First home buyers held their own in the housing market in February, but the average amount they're borrowing has started declining and they are taking out fewer of the riskier low deposit mortgages.

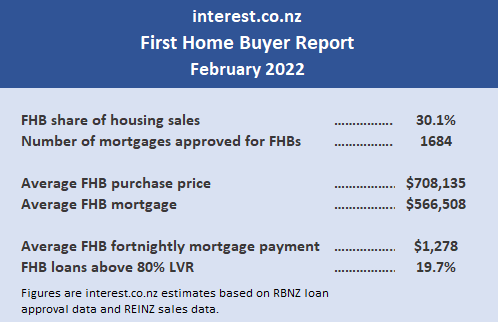

Interest.co.nz estimates first home buyers accounted for 30.1% of total housing sales in February, up slightly from their 29.4% market share in February last year.

First home buyers’ share of the housing market has steadily increased over the last five years, rising from just under a quarter of all housing sales in February 2016 to just under a third currently.

They have also started borrowing less money this year, with the average size of the mortgages approved for first home buyers declining for the second month in a row to $566,508 in February, down from its record high of $595,274 in December last year.

That means that on average, first home borrowers in February were borrowing $51,164 more than they were in February last year and $133,252 more than they were in February 2020.

The decline in the average size of the loans being taken out by first home buyers appears to have occurred mainly at the riskier, low deposit end of the mortgage market. This suggests recent moves by the Reserve Bank to rein in riskier lending are starting to work.

The percentage of mortgages approved for first home buyers with less than a 20% deposit has declined steadily from 37.9% in October last year to 19.7% in February this year, which is the lowest it has been in any month of the year since the Reserve Bank started publishing the figures in August 2014

The record high for low deposit mortgages was 40.3% in May 2020.

Interest.co.nz estimates that first home buyers are also paying slightly less for the properties they are buying, with their average estimated purchase falling for two months in a row from a record high of $744,093 in December last year, to $708,135 in February this year. That's a decline of $35,958 (-4.8%) over two months.

The reduction in the average amount being borrowed by first home buyers means their estimated mortgage payments have declined by $67 a fortnight over the last two months, from the peak of $1345 a fortnight in December last year to $1278 in February this year.

That’s a 5% decline since the beginning of this year.

That reduction in mortgage payments has been helped by the fact that mortgage interest rates have remained almost flat over the three months from December 2021 to February 2022, with the average of the two year fixed mortgage rates offered by the major banks staying within the tight range of 4.19% to 4.21% over that three month period.

However interest rates are expected to keep rising well into next year, which could put first home buyers under further pressures if prices at the bottom end of the market do not continue to fall.

Overall, the latest figures suggest a considerable reduction in the risk profile of first home buyers, because on average they are starting to pay less for the homes they are buying, they are borrowing less, more of them have at least a 20% deposit and their average repayments are coming down.

However those figures are just the first tentative steps in the right direction.

Unless prices at the bottom end of the housing market keep falling at a greater rate than mortgage interest rates are rising, first home buyers could find it becoming even more difficult to afford their own home than it already is.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

138 Comments

Running for the -30% Crash in home prices. By December this year.

14 Houses auctioned at B&T central auctions today. Result: 1 Withdrawn 13 Passed in.

Ouch.

Waikatohome - Thats crazy. When the media say that Auckland City median house price falls 19 per cent since peak in November you can actually see the proof in the pudding by the auction results coming out at the moment. Not much fun being trapped in a buyers market trying to sell, prices tanking, interest rates increasing at record speed, etc etc etc. Good time to be renting though, just lock in 12 months and sit back and enjoy the ride.https://www.stuff.co.nz/life-style/homed/housing-affordability/12811007…

i'm waiting to see how they put a positive spin on that one ;)

I'm surprised sellers and agents are really that stupid, that they are still going to auction.

What is the point of selling by auction in a buyers market? Buyers hate auctions.

If you want to sell your property in a falling market, you need to list it with the price you're willing to take for it... and hope like hell someone wants to catch that knife.

I used to hate auction but if your a cashed up buyer its the way to go. Auctions cut out all the shit, you set you price and go for it. Its even more fun if you have way more than you know the house will sell for. The obvious problem right now is that the market has turned and both the RE agents and the sellers will not admit it. Decent houses are still selling at realistic prices, problem is there is now a disconnect between buyers and sellers.

The prices are still far from realistic, but give it a bit of time.

The recent new RV's have put a bit of perspective in the market down here, however some people still think their place is worth hundreds of thousands over the new RV and that's simply no longer the case.

Still predicting small gains for Tauranga in 2022?

For sure, those fortunate enough to own their own home ain't going to give it up easily.

They will hang on to it like leeches.

Can't say I blame them. (Renting isn't much fun.)

TTP

No point replying to 2022, it's a bot. Has posted this same comment on a bunch of posts.

What could you say though. People are going to be underwater even without all this rain.

Thank your lucky stars it is not you flooded out. Forget making cheap shots.

2022 & Retired Poppy are one of the more obvious multi account holders.

Making such conclusions based on assumptions is foolish....

I have only one account.

Anyone who takes the time can see the truth. You constantly give yourself away.

Okay then, who else am I? 🤔

TheCrashCrusader

Oh the irony. TTP has been saying the same thing for the 4 or so years I’ve been around.

At least he takes the time to re word his comments. 2022 is literally copy paste

Thats not fair. If you pay more attention you will notice the beautiful chosen words are not actually the same. Same message though. Can't help whats coming.

Ctrl "C", Ctrl "V"

Cmd-C, Cmd-V

Only 4 of the 13 passed in properties received any bids. They are not holding on to the property through choice. No one wants their house.

Finally people are seeing sense. Wait let prices drop, take your time, plenty of houses out there. The problem before was that everyone was panicking. No need to panic, grab some popcorn and watch prices drop.

A leech is usually defined as "a person who extorts profit from or sponges on others".

That would be more property investor/landlord types, not homeowner. Landlords are extorting profit from others and sponging off their weekly wages via rent.

Hi Tim - Do you play the saxophone by any chance ? Maybe you could help out your agents for the open homes !

https://www.stuff.co.nz/life-style/homed/real-estate/128055412/just-how…

“The market has shifted really quickly, and values are back 10 to 15 per cent,” he says. “There are vendors who think the market is still buoyant and buyers who think they have heaps of control, which creates a big gap.

“The vendors who take our feedback on board are the only ones selling.”

The saxophone player thing screams of desperation....and wasted/excessive agent fees. Perhaps everyone should do it? Not just a free drone to do the house video, but also a free clown show and juggling at the open day.

You mean you don’t visit open homes for the free clown show?

Watching the prices being paid for some properties and the mania shown in auction rooms was certainly a bit of a circus.

To be fair, we (FHBs) bought pretty damn close to the peak. We managed to get a place with a bit of character and for a few hundred K less than what the vendors were expecting at auction (we bought by negotiation when everybody had forgotten about the place). Although I don’t regret it, and we can comfortably afford even steep interest rate rises, it’ll be hard not to imagine how much better we could’ve had it if we waited until the (probable) crash.

IO on the sidelines watching, where he has been waiting patiently for ten years

Nice troll…strange how my posts trigger you 🤔

My share, bond and property holdings have done great the last 10 years so not sure what sideline you’re referencing 🙂

Harcourts agents Matt Winiata and Aneil Daya are offering $5000 worth of Mitre 10 vouchers to the buyer of a house they are marketing in Royal Oak, Auckland – “to give your home a kick start”. Other agents offering "free" aircon, appliance upgrades ...

These aren't free, you're still paying for them, just indirectly. It's nothing to do with marketing the property, it's done to mask the price drops that are occuring. They don't want to knock off money from the price as it further sends the signal that prices are falling and people are reluctant to buy when the market is falling because they don't know how much more it will fall.

Was reading the other day that the top 20% of RE in Auckland are on $300,000p/a income.....so whats $5,000 to get a house off their books?

And there are thousands of RE in Auckland....the average RE income was around $120,000 or something, despite that it takes a few months training and you're good to go.

Industry is waaay over compensated for the skill set required and from a supply/demand perspective.

Watch the demand side of the equation tank!

Well spotted.

All the desperate old tricks starting to be pulled out of the hat...

TTP and Te Kooti practice for their open homes.

It's practise you grammatically challenged coward.

You looked very happy there kooky. Right in your element. I think Tim needs a haircut though.

Hahaha good come back

Tim The Point appears to have abandoned the soft landing 😬 Now he refers to those fortunate to be in financial difficulties as leeches? Slow clap for the Property Broker!

Maybe we should change his name to Toking The Joint ? TTJ

TTJ

Would love to Change my name to that.

But 50.1% of you said you prefer living in the 1950s.

Yes I'm still bitter about it.

Let's not go down that rabbit hole, FluffyBunny!

Your probably right... all for the best.

Agreed... I could imagine renting from TTP the Palmy mega-landlord certainly isn't much fun.

All 3 of your accounts run these "Imagine" scenarios... It's a dead give away.

Okay now you're looking foolish 🥚

You're not the only multi account holder commenting here... Keep up.

the way - Hi Tim, its those 4 upticks consistently on your fake accounts that is the giveaway. You need to break it up a bit.

Language is like a fingerprint. You may want to think about that.

Your comment is as weak as your argument.

Thats why we know you are Tim Mordaunt.

Any other fool can see that's not at all likely.

The affable Peter Thompson, Mr Barfoot and Thompson, is more likely

What's a dead giveaway?

Nah, single account - just the same point of view as the OECD, IMF and others on here (affectionally called by you and TTP etc as the DGM'ers) about an overcooked, unaffordable, unsustainable property market... so I could see why that would easily confuse you.

I see this market now as russian roulette - sure, you might be right, it might be a correction and not fall more than 10-20%, I guess that statistically, someone has to have the highest house prices in the world.

But things have certainly changed dramatically in a short period of time, and we now have bullets added called; interest rates rising beyond expectations, inflation out of the bag, building oversupply, relaxed resource consents, responsible lending, emigration, geopolitical risk, removal of interest deductibility, the list goes on etc that it's hard to see where there is an empty chamber...

CLICK

Lot of people are starting to get very worried. It's palpable.

We are well and truly into the 'Fear' phase of bubble psychology, moving into 'Capitulation'...

Your comment made me revisit the bubble graph. I see that after capitulation is despair and then the market returns to the long term mean. What level of prices do you think that would be? Would it take us back to pre-2020 levels?

2018/2019 levels.

I agree but I think there is an outside risk of 2016/17 levels if we don't see immigration levels returning.

2019 is looking pretty good to me. Depends on where the rates end up.

Roughly speaking, try this :

Take where ever rates top out at (consumer lending rates, main banks). Go back to whatever year they where last at that level. Take the avg house price at that time. Add CPI inflation since then (Wage growth maybe?). Factor in +/- 10% variance. what you think?

Having lived through the bubble in the US during the GFC, if this bubble does burst from here (which is always an if), I think we more in the denial/return to normal phase at present. Most people are still thinking that prices don't really drop in NZ, there's bad news out there but we don't really need to worry about because prices never significantly fall in NZ etc (more the denial type of thinking - even though there are reports of prices already falling 10-20% in areas).

The fear might happen throughout autumn if prices are consistently dropping, and capitulation if we have a severe recession over winter. The fear and capitulation phases are obvious because you can see it in the faces of people you meet - its proper pain. I don't see that yet...most people are still unaware of the possible risk.

The average number of FHB taking out loans above 80% LVR was 917 per month for 2021. First 2 months into 2022 the average is 311.

People on the side lines are critical of the CCCFA, citing how it penalizes FHB. I struggle to see how allowing FHB the ability to borrow "more for less" is the suitable alternative to limiting credit to more creditworthy borrowers, investor leveraging included. This should take out demand allow prices to fall. Ironically as prices fall, you should find an increase in the number of "creditworthy" borrowers with real cash deposits.

Ask any aspiring FHB, would they like to buy now with a 10% deposit, or buy in 12 months with a 20% deposit?

Partner and I bought with 15% at the "top" in October. Structured the mortgage (33% - 1,2,3 yearly) so that we see increases coming & can absorb over time. Lucky enough we can absorb up to 7-8% & can rent the spare rooms out for extra cash in to ease that pressure.

It'll be our home for 10 years +, so we just have to keep clipping the ticket, not shaking in our boots at the prospect of a short-med term dip.

It'll be our home for 10 years +, so we just have to keep clipping the ticket, not shaking in our boots at the prospect of a short-med term dip.

Sensible...

You sound like you have a good plan. Having your own home and not being subjected to the whims of a landlord is priceless. No one can predict the timing of a market peak until it has passed, you buy a home when you can afford to. Enjoy it.

"not being subjected to the whims of a landlord is priceless" - not quite, many people will be weighing up being subjected to the whims of a landlord for a little while longer. It might be better than committing the bulk of you income to 30 years of repayments on an asset that may be significantly cheaper in a few months time. Short term pain for long term gain. This is more likely to explain in part the big drop in numbers of first home buyers.

That is possibly true today, I wouldn't be rushing in right now if I didn't have to. But when engineer bought the market was still humming. They also plan to hold for ten years and have worked out their finances. If I was in their situation back in October I would have probably made the same decision that they did.

All good, I think we agree. I just thought the priceless comment was a bit over the top. For some people now may not be the time to buy.

We do agree. My comment further down explains my experience of renting. For me getting back into home ownership provided stability for my family and I place a high value on that. Entering into the market today would only be sensible for those with high deposits, good incomes and a long term view.

We traded up into our forever "10+ year" home in December. Tripled our mortgage. Chucked the whole thing on a 5 year fix, set and forget.

There will likely be other FHB that bought with less % and potentially with a higher loan than you. If there is a dip into negative, the most the bank could likely do is call in some margin but I imagine it'll become very political if they ever tried that

As Waikatohome mentions, you have a plan. Enjoy your home, it's difficult to put a price on the freedom home ownership gives you.

So you're not sweating it out then... I wonder if there were many others who did the same with 3 to 5 year mortgages

Not sweating here. Mind you, 12 months ago we were locked in 5 years at 3.05% with a DTI of 1.2 on a 7 year repayment schedule. But, you know, happy wife = happy life etc.

Your plan works for you which is great. Whatever works for the individual.

Im old though with kids, we will always need our own place, but we rent at a much lower cost then buying a house. Our rental house will always be available to rent as we know the owners, farmers with a couple of rentals for their kids.

We are using our money from a sold house to build a business, not all of it just a small fraction. The aim is to have greater than 100 products selling in a few years. Each product will bring in greater then USD 4 to 5,000 profit a month. Once we get to 30 products which will be 2 years'ish we will look at a house. We are content, the kids are happy, as long as they are happy we can tick along nicely. Different strokes for different folks and different circumstances.

Yeah as long as it works for you most important. Personally we are happy waiting and renting.

Your situation is fairly unique as you have a friendly landlord open to a long term relationship. We rented through a large Auckland real estate company when we first came to NZ. We were treated really poorly. In the first rental we were served notice that the landlord was selling after 2 months. We were handed a letter after a knock on the door at 7.30pm as we were putting the kids to bed "are we losing our house daddy?". Not great after 2 months in the country.

We found another house through the same agent and were charged another fee. It was really dirty with dead flies under all the windows. I took a lot of photos on moving in day. When we bought a house, we left the rental house far cleaner than we moved in, but they tried charging us for cleaning due to grease on the extractor hood. I sent them all the photos of how dirty it was and they soon dropped the charge.

Would never rent in NZ again, they treat you like scum no matter how much money you have in the bank.

that's no good.

As a landlord myself I go out of my way to treat tenants well. I had one of my properties come up last year & the tenants wanted some flexibilty as they where looking to buy. I could have moved them on and got new tenants with more rent, but they'd been there for about 5 years & the market is tough, so I wanted to help. I basically said just stay as long as you need, don't worry about min notice periods etc and move out as soon as you want whenever you buy something. They stayed about 12 weeks and then won and auction, moved in 2 weeks later.

When I was in the UK we rented long term from the same lady for years & she never put the rent up. Helps a lot when you are re-landscaping the garden for them.

If you are a good tenant, maintain the property as if its yours & dont call your landlord to fix a $20 shower handle, most landlords will go out of their way to maintain the steady income stream.

Its a good call also looking to see if landlords are open to long term rental agreements, 2 years etc.

Shame we didn’t have a landlord like you. I shouldn’t tar all landlords with the same brush.

I don't know.

As long as I see "no pets" in the most of the rents on trademe I will think that the most of the landlords are not good people.

Are you a "no pets" guy?

That is one big difference between being a renter vs owning your place.

There are many others, of course.

Diclaimer: I am a renter and I just decided to rent for another 12 months and I have a dog (and let me say that is not easy to find a place with a pet). I can afford to buy an house (even now) but I am convinced that I will whrow away 300k if I do, so I prefer to keep renting.

That's the sad thing. Landlords are a little too precious over their properties. They want to claim all sorts of deductibles because it's a "business", yet at the same time dictate whether a tenant can have a dog or hang a picture because they're renting out a "home".

How many renters out there are going to turn down a property because the grass in the backyard is a little patchy from the last tenant having a dog? Nobody cares except for the Landlord. Maybe we need to introduce a psychometric testing regime prior to people acquiring rental properties.

Some, like us are negotiable about it. You also get a lot of tenants who are not responsible and dont care if the animal causes permanent damage.

Glad you are a negotiable person.

For many others:

-to cover damages there is the bond.

-you can ask a bit more if there is a pet, instead of just say "no pets"

-you can ask a supplementary insurance

there are so many alternatives

I saw places, "no pets" places, that looked like CSI places.

And, I am sorry but I am biased here, "no pets" points to a landlord that is not a good person. The next step would be "no kids".

I have pets and kids, in our house (which we own) I would say the kids cause more accidental damage than the pets!

Depends what type of parent you are. While renting I was paranoid my kids would cause damage to the place so I never let them have pens/drawing materials unsupervised. The place was a 1960s/1970s mishmash time warp so I shouldn't have cared so much but I did because that's the way I roll. Now we have our own place I don't care if they draw on the walls a little.

I hadn't seen an article clamouring for the removal of the CCCFA recently, it seems the argument that it was crushing FHBs doesn't hold water.

Just like how gradually removing the tax credit on mortgage interest was going to cause a tsunami of investors exiting the market

You're exactly right. The tales of being being denied because of one trip to Kmart are rubbish. Likely they weren't able to service the loan anyway (LVR or DTIs) and the discussion about spending was part of the "this might help in future" coaching. Changes to the cccfa will make little difference, its LVRs, general interest rates, buyer confidence and FOOP that's curbing FHBs desire to borrow now. The mortgage data out yesterday says that high LVR lending to FHBs has halved. CCCFA has been a convenient scapegoat by mortgage brokers because they had to work far harder for the same deal and that impacted the time they have on the golf courses....

I think it was just another example of highly vocal people with partisan views being critical of anything that Labour comes up with, so they fabricate some David and Goliath story of unintended consequences to try bolster their position.

Labour & National = 2 cheeks of the same backside ;)

By your analogy only an arsehole separates the two? :)

That is no way to describe the Honourable Mr Peters, apologise immediately:)

While we're on it, what do you reckon the chances are of Winnie throwing his hat in the ring for Tauranga? I'd wager he's cheeky enough to give it another go.

Anything is possible. I quite liked the handbrake he put on Labour in the coalition. Ron Mark seemed to do a decent job in defence too. Not sure if I would vote for them though.

Be interested to see how the changes to the Ccfa will play out

it will do sweet bugger all nothing. Ignore the clickbait, It restricted less than 10% of borrowers.

All eyes on the cost of borrowing money & the spare income to pay for it.

My view is that NZ property is like an over-priced tech stock.

Lots of good feeling, hype and the promise of future returns.

But ultimately sensitive to rates going up.

We will see... or not, whats the Auck avg down since Nov? Sweet bugger all being sold by auction out East now...

Astute first home buyers will be taking a big step back as this toxic hot mess of a housing market implodes.

The writing has been on the wall for quite some time. My thoughts are with the victims that believed the spruiker drivel.

Just some anecdotal evidence here. some of my friends are landlords and from most of them I'm hearing the same yarn. "i'm busy painting / preparing for sale, i need to off load at least 2 rentals" I reckon there will be a lot more listings in the next couple of months.

I'm sure most will still do well, property may be down ~20% from the peak, but its still up ~10% year on year and the previous entire decade had annual positive growth.

Once interest rates come of emergency levels the housing market will fall back fast dropping around 50% from peak last November. It could be more in Auckland and will settle around the price a average wage earning couple can afford to buy. If anyone is thinking of buying soon I would wait a while.

That would take us back to early 2016 house prices and we would be staring down the barrel of the next great depression.

Would it? It didn't cause the great depression in Ireland, Spain, US etc and other property markets where bubbles have burst.

It certainly would be reverse of the wealth effect... and discretionary spending would largely disappear from many households.

But people would soon accept that it was paper wealth and their house is worth $500k again rather than a $1m.

And those that bought in 2016-21 would just be paying off their mortgages for the next 20-30 years like they planned.

But the next generation would have the opportunity to get on the ladder, like previous generations did.

And those with excess capital would be putting it into other investment classes that potentially created wealth or jobs, rather than residential property which would be seen as a homes rather than investments.

Not to that level. But they did see massive increases in unemployment and recession.

You have a very rose tinted glasses way of looking at this.

Yes, of course there would be massive increases in unemployment and recession.

Just like what happened in much of the Eurozone.

But that is short term pain for a longer term gain.

Rose tinted, is thinking what we have is sustainable. We either take the pain now, or kick the can down the road again.

I lived in the UK during the GFC. Even with all that carnage I was always able to find contract work.

The 30's depression was altogether different from just a single sector, in a small backwater country, going through a healthy correction.

We are completely screwing over anyone aged 20-something and younger on our current course. Some blood now will go a long way.

and we would be staring down the barrel of the next great depression. WE ARE.

We managed to dodge that bullet by the central banks and governments around the world going crazy printing money and intervening in markets.

I think we are just starting to see the unintended consequences of that 'free market' intervention.

Depression is always a possibility when you see the amount of price inflation in assets and debt that we have witnessed the last 20 years - see the comparisons with the 1920's and what we've just seen of late, including wealth gaps and speculative mania for things like property, crypto and growth/tech stocks.

It certainly sets the grounds for hard times....we are in unchartered territory and the central bankers are well aware of it.

20% fall would erase around 27% of growth in prices.

Plus you have agent fees etc.

Fine if you bought more than 2 years ago.

Mate of mine bought an apartment off the plans a few years ago, got a 5% deposit loan and all the FHB support he could get, lived in it for 6 months to meet whatever conditions on his grants and then rented it out while he flatted somewhere else. Was chatting to him the other day, interest deduction changes are going to kill him so he's putting it up for sale. Problem is, it seems a few others in his complex have the same idea and there are four others the same spec as his apartment already for sale, asking price is what they paid off the plans four years ago, so he's going to be lucky to get what he paid for it minus transaction costs.

Crash alert!

Is that an Auckland City apartment? I would imagine they'd be the first to drop. The city is dead. Around where I work my three favourite eateries have gone out of business in the last three months, and the newly completed apartment buildings - those "mixed" models with shops at the bottom and apartments above - not a single shop has been tenanted.

I'm assuming that the body corp rates would have been set with full business tenancy in mind, and are therefore likely to skyrocket if that doesn't eventuate.

Could be some bargains in the CBD in the coming 6 months, as I've said before.

Thats what I call a Race To The Bottom !

can you send me the link? =)

Ouch! Same as 4 years ago... no way....wow

A settling of the market is surely a good thing. May it settle for a while longer.

I suspect a key reason that low deposit loan approvals for FHBs is dropping is that, while low deposits are in theory much more possible for new builds than existing houses, the cost of new build townhouses has risen so much over the past 1-2 years that they aren't affordable for many on a low (eg. 5%) deposit.

For example, 1.5 years ago a typical two bedroom townhouse in Auckland in a low-medium value location might cost 650K. A 5% deposit on that is 32.5K. Assuming an interest rate of 3% over 30 years, that's a weekly mortgage payment of about $600.

Fast forward to late 2021. That same townhouse will be selling for circa 850K. Assuming an interest rate of 4.5% over 30 years, that's a weekly mortgage payment of about $950.

HUGE difference.

Plus add in general cost of living increases.

Bang on House Mouse... it just doesn't stack up when you remove expected short/medium term capital gains

Let alone with falling prices.

Especially when you factor in that for the first 5-10 years of mortgage you are effectively paying interest only, your principle repayments are so low.

Sadly not many really understand this. They should ask their broker/lender a simple question - how much of my debt will I have repaid in 5 years, 10 years etc

It would help them realise they are better to rent, put their money elsewhere and save a bigger deposit and buy once prices start clearly moving upwards again... which could be years away

Not many people understand these nuances.

Have you seen anything that aligns with what I just wrote? Can't recall it in any articles.

It spells extremely bad news for the residential development sector.

I haven't... but fingers crossed someone can spell it out in mainstream press as far too many people are financially naive, or you simply don't have the experience as a FHB.

Worse still, assume your calculations above at 6+% interest rates which is the base case of where they will be in 2023.

Just don't expect it to come from the residential building sector, or

Ashley Church - "the Govt/taxpayer needs to stabilise the market and give FHB's their deposit because I said it would never crash"

Tony Alexander - "thousands of kiwi's will come home once borders reopen and buy homes"

Opes Partners - "Here's where prices are rising fastest"

Any Broker "there's never a bad time to buy"

Any Agent "we are still seeing strong demand"

Any Bank "we'll take your life savings and put you in debt for the next 30 years with next to no risk, if you give us your current account so we can clip you with transaction fees there too"

At 6% over 30 years?

Wow - $1120 pw (excluding rates, body corporate, insurances)

For a tiny 2 bedroom townhouse in a low-medium value suburb in Auckland.

Wow.

Just watch the market and development sector tank.

Hey HM, always loved your evidence based arguments. Question: when do you see the development sector really hitting issues? I see so many massive townhouse blocks coming on the market in the hutt, cant see them selling like they did last year so wondering how long would you expect them to last? A key turning point must be when there already sold units under build buyers start forfeiting the deposit

Thanks Kiwi Tim!!! You might note that I have been mentioning this as a looming economic crisis for around a year. A couple of mainstream bank economists (eg. Zollner) have only started mentioning it over the past few weeks.

I reckon the issues are already starting. But I think they will really start biting from July - August.

There's a number of key issues here which I have mentioned before:

- In terms of all the townhouse and apartment developments that commenced prior to say May / June last year and are due to be finished in the next 4-5 months: to what extent do developers seek to abuse subset clauses, to try and get prices higher than those agreed to in S & P Agreements? (given that soaring construction and funding costs will be eating in to their profits). Big call for developers - they would be betting on actually getting better prices. Might be better just to count their losses and stay with the purchaser. This could easily reduce the amount of further developments these developers undertake - so bit of a vicious cycle

- Related point and what you allude to: to what extent can purchasers no longer make their purchase work, through interest rates hikes etc??? And forfeit the deposit

- To what extent might developments be abandoned midway through construction? (this happened quite often in NZ 1976-1977, and in 1987). I don't know the answer, but there will be at least some.

- When, and to what extent do construction starts begin slowing significantly? I think that will start happening quite a lot from now, and for the next couple of years. Which would mean CCC's (completions) would stop dropping a lot in say 12 -18 months. This would mean work for builders, subbies etc would start reducing in the next few months. And as more and more projects are completed, and fewer and fewer projects start, that will lead to more job losses over the period of 12-18 months from now.

- When and to what extent does work for people at the front end of the process - architects, engineers, planners, surveyors - start slowing? I think it will start slowing a lot by June/July. So job losses in those areas starting to show up in the final 2-3 months of the year (there will be a bit of reluctance to let staff go, but it will have to happen)

And of course RE Agents will start getting whacked by all of this.

Just some thoughts!

This could be the case for private development but KO have been ramping up and about to hit their stride, a lot of the work to date has been done by Piritahi getting sites ready for development. If there is going to be some slack in the market seems like a good time for government to pick it up. Up until now they would have been competing with private sector for sites, workers and materials which is not ideal.

All of those parties are going to be looking pretty stupid soon. Reputation-destroying stuff.

Does anyone else feel first home buyers having to cough up over $1200 a fortnight, at a time of extra low interest rates and whilst they are likely to face changing circumstances in the near future with starting a family, a bit scary.

'$1200 a fortnight' - or per week?

Does anyone know if banks are now stress testing at 7% or higher? Surely they should be?

Pretty sure you were the main guy that said rates couldn't rise so not sure why your posting the question. My pick is that rates are going to rise very slowly in the hope that nobody notices, I mean what's a 25bps rise? Probably not much until you get 7 in a row. A frog in boiling water comes to mind.

What a strange - and wrong - comment.

I never said they couldn't or won't rise, it's how much they rise that I have questioned.

Regardless, I recently acknowledged there's a good chance I will be wrong.

Anyway, back to my question. If I am wrong, and 6% really is on the horizon over the coming 6-12 months, doesn't it follow that the banks should stress test at a higher rate?

I thought you told us that youre an economist so shouldnt you know the answer. Or i suppose just lying as usual. Maybe if you come back triggered and swinging I will look up the post

Ouch. 'Lying'. Wow. Some early morning grumpiness FH?

You seem really worried and stressed. You can't handle people who have been predicting trouble with property, and we were / are right.

Maybe you shouldn't be an investor if you can't take the downs with the ups.

Some of us were saying investors should sell up last year, so if people don't listen that's their prerogative. It's not too late though, Flying High. If you sell now you can still limit some of the damage.

So, what have I 'lied' about?

We got a pre approval last month. Stress tested to 6.8% (one of the large banks).

Handy to have the approval in the pocket but would want a deep discount if buying now. There are a ton of developments in my area that are nearly complete and the remaining units aren’t selling, and are already dropping in price. Developers have completely left the market- most properties being sold as ‘developers dream’ etc are sat there with less than 30 watchers. Previously they weren’t even coming on to the market, just being gobbled up.

Thanks NeonLights, an informed view, and interesting to know. Not surprising that it's nearly reached 7%. That will rise and cut more and more buyers out, reducing effective demand.

Sounds like you have a good strategy, I'd be looking for at least 15% price reductions.

Agree re 15%, tbh I’m keen to sit on my hands a bit but keeping my partner onside is the challenge. Thankfully I managed to talk him out of something late last year!

I lived in Ireland during the boom times and visited frequently during the crash. Not everything feels the same but definitely some similarities. Very grateful to have been exposed to it - so many kiwis seem to think ‘property only ever goes up’ is a irrefutable fact in the vein of ‘water is wet’

Do you mind advising the area?

Central West suburbs

Ladies and Gentlemen, the carnage has definitely started: 'Over-committed developer quits'

https://www.oneroof.co.nz/6-nolan-road-greenlane-auckland-city-auckland…

No one's going to save this ship its just hit the iceberg. We pulled out sold in October and are in australia. People are not going to immigrate they will flee for greener pastures and in particular australia. Auckland will have an oversupply by June and the remainder of the country at the end of the year. Come to NZ young teachers or nurses earn 3_9$ less than a tradesman and 1$ more than a fruit picker. Pay 3 bucks for fuel and 1m for a rundown house . When you sell give twice as much to the agent as comparable countries. I'm in QLD sunshine coast bloody lucky we kept our property here i have never seen some many kiwis melbourne and NSW have invaded but kiwis everywhere and most new just jumped on a plane and now they can get home if needed more will flee.

Sharon Zollner, chief economist for ANZ, says the bank expects the official cash rate to reach a high of 3.5 per cent by April.

https://www.stuff.co.nz/life-style/homed/housing-affordability/12811961…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.