Prices at the bottom end of Auckland’s housing market increased by a shocking $85,000 in October, making it increasingly unrealistic for couples on average wages to expect to be able afford a home of their own in the region.

The Real Estate Institute of New Zealand’s lower quartile selling price in Auckland jumped from $850,000 in September to $935,000 in October.

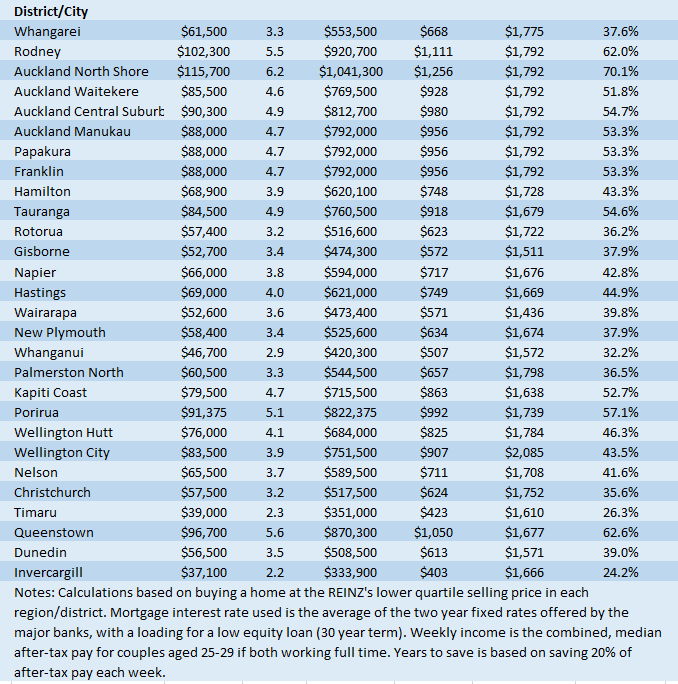

Within the Auckland region lower quartile prices now range from $855,000 in Waitakere to $1,157,000 on the North Shore.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing the bottom quarter of the market that is most affordable.

According to interest.co.nz’s Home Loan Affordability calculations, those prices just about rule out the possibility of home ownership for young people on average wages.

The median, combined after-tax wage for couples aged 25-29 in Auckland is $1792 a week, if both work full time.

That’s before allowing for any deductions such as contributions to KiwiSaver or student loan payments.

Unfortunately that’s probably not enough to allow them to be able to afford a home of their own in the region.

Their first hurdle will be getting a deposit together.

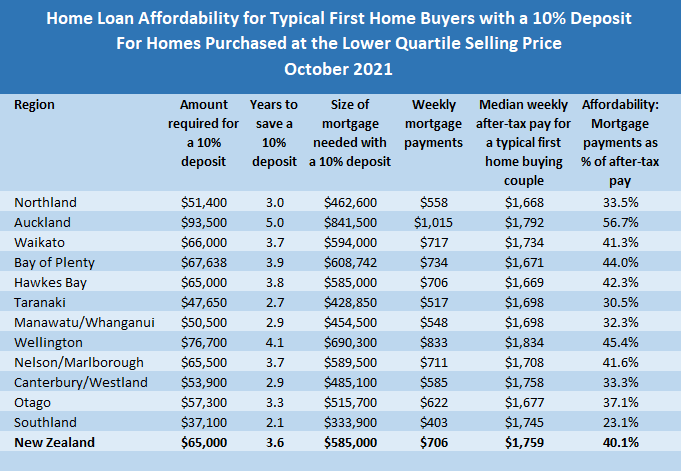

The amount needed for a 10% deposit on a lower quartile-priced home would range from $85,500 in Waitakere to $115,700 on the North Shore. If couples on median wages were able to save 20% of their after-tax pay each week it would take them between 4.6 years and 6.2 years to scrape up a 10% deposit.

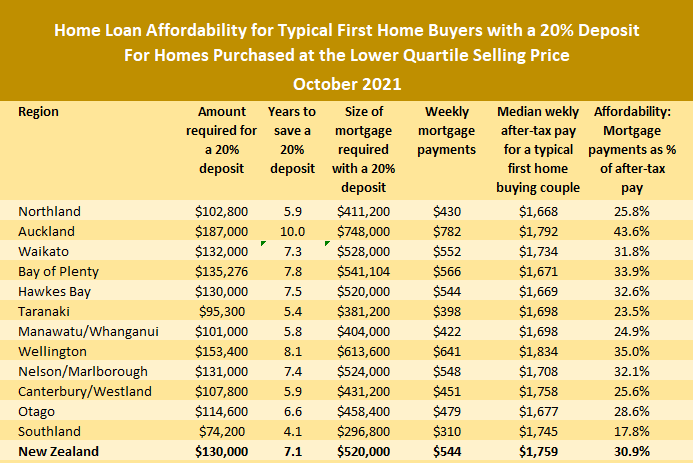

Those saving times would double for a 20% deposit.

Even if they could come up with a deposit, being able to afford a home would still be uncertain.

If they had a 10% deposit they would need a low equity mortgage, which is probably going to be around $700,000 on which they would be paying a premium interest rate.

Interest.co.nz estimates that the payments on a 90% mortgage for a home purchased at the lower quartile selling price would range from $928 a week in Waitakere to $1256 a week on the North Shore.

That’s equivalent to between 51.8% and 70.1% of the take home pay of couples on the median wage for 25-29 year-olds. And that’s before allowing for other property-related expenses such as rates, insurance and maintenance.

That is likely to restrict the availability of low equity mortgages to people earning higher than average wages, and perhaps substantially higher than average wages.

And even those who could pull together a 20% deposit may struggle with their mortgage payments in Auckland.

A traditional measure of affordability is that mortgage payments should take up no more than 40% of after-tax pay.

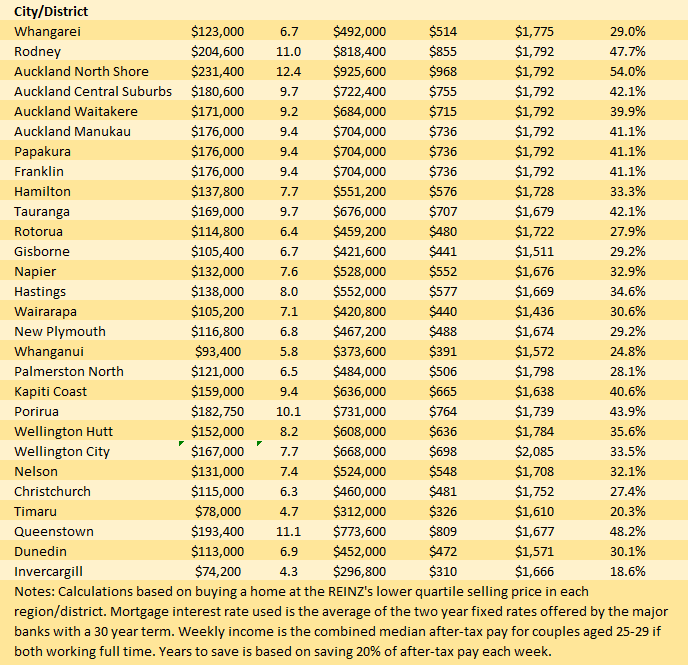

In October, Waitakere was the only district in Auckland where the mortgage payments on a lower quartile-priced home would be less than 40% of after-tax pay for couples earning median wages, even if they had a 20% deposit.

And Waitakere was only just inside the 40% affordability threshold by the skin of its teeth at 39.9%.

So even couples who have a 20% deposit are likely to struggle meeting their mortgage payments unless they are on higher than average wages.

Those sorts of problems are no longer restricted just to Auckland.

The REINZ’s national lower quartile price increased by $47,500 in October to $650,000.

That means couples on median wages with just a 10% deposit would likely struggle to meet the mortgage payments on homes purchased at the lower quartile price in Waikato, Bay of Plenty, Hawke’s Bay, Wellington and Nelson/Marlborough.

Housing unaffordability is no longer mainly just an Auckland problem. Like Covid, it is now spreading through the rest of the country as well.

The tables below give the main affordability measures for all of the major urban districts throughout New Zealand.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

101 Comments

These figures are absolutely mind-blowing, especially when put into perspective by an article like this (thanks Greg).

A good illustration of how a broken housing market impacts more than just houses. Raising a family in this country is becoming a very unattractive proposition for younger generations.

Are house prices rising or are real wages collapsing? That is the question

why_not_both.gif

House prices have risen (rapidly) on the back of crazy irresponsibly low OCR settings. Simple as that. OCR needs to be on a rapid path to normalisation.

Normalized rate of 10 percnt plus would you say ?

I’d set the OCR right now at a low normal of about 4 or 5%.

Luckily you aren't the RBNZ governor.

Doing that might drop house prices back 30%, but would also destroy the economy.

bugger...

Devil could care less attitude to what that drop would do to the majority of householders. Especially recent buyers

I'd say most householders could cope with a 50% drop in prices and still be ahead. Most households didn't purchase within the last 2 years

No pain, no gain.

You can't cook an omelette without breaking some eggs.

There's no such thing as a free lunch.

At some time we are going to have to pay the piper. The longer we wait the worse it will be.

Good things come to those who wait / he who hesitates is lost

to save the village we have to burn it.

Riddles always talk in you do?

More can you fit into one sentence yoda?

30% is writing off about 18 months. 18 month reversals should be part of the natural ebb and flow. If natural ebbs and flows destroy an economy it needs to be rebuilt anyway.

House prices rose 30% in Just one year; for them to return to a price of a year ago will not destroy the economy. it may just put some, arguably well deserved pressure on those idiots who got jumped in the market boots and all during our worst economic recession on record.

You don't understand our distorted and fragile 'economy' if you don't think a 30% fall would create carnage.

Anyone buying to hold for less than 20 years and not factoring in interest rate shocks deserves everything thats coming to them

I think the other thing is the absolute Frenzy by Developers, not just big developers but small time developer/investors trying to get the tax advantage from New Builds.

I dredged this Article from 2015 comparing NZ to the property Frenzy in Ireland.

https://www.nzherald.co.nz/business/housing-warning-its-an-ireland-repe…

While the predictions were very wrong, this risks have increased significantly from 2015. Housing affordability is quite frankly a social disaster in New Zealand.

Are house prices rising or are real wages collapsing?

The purchasing power of any cash savings and incomes has collapsed. That's what happens when the banks can create credit at a rate far greater than the rate of income growth.

Most peoples wages still buy all of the things they used to except for housing.

Do they?

Houses on mortgage

Consumer goods on After Pay, HP, Finance

Utilities on Credit cards.

The whole shebang is based on money people don't have now but hope to have in the future. Which we know isn't working, because now we have the rise of micro/payday loans to cover those gaps as well.

What "debt" based product will be next?

A million dollar mortgage!

Just pause and think about that for a minute.

Every second TV program is about house buying or house flipping in various countries. Its completely and utterly mainstream.

Made worse by the govts views that beneficiaries should live in a house which is as big and newer than what a first home buyer would be in.

Assuming the mortgage gets paid off that's a big chunk of a persons lifetime earnings. If you assume a person has 40 years of decent income that would $25k per year in after tax money to pay off the mortgage without allowing for interest.

Absolutely correct and at today’s interest rates you will pay another $1 million in interest - so that’s 50k a year for 20 years to buy a 3 and 1 house

Anecdotally there does seem to be an expectation that each and every beneficiary has their own home. Going off the number of "Will WINZ pay $xxx rent per week" on Winz Facebook pages. Any suggestion that people look at rooms to let is shot down.

Because that is what a prison is a place you cannot choose who to live with, are at risk of sexual and physical assaults daily and have limited access to an accessible bathroom so poor to no toileting facilities. Many disabled people died under the age of 40 because of what you suggest, some were just so traumatized and physically abused they were driven insane or denied any access to communicate. What a strange fantasy you have to relive those days.

Also in case you did not realise most of those disabled on a benefit lose any income support if they are forced to live with someone else. It often does not even need to be a relationship as close as a friend. Many disabled people have had their income cut for having flatmates or borders. If you think that the ability to afford or to be able to pay for or the ability to have visiting carer support for a disabled person does not factor into room rental decisions then that would be a moronic position. It is akin to saying that disabled people should be happy to have food prep and bathing access removed and be glad they are not put into pine boxes instead.

Because where you cannot choose who you live with but are extremely vulnerable is what a prison is a place you cannot choose who to live with, are at risk of sexual and physical assaults daily and have limited access to an accessible bathroom so poor to no toileting facilities. Many disabled people died under the age of 40 because of what you suggest, some were just so traumatized and physically abused they were driven insane or denied any access to communicate. What a strange fantasy you have to relive those days. In case you were not aware less than 2% of housing is accessible to people with disabilities, many do die from lack of access to safe or any bathroom facilities (often of sepsis) and funnily enough we often ignore and do not collect stats on the deaths of disabled people because it is deemed "natural" as if sepsis or injury from lack of suitable housing could ever be natural.

It also takes a moron not to know that it costs far far less to build an accessible home from scratch than to try to retrofit an old one (you basically have to almost shell it out, add extra reinforced structural elements for the hand and hoist areas and then need to add in floor supports for equipment weight and specialised flooring, knock down most walls in the process and remove most hallway designs, don't get me started on the additional needs if that disabled person on a benefit is a pensioner with brittle bones and an aging mind).

vote labour..the party for the average person, we will close the wealth divide ...not

Vote National.. the party for the rich people, we will make the wealth divide worse...

Maybe its an inverse pattern, or maybe we are just f***ed.

18 years of Clark & Key governments & 4 of this lot equals 22 years of sustained escalation in property value. Coming up to a quarter of a century. So it can only be concluded that all these governments have wilfully, deliberately indulged themselves in policies to create said escalation. Perhaps the end game then is the wealth tax sponsored by the Greens? Sure has formulated a huge collective target as catchment hasn’t it.

Won't work - on raw numbers it is the banks who own most of the properties. They've just put in place rent to own mortgages. Start taxing the capital value of properties and many, especially young will be forced to just walk away from them, just like what happens in the US.

There is no way to fix this now that i can see without causing pain. A lot of it. But for that pain to have the least long term effect I suggest it should be aimed at the wealthy and banks. And by wealthy I don't mean owner occupiers who are in their own homes, but the investors, speculators and landlords.

Simple to do in theory.. remove interest only loans and require all landlords to recapitalise and go onto business commercial rates....15 yr loans etc

seems hard to do in practice

They are each as bad as the other, in different ways.

It needs compulsive reasoning for the young couple to stay in this country, why does someone pay this crazy price in this highly inflated housing market with high interest.

Better to buy a one-way ticket to Aus and live their life with high income and less liability. Even the young couple with high income should not put their money to buy shoe boxes & work for many years to come to pay them off.

There is nothing special NZ can give that prompt you to pay an unreasonable amount of money, whether you compare living standard or amenities with our neighbor. We are well on our path to becoming a third-world country there also people cannot afford basic amenities because of the shortage of resources here also people cannot afford basic amenities because of spineless Govt.

I believe labor has fulfilled their promise of affordable housing but they haven't mentioned it will be only affordable for the rich.

Yep young ones should get out ASAP.

Even in Sydney, you may not be able to buy but you will have much more ability to save or invest in other things.

Yeah I rented in Bondi for 7 years and was able to save a whole lot more and had a great time as well.

Yet looking at suburb profiles on domain.com.au shows median houses prices of $2M - $3M or more within 20km of Sydney CBD

Yes - so my point being you may not be able to buy but you will have more money in your pocket to save, invest or spend.

They just need to make a choice - cake or death!

$85000 in one month that is 10% in one month, why is Greg Ninness shocked.

Hate when Government, RBNZ, Experts, Economist use the word Surprise, Shocked, Unecpected....as they all BS as everyone knows what is happening and data too on daily basis supports so please stop being shocked and hold RBNZ and government accountable by asking hard question.

You millenials should have got in before it was too late like your boomer parents did.

The boomers were at the start of the ponzi..if you were not born then a bit hard to get in?

I know someone that sold his house in 2015 as needed the money to support cashflow for his business that provides an actual service. What an idiot.

Thank you for your polite answer, after what I wrote you should have hit me with a hard stick instead ;)

Cynicism missed you did.

Frazz

I'm a white, pale, stale, old babyboomer but stop trying to put the blame on us for everything the disaffected find distasteful. If you wish to assign the blame correctly you should direct it at the Key government where all sorts of immigration schemes and scams flourished and were actively encouraged....many so-called immigration consultants were ex-MPs or had ties to MPS. The one scheme which I had privy to when I was selling my own business was that a Chinese immigrant would borrow enough money off these consultants and their Chinese liaison partners to buy any old business so they could become NZ immigrants under the 'business category'; they would have to then pay the loan back with interest. Inotherwords, they weren't bringing new money into NZ, but sooner rather than later they would be buying a house.

But I'm also aware that a lot lot of younger babyboomers than myself have been attempting to undermind Ardern's handling of the pandemic. For god's sake the Australian right wing think tank,The Lowy Institute, has released a report into the pandemic which lists NZ as number one in the world for the best handling of the pandemic. A lot of shameful criticism has been directed at Ardern purely because she's a woman and these white, pale, stale commentators (Prebble, Joyce, Taylor, et al) find it difficult to countenance being governed by a woman. We witnessed National's debacles where a man (Bridges, Muller,etc) flopped spectacularly. We have witnessed what the opposition tright wing parties have to offer and it's nothing; There's even a new right-wing party on the block in the form of a Social Credit avatar that recently placed a full-page advertisement in the Herald; things are so desperate the right has had to scrape the bottom of the barrel and reintroduce 'the walking dead'.

Finally, Austria, facing yet another surge of Covid has said bugger it to all the anti-vaxxers and introduced compulsory vaccination. Good on them.

Abysmal.

Well done to both Labour and National - *slow hand claps*

Foxy attributes the Clark and Key Governments too, but I wonder if the rot started before that. Remember Chris Trotter pointing out Mike Moore advising Lange, Prebble and Douglas on who the then Labour Government could not afford to piss off? Big business and money. It just took a while to become evident, but would have opened the door to lobbying. Could even speculate if Moore was bought by them?

Well Muldoon sure had his cronies. Cushing, Trotter, Fletcher, Davis, Myers, and even Jones sort of for a while, and on. Don’t believe before that Kirk was subjected to any such influencers but possibly Holyoake had a receptive ear tuned to the right frequency? But I would suggest Muldoon’s prime ministership was the incubator for the “lobbying” of today.

How any non homeowner can have Nat or Lab on their potential vote for list still astounds me.

Just plain dense.

Get off your butts kids, get political and get cracking. Use all your social media skills, do what it takes, but you have to disrupt Nat and Lab.

Don't disagree Rastus, but why would ACT NZF or TOP be any different? A big part of the problem is the quality of choice.

We need something very different today. People not bound by "conventional wisdom". People willing to challenge that wisdom, and try something very different, but they would have to have very high levels of integrity too, as the temptation would be huge!

Perhaps not, only one way to find out. Nothing to loose.

The main parties are not delivering, they are beholden to the banks - that's as clear as day.

Are any of these FHB's going to be able to afford to raise families and/or any real lifestyle?

Sure.... with support of the state.

So let's face the stark facts - in Auckland FHBs need a HIGH household income to POTENTIALLY afford a starter home, probably a flat or townhouse in a low value location.

It is looking that way. I doubt any of those options would be somebody's dream home

No no the problem is that young people all demand a big house by the sea in the CBD, didn’t you hear

While eating avocado, no less!

Strangely enough those 1 bedroom apartments leasehold or any freehold in the city (awaiting remediation) is selling for substantially less than CV... Could be the hundreds of thousands of hidden costs. However the govt is trying to push young couples into thinking that apartment living in high risk low quality buildings at risk of severe remediation issues and high annual rents is exactly what they need.

The stark facts are it’s also the worst place in the world to invest in productive enterprises because your workforce can’t afford houses.... more factory closures?

Surely there must be some major noise in this data? How does the lower quartile increase by $85k in a MONTH?! Would be interested to know what the previous months showed.

We have a $1m mortgage and so do a lot of my friends (30s). We all got sucked in in the last year or two. We can manage for now but didn’t expect interest rates to increase this quickly. We’re all struggling to figure out how we can afford having time off to have kids - times running out. Or have any money left over for entertainment etc.

Many friends still in flats paying a huge amount of rent and not able to save enough for a deposit. We’re all in our 30’s, I swear it was easier for previous generations at our age

Yes it was easier back then, if you had a job. Unemployment was high for many years which kept some from ever owning their own place. I think if we got similar levels of job losses and unemployment now, you would see house prices fall quite a bit.

Unemployment was also high because it only took one wage to afford a home. Hence, more often than not, one half of a couple did not need to support the mortgage payments.

agree, we got our first house age 27, but then you could buy a house with a mortgage 3-4 times your income. Nearing 50 now and will have it nearly paid off. In that time managed to have 3 kids and drop to the one wage. But borrowing 7,8 or 9 times your combined income, I feel for you as the likely hood you ever pay that off and have a family is zero, without a hefty inheritance I suspect.

Common situation among my friends too. Many like the lavish lifestyle and now are balls deep in debt lol. I'd say most are pretty tapped out now too. What is next? Years and years of grind to pay off that home loan is what is next. I'll be advising my kid to gtfo of NZ.

And the shit thing is that house prices have been going up for so long you really can't blame young people for eventually getting in over their heads. I'm sure the same boomers that said "stop eating avos and commit every cent you have to a house" are now going to turn around and say "why did you buy a house with no spare income to cover interest rate rises"

Exactly. According to the chat above, saving for a 10% deposit takes at least 2-3 years in the cheaper parts of the country. I don't think there is any time in the last two decades when you would have been better off waiting the extra 2+ years til you had a 20% deposit. In some cases you would have been hundreds of thousands of dollars (or even half a million) better off had you bought as soon as you possibly could rather than wait til you had a bigger deposit. And in those decades there have been many, many instances where 'experts' have predicted house price drops that not only didn't eventuate but were instead double digit rises. So for their entire adult lives, the smart thing to do has been to ignore predicted house price drops and buy the most expensive house you can as soon as you can.

Once you have kids you don't need entertainment money, so don't worry about that... Haha

I obviously don't know what your household income is like, but if it's possible - saving up a chunk of money (kind of like you're saving for a house deposit again) before starting a family and using that to help with mortgage payments during maternity leave? Maternity leave doesn't have to be one year either, I went back at 8 months because of finances.

Sorry, it sux. We actually made the choice to have kids before the house because of our age. When we did that I thought we said good goodbye to ever owning a place but it all worked out. We saved really hard but we also lucked out with the timing of our purchase.

The "well if you ate less avocado" brigade are quiet these days.

The irony is avos are bloody cheap this season. The avo farmers were crying they won't be making any money this year hahaha cry me a river.

Half an avo on two slices of dollar wholemeal loaf = breakfast's on the house?

I'm thinking all the cost comes from the smashing of the avocado and toasting of the toast.

Demand must have dried up from millennials saving that extra 85k a month they need just to stay where they were. Who knew it was possible to eat that much avo.

It is not humanly possible in a human lifetime, not without developing allergies and toxicity from the stuff.

He has some good economic skills, but I will never forgive Tony Alexander for his obscene comments about FHBs eating too much avocado on toast.

I was extremely close to dumping BNZ as a bank because of that.

Total knob.

Remember folks this is a first class problem to have, we are actually very lucky. The RBNZ can deflate this with ease.

What a fck up. I’ll be telling my kids to seriously consider leaving when they are of age. I manage a group of 11 guys at work. All earning around the medium income. Only one owns his house. They are all doing it tough with increasing living costs too. Sad times

This year my son is in his first job after uni. Once he gets a good 2-3 years under his belt, he'll be off to Aus. He's an engineer.

Definitely good idea. Actually NZ engineering in general is low wage and low quality lifestyle across the engineering specializations but especially mechanical, electrical, software, environmental, biomedical etc especially in comparison to countries like Aus, the UK, the US, many countries in Asia. A trip across the ditch can actually double the wage and provide high quality affordable housing within the first 2-3years (better education and support benefits too if they can become citizens). In addition the career opportunities are far better and the additional on the job training is much better (plus access to higher quality conferences and research opportunities). However the key is ensuring that family can follow them because like covid has shown returning or getting the childcare benefits of relatives so both parents can work full time is far more limited when the borders are closed. I guess they could sacrifice more for young infant and toddler childcare (also more affordable overseas) or they could just have older family with them for a couple years also to benefit from the improved living conditions and often better quality housing.

Other fields that should leave NZ immediately anything in the medical or other tech sectors, teaching and education, trades, agriculture, sports etc. Mostly just leaving NZ with property investors, financiers, bureaucrats, the serfs who serve them and those too stuck in this country already they cannot leave (like those who would struggle to get visas, those with family to care for, or those who could not get decent jobs overseas).

Great news. There will be plenty more recovering kiwis to hang out with overseas. All the good ones are abroad.

[ Keep the conversation based on the issues. Aggressive personal insults and abuse are a basis for being blocked. Last warning. Ed ]

This is a mystery. Please explain.

Crazy prices, maybe some should move to Timaru, a very nice place and very affordable to own a house

Moving to cheaper regional cities will work for some, but in many fields there are very limited job options in those places.

Given the socialite that you are, hanging out with the wealthy and influential, don't you miss Auckland Yves?

I do live in Auckland HM and yes I love it

I seriously contemplated moving there once. I saw a job advertised in my field and looked up houses on realestate.co.nz and did all mortgage repayment sums which were very favourable. But I just couldn't do it.

All part of the plan - make the people serfs to the banks and 1%ers.

Pitch fork time.

Keep raising interest rates, it will only help make it harder for FHB's to buy any home. Great job team!

Damned if you do, damned if you don't

At least there was a record number of FHB's who were able to enter the market at the low interest rate points. It gave them a chance to get in. Now? with all these DTI tools, sudden interest rate hikes, how is a FHB ever going to buy?

Oh there will always be advantages to using investment equity and rental income of a portfolio above anyone buying with intentions to actually live in a home. It is not like they are blocking the use of equity and interest only loans in housing purchases.

It seems clear to me that less people will be able to buy a house of their own.

That means more people will need to rent.

So why on earth is the Government doing its best to make it harder and more expensive to be a tenant off a private owner. Private owners currently supply 80% of all rentals and the percentage is going up.

The government has exempted itself from needing to supply homes that are warm, dry, correctly sized, and in some cases in emergencies from even having their own bathrooms and kitchens. Things are looking bleak for young people leaving school. Beware young people make sure you choose good parents and do what they tell you to do. You only get one chance to choose good parents.

You can buy a 40sqm freehold 2-bed apartment right now in central Akl for under 400K. At 10% deposit that's 40K. Not unrealistic for a working couple. A lot of property is very expensive but not all of it, if you're prepared to compromise on size

Mmmm..... a couple in a six by six something meter square room....

Good training for the space station I guess?

I think hundreds of thousands in remediation issues and tens of thousands in body corp fees have something to do with the apartment lifestyle not winning for most owner occupiers. Toss in trying to raise a child in a room not much bigger than the bed and you have immediate problems right there. Add to that disorderly neighbours and we have the slums of the past to torment the future.

A young couple used to be able to afford a 100sqm house on a 1000sqm section on one income.

Now they get a 40sqm apartment on 2 incomes. Fantastic.

What has gone up has to come down only way now 10 year to save deposit by time they get there they will need another 10 years if houses double in price every 10 like people no here say, can’t people see it’s over for housing market . Lot of people who purchased house last 3-4 year will lose deposit and be in negative equity.

Er no, if anything history has shown what has gone up in the past 10 years will never ever drop to rates of affordability of the previous generation. We have had several generations of local data and ever rising immigration rates supporting rental investment and growing company home purchase rates.

This is why we need a massive state house building programme, along with promoting the need for secure housing, not everyone owning houses.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.