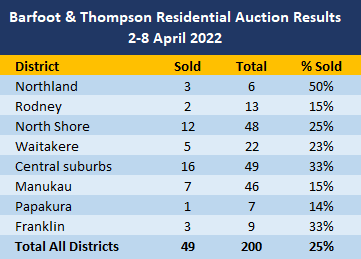

Activity in Barfoot & Thompson's auction rooms picked up in the first week of April, with the overall sales rate also edging higher.

Auckland's biggest real estate agency marketed 200 properties for sale by auction over the week of 2-8 April. That was up from 170 the previous week, and almost matched the 201 properties auctioned the week before that.

Of the 200 properties on offer, 49 were sold at auction, giving an overall sales rate of 25%, up from 21% the previous week.

That suggests the number of properties coming to auction in the Auckland market and the number selling on the day are both holding reasonably steady as we head into autumn.

Barfoot's has nearly as many (194) properties scheduled for auction next week, even though it's a short week with Friday being a public holiday and the start of the Easter break.

As usual there were wide variations in the sales rates around the Auckland region at the latest auctions.

At the main auctions where at least a dozen properties were offered, the sales rates ranged from 15% for properties in Manukau and Rodney to 33% for properties in the leafy central suburbs. See the table below for the district-by-district sales rates.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved are available on our Residential Auction Results page.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

84 Comments

And an expert says "The housing market is unlikely to crash despite........."

25%, that’s probably people just buying and selling in the same market, moving house for whatever reason. For a ponzi to sustain itself it requires the injection of fresh new ponzi dollars.

I'm impressed with the people that appear to get reasonably good bids but reject them. Unsung heroes keeping things afloat.

Ashely Church Interviews Tim Mordaunt and Zachary Smith about their Auction success 6 months ago.

https://www.youtube.com/watch?v=DrHkLv2414o

6 months later Tim gets a summer tan and is asked how the Auctions are going.

https://www.youtube.com/watch?v=r2H8BxDRmDE

7% interest rates this year Guaranteed . -30% Crash is Home Prices a Certainty .

A lot of idle chat from the Doom Goblins appearing today.

As always, beware of their misleading and deceptive (mis)representations.

Judge property on its track-record over many decades - and not on their fatuous words.

When the current market downturn ends and recovery comes, they'll be none the wiser.

TTP

So, you don't expect interest rates to go up further in response to inflation? Why do you hold that belief? Can you explain further?

Don’t expect any rational discussion from him…

Just bizarre that the concept of affordable housing for younger people and creating prosperity and opportunity for them turns a person into a doom goblin (lol)…

The real doom goblins are those that don’t want to create the conditions for younger people to experience prosperity in the country they were born (ie a low wage economy with the worlds most expensive houses).

Many of the young people I talk to suffer from anxiety and depression (let alone mentioning suicides). What I see is that the real doom goblins have already had their way by creating the conditions where young people find NZ to be hellish.

The people who get called doom goblins are those who want to make the future better for young people…not worse. Very much back to front.

That is true. I feel like I’m replying to a spam email when I reply to TTP.

Hi Independent_Observer, JimmyJames & MouseHouse,

Over generations, younger people (and people in all age groups) have bought first homes - which typically has brought them a sense of achievement, happiness, contentment and wellbeing.

It has never been easy to buy one's first home, because houses are always a much sought-after commodity. Nonetheless, many people have succeeded in getting a home of their own - right up to the present time. (In the early-1980's, mortgage interest rates were typically around 20 + per cent, I understand, but people still got into homes.)

A home of one's own is not a hand-out. Nearly always it has to be worked for, savings have to be disciplined and sacrifices made. Education, training and building a career all play roles. That is the nature of first home ownership - and it is unlikely to change.

You three come across as being sanctimonious and holier-than-now. Rather, I believe that one needs to be realistic, pragmatic - and get on with it!

Rewards come to those who work - and not those who whinge and moan. "Nothing without hard work".

TTP

Spoken like the boomer 😈 you are Timmy

Yup. What people who keep banging on about how 'it was never easy to buy a first home' fail to realize is that of course it's never usually easy for any particular person/couple to buy a first home because people tend to buy their first homes as soon as it is reasonably practical for them to do so. They also tend to buy homes at the upper limit of what they can afford. Pretty much no-one waits to buy a home until it would be 'easy' for them to do so. It's a mistake to think that this fact means that inter-generational comparisons are meaningless. There's a big difference between it being difficult but achieveable to buy your first home in you early 20s (as was the case for most boomers), and difficult but achieveable to buy your first home only by your mid-30s (as is the case for most millennials). This is such an obvious point I don't understand why people seem to keep missing it.

All good points - BUT - boomers didn't have the opportunity to:

- travel internationally for the cost of a few months savings

- drive a cheap, safe and reliable car

- have a butt load of labour-saving, life-enhancing and/or entertaining consumer goods

- sell their marketable skills on the global market

...

The list goes on and on. I wonder how many boomers would have chosen to buy that first home if they had all of today's benefits to sacrifice in order to do so?

See all of that is undermined by the fact that I do have a house.

Stay on point, my question was as below

"So, you don't expect interest rates to go up further in response to inflation? Why do you hold that belief? Can you explain further?"

If it wasn't transparent already, covid completely exposed that house prices are not correlated to productivity, they went up when many were not working so don't talk about hard work.They continued to go up because interest rates were lowered beyond emergency interest rates. The past decades you referenced were defined by ever decreasing interest rates, now we are entering a period of increasing interest rates. Why do you see that as irrelevant?

Like P8, it’s a waste of time replying to these trolls.

Just a neutral type observation re interest rates. The intention of Reserve Banks worldwide may to be increase interest rates to subdue inflation but your comment 'now we are entering a period of increasing interest rates' made me think are we?

https://www.longtermtrends.net/real-interest-rate/

This graph show that the peak of real interest rates was in July-September 1981 with a real interest rate of 4.92 per cent, a nominal interest rate of 15.76 per cent and an inflation rate of 10.84 per cent. The bottom of the real interest rate cycle was around 1940 -1949 with a real interest rate outlier of negative 17.49 per cent in 1947 but the majority of real rates being .17 to 1 per cent. The next bottom of the real interest cycle appears to be now.

The interesting thing for me is that the climb upwards from 1954 to 1970 seems gradual and uneventful. So does the period of the downwards sloping curve from 1980 to now where real interest rates are again at their lowest. However the period before 1952 is characterised by wild short term swings in inflation rates and interest rates all the way back to the 1870's. The first sign of a change in this uneventful pattern and a return to the wild swings is - now.

In January-March of 1932 you have a real rate of 3.64 per cent, a nominal rate of 13.81 per cent and an inflation rate of 10.17 per cent. In July-September 1935 you have a real rate of negative 1.20 per cent, a nominal rate of 0.53 per cent and an inflation rate of 1.74 per cent. If those are the types of swings in inflation rates and nominal rates we are in for then perhaps it might be be good to bear in mind that a gradual rise in the real rate of interest over the next 40 years may in the first 20 years be characterised by very wild swings in nominal interest rates if the past is any guide.

We may have seen the end of the Bretton Woods interest rate regime from 1954 to 2020 and be going back to the neo-classical dramas of the period pre 1954.

Interesting graph. Have to go back to the 70s and 80s to see negative real Interest rates like now. We need a Paul Volcker to steady the ship and up those rates, although there is too much debt in the system this time. Interesting times.

Trolling The Poors.

It's never been easy to run a marathon either, but try telling that to someone who has climbed Mount Everest.

The problem is, we have a bunch of people lecturing the current generation about running a marathon, when it turns out the current challenge is climbing everest and the people doing the lecturing only ever ran a 10k.

Wellington's red-hot house prices are finally cooling ... why, then, is no-one buying?

House prices, accordingly, have dipped – by 1.5 per cent during the last quarter, according to valuation company Quotable Value, with claims that some sellers have lowered prices by up to 20 per cent.

Beth Coughlan has a phrase of her own: “quite disappointing”. At the start of the year, the Coughlans listed their first family home, in the Lower Hutt suburb of Naenae, for enquiries over $859,000. No-one was interested. They dropped the price to $815,000, then $759,000 and, now, earlier this week, $699,000.

https://www.stuff.co.nz/life-style/homed/housing-affordability/12829503…

"As always, beware of their misleading and deceptive (mis)representations. "

https://www.stuff.co.nz/business/91418098/property-brokers-manawatu-and…

Oh poor Beth. They're sub-dividing, it was originally a 600sqm piece of land. They obtained a consent in February this year to put a detached dwelling on the rear part of the section, hence the property now has 300sqm of land. Probably still asking the going rate for a 600sqm property which is why nobody wants a bar of it.

Time To Panic

Too late for The Penthouse.

Houses auctioned December 4th 2021: 368

Perhaps conditions for auctions as a marketing device have turned.

May be 25% selling are those where vendor is realistic as RE agent says to meet the market

Strong demand for sections is increasing prices of land throughout the country.

https://i.stuff.co.nz/business/128282713/section-prices-rise-across-the…

Give it time and they will go the same way as houses 👇📉

Sections are often priced at last quarter prices and we are seeing sections sit on market for the first time in a couple of years,” Dredge said.

Yes, it will need to. Land being the key component that could reduce price.

Also,

"Part of this increase can be attributed to the increase in vacant land which is now zoned for multiple properties, as opposed to single dwellings,” Goodall said.

It's great that the expansion of the housing supply has been incentivsed due to zoning and interest deductibility remaining for new builds. Hopefully this will add more downward pressure home prices.

The only way house prices are going to come down under the present system is if someone else takes the loss. Which is what needs and will happen.

There is going to be tears. There are a lot of people out there who bought into the hype of the housing ponzi and jumped in without due diligence, believing the generic RE agent and media waffle that the housing market is different, bricks and mortar is a risk free investment etc. Paying crazy money in places like Palmerston North, simply because houses were ‘relatively’ cheap there is just insane.

Those that have made terrible financial decisions based on terrible financial advice are going to have to deal with the consequences, no one else.

The likes of Ashley Church and Tony Alexander have an awful lot to answer for.

Come on now - this is not a crash, it's a correction. *smirk*

Dr Doomfield joins the Church Of Ashes, can I get an Amen ? The narrative of the Paid To Say Brigade is going up in smoke. It must be truly exhausting to peddle lies and fear to the gullible for your master. And I guess it has taken its toll. Not to worry , the team of $50 million MSM will give him the well orchestrated send off he does not deserve.

For those Church members who have given diligently to the belief that interest rates would stay low for a very long time, and that the MSM tell the truth, we would ask you to join us with the 2 Ashley's for a very special Sunday Service at the Church Of Ashes.

Everyone knows that they both represent Real Estate industry so are just doing their job as lobbyist are suppose to do.

We could be talking quite large losses too. In the old days being negative 30k was pretty bad but now it could be something like 200 - 300k. It would take a long time to save that much money.

It's simply finding out that leverage works both ways yes. Who knew.

simply because houses were relatively cheap there is just insane

Most regions in NZ are undergoing quite a bit of population growth whilst lacking a decent sized construction force to build enough dwellings.

If you're talking about due diligence.

Low Auction sell rates are not all bad news for the Real Estate industry, after all the second string to their bow is as an advertising agency, so they are paid the advertising money regardless.

The homeowner, on the other hand, has not only found out what their property is not worth, but is approx. $5,000 lighter in the pocket to find that out.

More like only $1000 down for the auctioneer's fee.

It's interesting studying some of the 'passed in' properties. Last Wednesday's Auckland City auction has a house that was bought in 2020 for 2630k pass in at 3000k. 370k for holding onto a property for two years seems like a good deal but they want close to a million more than that. Another was bought in 2014 for 1100k but they turned down 2375k and another bought in 2012 for 626k turned down 1240k.

The last decade has seen people lose sight of the value of money. It's like one million is the new 100k. Probably time to put an end to this malarkey. Hold onto a property for two years and receive enough money to buy 40 brand new cars? Something's gone badly wrong.

Yes, i am personally starting to lose confidence in $

Indeed. Greed has no correlation to being smart, or reading the correct tea leaves. Watch the debt wreck unfold over the next couple of years.

Went to a couple of open homes last weekend for giggles. Dead as a donut. When the Agent called and asked my pricing thoughts (their job), I indicated much closer to the old CV, not the new one.

Silence. "I wont even pass that on". My response was "it will be less if you call back, I can wait".

Everyone else should as well....

But this always has to be the outcome when house prices rise far higher than wage inflation for a long period of time…the only way that it was possible to keep that trend going was to continue to decrease mortgage costs.

There are no free lunches and in the end any asset price is only a reflection of the sum of the discounted future cash flows. We decided we wanted to increase asset prices in the short term by reducing the cost of debt/discount rate using an artificial market externality (QE). That isn’t a real market..it isn’t sustainable…it’s living in lala land where you think you can beat the laws/principles of finance.

Very well put.

It's called Anchoring - Daniel Kahneman is an expert in this area. Once people have a number in their heads, it's very hard to get them to accept a lower price.

Also while the potential buyers have a low number in their heads with a crashing market like this , then its almost imposable to get them to accept a higher price.

Its not just a number in their heads. Typically house sales are a "Chain" event. Sellers more often than not find their next house and go conditional on it and therefore know the price they are paying and then this reflects the cost of what they are selling. Pretty simple they can get into a position where they simply cannot accept a lower price. I have always been in the position of either renting or flatting and hence have never been put under self imposed pressure to buy, its the best position to be in.

Renting or Flatting is the best position to be in at the moment. Even if you can buy a house with cash.

2022 is it good sitting on cash that is losing value by the day? If the crash is as big as you say, the cash could also be at risk sitting in the bank.

"Cash" could include shares, precious metals, bonds, classic cars, lots of alternatives to bank deposits.

No its not. Off to the auctions this coming Wednesday with the intention of buying a house. There is never a bad time to buy if you find your dream home.

Sometime not. A couple we know have bought and paid for the new bigger home in Dec last year. They took a short term interest only loan on the lot while they prepped to old house for market. This took longer than expected with xmas, trade shortages etc.

They want $2.2m in a location that is now most likely $5-700k under that now. Failed to attract any interest at auction last week. Interest only expires next week. At that point they will be unable to meet PnI payments.

What happens then...?

They should probably put the big new house on the market ASAP.

I bought a house before selling the current one. It was a very stressful time needing to sell at auction and settle on the new one on the same day. I wouldn't do it again. However it is often quite disastrous to sell and rent while looking for a new house. Maybe not today but these times are relatively rare.

The last decade has seen people lose sight of the value of money.

Absolutely and that is a huge part of the problem. Everything is on tick, buy now pay later etc which is a great marketing ploy but terrible for societal views on money and debt. And as humans do, we can’t do things in halves, we drop thousands on worthless pot plants on Trade Me, buy European cars that cost thousands to service and make offers on houses simply to ‘win’ because we can just go and borrow more right? Wrong!

More confirmation prices are crumbling with interest rates and inflation set to climb only way is down, just how far I would suggest it will hit bottom when average wage earners can purchase a house.(so a long way down)

When does this lead to people not settling on new builds?

Might already be happening as there are weekly news reports of developments going into liquidation

Well they probably want them built before they settle!!!

Follow off the plan section subdivision developments. People are already failing to settle. Or choosing to not settle.

Why follow through with a 600k postage size section settlement when it will be worth 1/3 of that soon ? Sections always fare the worst in a Crash.

Who cares if you lose the 10% deposit . You still save 340k. It takes a long time to save that, especially if its borrowed money at ( 7% ).

Property Brokers lose there contacts with developers because they keep most of the 10% for themselves and leave the developers with often nothing, the developer usually does not know this until its to late.

I wonder what price these sections will sell for in 12 months time ? There is a glut in unsold sections already on the market. In the last GFC sections in the same area were dumped by a similar size developer for 60-80K , and the sections were bigger.

https://landsdale.co.nz/brooklands-estate-hawkes-bay

Your a dreamer 2022, you will not last the year, Oh wait only eight months to go.

Property Brokers will not keep the listing for the year, or eight months. But 7% interest rates will be here well before that.

Got some sections to offload or sell for someone else Carlos67 ?

Tough Times Ahead.

You make it sound like they have a choice or not to settle. They don't.

If any developer has, so far, allowed a purchaser to cancel and only lose all or part of their deposit, then that was entirely at the discretion of the developer. And they normally only would do this if they know they can on-sell at a higher price and make more money doing this.

Otherwise, the purchaser will be made legally to settle by getting sued for specific performance. It sounds like there is a reality check coming for many.

Don’t you think there’s much more risk for developers than buyers, in general? Won’t banks typically be honouring pre-approvals, or do you think they increasingly won’t, if prices continue to decline?

Banks don't offer confirmation of any pre-approval, generally more than 3 months prior to settlement. They can outright turn you down or may change your terms like lending you less, ie you have to come up with more deposit.

None of that is the developer's concern. Irrespective of whether you have bank funding or not, you will be required to settle. And the developer's lending conditions with his bank will require him to take all legal steps to show that the developer made every effort to get you to settle, ie to bankruptcy if required.

Money will need to be diverted from other assets, or other things that you would or need to spend money on so you can settle, so on the stats. it will look like the housing market is trucking along ok still, but you won't see the frantic amount of effort required to feed that debt.

One thing you can be assured of, the banks will be the last to lose any money, in fact, normally make record profits.

The pre approval I got back in late 2018 for an off the plans purchase was for 12 months. Are you suggesting that is rare?

I would have thought that would be standard for a new build? After all, most people who put the deposit down for a new build won't typically be settling for 12-18 months, to allow time for the development to be built.

I've just looked at that pre-approval of mine, and I do note it was subject to a number of conditions, including change in interest rates, and requiring a final valuation upon completion of the house and prior to final approval and draw down of the mortgage.

I guess if interest rates move from say 2.5% to say 5% during the construction period, and the valuation of the house following completion was down 10-20% on purchase price, the bank might not go through with the transaction??? How likely is this, though? I would have thought they would still go through with the transaction if the purchaser is not in negative equity, and if they can still afford to pay the mortgage at 5% versus 2.5%.

Yeah it's usually 12 months preapproval. It depends how the builds being done as to what the bank will do. Obviously 'turn keys' where funds get drawn down on completion - the bank could easily pull out vs a build loan which funds have been drawn down in stages ... If the bank's already lent out money, they'll want the build completed.

Maybe we are talking at cross purposes, but the question is, what happens if for whatever reason the bank won't advance you the funds when you have already have gone unconditional on a property.

You will have to settle come hell or high water. Just wait and watch.

You cannot get Blood out of a Stone. The developer can chase the purchaser, yes, with lawyers , and that is expensive and time consuming. When markets crash there will be little or maybe no equity left in the Purchasers assets to even chase.

If the Developer has not got the title in time according to the contract then he is shit out of luck.

Banks can become extremely difficult to deal with if the Interest rates are rapidly rising, prices are crashing, asset equity is disappearing and settlements seem long.

Banks don't like sections because if it all goes tits up - the bank can not rent it out.

Banks only lend a small portion for sections compared to a House, ie more equity is needed, if it has not already evaporated.

"One thing you can be assured of, the banks will be the last to lose any money, in fact, normally make record profits." And thats why they will find every excuse under the sun to not lend 600K for a section that will soon be worth a fraction of the Over valued asking price.

You cannot get blood out of a stone, and the bank is on the side of the purchaser .

Yeah and I think that speaks to my point that generally it’s going to be worse for developers than purchasers, although it won’t be nice for purchasers who settle and are in or close to negative equity upon settlement. But shouldn’t be a big deal if they are planning to be in the home at least 5 years.

Again, like House Mouse, you are talking at cross purposes. If the purchaser cannot or will settle they will get sued for specific performance.

That is different than if the developer reneges, but then it does not automatically mean the purchaser can pull out as if that happens then the bank becomes the new owner and may pass the property on to someone who will complete, so the purchaser is still on the hook to settle.

This pattern is more prevalent in new subdivisions and apartment sales.

But if you haven't seen how much blood there really is in a stone, then you haven't been involved in developer or bank settlements before.

"If the purchaser cannot or will settle they will get sued for specific performance." - Yeah, we covered that. If there is no money because assets have devalued due to the crash then there is nothing to get. No blood in stones.

"That is different than if the developer reneges, but then it does not automatically mean the purchaser can pull out as if that happens then the bank becomes the new owner and may pass the property on to someone who will complete, so the purchaser is still on the hook to settle." - If the developer does not get the title in time then the purchaser can walk.

"But if you haven't seen how much blood there really is in a stone, then you haven't been involved in developer or bank settlements before." - you clearly have never been a property developer.

Well, I have, and you really don't understand how it works.

For some people, the lesson best learned is the one hardest learned.

If a purchaser truly cannot settle, they will discover that 'truth' when they get sued for specific performance, followed by bankruptcy. That's how the system tests whether you really can't settle. You will have to excuse them for not taking your word. Plus the banks have their underwriter's obligations to adhere to.

And the developer or bank if they take over the loan, has a process that can take years to supply the title. Of those developers who have already gone bust holding purchaser contracts and their deposits, how many of the purchasers have had their contracts canceled and their money back?

Here’s one from the granny herald today.

https://www.nzherald.co.nz/business/darcy-ungaro-property-house-prices-…

The social damage if this goes pear shaped is going to be disgusting.

Paying to read a MSM Granny Herald article is never going to happen . I would like to have known what they had to say though.

It's a soft paywall - just disable javascript for the site, or get one of those chrome extensions like freemium, bardeen etc.

Townhouses in Auckland on TradeMe at 453 tonight, so listings only about 5% higher than 3 weeks ago when I first started monitoring. Will keep tracking, will be interesting to see if it moves towards 500, or not, as more and more townhouses are finished over the next 3-4 weeks.

Napier was 250 on the 27 Dec 2021. Now its almost 450 listings. Thats a very big deal. And the speed of listings increasing per week is accelerating.

80% increase in less than 4 months.

What was it in December 2019?

Most areas I'm watching are only just getting back to those levels after 2 1/2 years.

It's funny on interest...

When house prices go up 40% "it's just paper gains, it doesn't matter until you sell but likely you'll still have to buy in the same market"

When house prices go down 1%-5%"it's all over, it's a crash! House owners paid too much and they're going down! They should of rented instead.

^^^ ✓ :)

Theres always two extreme ends of the spectrum.

But to ignore the macroeconomic headwinds that is clearly brewing is not wise either, akin to the wallstreetbets apes whom keeps screeching

gme/amc to the moon...

just here for property bull comments on the way down

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.