so young) people in NZ have every reason to be angry at what has evolved, particularly given it was so avoidable. Greed has taken over, and the property market is the purest example of this.

Hey I’m fairly young and it’s hard for me to judge the way things were. Do you guys truly think that “greed has taken over” is a recent phenomenon?

It has most definitely worsened in my lifetime. The social fabric that I remember in my youth has fragmented to a great degree. People looked out for each other, it's far more dog eat dog now.

I have to agree with Ngrrk. Growing up my dad told me it was morally wrong to get a hard working kiwi to pay off an investment property for you, the tenant ends up with nothing. But now its become mainstream, almost half of the houses in Auckland are rented, morally corrupt landowners screwing other hardworking kiwis to pay off their mortgage. Profiteering and hoarding by any other name.

You have this misty eyed view of what NZ used to be like, it wasn't my experience, or my whanau. If owning your own place is the single most important thing to you then move to where you can afford to be - if that's Bluff then so be it. Life isn't fair. I have been berated by contributors on this site for 4 years about house prices, in that time they have more than doubled.

Always been a dog eat dog world here in NZ as far as I can remember, maybe at only 54 I'm not old enough to have witnessed the "good times".

It’s dog eat dog anywhere in the world but too many in this country have a sense of entitlement.

The immigrants arriving here don’t sit around complaining with their hand out they get to work and in a few years have built up their wealth.

Human nature, each generation "Expects" more than the last. I was lucky to catch the 70's, good times as a kid I bet the 60's were probably better still in NZ. Simple times compared to now. I feel sorry for the current generation of kids.

Your initial sentiment ('life is a competition') is at odds with your actions. If you wanted your sons to be winners you'd have left it to them to work out how to become homeowners. Although, admittedly I'm making some assumptions WRT the size of deposit gifted.

I just bought a house in a central Auckland suburb (without help from anybody), and as excited as I am to move in, it does sicken me a little bit. Would be more than happy to see a huge drop in prices before I even move in and start paying the mortgage. It's a pretty modest house that needs plenty of work done, and yet is somehow completely unaffordable for the vast majority of people. Something's gotta give.

Yes very correct that I want them to do well, not to win at others expense. I am happy for them to compete and have always encouraged that but sometimes a person also needs support be that emotional or financial. In the last 6 months I have seen them blossom, in a very non gender use of the word, and mature.

Well done to you too CK

You're a Doctor right? Average income for a full time GP is about $200k per annual. You have a significant lead over others. Recognizing all the hard work and study the chances are you had an advantage in getting into Medical School, probably well educated parents, private school or using the special entry criteria for Maori/PI. Not too many working class immigrants in late 80s. Not a criticism, and if you fought against the odds even more respect.

Really. What education did you give them?

I would never ask my DAD for a cent. I like to give back for what he did all those years when I was growing up.

This is just next level kids. I don't know if I would laugh or cry.

After all It was not their choice to come into the world so they deserve a handup imo. As for the education I personally gave them, it was not to expect anything from me when I eventually die, that I would be giving my 'vast' wealth to charity because that way I would be helping a lot more people. I was being only half serious but they did not know that. Also you assume that they came to me first to "ask for a cent". A very good opportunity came along and that was a great deal so I basically led the move with them. It was obviously the right move as we are all very happy as a family with the outcome. If you can please the wife and she is happy with you, you are doing well :)

Bl**dy Orrsome HW2 ... I should have done the same with my kids

Usually you don't need to ask your parents for a cent, they have already evaluated their chances that the money they gift to you will be pissed up a wall or not and they just give it to you. Its attitude and study at school before they even need to look at your work etic and spending habits. If its going directly towards a house deposit and they are in a financial position to help you, quite often they do.

True. The sad thing is that it's not a free market but the deliberate transferring of wealth from younger working folk and savers young and old - including pensioners. These folk should be very angry that their wealth is being transferred to prop up and enrich speculators.

Wait till one can buy houses here with cryptos. To the Moon.

Astronomical mortgage dept - sucking the life out of everyone who bought a house in the last two years...

Does the HPI take into account the size of the land/zoning or just the type of property (unit/townhouse/detached house)? I can’t help but think if we were able to weed out the properties with development potential (see most of south Auckland) these figures wouldn’t be nearly as impressive.

The HPI uses the CV to make comparisons with market value and therefore should account for large section size. Realistically it is only a measure of the market, an index and there are variations within that.

Good question and good answer from HW2. Although, how granular is it? I would doubt the HPI distinguishes between a house on 400 square meters (not readily developable) and a house on 700 square metres (readily developable)

I do think massive developer buying activity has distorted the median a bit higher, and I have in fact been anticipating and predicting this on this website.

I think that the last big zoning changes as much as the easy cash where responsible for this big increase last 2 years. Lots of people getting a 1.5mil payout on old average houses but large sections and then giving some to thier kids (to compete) or using it to buy a bigger place at say 1.8 or 2mil.

I wouldn't put it past us to pump things higher, but I just keep coming back to avg price to income, compare this to Historical /global data, and it doesn't read well.

I have wanted to know how, precisely, the HPI accounts for various dwelling types, sizes, specifications, location, land size etc... but I have never found a detailed explanation. If anyone has a good link on a DETAILED explanation, please post it here.

Thanks

an opportunity for some.there were 45 houses listed in whangarei this week and 36 the week before,compared to the rest of the year this would be a flood.

Listings are up 20-30% in most markets, investors with the new tax are already effectively paying 6% interest on existing or buying new at 3-4% yields and either way going backwards so are really questioning things.

The party is over. Last drinks at 2am. Headlines in the news are designed to get clicks.

Ironically a lot more properties would be for sale right now if not for the bright line test. The 2 year measure designed to stop speculators from avoiding tax on flips is now a 5 or 10 year political "we did something" statement preventing houses from being sold to home owners.

The only thing that will skyrocket from now is the emergency housing wait-list.

Compared to what though? I’ve certainly noticed a lot more auckland listings come on board but is it just pent up supply from people not wanting to list in lockdown (and now knowing more freedoms are coming) and are the number of listings any more than this time last year leading up to summer?

Listings are up 20-30% in most markets

Do you have a source for that? The latest REINZ report was claiming record low levels of inventory.

Just looking on TradeMe sorry. I have the app and there has been a real jump in the markets I watch and I speak with folks around NZ and they say the same. Example Rotorua was 160 now 240. Wellington was 450 now 570.

Compared to what, though? This time last year? Or last month?

We should expect to see more properties coming on the market at this time of year.

I'd like to see a year on year graph of the number of houses for sale in NZ. I've been watching hutt valley listings surge on trademe, it was 190 earlier this year, now it's up to 360. But like you said, it could just be spring selling season, I don't know.

Compared to everything; last month, last three months and last year.

Although we are more interested in turnover and weeks of inventory, we have kept daily totals of Trade me listings for New Zealand /Auckland and Waiheke for a year. As of today,' listings"( which could include house removals) nationwide are back to levels last seen in March of this year, having bottomed in September, Auckland listings are back to levels seen thru April to May ,below those of March but off the extreme lows of September and Waiheke listings remain low and about 40 percent below those seen in March of last year. Looking at the long term , listings not adjusted for stock remain very low, similarly sales or turnover of housing stock is very low in a New Zealand context.

I watch the Rotorua market, and it is not that many years ago that Rotorua listings sat at between 1000 - 1200

yep the listings are coming on fast now in my area. Started about 3 weeks ago. You will know when the market has turned, the PBNs and auctions will be replaced by a price.

Chebbo, there's a difference between new listings and inventory. Example if new listings go up by say 1'000 but sales increase by 1'500 inventory goes down by 500, even with the increase in listings

More listings than sales... replenishing inventory. Inventory levels are still at historic lows weavil

??? Your 2 sentences contradict each other, first you say "more inventory" then you say inventory is at historical lows. Make up your mind

Take it up with b&t if you do not like or understand it. Their figures for october are: 2000 listings and 800 sales as well as lowest october inventory for 20 years. Of course net sales is an absolute while lowest inventory is a relative. There is also the not minor aspect of the level of withdrawls, something they have not disclosed. So weavil, just maybe it is both. Ps before you start getting nìt picky, the numbers are approx

Why do you call me weavil?

I am sad that Christchurch, which saw house/plot prices essentially plateau for a decade after the 2010 earthquakes because land supply was thrown wide open, has now joined the race to the bottom.

It's a reflection of the fact that price osmosis, driven out of the most tragic cases like Awkland, eventually gets most everywhere.

Time was when cashing out of a rotten shack in the Big Awk would buy you two nice Christchurch properties. Them days are gone.....

Christchurch residential property prices also used to be constrained by local salaries. Employment mobility has changed the game and I've met a lot of people who have moved from AKL to CHC with their AKL salaries. A million dollars is not only affordable for those people, it is a massive lifestyle unlock in terms of lower debt servicing.

Good point. Begs the question then; Why are Auckland property prices not constrained by local salaries? We haven't discovered vast oil fields under the Hauraki Gulf. Average household income here is only $140k. Average house price here is 10x that. We're lost all grip on reality. I'm not at all interested in joining this collective delusion.

Developers, securing funds off shore.

Maybe volumes tell a story. If total national residential property stock is ~1.8m dwellings and annual sales volumes around 5%* (being generous), that's a total of 90'000 properties sold per year. According to IRD, there were 135'000 individuals earning ≥$200'000 per annum as at September 2020, and 5.3% of households with household equivalised disposable income (before housing costs) >$100'000. i.e. there are theoretically enough high-income earners and households around to keep prices elevated on relatively low volumes (compared to stock).

*headlines always imply that all property prices in a particular area have gone up X%, just because 5-6% of that area's properties have sold at those levels. This might be an ok extrapolation for fungible and highly liquid assets like stocks, but not for non-fungible, illiquid real estate.

Making predictions about the housing market is a bit like reading tea leaves, which is why we shouldn't try to do it. We should only talk in terms of risk.

We can't with any certainty claim to know that the market will crash this year, next year, or ever. What we can say with confidence, however, is that the risk associated with such an event is increasing.

If you are a property owner, you need to think very carefully about whether or not you are being compensated for this risk, and are sufficiently hedged against it.

Great comment.

Just an anecdote, but I'm seeing many more listing clusters than usual in CHC - i.e. house sells at auction for crazy price, 2-3 more listings go up on same street. In the most affluent suburbs, too - which to me is a sign that the top is in.

I am really interested in where house prices are heading. Really note any comments here relating to that. Totally disregard anyones predictions either way, including from me.

I wonder how many folk are putting their house on the market as soon as they see their neighbour do so (or planning together). Would seem to make sense in some of those suburbs to make them a target for developers.

It's the free gains, with a topping of cheap cash. We cant help ourselves. People avoiding the flipper tax when their "circumstances change". Once everyone starts doing it the market is where it is today.

Do we need more tax...stamp duty perhaps?

Definitely stamp duty

That prevents turnover for the right reasons though (eg old people will hold onto rotting villas in Merivale/Thornton/Ponsonby). Tax the land instead.

A quarterly land tax, that would absolutly work. Vote Top next time then.

I joined the party and voted for them in the Gareth era. Now they’re just annoying.

However prices can't remain detached from the market's underlying fundamentals forever.

The RBNZ & Government changed these fundamentals, over inflating a market that should have tanked a long time ago.

And we all know if prices start crashing, they will rush in with more OCR cuts, probably going negative next time.

Well, it's a welfare scheme for the wealthy now, not a free market. Our biggest welfare scheme by far.

The houses haven't really gone up in value, the bankers have just watered down the worth of their tokens closer towards their intrinsic value of zero.

If you trade your time in exchange for these tokens or try to collect them you are a fool.

You have a couple of really fatal flaws Brock that are stopping you dead in your tracks.

Envy? Jealousy? Feeling like he missed the boat but deserves so much more? Bitter man.

Nah I'm actually just strongly principled person who believes that everybody in kiwi society deserves a fair chance at life without the lottery of when you were born and how rich your parents are.

We used to pride ourselves on that. Now anybody who still believes that just receives petty and snivelling insults from boomers who had the world handed to them on silver spoon.

Egalitarianism has been dead for a very long time in this country.

Nonsense, the recent rise in property values has benefited Gen X and Y as well as boomers. I know lots of boomers who've worked hard for decades and never got any assistance from their parents while they were bringing up their families and improving their position. Their wealth is a function of time in the market more than anything else. No silver spoon for them.

Even Gen Z is still able to easily get into the property market in some parts of NZ like Christchurch. It starts with disciplined saving for a deposit.....never ever has been easy but still do-able today. A Gen Z couple should be able to save $60k in a couple of years. That's $576/week or $288 each for a couple. You know, sacrifice and all that boring stuff. If they're earning $50k pa each that's a combined $954/week to live on after saving....such a hard life.....

I agree. I was living in a car at 15, went to the mines in Aussie as soon as I could and got my first and only house in my early twenties. I don't care whether it's worth 200k or 2 million as I'm not selling. In fact I probably want it closer to 200k as my rates would be cheaper!

Back in the 80's both of my aunties were DPB mums from 18 years old and they both managed to buy a house while on a benefit, now nurses and teachers struggle to get on the ladder, let alone low wage earners and single parents.

It does make me upset when I hear about parents getting their kids on the ladder, not because I'm jealous but because it tells me that society is only becoming more and more unequal which is sad.

I think the difference here is not can your kids achieve things without your help, but how much will you improve their lives in doing so. Your kids may be saving for a house and be a little short - helping them buy it earlier saves them from being saddled with a much higher debit in the future (when they would have eventually made the deposit). I don't think helping your kids makes you/them weak. I understand the bitterness of those who have not had this help, however.

Why don't you elaborate on them just to demonstrate how little you know about me.

Spot on Brock.

What not to buy when looking at shitcoins - unlimited supply and shit governance team.

Funny the NZD mirrors these exact qualities!

Fix the money, Fix the world. Brrrrr goes the $3T platinum coin mint hahaha

It's all about "Perception". Whether in line with fundamental realities like earning power or not, perception of value is purely in the mind. How stretched beyond correlation to fundamental realites can perception push a market? Just as far as it can push fear, I suspect. And look how far that can be pushed with the use of certain tools.

The law of equilibrium is not just a perception but a physical reality. And so the bow will break (eventually).

So let's just say house inflation stays at 20% p/a (I'm sure some on here are predicting that 🤣), that means when my kids would normally be looking to buy a house in say ~20 years, the median house price would be $21,085,679 where we live (Akl $42,171,359)! Let's be really ‘conservative’ and say 10% p/a, thats still $3,700,000 (Akl $7,400,259) for an average first home.

I wonder what wage inflation will be like over that period, 2%? Let's give it a modest 3%, so the average income at the point when they will be buying a house will be $99,366.

I realise that these are just numbers and that house inflation 'can't' remain at 20% and there are other factors involved, but still a pretty shocking picture of where things stand at the moment.

If something cannot go on forever, itit will stop. Herb Stein, IIRC.

Ah, but when?

It stops before everyone knows it has - ie Lehman Bros. Evergrande will not be the same because everyone has been saying it's going to happen soon ... therefore it won't.

"Evergrande will not be the same because everyone has been saying it's going to happen soon ... therefore it won't."

It may not be the 'same' but it is 'happening' as you write.

and its all down to incompetence and backscratching at the highest levels

I personally see the reserve banks of the world worried about the new kids on the block (crypto currency’s) this phenomenon has occurred since they’ve had rates set so low. I can see rates going back up to put the value back in their currencies. House price declines will be collateral damage.

Interesting thoughts. On balance I think it is more likely that if they see non-govt cryptos as a threat to their power monopoly they will try to use regulation backed by surveillance and propaganda (not interest rates) to try and stomp it as much as possible.

If it is accepted that the main driver of RE price growth is low interest rates and credit availability then we can confidently say that prices have at the very least plateaued....no matter the desire by any and all parties there is no further capacity to repeat the long term interest rate decline.

Totally disagree on your last statement.

The next economic crisis will bring interest rates closer to zero, the OCR will probably go negative.

Which can only happen if central banks are prepared to accept a contradictory wage inflation spiral at the same time....how long do you think that will last?

Id suggest that it is exactly the 'belief 'you have expressed that has driven the last gasp of RE inflation we are witnessing.

This is a question only Adrian Orr can answer. If we had house prices falling rapidly and CPI still rising briskly, would he cut rates into an inflationary climate to save the housing bubble?

I tend to think ‘yes, but only to a point. 6% CPI to save the bubble, maybe. The do love the bubble. 10% would probably be too much to stomach.

Then id suggest Mr Orr has already shown his position....the OCR is on an upward trajectory and he is jawboning RE investment down....and thats with a relatively stable NZD.

If we go negative with rates we really need to ask the question why we as taxpayers are paying banks to lend to push up house prices rather than paying money to those who need it instead - which would increase the velocity of money through the economy because they'd spend it.

It seems blatantly immoral to use negative rates to keep the already wealthy protected from risk.

Negative rates wont stop the bubble bursting....indeed negative rates are little more than a slow motion default.

The FIRE sector, big business and construction sector never want housing supply to meet demand to keep prices high.

Therefore expect the govt to open the floodgates to mass migration again to keep the housing ponzi alive.

Furthermore, the govt will need to bring in submissive vaccinated workers to replace free-thinking kiwis who will no longer be able to work if they decline to be coerced into vaccination.

Meaning pretty much the only party you'd be able to reasonably vote for next election is TOP.

We are in a land price bubble and it's one the Reserve Bank of New Zealand and successive Governments have constructed. Bubbles in illiquid assets don't moderate, they expand until they burst and collapse.

We are going to have an Irish style correction where we get a cycle of population exodus accelerating the economic collapse. The only thing I'd say is that we shouldn't bailout the losers, in Ireland that was their big mistake, instead we will need to accept massive debt restructuring.

"cycle of population exodus"

Excuse me.... when?

When it’s easier to travel and make plans, and half our under-40s move somewhere where a working human being earns more money per month than a run-down shack on some God-forsaken suburban fringe.

Are the borders open without quarantine for travel to australia from nz right now? Were the Aussies going to poach all of our young workers when that happened?

The answer to both questions is yes. And did it happen? no

TA was just on the zb property hour and he thinks that the brain drain might take off late next year. Didnt he previously say it would be when the trans-tasman bubble opened last year? Pity that an economist only has one Brain because they like to be in two Minds

Hahaha good one

If you are 21 years old, in nz. But don't have asset rich parents, what you doing after covid?

Stay in nz just be locked down in housing you can't afford?

With tenancy rights that still trail behind much of the more advanced civilised world too.

Yeah sure

He's right.

Just like 21 year olds have always done since travel opened up for OEs in the 70s. The brain drain of the early 2000s was massive and returning expats, and immigration must have had an influence on the mid 2000s property boom. My point is, people forget it’s totally unrealistic to expect to buy a house before the age of 35 and it’s always been that way. People stuck in NZ have rose tinted glasses about the past. Exodus and return is very common.

When this tower of s*** topples over and the govt attempts to bail out property owners at the expense of young, skilled renters. This country’s general demonisation of immigrants is going to come back to bite it.

How has this country demonised immigrants?

That might have started around the time the government banned non residents from buying homes in NZ. This was championed by influential politicians and signaled intentionally or not to the population that it was immigrants/foreigners that are responsible for rising house prices and the resulting crisis of inequality in NZ. Which was of course just an attempt to distract kiwis from the real fundamental issues they have failed or are unwilling to fix and has only resulted in increasing anti immigrant sentiment as seen in these forums. I expect it won't be long until NZ has its own populist strong man taking power by vilifying immigrants and foreigners and blaming all of the problems here on the most weakest members of society. Just as it has happened/is happening in many other countries.

I wouldn't class non residents as immigrants and the odd comment from someone on this forum is hardly representative of "the country". A hard man gaining control of NZ in the future seems highly remote.

Immigrants are non residents until they become residents. And my point isn't necessarily to suggest it wasn't appropriate to ban non residents from buying. But to point out its almost always foreigners that are first targeted as solutions to these kinds of problems. Hindsight has proven that non residents were not the primary driving force behind the housing crisis. But it will take time to wean some kiwis off the notion that foreigners are to blame.

It was much worse in the 90s, there was a lot of racist sentiment in Auckland / NZ towards East Asian people.

And W Peters stirred a lot of that up.

Not demonised - treated like sh**.

https://www.nzherald.co.nz/nz/migrant-family-holiday-turns-into-covid-n…

Quotes from the immigration lawyer Alastair McClymont:

“”A lot of education fairs, like in India, they’ll have reps from the schools, the education agent, Education New Zealand, and they’ll have reps from Immigration New Zealand. They’re all working in conjunction to promote a product that is the export education industry, using the ability to work post-study and obtain a potential pathway to residency.””

and

“”Quite a lot of them borrowed a lot of money or sold their assets, so they feel they’ve been ripped off, conned.””

The Kaur's situation is a bit sh**ty but on the whole NZ is very good toward immigrants. You can always find a case like this if you look hard enough. It doesn't represent the country's systemic attitude toward immigrants.

It depends on what you mean by country - the people are fine once you are here. I know this because I have a visible immigrant family.

All my complaints are against successive governments for not having a transparent immigration policy and the outrageously incompetent, bureaucratic and unkind INZ. Prof Stringer in 2016 discovered "exploitation was rife" - she even said that she expected to find rorts and exploitation but after her investigation she was surprised at how common it was. From the expert immigration lawyer ""a product that is the export education industry, using the ability to work post-study and obtain a potential pathway to residency"". Did Mrs Kaur need a business diploma to become a machinist at a furniture maker? Who benefits from this business diploma - only the NZ education industry. NZ should have an immigration policy that puts the needs of Kiwis and immigrants ahead of specific NZ businesses.

The Kaur family appear to be delightful, NZ would be a better place with an attractive young family like theirs. If INZ employed anyone with a heart then there would be no cases like this.

It is not a question of look hard enough; there is a similar case every other day.

good to see Labour tackling inequality and making housing more affordable -

Another beautiful Saturday and a charting session with my grand kids.

There is still room for upward valuation.

People should be out buying house instead of complaining on the internet- the market won't wait for you.

Be quick!

Have they charted how long they have left until they get their hereditary handout?

Be quick!

Greg Ninnes, Nothing will happen as neither Mr Orr nor Jacinda interested in controlling the ponzi. Hard to believe that they are so deaf and blind that are unable to hear and see what is happening.

When you say 40% - being soft as in many places like Mangere it is more than 100%.

A monster has been created which has to be supported and promoted to avoid disaster as key feature of any ponzi is that to be kept running or it falls as has no place of plateauing or stabilizing.

Height of absurdity and stupidity is : Mr Orr saying that they have no influence over housing ponzi..............Really...he even has the balls to say it is indication of how immune they are to real world to feel that people will actually fall for it.

Jacinda Arden...less said the better and she is the one who was shouting from roof top in 2017 using every platform that how unaffordable house prices are when median was appox $500000 and in Auckland appox $800000....Now where is the photo opps Queen.

Labour and especially Jacinda have achieved top-notch failure status to run and control the govt.

It's not about the current population as we have seen this bad face and to some extent accepted it. Now it's about young ones they will never accept living in a country where for a tin shed they have to mortgage their life.

This is simply pushing kiwis to mass exodus, and Jacinda and Orr is the culprit, if they cannot handle it they should resing. Just for sake of getting big packages, they have pushed young kiwis out of NZ.

The demography of this country will be change very fast in coming years and labour is the root cause of it. Shame

The problem is a lack of a viable alternative party for young Kiwi voters too. National/ACT aren't offering anything, and lack credibility on housing.

Likely they'd need to vote TOP to get any change.

agree with the failures of Labour AJ123, but the incompetence of National led us here. In times when they should have used Cullens legacy to prepare for an equitable future they cemented the rich and powerful control. Then Labour has to keep all the National converts and NZ First happy so tread way too carefully, don't want to upset the old boys network. Can't see National doing anything that would negatively impact house prices. Maybe I'll vote for Swarbrick for PM, at least she's having a go at those with plenty wanting still more. I'll be the only boomer doing so

I’m not so sure that lower interest rates were necessarily the main driver of the 30 - 40% rise in house prices.

Mortgages were also low in the first half of 2020, and back in 2019 with fixed rates of 2.x.

It’s more a mix of human behaviour post lockdown, lack of alternatives, kiwis love of property, and a catch up of stagnant regional prices from 2008 to 2017.

Prices still have another 10% to go over the next 10 months.

...the iron law of investing is that a security (asset) is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment..

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on assets (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that residential property prices are higher also implies that future long-term returns will be lower, but that's part of the deal. https://www.hussmanfunds.com/

Great comment. Just think when money in the bank is making 4% and investors are still doing on property at sub 4% yield. How them apples...?

Well they have a big fat $250k apple from the last year alone that will also be tax free in a few more years.

Only....if they actually sold.

.

dp

Reserve Bank governor Adrian Orr is not doing himself any favours with his revisionist approach to the house price issue. Not so long ago, he was saying increasing asset prices, including house prices, were a feature and not a bug in the bank's policy response to the pandemic because they make consumers feel wealthier and spend more. This week he suggested his bank's policy settings have only a minor impact on house prices.

He actually has quite a bit to answer for. The bank has been consistently under-forecasting increases in inflation and house prices, and overforecasting unemployment. While no one is expecting perfection in these times, the ongoing nature of the forecasting issues is concerning. Link

Exactly: Around 61% of NZ bank lending is dedicated to residential property purchases for one third of already wealthy households because the RBNZ offers them a RWA capital reduction incentive, to do so.

{kind=link}

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of June 1998 to $319,231 million (61.39% of total lending) as of September 2021 - source

The Chinese Communist Party has done it so well.

In a play on Karl Marx's (an economist among many other things) supposed quote"

"We shall enable Capitalists to create the debt to bankrupt themselves with"

Blame Supply, Demand......except the perpetrator .....Uncle Orr who has been supported by Queen Jacinda.

Question to be asked after such massive....are they even thinking of controlling......

After the GFC Iceland went after the Bankers that caused it.

After this bubble collapses, the governments that truely represent the People should go after the Central Bankers.

Public execution in front of the beehive.

But isn't it the Mayors and Councillors of every major city who need to be shot? To me the ONLY housing related, supply and demand factor that has meaningfully changed since '61 - when I popped out - is that Councils will nowadays never release any farm land for housing...And as a result land is now 65% of purchase price not 20% (as it was in 1961 Matamata.)

I humbly would suggest releasing all the land that should have been released since 1980, ie doubling each city in size. That would reduce house prices back to 3 times family income ie $270k. Otherwise we will all end up in Cindy and Judy's Soviet style boxes - which will still cost $600k...

The govt wants UP (new urban rules circumventing res consent) as well as OUT (fast tracking of drury). Councils are usually lacking the capital for new infrastructure that is required for new housing. There should be a special rates levy instead of DC's or an option whereby the developer funds the infrastructure

Mate, I can't stand Cindy and her comrades any more than the next person but I think maybe the language suggesting certain people should be shot is a bit aggressive.

Take a look at Auckland days to sell last month. It was 45. That compares to 32 for prev month. Also look at what comes to market. On RE NZ this week Orewa had 99 listings. Only 25 of them were built with rest rep by graphic image of what it would look like eventually. Sales in Silverdale were 64% below Oct 19 and 46% below Oct 20.

Yes prices keep rising but if you cannot afford them then there is no “market” for you. Disposable income is taking a hit and will decline more next year as slowing world GDP impacts NZ growth.

All of the existing stock is waiting out its 10 year tax free status. If the worm really starts to turn there will be a rush of epic proportions to the exit. Prop can be a very illiquid asset in a falling market. Rents cant go up by a factor of 10 times. Imagine a market were existing rentals need 60-70% equity from DTI regulation.

I have plenty of years of experience in social housing and one thing I know to be consistently true is that the floor price for the bottom decile of housing is determined by the maximum rent that beneficiaries and people on the edge of the job market can afford to pay (with Govt support). This is what sets the price of a house in less desirable suburbs up and down the country.

I am increasingly of the view that the ceiling price (top decile or so of housing) is set by how much wealthy people can afford to borrow to live in the most desirable suburbs with good schools, leafy parks, quality shops and amenities, easy access to CBDs, and, of course, no poor people. Over the last few years, low interest rates have accelerated house price growth because people have been able to borrow more, but the data shows that prices would have gone up regardless. This is unsurprising given that the upper middle classes have done really well out of Covid (wages protected, costs reduced) and Govt has committed to sustainable increases in house prices, giving people the confidence to reach for the stars. Add in eager banks, aggressive estate agents, and fear of missing out to this mix, and, well, boom!

Obviously all other house prices arange themselves between the floor and ceiling prices.

Tackling the housing price boom needs to recognise the different dynamics across the price spectrum. For example, prices at the lower end could be tackled by building tens of thousands of social houses for affordable rent in the medium-term with landlord licensing and rent freezes introduced whilst we wait for supply to come on stream. However, this will make zero difference to prices in the nicer suburbs, which would be better tackled by increasing the cost of borrowing or taxing more of the disposable income of wealthier people to reduce what they can afford to spend.

It has been a long while since I've posted here. I got tired of saying "it's a bubble", back a few years. It was a bubble then, now it's incredible. These are Nasdaq-type gains in a good year, not real estate. It seems likely this will not end well. It's a shame, it could have been avoided.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.