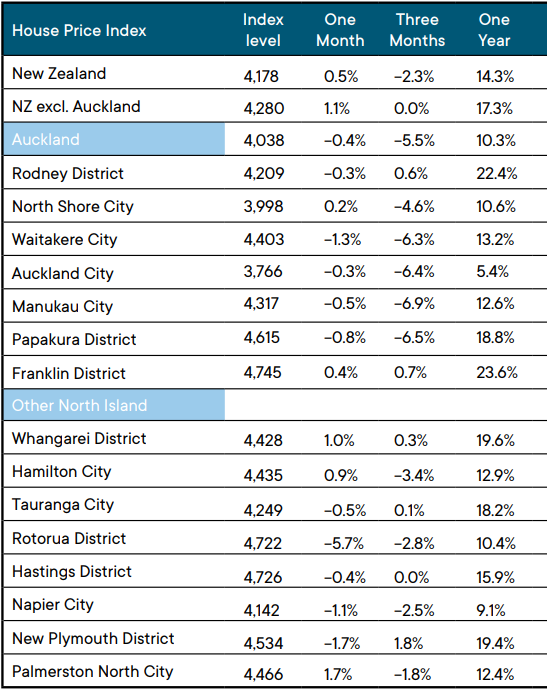

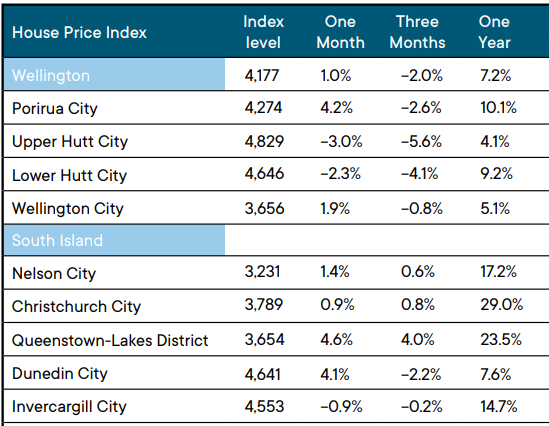

Although there was a small rise in house prices last month the longer term trend is still down, according to the Real Estate Institute of New Zealand's House Price Index (HPI).

The Index shows prices rose 0.5% in February from January, but were still down 2.3% compared to three months earlier.

The HPI, which was developed in conjunction with the Reserve Bank, adjusts for differences in the mix of properties sold each month, so is a more reliable indicator of housing price movements than other measures such as average or median prices.

Of the 28 districts measured by the HPI, 14 showed a price improvement in February compared to January and 14 showed price declines.

The biggest price increase was in Queenstown-Lakes where the HPI was up 4.6% for the month, while the biggest decrease was in Rotorua with a drop of 5.7%.

Compared to three months earlier the HPI declined in 18 districts, rose in eight and was unchanged in two.

Queenstown-Lakes also showed the biggest increase in the HPI over three months at 4.0%, while the biggest decline was 6.5% for properties in Manukau in south Auckland.

The table below shows the changes in the HPI over one month, three months and one year.

The comment stream on this story is now closed.

REINZ House Price Index - February 2022

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

106 Comments

The trend is your friend until the end when it bends... Gravity will kick in at some stage. The trend of the US year bond rates is definitely up (cost of borrowing money) and has properly broken out of its 30+ year downward trend. (see also https://www.interest.co.nz/personal-finance/114834/bond-and-swap-rates-rise-inexorably-only-kiwibank-has-moved-match-anz)

As newshub is warning today: "taming inflation is not growth or asset price friendly....,..., 2022 is going to be pretty tough and there is going to be a little bit of paying the piper"

Gradually, then suddenly.

What suddenly up again ? I think there needs to be some clarity in the reporting here. People are talking about "Falls" but in relation to price increases. So people see a "Fall" in the growth rate of say 10% to 8% and they call it a fall but its not in the true sense of the word. A fall is when the prices actually begin to drop and you still need to keep it in context over the course of months or even for the year. The longer term trajectory remains unchanged to date. The alternating cheers and jeers from one day to the next from either of the team supporters can get a bit tiring.

It's just a Hemingway quote, relax TTP.

Putting a quote as a metaphor with an intent meaning expecting a reaction, then telling people to calm down that it was just a quote, smooth.

-7

I'm jesting with the Carlos67/TTP scandal below.

And sure, my belief is it'll be a slow change, then will suddenly happened. However, I don't particularly care what happens to the NZ housing market to engage in a debate.

This has been up for 10 minutes and none of the heavy weight doom merchants have commented yet?

It's been up for 10 minutes and we already have Luke83 with his childish jibes at people with opposing views on the direction of the housing market.

You do realize people are entitled to a differing view, and you don't have to take it personally?

When the market value of your property portfolio decides not only your entire net worth but also your self-worth, you get personal.

NZ preaches the world on respecting human rights, but back home controlling the supply of food and shelter have become get-rich-quick investments.

We reward housing speculation with tax breaks and just look the other way when oligopolies fleece Kiwis at checkout.

He definitely has skin in the game, which as you say is why he's taking it so personally. It's like an attack on his livelihood and ability to assess risk.

His response to a comment last year suggesting the price of new builds could potentially skyrocket 20% due to supply chain disruptions.

by Luke83 | 5th Jun 21, 4:46pm

Hope so, means what I've nearly finished will make me even more, gravey train baby

100% true. My comments are targeted at the merchants who love to get excited about falls, Im happy either way, goes up and down over the years, always has always will And yea that 20% was actually 25,% funny to see that comment came true. God I hope you don't think i actually care what a bunch of people on a chat like this actually say. You have a good one.

Excited by falls, is different from criticising Rampent asset inflation due to loose monetary policy.

We all know you care what people say, we're not under any illusion, otherwise you wouldn't be on here calling them out and trying to convince us otherwise.

Auckland down 5.5% in 3 months. Nothing else to say really. That will be 20+% yoy if it continues it’s titanic like trajectory. I think Winter will bring on slightly bigger declines as interest rates climb. Luke, you seem to struggle with the fundamentals… when Mr Bank says interest rate go up, Mr Joe Bloggs goes poo poo pants because Mr Bank will lend less money. When Mr Joe Bloggs has less money to shop with Mr House owner has to drop price to suit Mr Bloggs new budget or house no sell . Mr Luke thinks house price only go up. Mr Bank and Mr Bloggs laugh at Mr Luke because he lives in la la land

Stock levels still climbing, at least in Auckland. 2019 was similar (kept climbing until end of March), but 18,20,21 all had peaked by mid-March. Will be interesting to see how it goes in the next few weeks.

The housing market is tanking way over valued.Rates are on way up from emergency levels this will create a huge spiral down anyone who has been fooled by FOMO and bad advice from dodge people will find out the hard way as they say goodbye to deposit and are in negative equity. When average wage earners cannot afford a house the games up .

We are already there with unaffordablity for the averageman. Sweeping inflation means the only fat to cut is from the ponzi of debt.

Maybe because your so-called "doom merchants" have already foreseen this coming and no need to make a big deal about it? As I remembered, no one called there would be a crash during Feb, am I right? The data itself is enough to show where housing market is heading. Inflation continues to go up, interest rates, swap rates, OCR continue to go up, more stock in market but less sales...

You must be very busy TTP switching from one account to the other.

Index down by 0.5%....eh why does it still cost so much.

Bugger have we landed yet ? I didn't feel a thing.

TTP

Maybe you should ask one of your sales staff who hasn’t been paid for the last 4 months how their landing is looking

Forgot to switch accounts TTP?

Priceless… I didn’t notice

Well, that explains everything!

Seriously Tim (TTP/Carlos), you are the chairman of a nationwide RE agency.

Your staff remuneration and morale is at a new low, with a grim looking foreseeable future.

Is the best use of your time really spruiking on here?

Get off and do some governing!

Strong similarities to Matt Hill from new talisman mines here - he was fired and is currently under investigation for posting anonymously on sharetrader.co.nz supporting his business.

Absolutely pathetic to do so with multiple accounts with different back stories.

Then also P8 has been on here encouraging young people to buy into the market....and appears he was doing that so that his children could offload a bunch (4 I think) rental properties at what he thinks was the peak of the market. i.e. trying to get maximum price for his kids...while pretending to have the interests of FHB's at heart.

All very dodgy. Like insider trading, but just in a more creepy type of manner.

Just on this topic - if we really do have people actively associated with real estate here in a professional sense and they have been talking up the market for their own benefit (business income/capital gains) - surely they have to be very careful with respect to the law around Misleading and Deceptive Conduct as well as making False or Misleading Representations..as detailed in s9-16 of the Fair Trading Act. This could be considered illegal.

If a bunch of young people or property investors lose their shirts because they followed somebody's overly bullish representation on here of where the market is going, I don't see how their case differs from Matt Hills. "FMA accuses CEO of market manipulation for anonymous posts on investor forum".

For the other real estate non-professionals out there (like me) who aren't involved in property in a professional sense...all comments are my own and with nobody's particular benefit in mind - I prefer to view these issues through the utilitarian lens of best good for the most people, now and into the future. If I were actively involved in the real estate industry I wouldn't be commenting on those articles. It would be like me talking up the company share price on here - which obviously would be far from professional and illegal.

If TTP is Tim and he is the head of the Property Brokers - and a number of young couples have purchased because he's made a represenation on here that they can't lose...property is a one way bet.......well both buyer and anonymous poster beware I say.

A bit of a false equivalence I think? Having opinions on the general property market are not quite the same as misleading investors of a specific company. While TTP could be leading young couples down the garden path by suggesting property is a one way bet, he's not providing 1 on 1 advise and ultimately the onus is on the individual agent conducting the actual transaction to do so ethically.

If Tim came on here under many anonymous monikers and made specific claims about Property Broker's ability to boost capital gains by 50% based on some fictitious "helped my friends out" stories or that all FHB that purchase from Property Brokers have seen a minimum of 20% capital gains in x months, then that would be misleading and deceptive conduct.

The difference is is that there is only one company or investment product...its called the NZ property market. Professionals within that industry telling potential buyers in an anonymous forum that the only way is up and the market never falls, because that is the position that is in their best professional interest, is to me very misleading and deceptive.

Having each person declaring their bias at the end of each statement would make peoples positions clear and remove any intentional (or unintentional) ability to mislead or deceive.

e.g. my username is TTP and the housing market never falls...but I only say that because in real life I work for the management of Property Brokers and I make more money if house prices keep going up and don't really care about your personal circumstances if prices actually fall.

Wrong and misleading. Agents make money in a moving market regardless of direction. Beware those with bias particularly those who try to claim none

https://www.govt.nz/browse/law-crime-and-justice/crimes-and-emergencies…

I think Carlosgate definitely counts as a scam

Bugger have we landed yet ? I didn't feel a thing.

TTP

Multiple account snafu. Busted. Best start a new one as both of these are now tainted as RE Agency pump and dump.

Another one of your fake accounts I see TTP.

Some people (like 2022, above) hang onto my every word......

And become delirious when I don't speak up. 🤪

See the comments of the various nutters below, as well.

TTP

I'm afraid the value of your words has undergone rapid deflation - turns out the supply was at least double what we thought it was.

Didn't think a copy cat type of post would get such attention, They clearly all really love you here.

Yes I agree. You are very wise.

TTP

I would be very carful Tim Mordaunt TTP. I would imagine this is going to be you next.

https://www.fma.govt.nz/news-and-resources/media-releases/fma-accuses-c…

2022 surely everyone knows that you are Retired Poppy too though right?

Been following comments for a while now and recognise some regular posters, so does this mean Carlos 67 the recent homeowner in Tauranga is also To The Point, who is some guy called Tim from Property brokers who claims to be renter? Is Luke83 and CWBW also same person?

YES. Tim Mordaunt ( TTP ) has been caught doing this before, he uses multiple accounts to fool the public into a false sense of the fake narrative to further his Property Brokers agenda. Listen to how Blow Hard his radio advertisements are.

https://www.landlords.co.nz/article/976511533/property-brokers-advertis…

Wow, I've seen TTP have conversations with Carlos67 were they agree with each other. So it's the same guy switching accounts. If this is true it's some next level deviousness and dishonesty. Would anyone do business with this guy if they knew the nature of his character?

To be fair I think a few do the multiple account thing - there's several with a similar writing style and the same opinion.

Amazing that people choose to live such complicated lives just for the sake of making their point of view look popular. No confidence in their arguments?

Now I am confused.

TTP

Oh shit I'm in the matrix and have morphed into TTP.

TTP or was that Me.

Yes I agree. You are very wise.

TTP

I know many friends, family members and developers who have all stopped using Property Brokers Realty because of their con artist tactics. I wonder why those salesmen for TTP Tim Mordaunt ever thought they could ever get away with such low morals ???

I have had the misfortune to deal with them twice here in Wangavegas, I was truly aghast at the standard of service or lack thereof

I called them both knobs last week. I feel silly now. It’s a bit like the ending of fight club where it turns out to be the same guy… except not cool and extremely pathetic

I always knew those 4 thumbs up continually on TTP comments were his own fake accounts. Who ever would of thought Tim Mordaunt the owner of Property Brokers Realty would be so manipulative and dishonest ? I wonder what the editor will do ?

The whole connected industry is Dishonest and manipulative. RE agents, brokers, MSM pumping out ads and reenforcing everything only cause they all get paid to.

Bubbles don't get this big without being constantly hyped in the right direction. At this point, increasing inventory and the promise of ever increasing loan costs, its turned from easy sell, to pushing water uphill with a rake.

How many new agents started in the last year? There are a lot of people who are used to easy debt fuelled cash and NEED the party to continue in order to sustain business and therefore personal cash flows.

Example : Wifes RE boss bought a new boat in December, last year was party time, making money like its grown on trees, This month he's complaining that there are no buyers and auctions keep getting pushed out.

Winter is coming and agents need sales to survive.

Would've is short for would have and not what you wrote.. "would of"

LOL I knew the multi-accounts were brewing here.

So sad and pathetic.

Desperate. And yes, sad.

I used to enjoy the comments sections on interest.co.nz because of the seemingly diverse community of commenters from different walks of life exchanging ideas and opinions etc. Quite disappointing to find out everyone on here is actually just some guy called Tim having conversations with himself.

TTP

No, I do not have multiple accounts.

TTP

That goes a long way towards explaining the dropkick vibe that seemed to ooze from so many comments.

The Putin apologist was a nice touch.

Here's hoping its just Carlos taking the mickey out of TTP (and they actually are individual entities).

If not it is all bit sad and desperate.

Just like I watched in the US in 2008 though, is that those who were arrogant and acting invincible (and know everything...) while property prices were going up and they were making large $$, they start becoming quite angry and defensive when the market turns. And the more debt they were holding the bigger the change in personality.

If the market actually does fall properly, I wonder what other side of their online personalities we will see. Usually its at that point you see the true character...i.e. the wolf in the sheeps clothing becomes very visible.

You got it right IO but shit did it stir up the hornets nest. People are really sensitive on here. God knows how I'm going to clear my name, maybe I should become a DGM.

Good luck - you might need a new username! Carlos67 has been tarred with the TTP brush...

Interest.co.nz need to tighten up on their new account generation by linking a mobile phone number to it. When you setup a new account it needs to send a confirmation code to the mobile number to enable the account. Still not perfect but it makes it harder to have a multiple personality disorder.

small and miserable

An increase from January to February on the HPI is typical. 0.5% is very low when compared to previous periods, but not too surprising given the CCCFA has just come into play.

Previous Jan to Febs:

- 2021 6.8%

- 2020 4.1%

- 2019 1.8%

- 2018 1.9%

Anyone know how many FHB's purchased on low LVR's last year..say in Auckland?

If a 10% deposit they are quickly facing the prospect of negative equity. Another 3 months might be enough to see them below the line.

Yes would be interesting to know.

5-10% deposits have been possible on new build townhouses for FHBs, but not on existing homes. And it's probably the new build townhouses that will suffer the biggest drops.

Hopefully a few potential FHBs were listening to us DGMs last year, rather than TTP, Yvil etc, and didn't jump in.

God only knows who would be stupid enough to buy off the plans now, falling prices and rising input costs equals recipe for disaster.

If you are thinking of doing it - don't.

You have been warned.

Yip - had a relative just finish a build for retirement. Ended up 30% above initial estimated cost. And now the potential for the price of it to be falling.

Many developers are putting their off the plan prices 5-10% higher than current input costs would demand, to account for further inflation over coming 12-18 months.

Most of the off the plan townhouses and apartments on the market right now are at stupid prices. Avoid them. Or...wait for the prices to be slashed 15-20%.

I would definitely think of buying a two bed new build townhouse in a goodish location if the asking price was cut 20%. So from say 1 mill to 800k.

And maybe somewhere like Mt Wellington if the price was cut from 900k to say 750k.

Tell him he's dreaming

Why?

Both of those numbers look like a nightmare! Unless of course we have massive wage inflation...

But that's the reality, right now. Yes, two bedroom townhouses in Mt Wellington for 850K.

And I'd like to hear HW2's response, why he thinks 15-20% discounts aren't at least a possibility, or perhaps 10-15% (I've seen 5-7% discounting already). It's very clear what the headwinds are for new housing development, if developers have to sell at a price that only provides a tiny profit margin, to save their backsides, then they will (or at least some of them will - some will hold out for too long, hoping / expecting that things will recover quite quickly).

BTW, has anyone seen the header 'Quiet Response' on RE agent advertisements? I saw that the other day, for an off the plan development. What's it code for? Presumably low sales rates / low interest? It felt odd to see it in an RE agent's advertisement, where it's almost always bullish and full of BS.

Whatever happened to that old username Fritz... always overcooking what might happen. When you/housemouse were pumping for big rate rises at the last review it did not happen, and did you ever eat any humble pie over that?

What planet are you on?

When did I ever plump for big rate rises? Never!

If you read this website consistently, you will know I am bearish on interest rates rises. Much more bearish than almost anyone.

Thanks - not! - for totally misrepresenting my position.

I've made a note - totally ignore anything 'Flying High' has to say!!!

Are you a developer (your user name sounds a bit like a developer's), really worried that what I just said is likely?

Have a lovely evening...what a weirdo!

First of all, take something for that to help control yourself.

I recall you involved in several convos and agreeing with every one of the opinions. You couldnt make your mind up where you stood but in favour of big ocr hits

It's unfortunate RBNZ C31 is not that granular.

11,000 FHB purchased at higher than 80% LVR last year. The spread was fairly even throughout the year, apart from December where the monthly number dropped 25%.

Average monthly borrower numbers (Jan-Dec) for over 80% LVR FHB:

- 2017 = 441

- 2018 = 654

- 2019 = 866

- 2020 = 922

- 2021 = 917

How many... a few thousand I would hazard a guess had less than twenty percent deposit.

a bigger worry is the number of developers that hatched a plan some three years ago to buy a house, remove it and build six townhouses( and the amount of 2nd tier finance cos only available to so called sophisticated investors and friends and family of coarse)

I think we are going to find out a lot paid only six hundred thousand for a house in some unheard of area yet a year later they have had revalued it at 1.6 mill. Then they have a contract rate somewhere 3500-4000 to build and it ain’t going to be enough.they have used the new equity borrow two-three-four million from a second tier finance co.delays, delays, extended interest costs and now the prospect of each unit being a hundred or more thousand less.there’s another million blown.

Do they developers keep putting money in or abandon ship?

Do investors keep putting money into these finance companies?

Yes the whole system is exceptionally reliant on prices continuing to rise.

One reason why I think its been crazy allowing investors to use equity in existing homes to buy even more homes. There is no real earned income there...just magic paper money being created and used to push prices even higher and out of reach of FHB's who have to generate real income to save for their deposits..a completely unfair/unjust/unethical market/system.

Most developers are effectively beholden to prices continuing to rise, ESPECIALLY when input costs are soaring and will go higher.

The party is coming to an end.

I'm actually more afriad of the government and RBNZ now...than the greed of property investors pushing the prices of homes out of reach of FHBs.

What worries me the most is what insane things we are likely to see from Robertson and Orr if prices do really start falling - and what the unintended consequences of that will be on the broader economy.

Social instability we've been witnessing (while blamed on COVID), in my view is really related to people completely losing hope as a result of monetary and fiscal policy that has gone very wrong and is so terribly in favour of asset owners that its causing fractures in the social contract.

What do you think ORR / RRObertson might do?

Surely not stop hiking the OCR?

Surely not dishing out FHB Grants of say 50k for new build purchases?

Surely they will start dishing out big first home buyer grants. And even more money to prop up failing developers.

Yeah that's what I think 'could' happen. (but not a prediction!).

Helps get FHBs into home ownership (until it doesn't - because it would push prices up) - TICK

Saves the residential development sector's bacon - TICK

However I suspect they won't (or at least not this year, maybe they will next year - Election year), mainly because I suspect they are too dimwitted to even know the headwinds approaching for the development sector. After all, hardly any economists are foreseeing this.

So maybe something they do in Election Year budget - when it will probably be too late for the development sector.

And probably not 50K, Homestart is already 10K, might go to 20 or 25K? Which won't make much difference.

Be interesting to see just how much further of a welfare scheme property gets turned into.

Anything is possible, really.

But I suspect the govt will tinker to almost zero effect, as per their shared equity scheme.

For example, increasing the Homestart grant from 10K to 20K or 25K - would make jack all difference, but it's performative isn't it.

50K would make a difference, but I doubt it's tenable.

They might remove GST payable on new build housing for 2 years - probably very unlikely, but it's been done elsewhere.

Yes it's a house of cards.

The reasons you mention and others have been why I have been calling a big building slump for later this year.

So its either, there is a crash/correction coming/happening or prices stable/going up depending on what you read in the comments here.

I would be interested to know what people think of the following:

Do you think the RBNZ/Government can do anything to stop house prices declining or are their hands tied with inflation and raising the OCR.

Would removing all restrictions i.e LVRs, CCCFA have much of an impact or is it too little too late and you think that its a foregone conclusion that prices will keep heading the way they are?

Do you think the RBNZ/Government have any tools left that could send house prices up rather than down regardless if its the right or wrong thing to do.

With the boarders eventually opening to all giving a boost to tourism and the economy, will tourism save the economy and possible recession? or is tourism so far gone it will take a couple of summers before we get back to normal tourism levels?

Q1 answer: no, not in the short term. I have predicted the OCR won't go higher than 1.75 this year, but that's an entirely different thing to cutting the OCR now. Which is what would be needed to halt the decline, but is clearly not tenable.

Another thing that might halt the decline is dishing out 50k FHB Grants.

Q2 answer: might mitigate the extent of falls, but not prevent falls.

Q3 answer: No. Mitigation of falls possible, but not avoidance.

Q4 answer: Will need at least 1-2 more years before there is a significant tourism rebound. Even then, there are heaps of headwinds, especially inflation eating in to disposable income for luxuries such as travel.

On the tourism side of things, my wife is a Travel Broker, after no business to speak of for a couple of years it is coming back hot and heavy, admittedly her clients are all big earners.

We have friends with pretty big inbound tourism operations in North America and the UK, they are struggling to find staff to deal with the volumes they are processing now. I really dont think it will take long to roll back in, the biggest hurdle here is getting it back to a free for all, both with borders and the hospo restrictions (which are just stifling and pointless at this point in my opinion)

Yeah I think high end will rebound quite quickly, but not low-mid end.

People talk of 'revenge travel'.

This Weeks Hutt Valley Update ( for those who have seen my weekly updates).Please note I also posted it on the Kiwibank article from this morning - but may be more relevant here.

610 houses on the market. REINZ data showed 96 sold in Feb – so less than 25 a week now selling – down from 40 a week this time last year.

If the current sales continue – that’s 6 months stock on the market. Using 40 sales a week its 15 weeks (close to 4 months stock on the market).

I was surprised to see Lower hutt’s Median Value jumped to a record $940 000 in yesterdays REINZ data. Using the sales data I record (which is the last listed price for the property) my data showed the Median house price was $895 000- but this was on sales of 30 houses.

From the 30 houses sold in Feb that I have a price for It appears there were a lot more houses sold over $1 Million in Feb (12) vs 18 which sold for less than 1 million. When I compare the 26 houses sold in Jan – only 7 were priced above $1 Million and 19 below 950K

It’s not necessarily a signal prices have lifted in the market- it appears the mix may be the big factor- a lot more 4 beds and 2 baths’s sold in Feb vs 3 bed and 1 bathroom in Jan. This could be a sign that a lot more owner occupiers bought in Feb than first home buyers and investors which typically are attracted to the smaller cheaper properties.

It did however make me curious what was happening at each price band – so I did some further segmentation. Looking at the 251 houses listed with a price

- 32% are priced over $1 Million – 36% of which have dropped their price. Average price decrease is 121K

- 11% are priced between $900K and $1 Million – 34% of which have dropped their price. Average price decrease is 73K

- 26% are priced between 800K- 900K – 45% of which have dropped their price average decrease is 47K

- 31% are priced below 800K – 49% of which have dropped their price. Average price decrease is 49K

So interestingly the top of the market is taking bigger price decreases (10% reduction on listed price ) than the bottom of the market – which are decreasing by about 5%

The data also shows the majority of houses listed are under 900K. The Median house price for all 610 listings is 850K

Time on Market

380 of the houses have been on the market for over 30 days - 62%

196 of the houses have been on the market for over 60 days - 32%

Rental Market

Meanwhile the rental market has 171 properties for rent (this is now extraordinarily high) – normally the properties for rent are 110-120 at any given time.

This would be deterring investors big time and is a market to watch. It would be a strong indicator of an oversupply of housing.

Great work again!

Yes rental availability is surging in Auckland, lots of new build townhouses sitting still for weeks.

Makes one think that average rents may not increase much this year, despite inflation.

Just looked at Meadowbank, Auckland, the last suburb we rented in before buying 2.5 years ago.

Rents only look to be about 5-7% higher than what they were 3 years ago.

Thanks for the comments and analysis

Thanks for your mahi sir - most informative!

One would normally expect a much stronger seasonal bounce from January to February. These numbers are very flaccid.

It's okay. It happens to all HPIs on occasion. It's nothing to be ashamed of.

Not really after the gains of the last 12 months which must be a record in absolute dollar terms, let alone percentage terms. Predicted a while ago it would be flat house prices for years now, its happened before even without with the crazy gains. Still predict single digit gains for Tauranga in 2022 but we may be in a bit of a unique situation down here we are duffrunt.

I'm glad you are real Carlos, and not a TTP alter ego.

Watch out for Tauranga price falls though, they will sneak up on you. Check trademe for Tauranga listings, they are up massively and many now with a price or "by negotiation" when before it was all by auction.

The stock for sale in Tauranga is building fast. All you need is a few desperate or frightened sellers and the falls will be just as fast as Auckland.

At this point, I fail to see why most people wouldn't just sell and rent for a while. Save your shirt.

I saw this today about Aussie house prices. It makes me think NZ house prices are probably overcooked.

Ratio of value of housing stock to GDP Australia: 495% (similar proportion to NZ)

United States: 180%

United States + Every publicly listed company on U.S stock indexes: 354%

And there are fears that the US is back in housing bubble territory given the buying frenzy of the last few years.

I'd imagine that Canada could be similar to NZ/Aus.

Just completely off scale high....far too much capital mis-allocated to residential property to allow our economies to be competitive in the future.

Completely agree, we've had incredible influx of debt i.e future spending power, spent on bidding up the cost of existing assets, it makes sense for individuals who have profited from it but as a nation it's just dumb. Would have been far more sensible to have focused on increasing productivity which would have increased wages and decreased the cost of living, and then we could have been a actual rock star economy rather than a one hit wonder

Greg

This daily saw-tooth up and down of house-price movements is simply not good enough reporting in the age of advanced computer technology. The readers rightly expect an hour-by-hour reporting of these statistics.

Please no. Much like Bitcoin, people will cheer granular spot price increases, and cheer granular spot price decreases, while ignoring the overall trend.

It's going to be an interesting year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.