The housing market downturn appears to have reached a significant milestone with prices in Auckland's leafy inner suburbs and all of the Wellington Region now lower than they were a year ago.

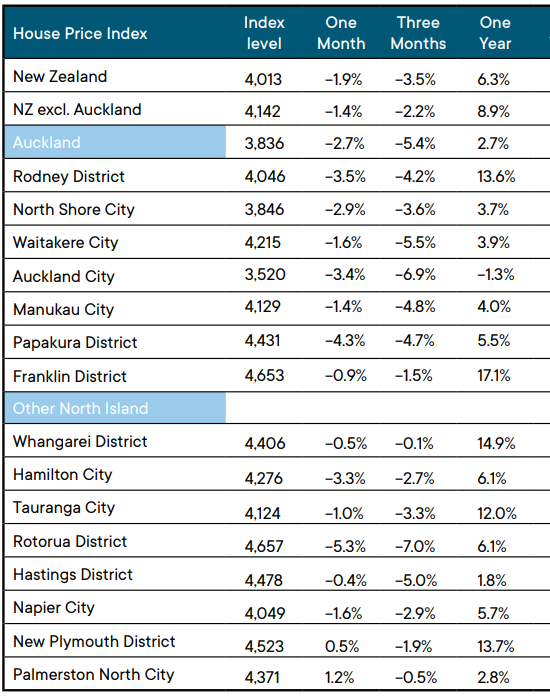

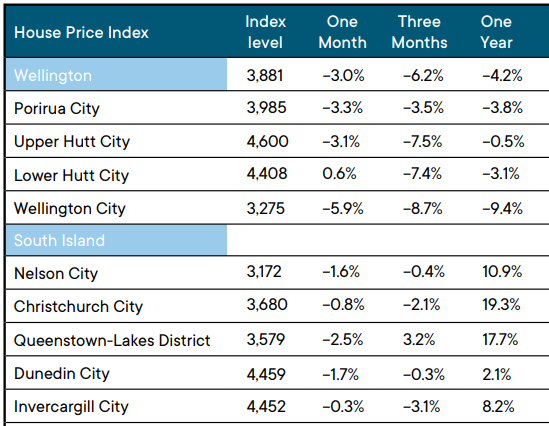

The Real Estate Institute of New Zealand's House Price Index (HPI) declined by 1.9% nationally in April and is now down 3.5% from where it was at the start of this year.

The HPI gives a more accurate indication of overall price movements than either average or median prices, which can be affected by changes in the composition of sales each month.

Of the 24 districts around the country tracked by the HPI, prices were lower in 23 of them in April than they were at the start of this year.

The only district not to record a decline over that period was Queenstown-Lakes, with the Index up 3.2% in April compared to January.

However Queenstown-Lakes may also be at a turning point, with prices in April down 2.5% compared to March.

The slide in prices has been particularly strong in Auckland and Wellington.

In the Auckland Region the Index declined by 5.4% between January and April with the declines within the region ranging from 1.5% in Franklin to 6.9% in the central suburbs, which includes some of Auckland's most expensive real estate.

The central suburbs are also the only Auckland district to record an annual price decline, with the HPI for the district 1.3% lower in April than it was in April last year.

In the Wellington Region the HPI was 6.2% lower in April than it was in January with the declines over that period ranging from 3.5% in Porirua to 8.7% in Wellington City.

On an annual basis, the HPI for the Wellington region was down 4.2% in April compared to April last year, with the annual district declines ranging from 0.5% in Upper Hutt to 9.4% in Wellington City.

Outside of the main centres the biggest declines in the HPI over the three months to April were in Rotorua, down 7.0% and Hastings down 5.0%.

The table below shows how the HPI has changed in each district over the last 12 months.

The comment stream on this story is now closed.

REINZ House Price Index - April 2022

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

181 Comments

But those price falls only put us back to October last year!

Oh wait...

O CWBW, CWBW, wherefore art thou CWBW?

I have to say, I almost miss him.

Pray for the welfare of the boys in the basement who might have got the numbers wrong.

Good 'ol CWBW will be rousing his boys (and girls) to the MAX ! for all those open homes this weekend ! ....SELL SELL SELL !!! .....BUY BUY BUY !!! ......bye bye.

The pendulum is swinging back, price drops will accelerate in coming months each rate hike and inflation pressure will just increase momentum. What can stop the housing market from falling? Everything is pointing to huge losses over next few years.

ANY house price increases in 2006 were wiped out by the downturn in the market over the past 12 months, a new report claims. ...

Despite also predicting a 4pc slide in property throughout the city and a 3pc fall elsewhere, IAVI president Robert Ganly was relatively upbeat about the coming year.

"Overall, I would say to people that the market is beginning to stabilise. The worst is over," he said.

Robert Ganly, January 2008.

https://www.independent.ie/irish-news/property-price-rises-wiped-out-by…

"The worst is over".....reminds of TTP saying the market is resilient (when it appears very fragile and vulnerable).

As in ALL previous market downturns, those who don't sell will prosper in the next upswing.

TTP

Spelling corrected.

As in ALL previous market downturns, those who don't sell will proper in the next upswing.

When you say proper, do you mean properly ruined?

I've talked to a few people in Japan....they're still waiting for their post QE upswing from the late 1980's. That is a properly long time.

Clearly the correct spelling is Prosper. Sorry cannot change it I'm not TTP.

Thanks Carlos.

Clearly, Independent Observer hasn't got much to do with himself these days.

TTP

As in ALL previous boom cycles, those that were too greedy on the way up, suffer the most when the market turns and they are left holding lemons (erm… waiting and praying for 15+ years until the start of the next upswing)

The Penthouse Palmy has been listed since August 2021 - when everything in town is selling like hotcakes.

Auction in Sept - Vendor wants $850k - doesn’t sell

Tender in Jan - Vendor wants $800k - doesn’t sell

Now listed as ‘Seriously for Sale’ - $750k

https://www.trademe.co.nz/a/property/residential/sale/manawatu-whanganu…

Seriously for sale? - is it even worth half what the property guru wanted with his original asking price of $850k - would you pay $425k?

Let's be like the other property gurus/coaches Opes Partners and do the numbers:

$425k purchase price, with rent of $500 per week (the highest 2 bed in Palmy on Trademe is $570pw).

A $425k purchase price would give a gross yield of 6.1% - less op ex such as body corporate, management fees etc and you would be lucky to gross a 3% yield.

Residential property investment doesn’t stack up without capital gains, everyone knows that... you don’t need a Opes Partners spreadsheet to work that out.

But poor fools that believed it was a one way bet.

#talebsturkeys

Weren't they serious before? Was it a joke? Because it WAS a joke

Chance that's a leaker, too

yeah... the way things are acting at the moment.

that next upswing could be 10 years out... best to keep an open mind right now.

Famous last words!!!

Suck on that, lords of the land.

I hope you will find peace

As a landlord this does not affect me, the properties I own are not for sale.

I am thinking of the hard working builders and developers, this is actually going to hurt them most.

This is not about you personally. Its about all landlords vacuuming up homes our young should be owning and living in.

Landlording in NZ is a disgrace, an abuse of our young and something you should be ashamed of participating in.

Yeah, lets get rid of all landlords. Renting a home is to be outlawed. Houses are to be handed out to everyone as soon as they turn 18.

Your comment shows just how much you love the status quo: https://www.macrobusiness.com.au/2022/05/new-zealands-housing-system-eats-its-young/

What do you mean? I don't like the status quo, I want all houses to be free. Handed out to everyone when they are 18. Is that happening now?

Strawman.

Ooooh do they get handed out too?

Well we could just introduce and enforce DTI's. Overnight it'll weed out the crop of marginal landlords who only gain property through leveraging paper, the dunning krugers who have little clue and tend to outbid/displace aspiring FHB and ultimately (in a round about way) end up renting the properties back to the very FHB that would have bought them to own.

DTI's , no IO loans , continuation of removal of mortgage interest deductions ,3 simple things which will prevent a run away market again.

Your rules would benefit the majority and improve financial stability. The problem is, those making the decisions also own investment properties and therefore have clear conflicts of interests. Hence they claimed that all the settings should remain the same and all that was needed was more houses.

DTI I agree with, no Interest Only loans should be allowed in certain circumstances like bridging finance, or revolving credit that allows you to pay off your loan faster, but otherwise I agree. I think interest deductions are a reasonable expense, and should be claimable, they are claimable for every other business (not I don't have a mortgage on my rental so doesn't effect me in the slightest financially). I do however think if you continue borrow so that you never make a taxable profit, you should be charged capital gains and it should be retrospective, since the law has always been you should be paying tax that if your intent was to make a profit the sale. What sane person would run a business that never makes a profit?

There needs to be some rentals in the market, despite what rastus thinks.

Do we need to regulate so we have better landlord with healthier homes, yes.

Do we need to regulate so we have better tenants who are respectful of the homes, also yes.

I don't think there would be much correlation between leverage and quality of landlord (although there is probably some).

The $1 million question is: How many rentals do we truly need?

Also: How many rentals will we need if house prices are 20% lower?

Plenty of work for builders at the moment. Hopefully in future government will keep them busy with building projects for homes for them to rent out for people who cannot afford to rent privately.

If the govt had any brains they would be buying out any developer that goes under and cost price of land & materials only and keeping the builders on to finish the jobs. Then completed homes go into the state housing pool.

Builders have job security, developers get punished for over leveraging, govt gets cheap state housing.

Yawn…been here before.

Doubt it - what period of history are you going to compare this to?

Nobody has ever witnessed or been part of the situation we currently find ourselves in.

I just want rid of this Government. Every financially hurting voter is good.

Do you think that 7 houses Luxon will improve the housing situation for the majority or just the investors and landlords?

Couldn’t be any worse than this lot. My wife is at an education conference up North. She has been in tears at some of the stories. Meanwhile, we have personally never been better off. Our children left for overseas in the last two months to look for opportunities. NZ is a nice place to retire to. Thanks Labour.

Now you're discussing education not housing. On that we may agree. If Luxon stood up and said education, education, education. I might give him a second look. Unfortunately politicians tend to send their kids to private school so there is not a lot of incentive for them to improve the public system. I would love to know the number of MPs who attended a school of decile 4 and below. It is the poor that are under represented in power.

Even Willy the working class hero sent his son to Kings.

-

Quite obvious which parties MPs have benefitted the most from the housing frenzy.

I'm not getting into a political debate but the other "potential government" would have done exactly the same thing. Don't blame Cindy and co. Aotearoa is just a piss ant on the global scale, we are just doing the same as all the other OECD countries. It wouldn't surprise me if Adrian Mole (orr) has a direct phone line to Captain Biden so that he can receive further instructions.

Hardworking builders x developers.

Crocodile tears.

They been on a stroke for awhile now . Be good to have suppliers x tradies to get real .

So bitter...hopefully you also have something positive to focus on in your life Fitz

If you annualise some of that 1 or 3 month data, and assuming the trend continues, then there could be some serious drops in prices by the end of 2022.

Rotorua down 5% in a month....Wellington city 5.9% in a month....

It will only take 6months of falls like that and add in 8% inflation and you are looking at a significant decline in the real value of those assets. Perhaps the biggest we've ever seen in the NZ property market?

Don't be concerned IO .....our resident spruikers will be along shortly with their "soft landing" BS and residential property investment only goes in "one" direction, no matter where the market stands, according to the nice lady who keeps telling me on the radio ....the greed and "self interest" out there is just phenomenal !

residential property investments only go in one direction.

The direction depends on whether you're a "spuiker" or a "DGM"

What are you then - spruiker because its in your best interest given you property investments and risk profile?

I don't really know. House prices go up and I'm validated buying the investment property because it'll be impossible when my kid (soon to be kids) grow up. House prices go down and my kid(s) will be able to afford a house when they grow up.

I'd prefer the latter because I think it gets more people into the housing market, although that is arguable. If prices crash like the DGM's are braying for then it'll be recession which means FHB's probably won't be buying as having enough for a deposit is one thing but no income is another. Also astute investors will be buying up large once the market turns at (or near) the bottom.

Either way it makes no difference to me. I re-did the budget, looks like I'm on track to be mortgage free (on OO) by 39.

I guess I, unlike some, can truly say I am an Independent Observer.

Hard putting things into binary buckets isn't it...as opposed to a wide scale from which we are all jumping across different points with different biases and heuristics.

sure is IO, we all carry round baggage...my folks grafted a lifetime, got comfy but refused to be landlords in principal so I inherited that...others grow up with property investor parents who think its OK, in a recent house and garden a mum is waxing lyrical from her architect designed kitchen how marvellous it is to watch her kids riding their ponies as she cooks dinner... those kids will go to flash schools and develop their own view of how we all have the same opportunities...

I worked through the gfc in London. As a contractor in FS. The whole economy was in meltdown and I still found work. A recession ain't so bad.

A reset in prices will help in the long run. Though there will probably be another boom before your infant child is in a position to buy anything =)

I'm a so called DGM but even I wouldn't dare extrapolate monthly changes to half a year or more. Still, I agree that monthly drops of 5% are a very clear signal. Now let's hope RBNZ doesn't do something stupid again to take "the path of least regret"...

Yes agree....hence the use of 'if' and 'could'.

As opposed to statements used in certainty by property bulls who say without a doubt that 'property doubles every 7 years'.

Don’t worry. Ashley Church says you can predict the future by looking at the past. It hasn’t happened before therefore it can’t happen now or in the future. He said so on the one roof radio show last week.

I apply the same principle to driving and while my insurance premiums might be a smidgeon high I consider my driving ability to be far greater than all these forward looking muppets on the road.

He's like the Anti-Taleb.

If nominal prices for Wellington fall 5.9% for 6 months that's 30% down.

by Nzdan | 11th May 22, 6:04pm

They will decline as much as interest rates increase, where servicing is maintained at current levels. It's purely a numbers game, anything else is just trivia.

e.g. Calculated on 30 year mortgage:

- $800k mortgage @ 3% = $778 per week.

- $550k mortgage @ 6% = $760 per week.

30% drop in borrowing power. Maybe compensated slightly by wage inflation. But then what's a loss in sentiment worth?

"If you annualise some of that 1 or 3 month data"...Wellington city 5.9% in a month"

Yep that's 70.8% down annualised for Wellington, but wait! There's more… that's 141.6% down in 2 years, 212.4% down in 3 years! Imagine that, what a bargain!

I hope that you find peace.

Thank you Fitz, Bali was very relaxing!

Did you help the Bali locals pick up some of the garbage & detritus littering the beaches,seen some pics lately,looked a bit of a mess.

I do actually often pick up rubbish from public area everywhere, be it Auckland, NZ, Bali, Europe or anywhere at all, as I consider that I partly own these public spaces, together with anyone else : )

That reminds me of when they were talking 2 years ago about the banks paying us to borrow money.

I know youre being facetious but for anyone interested if that trend continued an annualized 5.9% monthly decrease becomes a 48.2% decrease.

8 upvotes and nobody checked the math, it says a lot about the kwality of the comments section.

FYI: It wouldn't be a 48% decrease, it would be worth 48.2% of what it was originally, so 51.8% decrease

Okay but a few percentages either side of 50% is the significant takeaway surely?

Math doesn't seem to be your strong suit. If prices decline by 5.9% each month it would in fact be down 30% after 6 months. If prices fell by 5.9% per month for 24 months they would be down 76%.

Well, it's actually 88% down in 3 years.

There is a calculator here Yvil if you want to run some numbers:

Annualized Rate of Return Calculator (valuespreadsheet.com)

Thanks to all the people's help, who really thought I was serious about a 200+% drop in a few years, LOL.

I was actually just exemplifying how silly IO's suggestion is to "annualise a monthly loss".

Why? Does it appear to ugly to be considered possible? We're not even officially in a recession yet, and unemployment is at record lows....imagine what might happen if people start losing jobs and credit expansion to the property market stops in its tracks.

Credit expansion has already significantly reduced.

No you are making yourself look silly. His calculation of 30% extrapolating 5.9% over 6 months was the correct math. It wouldn't be down 5.9 * 6 (i.e. 35%, as per your math). Jog on.

LOOOOOOL GUMMON GUYSSS I WAS TROLLING IT'S JUST A PRANK BRO

Market corrections do often last a year or two, with periods of acceleration and/or plateaus so it’s not entirely insane to look at the momentum of monthly price decline and extrapolate out to a year. .

The NZ housing market is nuts, and we’re all here wondering what the hell will happen. Speculating what monthly declines would look like over a 12 month period is not a hard science obviously but its just part of the context to consider.

Good to see ol' Palmy holding the fort there with a 2.8% pa gain TTP .....got anything you would like to sell me at a 8% gross return ......do the numbers and we could have a deal :)

I still think his username is a typo. Should be TPP, The Palmy Penthouse.

or Troll Properly Poleaxed

Time To Panic.

Lots of staff on the books not bringing in sales.

If I had property in Palmerston North, I wouldn't be selling it.

PN's future prospects are A1.

TTP [CNZM]

Still better than stocks though and don't mention crypto....

Two important differences:

1. Leverage,

2. Mortgage.

Usually people buy crypto and stocks with money they have, with no leverage. So when sh** hits the fan, they only lose the money they had. Whereas with housing, it's easy to lose a lot more than what you started with.

A 10% fall on the stock market will erase 10% of your money.

Assuming 20% deposit, a 10% house price fall will erase 50% of your money. A 30% fall will erase 150% of it. Plus what you've paid as interest.

Correct. Leverage is bi-directional. Just because it hasn't work in a negative way for quite a long time, does not mean it cannot.

Only if you panic sell of course. With no leverage and dividends still flowing, sitting it out not such a biggie.

I theory leverage is bad in practice not so much since you can go bankrupt.

TK, you are obviously in the group that owns multiple properties ......has taken advantage of the very recent low interest rates ......particular tax breaks 'custom made' for property investors ........already having leverage, you would of bought much earlier when prices were reasonable.....being able to 'flip' particular properties and in a market, even if taxed, gave a handsome return .......rents ever increasing ........etc etc

Believe me, as a true capitalist in business, you have done well and I respect what you have achieved.....however, if there was one thing that totally "distorts" this residential property market and it is not of your doing, and that is the Accommodation Supplement.

For a small business, which is basically what you are, why should you provide a service to the marketplace, that some consumers can not afford , so have to be topped up by TAXPAYER money, by way of the AS, that goes straight into your pocket (or the banks)

I believe in a "true" free market and had the NZ residential property market had one, with no "interference" from central banks, government etc, this mess (which will only get worse) could of been reduced or avoided.

I truly hope this property market "settles" right down and more resources, labour, R & D, capital etc can be put into the NZ economy to create new opportunities/products/services, while promoting "true growth" for everyone - not just an ever decreasing pool of multiple residential property owners.

Great post - as I've said in the past, if we were to remove the accommodation supplement tomorrow, you'd likely find that it will be property investors who whinge/complain more than those living in poverty and who are reliant upon it to pay rent to the landlord class. That is because they have everything to lose from it, while those living below the line have nothing to lose at all.

Sure the landlord could throw them on the street - but then who are they going to find to replace them with? Another person living on the street who also can't afford 'market rent'?

My son is at Vic Uni in Welly,a couple of years ago either a student allowance or AS(can't remember which) went up by $50,almost immediately, the going rate of rentals went up by $50..."thanks Mr Taxpayer,we'll take that thank you..."

Yes and then the increased cash flow pushes up the valuation of the asset.....basically using taxpayers money to subsidies property investors and creating financial and social instability.

Just like how the increase in interest rates has an impact on cashflows, pushing down the valuation of the asset.

Yep, then landlord has $50 extra free money to spend every week. Why are we getting inflation again? Hmm...

CH, I've been pro capital gains tax on property since I've been commentating on here. I'm not tin-eared about affordability and Maori are some of the most adversely impacted.

There is a role for residential landlords, I used them for some time. My point is that crypto and stocks have fallen more than housing - so relatively its not performing that bad. I do expect prices to fall harder though.

Trying to compare assets that can be bought and sold near instantly and prices move quickly, with property, where transactions are considerably slower and costly you can't really call that "property has done better" this early.

We can clearly see that, while prices have fallen a relatively small amount, the backlog of unsold properties and falling sales rates signals that sellers expectations have not caught up with what the market is willing/able to pay. It will take time for prices to adjust.

And then of course the issue of leverage makes the world of difference. Those that have leveraged up, a 10% drop is price is far more significant than people who bought shares with their own money.

To me this is the a counter low/medium income earners don't pay their way in tax, what happens any money the poor get goes straight back into the pockets of the rich. Property is just one example.

How about One News last night. Lead item on the property prices. Talk about trying to put a positive spin on things. More like an ad for the REINZ than a news item.

So I'm not the only one who noticed the "8% annual property price increase".

Two more months and they won't have anything left to say.

REINZ did that on their twitter yesterday also....sure its true, but its also very misleading.

They'll simply zoom out - "x% increase since covid hit :)"

OneNews has hardly any more substance than the Womens Weekly.

Populist tripe - news as so-called 'Entertainment'.

Call me old school - but deliver the 'real news' in 30 minutes max, no gimmicks just professionally delivered.

I'm not interested in a story about a cat stuck in a tree in Eketahuna, FFS.

The real question here is what was the equity people used as collateral for the Loans on these investment properties? If the underlying collateral falls in value, then you can find yourself in hot water very fast. And with everyone exiting the market all at once, no one is going to buy except at bottom prices.

Also how much fraud has been going on? The bank of mum and dad stuff was considered fraudulent and a sign of an unworthy borrower in the past but that changed as soon as the suckers (FHBs) were struggling to pay, so how many marginal borrowers with dodgy books have purchased houses as a store of value and now are totally broke?

Something is rotten in Denmark and it is clearly coming to surface over the next few months.

This screenshot I took in 2019 might answer some of those questions (read the two top comments):

Just your typical kiwi borrowers. Based on the popularity of those comments, this mindset is actually celebrated instead of being taken as a HUGE red flag.

I can’t believe that people were allowed to plunder their retirement nest egg in order to buy a house. I am not celebrating people going into financial difficulty, but there is some relief that the madness that drove the prices up to such ridiculous levels may finally be over. Someone with an $85000 income should not be borrowing more than $340k in my opinion.

Before the CCFA some of the stuff the mortgage brokers got through was criminal.

I know of people on two full time minimum wages (circa 80k a year combined) who have almost a million in mortgage debt.

Eeek. Refix time is going to be naaasty.

If you care for them, get them to sell asap. The sooner the catch the falling knife the better as it will end up somewhere else come mortgage re-fix time.

Holy crap, we are more than 3x that income and wouldn't even think about a million dollar mortgage. What have people been thinking?

Well, probably they're thinking that they want to own a house, because society as a whole says this is a good thing, and they lack the skills to understand the decision beyond "the bank will lend so it must be ok".

Yes and you'll be surprised how financially naive people are outside of interest.co. That's not a bad thing, that's just society. Just like you're probably not an expert in electrical work, plumbing work, driving a bus, open heart surgery. It's why we have rules and qualified people in place that are paid to perform the tasks and manage the risks.

- If an electrician tells me I can have a certain type of heat lamps in my bathroom, they install it, and the place burns down who is liable?

- If a plumber tells me I can have a mains pressure gas hot water unit, installs it and floods the place in the process, who is liable?

- If the bank tells me that I can borrow $1 million over 30 years on a $100k income, my financial situation doesn't change but the bank doubles the interest rates in 12 months and I end up foreclosing, why is the bank not liable?

Personally I'm surprised at how financially naïve people are that are here on interest.co.nz. I have not done the math but I very much doubt the bank would give you $1million on only a $100K combined income. I suspect you would need something much closer to $200K to make it fly. Really its personal responsibility as well, if you have to cut back on spending to pay the mortgage, you have to cut back end of story its not the banks fault.

The $100k on $1m is Hyperbole. But yes, personal responsibility comes into it to a certain degree.

Hypothetical: What if people cut back on expenses AND interest rates become terminal? I.e. 2.5% to 8% in 2 years of a 30 year mortgage? Does personal responsibility still apply or is it reckless lending? The banks have access to all sorts of data and expertise that common people don't.

Not Quite a Million for 100k income. But RBNZ DTI figures for 4th quarter 2021.

Total lending to FHB in Auckland with DTI > 7 was $297 million. Spread over 331 borrowers. Average of $897 k each. If D is $897 and the multiple is best case 7 That makes the average combined income 128 k.

Q4 2021 $354 million lent to 291 Auckland Owner Occupier non FHB borrowers with DTI > 9. That's $1.2 million loan average with average incomes to support of $135K.

The fact that they have that income now doesn't necessarily mean that that's the income they had when they applied for the mortgage. Also could have boarders, some of the debt could conceiveably be on rentals, etc. It might be unlikely, but it's not impossible that people could be in that situation.

There's probably a bit of 'gilding the lily' going on in loan applications, especially with brokers involved.

I used to work with one of the head people lending people in ANZ. One of his favourite saying was "If the bank lends a person a few hundred thousand for a house and they can't pay, that's their problem. But if the bank lends a person $1m for a house and they can't pay, that's the banks problem". The people in the bank are very aware of the situations they could create, problem is they work in a competitive lending environment that incentivises them giving loans possibly when they shouldn't in a race to the bottom between them. And it's right throughout the bank (well it was back then), front line staff given bonuses for writing loans, all the way up to the CE whose job it is to please shareholders by growing the loan book.

In real downturns, banks still wear it quite badly, having delinquent loans on their books, hanging around, is pretty horrible for them and they try to avoid it at all costs. Hence they try and go to the ends of the earth for customers in restructuring their lending etc to try and get them to keep paying the loan. Once it turns into a non performing loan and they have to act, it's pretty fast and they becoming willing to take a bath on it, just to get it off their books and move on.

I earn close to 300k and wouldn''t take a 1mil mortgage if you guaranteed me 2.5% for life

I have a bit of a hypothesis on this.

The reason the Key Government opened up kiwisaver for first home purchases, which isn't necessarily a bad idea for people under 30 who can recover their kiwisaver balance with regular contributions, was because younger people were otherwise struggling to save money in a bank account which earned very little and had no confidence in the stock market after the GFC.

Alot of the Key Government's efforts in the realm of finance, including the partial privatisation of the Power Grid, were about creating confidence and general will to invest in the Market. Kiwisaver was a sort of forgotten about contribution which no one really cared about unless they were preparing to retire. The long term thinking was obviously to get young people interested in saving for retirement early by getting them to think about their Kiwisaver as a housing deposit nest egg.

I also largely do not think it drove the housing bubble, even if you were earning $140k and contributing 10%, you are still only putting away 14k per year in kiwisaver + employer contribution + government contribution. What is driving this, IMO, is people using the paper value of existing properties they own as collateral to purchase rental properties, particularly after 2019.

I think they opened it up for property because it's a optional scheme, and people trying to buy a house would opt-out because they needed the funds.

It would be better to make it compulsory and get rid of the housing element.

It was of course a nice way to enable younger generations to pay more, too. Benefited investors again.

And effectively another taxpayer funded subsidy to the housing market with the Kiwisaver Government Contribution.

Its the employer contribution and government contribution we should be concerned with, as that's money from business and government going straight into the housing market, via first home buyers using their kiwisaver.

Snap re the contribution from employer/taxpayer...criminal.

KiwiSaver use Just pushed up house prices and when housing crash is complete people won’t have anywhere near as much for retirement, another great con for housing ponzi

Yes allowing investors to use equity in previously held properties to buy even more properties gives our housing market many of the characteristics of a ponzi scheme........which if prices ever start falling, the equity across an investors portfolio could reduce rapidly and start a doom loop across the market as a whole.

When the market became speculative (about 2012-2013 in my view...), cash only purchases should have been allowed so that investors were competing with FHB's on even footing. As opposed to an investor sitting there doing nothing and using annual gains of 10% in a previous property, to use as fund to purchase and additional property....and at the same time outbid a FHB when buying the new rental.

Its a bad policy mistake and why if the market does start falling, it could fall far further and with far more severity than many people can currently see....the investor 'equity' is just paper money that lives on a computer screen at the bank....without cash flows or the continued expansion of credit to the property market to justify its current value, it could just evaporate......

Exactly IO

At the moment people just think some fhb’rs and developers will get burnt.

But there will be a series of second order effects where people will lose their investments in non bank finance companies offering first mortgage securities.Additionally hundreds of thousands of people rely both directly and indirectly on the building industry for employment.

A couple of small time investors (in law sibling and their friend) have had no regard for their loan over the last 3 - 4 years, paying only interest claiming the gains outstrip the debt so it is fine. Any % loss or gain on the "value" of a home they own impacts their equity directly. At the end of the day, the debt is still there. They're fine as they bought a number of years ago, but the recent article indicating high DTI loans to investors in particular is cause for alarm.

The real question is, not that they should be allowed to borrow that amount, but why do they need to borrow more than that?

The answer is that in jurisdictions with the right type of land use and housing policies, they don't have to borrow any more than that to buy exactly the same type of house in jurisdictions like NZ where we have the wrong type of land use and housing policies.

If your goal is to buy and own your own home, regardless of capital gains, you will need _some_ debt. While you have that debt, kiwisaver needs provide the same return as the interest rate you pay on your loan before it can be considered a viable investment.

For the FHB, kiwisaver is their money, a portion of their income - it's not tax payers money like super. You can argue that there is the employers contribution however it is somewhat redundant given the fact that many salaries give total rem, that is "including employer contribution" and if it were removed employers may use that money to provide more attractive salaries (real world low unemployment problems).

SO aside from $500 a year from the government, a FHB would be better off in the long term using all of their kiwisaver to purchase, then taking a 5-10 year kiwisaver holiday to reduce the loan principal instead, then kickstarting kiwisaver again when they have less debt, than to keep their kiwisaver investment and struggle with debt for a much longer period of time.

If the argument is that Kiwisaver has pushed prices up, then what would be the difference if the astute FHB had saved and invested the money instead?

Those 10% buyers may now be in negative equity and with recession looming, will have to hope that unemployment doesn't come for them.

How many purely fictional boarders got mortgage applications over the line do you think?

If the answer is 'a lot', this won't be pretty. But I suppose that some of those fictional boarders might materialise into real ones.

A source of high passive investing income is disappearing. Back to some productive work.

Non-Bank system total outstanding mortgages grew from $3.5 billion in October 2020 to $4.8billion in October 2021. But don't worry. They only lend their investors money for quality deals like this.

https://homes.co.nz/address/auckland/henderson/17a-kereru-street/Aw2Gz

Assume 1 mil per property. That's 4800 quite stressed loans

It sold... astonishing. You'd could put together a better kitchen in a tent.

Nope, still for sale.

https://www.trademe.co.nz/a/property/residential/sale/auckland/waitaker…

My bad!

It didn't sell, Homes.co.nz is still showing the recently sold banner from the last time it sold in October 2021.

https://www.trademe.co.nz/a/property/residential/sale/auckland/waitaker…

Didn't *everything* sell late last year? Peak madness for sure.

Now they are trying to sell the flip for 930K. That mortgage is dog poo.

2 beddy !! ...ideal for busy professionals they say..lol,tell em they are dreaming...

Based of the current market they'd be lucky to get 800k for it. There goes most of the deposit.

the market has definitely turned to a buyers one.

Just received an email from one of my local Hutt Valley real estate agents - titled "huge price reductions on these properties"

Once the RE Industry starts spruiking it - you know its already happened.

It's almost like they have suddenly become Briscoes or Kathmandu and we know you never ever pay full price at these retailers unless your desperate. Bottom feels like a long way off still.

"Please?"

Ha, I received a similar one from a Wellington REA. We were about to list our rental with them too, maybe it was sent to the wrong mailing list.

Those that do not need to sell will lose no money at all. None.

Those that need to sell (divorce, mortgage to expensive) will lose some money depending on when they bought. If they bought a couple of years ago (or any time before that) then the market will need to fall by a 33% to get back to where the bought in. If they bought in the last 24 months then yes, they may be in trouble and unfortunately this will mean about 90,000 FHB's will not get back to price growth for some time.

2019 -

"Median prices have already risen 20% this year, according to the Real Estate Institute of New Zealand, taking the median national price from $605,000 in October 2019 to a new record high of $725,000 in October 2020. The median price in Auckland is now above $1m."

2020 -

"Auckland’s median price increased by 26.2 per cent annually to $1.3 million in November, from $1.03m last year. All seven of the region’s districts had annual median price increases."

" 44,300 withdrawals for first home purchase in the year to March 2020"

Thing is even if price drop 50% those who can’t afford still wont be able to afford and will still be complaining.

The market needs both positive and negative to work you see.

The deposit is the biggest hurdle for most FHB....if prices drop by 50% that hurdle is reduced by a large amount of money making the prospect of buying far more realistic.

Your line of thinking is very misleading....and appears to be more along the lines of 'I don't want prices to drop because it will impact me personally' as opposed to thinking about the interests of those who currently cannot afford.

The deposit was the biggest hurdle. That is true but will not be if inflation persists. Then the biggest hurdle will be servicing the debt on the mortgage.

The challenge for people who's labour is not as valuable in $ terms as others has not been removed, merely shifted, so what he says in general terms is true.

Well won't that cause banks to reject more applicants, causing more falls in home prices? If they know straight up the mortgage can't be serviced, they'll have a clearer reason to reject the application, rather than deposit reasons, for which many ways around can be negotiated.

This is just incentive for potential home owners to wait even longer before buying, and home owners will lose even more equity... just saying.

At a lower purchase price and lower quantity of debt, the affordability of mortgage repayments stay the same. Your assumption, I think is that prices can never fall.

Relax, getting too technical and analytical will blind you and will potentially missing out on the simple things. No offence to all the economists out there.

Price drop will not impact me as this is what we’ve been waiting for and expecting, we like to buy when there is “less competition”(during property down turn).

This is the internet and that was just an opinion, different people make different choices and this is what makes the market work.

Odd how people back down from their positions when presented with ‘alternative facts’

Surely paying 7% on an $1M mortgage when you could be paying 7% on an $800,000 mortgage is losing money?

Somehow, people seem to find this very hard to understand. And then they say 'the best time to buy a house is yesterday', while this is clearly no longer true.

https://www.nzherald.co.nz/business/effects-of-rising-mortgage-rates-ye…

Everything is pointing towards one direction....,... If with just thought of interest rate rising is having such negative effect, can imagine what the actual damage will be when it actually hits as per article by Jeenee T in NZherald.

Good thing most mortgagors are on fixed rate mortgages at the moment.

Stats show most mortgages roll of 2.x% loans sometime this year, to be upgraded to a 5.x or perhaps a 6.x refix.

Interest rates were suppressed for too long from March 2020. Allowed 500,000 new mortgages to be written. 50 billion of new mortgage debt added to pump up house prices and stimulate demand for everything else via the wealth effect.

Hadn't realised Jenée Tibshraeny was at The Herald now... her more balanced reporting perspective might become a bit of a problem for property spruikers. Hopefully.

Oh no, bought this place at Auction 2 months ago

https://homes.co.nz/address/auckland/st-heliers/111-melanesia-road/5jMzR

Doesn't settle for another month, had trouble selling our current house

Maybe set up a Givealittle page

That's a great idea, "help this young family into their forever home"

I assume you have now sold your current house?

Yes, just went unconditional Tuesday after being passed in at auction and then 'offers', had to drop a few hundy but happy to move on

Sincere congratulations.

I note there is a column on this site today about public health & infrastructure investment that has garnered 2 comments...whilst any column on house prices going up or down attracts hundreds...bit of a sad indictment on the kiwi mentality aye...as long as my house is going up,who cares about anything or anyone else...

Only economy in NZ =Housing Economy

It's a really good article too.

I bet there must be a few people out there changing their mind about the CCCFA rules.

They will be happy they had one too many lattes & smashed avo to get their loan application across the line.

Doesn't look such a stupid rule now aye,saved people from themselves.

https://www.stuff.co.nz/life-style/homed/real-estate/300587995/asb-pick…

ASB picks 20% house price fall, biggest drop since 1970s

Hold on, they are picking a 12% decline in nominal terms, 20% is in real (inflation adjusted) terms.

Thats the 'gotcha' headline...

Grant to Jacinda: "House prices have dropped 0.0001% annually!!!"

Jacinda to Adrian: "Adrian fire up the printers! Now!"

Adrian to everyone: "Yes I decided to do that - all on my own. We've got this, this is what we do best.

Net result: Housing is saved once again and we now lead the world, with the best house prices on planet earth.

inflation. Low NZ dollar.

No money printing this time round.

Nothing for it but for a little blood letting. Strap in, clear down your debts and wait for the opportunities...

I've made comment before, that I've never seen so many supply restrictions to affordable housing before.

The restrictions fall into two main camps 1) Those that we as a Nation have control over, and 2) those more universal ones we don't.

We have chosen as a country to allow the restrictions we could have controlled to feed a house price rise to give unearnt and untaxed capital growth gains to property owners., and hence unaffordable housing.

Now that there are international factors that we have no control over that are dominant, we now find ourselves at the crest of a boom of our own creation, and a fall that we have very little control over.

We have set ourselves up for this fall, so it's just a matter of what we do to reset, or not, the system when we are at the bottom so we don't get a repeat.

It's been policy of greed and intergenerational looting by propertied politicians and bureaucrats. Living beyond their means by passing the cost to younger generations.

I don't think you can only blame the politicians and bureaucrats mate, plenty of property investors I know we're the ones who were gorging at the trough and their attitude was everything is fine I'm milking it. To be fair quite a few oo very happy with the massive price increases too, loading up on new cars and toys, no regard for wider consequences. Anyone who bought or lent money to their kids to buy in this boom is partially to blame.

If the Govt. set up the rules of a corrupt game, that due to your ignorance, you find you are good at, of course you are going to follow it.

It's a dysfunctional system that if deliberately perpetuated by the Govt. as they are appealing to the lost common denominator in all of us.

In this case, the egg (the Govt.) does come before the chicken (the voter).

its gonna get a lot worse. its been too easy. Jacinda must do a CGT.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.