House prices have dropped 10.9% from their peak in November last year, and are now lower than they were a year ago, according to the Real Estate Institute of New Zealand's House Price Index (HPI) for July.

The REINZ HPI is the most accurate measure of price movements because it's based on sales as they become unconditional each month. That means it's at the leading edge of price movements, and it adjusts for changes in the mix of properties sold each month. Thus it's less affected by changes in particular segments of the market, giving a better overall view of market activity.

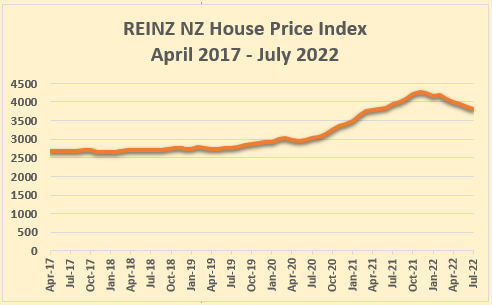

The graph below shows the monthly movement in the HPI between April 2017 and July 2022, showing particularly strong growth in prices from October 2020 until it peaked in November 2021, after which there has been a steady decline.

The HPI is now back at the same level it was in May 2021, meaning properties, on average across the entire country, will have lost all of the capital gains accrued since May last year.

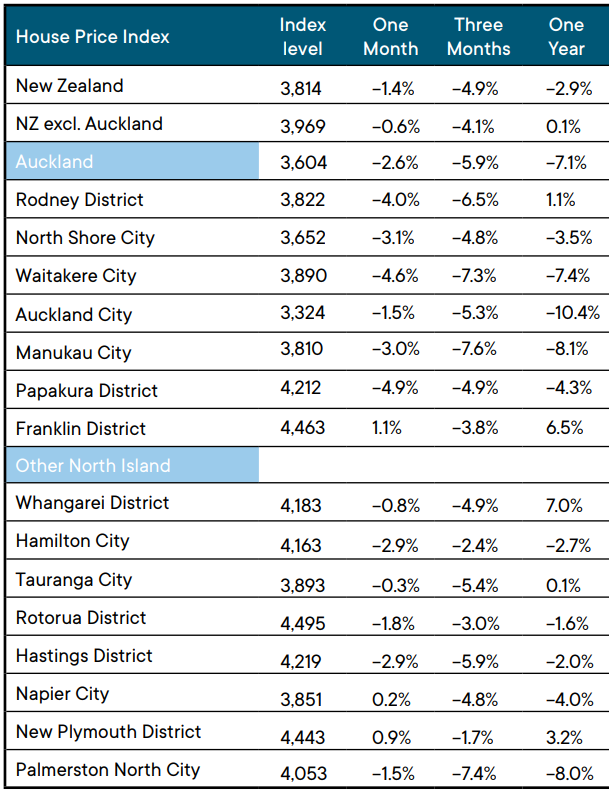

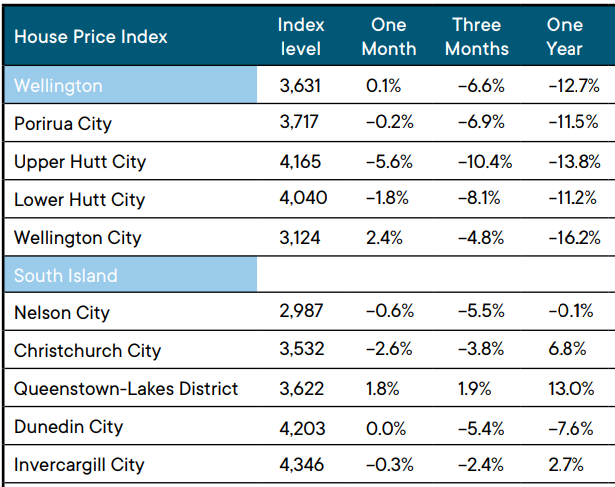

The tables below show how that has played out across the main urban districts around the country, with the changes over one, three and 12 month periods.

It is particularly notable that most districts are showing price declines compared to 12 months ago and most of those that are not showing annual price declines are showing declines over three months.

That suggests differences between places like Wellington, where price declines have been steep and prolonged, and Christchurch where prices have been more resilient, are mainly timing differences, with prices in places such as Christchurch taking longer to start falling.

However the trend for falling prices is now clearly evident nationwide, with the few places such as Queenstown-Lakes where prices have been more buoyant now also more likely to start showing price declines over the next few months.

The comment stream on this story is now closed.

REINZ House Price Index - July 2022

167 Comments

[ Defamatory comment removed. Also, this was not about the issue. Ed ]

Something about 7% interest rates and -30% house prices by December.

I'm curious what this comment said now.

Looks like the prophet has eaten another ban, we'll have to wait until 011111100110 shows up to clarify.

I hope that the scrolls are not lost. I want to know the revelations they contain.

2022 That was quick

The cheap finance fueled surge during Covid was 100% artificial sweetener. No one should be surprised at this retreat. Nothing but speculation seeking tax free gains. If you bought after 2019 you should be happy to get your money back. Anything after that your either stuck for a while, of facing capital loss.

Rates are going up another 50bp next week and more to come. Popcorn.

It's all positive for Queenstown, no wonder no one can afford to work there.

Pay rates are currently going up in Queenstown fast.

Demographics shifting. Those cashing out and moving to a place were there is a. Highly desirable lifestyle but highly restricted land available?

It’s a shame this article doesn’t call out the fact that prices have declined 15% in 8 months in Auckland.

Give it 4 months, the "12 month" house price index will no longer include data from the tail end of the upswing.

And just like magic the mainstream media will cease reporting YoY numbers when they don't paint the narrative that their benefactors desire.

"REINZ report today that the 5-year returns on property remain strong"

OneNews last night, property declines 2% in the last year, great opportunity for first home buyers.

Yes, they have been using to YoY number to hide the current trends. Whats more, the "fall from peak" also ignores that regions peaked at different times.

When you look at the annualised rate of fall (from the time each region peaked) you start to see a much clearer trend. Some regions (wellington, Auckland) peaked earlier, so it currently looks worse, but the rate of decline for other regions that peaked later aren't that far off in terms of trend:

Hi Miguel, I'm so hoping you'll update that awesome graph where you interlay the housing crashes of different countries over time, showing the 3-month rolling average of price falls per month. Any chance of you updating that graph, please? Pretty please?

??? The media will always dramatise everything to the max. It’s often this that unfortunately discourages the inexperienced from taking advantage of the downturns to get on the property ladder.

That, and it's a ladder that goes down these days.

Snakes and ladders?

Wellington is definitely starting to look ugly. Next few months could be very interesting. Stock levels still very high for August, very little selling, how big will the spring surge be?

Interested to know how many of those sunset clauses eventually got used, given everyone was trying to figure out how to use them to their advantage. The buyers who walked away might have been the biggest winners after all.

A mate also tells me that new residential development proposals there are dead in the water. Seemingly much worse than Auckland

Good news! Onwards down the spiral staircase, but slowly and gently as we want a soft landing

Wait a minute. I was here first. You can’t just copy my username and change the last 2 letters. Yours sincerely, N.Raged

Well this is awkward....

Interest.co.nz team - any idea of how many mortgages or what value of mortgages might now be in negative equity across regions/country as a whole? Would make an interesting article (from my perspective).

Areas like Wellington must now have many FHB's underwater - ie those with low LVR's and even now those with 20% LVRs.

Been wondering how this plays out in relation to banks not getting caught out. Basically I see the banks having models that see them pushing sales in 20% increments or so meaning only the buyer loses their equity. Surely they must have some strategy to see that they don't lose or am I over crediting their collective intelligence?

Starting to see stories like this in the mainstream media - I highly suspect that the banks are putting the hard word on over-extended borrowers behind the scenes.

https://www.nzherald.co.nz/business/rising-interest-rates-bite-bank-won…

Mortgages under 20% LVR have LMI so the banks are covered. Its mortgages that were over 20% LVR and don't have LMI that is the problem. Just like in The Big Short, the real money didnt come from shorting the triple B's, it was made by shorting the double As.

10% of homeowners who bought in hot market now in negative equity

Nice - thanks Nifty.

Brought to you by OneRoof, the people who told you that prices would not fall, at least not meaningfully.

Evil

The analysis is fairly simplistic, but interesting nevertheless. They assume everyone had 20% deposit … we know the LVR limits allow a percentage of buyers to have lower than 20% deposits.

The biggest concern will be if prices get substantially below prices in early 2021 when the LVR limits had been removed - that could get ugly, quick

This is the drop from peak for each region:

LOOOOOOOOOOOOOOL.

Ireland fell 7% and Dublin 9% in their first year of their property market crash and went on to be down 70% by the time the market bottomed out.

Upper Hutt and Wellington are down 19% in the first 9 months = 24 - 25% annualized.

Yes, any talk of soft landing should be stopped in it's tracks, the RBNZ aren't nearly competent enough to deliver that. You don't turn this sentiment around, we are most definitely looking at 50% falls peak to trough in many parts of the country. Maybe not Prime Auckland, and Coro/Queenstown it would seem. The wealthy will be fine, it's the average Kiwi who will suffer.

I find it odd that people who were previously pro property, are now claiming the market could fall by 50%.

And yet I've been told on here for years that it would be impossible for our housing market to ever fall by 50%.

What a strange world we live in.

I'm still pro-property and they won't fall by 50% in prime Auckland. It's the insane gains in regional NZ that will be eviscerated.

You have jumped from one extreme to the other.

I doubt very much that prices will fall 50% in most markets in the country.

Correct. You would need either accelerating inflation. Or a combination of high unemployment and an oversupply of housing to cause such a big drop.

Unfortunately posting emotionally charged comments on interest.co.nz alone can’t cause that larger fall. But many will try.

I am a long time housing bear, but some of the predictions of house price falls are an absolute nonsense, perhaps even sillier than the people who said prices would never drop significantly.

Id say its better a bull than bear. So you got it right this time but not the last 2 years

Fat tails make bears whales.

What is going to stop Auckland houses dropping considerably more than they already have. I think Auckland is is in more danger than some of the regions. For a start you don’t have to live there to get a good job. All you need is a phone, lap top and internet.

I think you are exaggerating the potential of remote working. There are still limitations as to how widely it can be taken up.

I think at least some of Wellingtons property woes can be attributed to this.

I live in Nelson and have run into 3 people recently that have Wellington jobs.

They only have to go into the office occasionally so decided to move to Nelson.

These were Government or local government jobs. So I'd imagine this is probably quite widespread.

T U R A N G I

Curious ey

oh well, at least Te Kooti and Yvil admitted the error of their ways, unlike TTP. They begged the Prophet for foregiveness.

And P8? He just disappeared

Yes and you do wonder why type of numbers the boys in CWBC's basement are running these days.

From memory he claimed to be flipping 30 properties a year....that won't be a profitable business at present, nor perhaps in the coming 12 months. The losses could be massive.

Lol.

I've got my boys in the basement today also, though I can't make them do data analysis, they just want to play lego 🤣

Anything possible from here, All roads heading south presently, though I can't decide how pessimistic I am.

The only data analysis my 5 year old has been doing today is seeing how much glitter she can mix in the various paint pots. The joys of WFH + sick child, very hard to multi-task.

Not sure what your point is HM, I have done very well out of property, even at a 50% correction. I didn't buy or sell during Covid and I am already looking to acquire more. The market will recover back of 2023 early 2024. These are perfect conditions for long term investors as the pretenders get flushed. We will be there on the bid when it's at it's worst.

Well apologies if I am totally wrong, but I thought you were one of those who, before this year, effectively promoted property as a one-way bet.

Again apologies if that is unfair.

Rarely, I am a property investor but generally refrain from commenting as it's an emotive echo chamber and I get it has been hard for the average person. Why rub it in.

I'm very pro-property, but I've also said that the market has the potential to fall 50% based on the amount of non-value added costs in the system. IE these are costs only due to monopolistic price increases that restrict supply and cause prices to rise but add no extra amenity value. This is just what the evidence shows if you want to acknowledge it.

If we had a different Govt. policy, these costs would not be allowed to exist and would disappear and you would be able to buy the exact same house at a lower price, or a better house at the same price.

The ones that have been saying prices cannot fall by that amount are only saying that based on their own self-interest in that 'it is hard to understand something, or easier to remain ignorant when their income is dependent on thinking that way.'

And for some that have been a very profitable way to live, giving them the overconfidence in thinking money equals intelligence and even some moral superiority.

They are also the same type of people who might think winning money at the roulette wheel is good management or some divine being guiding their hand, rather than good luck.

But I think your ‘pro-property’ mindset is very different to the speculative one? You are pro-property in terms of the benefits of housing for people to live in as a home. And that that housing should be affordable, with non-volatile prices.

That is a very different ‘pro-property ‘ mindset to the spruikers.

Yes, I am, which I think is the correct definition of Pro-property, and is of benefit all the way through the economy as to how much income people need, ie they don't continually need wages to rise (which they are not rising fast enough anyway) to keep up with over-inflated house prices. and further follows on to affordability of education, health, retirement savings etc.

The definition used by true speculators is more 'Pro-sell their Grandmother.'

The other problem is the "Recency Effect" kicks in. People read recent articles or stats about a monthly price fall of 2% and think "well it's only 2% the market is cyclical" and completely ignore the previous 8 months of cumulative 2% falls.

Sadly you are right. I think we're in for a rough time. Lots of overshoot on adverse economic indicators coming, as well as the period in which various people responsible try to convince us they're transitory as well.

Don't fall for it.

yes, the average kiwi will suffer, including many here who are laughing, someone may repost the video on Ireland 2007 to 2014

Yes property spruikers thinking that a National government will save the housing market, might find that the election is going to come too late in the piece at the pace at which the market is dropping.

It would be tragic if National got in just in time to change the overseas investment rules... and sell our country's housing out to foreign interests at bargain bin prices.

It is past time that everyday Kiwis had a crack at owning their own home.

Yes, at the bottom of this cycle, less restrictive policies need to be put into place so there is no speculative reason to buy the property. That will get rid of both local and some of the overseas speculative investors, plus needs to be tied into a descent immigration policy so only owner-occupiers are buying them.

A freer less restrictive market will take care of anything else that would lead to monopolistic behaviour.

However, the big issue after that is if you can't make a killing in speculative behavior on the property where do you put it so that you have money at retirement, given that NZ has nearly twice as much and the majority of their personal wealth tidied up in their property as the USA.

I think that a lot of the demand may not be there - look at China. Their RE market could be in just as much trouble as ours. There could be some very gun shy property investors for many years if things get as bad as what some people are suggesting.

According to Geo Politics specialist, Peter Zeihan China has an over-estimated population by 100 million, and their demographic spread via their 1 child policy could see them lose half their population by 2050.

https://www.youtube.com/watch?v=t5nlKopzg80

According to these numbers, Auckland is less than 5% away moving from correction to full blown crash. 💥

Not much better around the rest of the country either. One can only imagine how flaccid the mood is turning at the Property Brokers HQ.

It’s going to be fascinating to see how TTP, Ashley Church and Tony Alexander spin things over the next 6 months.

Bring the popcorn.

I'm not sure that two of the three people you mention are even self-aware.

Yeah quite possibly done unconsciously for two of them.

Queenstown and Coromandel +13% while Auckland and Wellington collapse, working from home trend? Even the once remote parts of Coro have fibre now, mostly thanks to Labour's school commitment.

Places like Tuateawa have had it for ages! Our fibe-rollout really was a pretty solid effort given how much we've buggered up everything since.

It's impressive and all down to Labour's commitment to schools. I know several people working senior roles from remote Coro spots 3 days of the week now, they can zoom, stream etc etc.

I think that will come as news to many who remember National's promise to roll out fibre as part of the 2008 election, which may have played some small part in it.

Either way, a good effort.

Like happens with most tech though, now obsolete with the advent of Starlink.

Maybe in remote areas. But on the whole starlink is not a replacement for fibre.

Absolutely, Im just waiting for the affordable marinised version, and the rest of the south pacific to go live and bye bye

Apparently you can use the RV version on a boat for a tiny fraction of the $.

Yeah that works fine but the South Pacific isnt turned on until 2023. Also from what I have read they are geo fenced, 12 miles off shore and its a no go. The marinised function also needs to work without the land based connection, uses laser connection or some stuff that is way above my understanding.

Current marine version is 10k usd for the gear, and 2k usd a month, and really only works in US and european waters currently.

Yeah I thought that sounds odd, Chorus have been doing fibre in schools for years. In fact a quick Google found a Stuff article about not-Labour Nikki Kaye's press release way back in 2013 about allowing schools to onsell their internet to their communities, benefitting rural schools.

Tuateawa doesn't even have VDSL yet, let alone fibre

Oh yes it does, runs up that Coast and over the hill to Colville Primary. There are then repeaters on all the hills around there.

Indeed. If you can truly work from home you can even work from the Gold Coast or from Bali or from Portugal.

It's what myself and many people I've worked with previously are now doing for the foreseeable future.

If you can work from home, someone in India can do your job for half your wage. Cuts both ways.

Hmmm sounds good. But have you actually tried working with some of the cut price alternatives? In demand skill sets is a complicated thing. Certainly not like for like.

I’d second that. In my experience with outsourcing, very mixed results. Worked with dedicated resource centre in India and that worked really well, but yet to have success with any cut rate freelance or contractor who provided value equal to or greater than their pay. Generally my experience has been that what you don’t pay for with money, you pay for in time back and forth trying to communicate issues or problems with the work, lengthy resolution times and deadlines pass.

Had a lot of success with remote workers, but only at market rates. And market rates for remote jobs are generally a lot higher overseas.

Depends on the type of work being done, and what level of quality you want, and the the legal, cultural and people management issues that come along with it.

On paper sure... in practice, not really.

dp

Yep TK called that for Tauranga as well months ago but it got rubbished on here. Obviously Coromandel is a closer commute to Auckland so its even more viable. Prices there have always been a bit stupid anyway so no surprises there. On 300mbps fiber here now, and 300mbps Wi-Fi if you have a modern device nothing you cannot do from home.

That just leaves schooling, but then you have greater assets/disposable income to address that problem if you're not living in central Ak.

Our company's Kordia VPN speed is 100mbit max. So 300mbps (or Gigabit like I have here) means WFH is completely doable.

TBH, the most bandwidth you need for WFH for 99% of jobs is enough to run a Skype call.

Well yeah, 99.999% even. I'm handling fairly large files (tender documents) but even then the biggest tend to be no more than a gig. Easy enough to upload/download in a couple of minutes but opening large drawings on the fly from the server is another issue. I end up just filling my hard drive with projects I'm currently working on.

And for me it's latency rather than the bandwidth that slows things down when it comes to running database queries.

Pro tip, the speed of light is three times slower in glass than in the vacuum of low earth orbit.

Google says the speed of light is 200,000km/s in glass vs 300,000km/s in vacuum. Not 3x slower.

I still strongly maintain that there is a limit to how many people can do this.

Most jobs still require a daily, or perhaps 2 days per week, presence at the place of work.

I also think it’s become more accepted / tolerated in these times of low employment, by necessity. I wonder if there will be as much leeway as unemployment ticks upwards.

I have seen plenty of examples of people taking the piss working remotely.

Again, it has got its place but there are limits.

It's not going to last forever. Just wait for the next unemployment spike and ceos will be demanding you all to present and actually working again...

Not everywhere, there are a few positives on here.

Wow, that is plummeting by historic standards. So the big question is, will it slow down after the froth from the last couple of years is skimmed off the top? Or will it be a positive feedback loop and blast right on through?

Yeah I think its possible people are underestimating the animal spirits that could be at play here. If house price falls becomes the common narrative in the Kiwi psyche, it could take months or even years to reverse the housing market when the RBNZ starts dropping interest rates.

If people honestly believe that they can by a house cheap in the future, they will wait. This is what I saw in the US during the GFC...even as interest rates were dropping. Cheaper lending wasn't the primary focus of buyers....it was protecting the capital they had and not losing it.

I want to buy another rental, as well as an upgrade on primary residence.

Though we could do both now. We will wait until prices stop going backwards for at least 2 or 3 months.

Whether this is 6 months, or 4 years from now. Doesn't bother me.

As pointed out above, the more prices sink the more collective wariness will entrench when looking at taking on debt.

Anything possible at this point.

Reminiscent of Gold Corp days perhaps...

I’m with IO.

This is getting very real for anyone who bought in the last 12 months. The cost of owning a home has grown while the value of the asset has shrunk. Negative equity is now a tangible part of the landscape. FHB’s are the spark to the flame of housing market. They may have worried about the possibility of soaring interest costs but watching the value drop too will be a terrifying combination.

First homes always squeeze finances, so why would you enter a market with this not evening threatening but actually happening.

I would think the narrative is being tightly managed.

no mention of investors on interest only?

and if house sales have fallen off a cliff please enlighten me how presales for developments are going

because that’s the red flag for employment a year out

and it’s one thing to be in negative equity….a much bigger problem if you lose your job and can’t sell or move

Those investors on IO and finding they're now on negative equity won't be selling in that kind of market - not unless they've got some high equity properties and rents shrink too much to cover the P+I the bank may force them onto.. So don't count on them to boost housing supply for FHB.

The banks won't let them stay on IO if equity is gone and prices are falling.

The only two options will be P&I or a forced sale. There are a ton of landlords who have been relying on IO to make things work... some are in a position where the rent doesn't even cover the IO payments!

I am fully expecting overleveraged landlords to be a significant source of new listings. I think there will be a flood of them.

I think they'll hold on for longer that is rational. The narrative is too strong. They'll go into bankruptcy before admitting defeat and selling at a loss.

Ashley Church will be in their ears, telling them to hold on... it's just a cycle... property always goes up eventually...

And after a while he will be right.

HODL

That was my point. If they have some mortgage free properties or ones with sufficient equity many may choose to sell one or two of those to pay for the P+I on the 10 highly geared properties rather than take a haircut/not profit.

yeah but those interest rate increases are going to start to bite

Only to the recently over leveraged. Current interest rates are about par. Most will be completely fine.

Agree this is starting to get ugly for people who bought in the past 12 months.

I bought 2.5 years ago, my latest Homes.co.nz valuation (not that I place much weight on that) is only about 10% higher now than the purchase price.

The hospital pass of the century continues. Really starting to look like the 2020 - 2021 OCR levels were more about an exit-strategy for one generation to pump their retirement savings at the expense of another. The real trick for financial wellbeing in this country is to be born as a 65 year old straight off the bat. Otherwise, frankly you're buggered.

I guess millennials will be relying on Gen Z to use their disposable income left over from their smaller mortgages to start businesses and hand-out jobs, given that we'll be dealing with these massively inflated mortgages for a while. Better start learning how to TikTok I guess.

Certainly boomers had a good run of things.

But its still easy enough to generate compounding returns no matter your age.

Invest time/effort into your professional development. Check.

Aim to save 15% of your income straight out of uni. Check.

Don't marry someone who likes flashy jewellery. Check.

Everything else is gravy.

Until of course petrol runs out and society as we know it collapses...

>Until of course petrol runs out and society as we know it collapses...

Cue PDK

His diatribes certainly have that Ted Kaczynski vibe.

Fool. Have you never heard of entropy or EROI. Please educate yourself: https://www.nzwomansweeklyfood.co.nz/recipes/butterfly-cakes-35073

Woman's weekly butterfly cakes? I guess it's different from the usual line, I'll give you that.

The physical constraints of this world are very real.

The increasing co2 in the atmosphere is very real, along with the increasing heat this traps.

Our current (lack of) change to our consumption behaviour is also very very real.

Yes, your current lifestyle, supported by current technologies and energy supply. Is 100% not sustainable in its current form for more than another 30 or 40 years.

Change is coming, either we adapt to it or not. The physical reality does not care.

Invest time/effort into your professional development. Check.

...and end up with a student loan that costs you 12% of your income after tax over a pathetic $21K, massively more than what it costs you in Australia?

Aim to save 15% of your income straight out of uni. Check.

See above.

Don't marry someone who likes flashy jewellery. Check.

...And let me guess, doesn't like avocado on toast? Is there really a thing where there's a bunch of renters flashing Rolexes out there who are perplexed why they can't afford a house? Or is this just a low-effort stalking-horse.

I managed a lot of these when I graduated but the grad wages in my industry are about the same as they were and living costs are about 40% up in nominal terms. So I don't think it would be quite so simple as things stand.

I graduated uni with a stock standard marketing degree. I think I was earning 46k PA back in 2006. Also with a big student loan for my troubles.

20 years later I now contract myself out, self employed at 1100+/day. Different job of course. And I realise I am fortunate. But Do you think I found this earning power inside a cereal box?

Investing in your professional development is not about just taking a certain course at uni and expecting a pot of gold at the end of it. It's career development. Constant learning and development. Networking. Trying and seeking new opportunities. And having the courage to leave and move location or companies if you are not getting what u need from your current position.

Moving overseas may well be part of this. I gained valuable experience from my time in aus and EU.

I work in professional services, but It can apply to anyone, in any vocation. Sacrificing your time at night to plan out what your career objectives are, what roles you are aiming for, and slowly stepping towards it. Say you are a new tradie, sitting down with someone in your line of expertise and asking them how they came to operate a successful company etc.

Im not talking about rolexs, but yes a wife who naturally likes to save money is a blessing.

I earn big money. But we are both happy driving old cars that cost 10k each.

Great post!

when my son asked me about shares recently, I suggested maybe to instead invest in himself.

For example, he has an engineering degree from the University of Auckland. But he has weakness in public speaking, or just simply speaking in even small-mid sized groups.

Doing something like Toastmasters could bear significant return on investment.

Yea, see that's the thing. This isn't enough anymore. That's the bit I don't think people understand. And while marketing might reward people job hopping, it's red flag in other professions. I'm almost there, but by no means has it been as easy as this makes it out to be. You need a fair degree of luck along the way and people seem to have an allergic reaction to the idea that sometimes they were in the right place at the right time, and others might not have been.

Having the time to plan development is easier when you can set your own hours, work from home, don't have to commute, and so on. It's a lot easier to get those things once you've already got the seniority, but it's a hard graft if you don't.

Signed, the guy who kept driving a beater Corolla even after it caught fire on the way to work one morning at around 300,000km at the bottom of town (eventually someone rear-ended me on the motorway on a Friday night drive with some friends and it was a write-off; it took an inattentive 4WD owner to do what Father Time could not).

I work as an IT project manager, marketing doesn't pay that kind of Day rate.

And I could write you a plan to get this job in the next 6 or 7 years.

It will be hard. And difficult. It was for me. But anyone with the right attitude can succeed in my practice.

Its hard work. Persistence. Planning. Readiness to learn from failure.

Luck has nothing to do with it.

The next 12 months will be very interesting in NZ.

Its going to depend in the next few months whether RBNZ decide to hold their line, to smash inflation and raise the OCR until its tamed, and ignore pressure from the Government and housing related industries. Which is by far the best solution long term for our economy.

Or if they cave to the pressure, and start to take their foot off the brake and slow down the ocr hikes.. which will give a short term respite for house prices and the government but possibly mean much higher OCR raises in the medium term, and deliver a longer drawn out downturn

Personally I think the labour government has lost its leverage with RBNZ and is fighting too many fires including losing credibility of the covid economic response (with a possibly brutal report on their actions ), the opposition is now strengthening its hand and RBNZ will feel confident to go hard and keep raising, and in doing so will be siding with the opposition and further weakening confidence in our govt.

Neither the Government no the realestate industry have any influence over RBNZ other then when they added employment to the RB mandate.

The only pressure RBNZ have is that they probably all have large mortgages.

Or they may have a bunch of investment properties (in which case is there no little voice in their head that would make them averse to dropping house prices too fast)? Or perhaps some of their mates at the golf club do.. or whatever.

Its the other little things like.. who makes the decision to reappoint Mr Orr.. and who writes his reference letter.. and who would be involved in his selection for other roles later (i think Mr Robertson is the key guy)

And which key stakeholders in nz and overseas does rbnz need onside sometimes to drive certain behaviours... the banks etc?

Whilst i am sure the current team are independent.. as with all such organisations they cant do everything alone and will for sure have a lot of external influence. Its unavoidable and whilst i would never say they will be knowingly biased due to external factors.. anyone in that positions would have to be biased even if subconciously.

I still think the OCR will hit a glass ceiling of 4% and stay there. The RBNZ would rather have you paying more at the pump and at the supermarket than crash the housing market. We only need to wait until December 2022 to find out if I'm right or not.

The housing market is already crashed.

Just like a 737 Max. There is no pulling out of this dive in time now.

Poor analogy. The housing market won't crash into the ground and not recover.

The housing market (plane) will fall for an unknown time at an unknown pace, but, at an unknown time it will come out of the dive and return to high altitude.

Wrong. The housing market crashes when the drop hits 20%. That's ground level. There may be some cratering.

Prices are likely to never return to the same level in real terms.

Prices are likely to never return to the same level in real terms.

Correct. People need to stop seeing this as a temporary deviation from an otherwise sustainable trajectory, to which we will eventually return. It's a reversion to the mean, from historically unprecedented (and unjustifiable) heights.

Developer above Orewa with tinted glasses. $830,000 for 459m section😂

https://www.realestate.co.nz/42163884//42163884/residential/sale/lot-51…

Must be $380k, miskeyed the price.

Agree that the housing market has always worked in cycles. However, I don't agree that prices will never return and exceed the high prices achieved in the past year. If that occurred, that would be the first time in history that house prices have not increased over a medium to the long-term period from the 1900s to today.

As long as our reserve Bank model continues to increase yoy money supply, there will always be long term growth.

Its just a question of what that money is spent on...

and how much inflation that causes

For what country/s are you referencing in this comment?

In real terms however, the evidence from hundreds of years of tracking house prices on a street in Amsterdam is that house prices stay relatively constant over the very long term, although there is considerable variation over the shorter term. That stands to reason actually otherwise eventually no one could afford to buy a house. Real house prices have dropped significantly in NZ due to our high inflation rate.

RBNZ, though nominally independent, is tightly constrained by global forces, above all the US Federal Reserve and global bond markets. Also, several commentators are picking a sharp uptick in oil prices again toward year's end due to Russian intentions regarding European oil markets. If that eventuates, the Fed will have to raise interest rates and RBNZ will have to follow.

Have you seen the video about Ireland 2007 to 2014 that someone posted in another thread? The unemployment and suicide rates, Irish people leaving to work lowly jobs in mainland EU? The result of a property crash. At the end, Ireland was ironically left with another shortage of rental accommodation. It is in that video.

I cannot understand why peeps want this here and what makes them think they could benefit from a massive crash and ensuing economic collapse.

Markus - I wouldn't confuse 'wanting to happen' with 'what could happen'.

And even if you don't want it to happen, who is going to stop it from happening if it possibly could happen? Is it within somebody's control to do so? And if this is the case, how do you explain all of the other countries around the world where property booms have had resulting crashes? Was someone meant to step in and stop this from happening? And if so, why didn't they?

I would agree that back in about 2014/2015 we had the option of doing something. But now the horse has bolted...but when I started warning back then that this was a possibility....but most people were blinded by their own greed and 'getting ahead' to worry about the potential consequences of blowing up a massive property bubble.

Only five more percent until we are officially in crash territory.

Markus, maybe it wasn't a such a smart idea to go all in on property.

Havent you realised Markus that half the peeps here are in cuckoo land. The other half, well they are just nuts. Do you think you they will thank you

LOL. It's ironic that you say "peeps" are asking for a crash today, but conveniently ignoring how they were asking for a crash for the last 5 - 10 years.

"Hey, omg, you're wishing a crash that would cause mass suicides etc" uhh no they were wishing a crash to happen before we got that far down the track i.e. where we are now.

Exactly - I've been warning on here for years about the consequences of the selfishness and greed I was witnessing. But everyone was mostly like 'be quiet mate...I've got money to make'.

So I have no time for people saying that they don't want to deal with a crash if it comes.

In life, as a principle, you have to deal with the consequences of your actions. And our collective actions have been bad, so the consequences are likely to be bad.

It's not about wanting a crash. It's about how you perceive the status quo. And that probably depends a bit where you sit.

I feel like I've seen the fabric of society tearing apart over the last ten years, and that the property bubble has been a big part of that. My circle of friends and family are not wealthy people. No one has any security. Children are constantly shuttled between schools as landlords kick families out because they want to reno/sell/raise the rent. Anyone who doesn't already own property has been in despair that such a thing is possible, as they spend an ever-larger percentage of their income on rent. Meanwhile, those who already owned property and had some equity have been able to lever up infinitely and extract ever more wealth from the bottom 50%.

So if the downside to a property crash is, say, 7% unemployment, we can live with that. We have before. But if we don't kill the property bubble stone dead the alternative is a society that looks more like Brazil or South Africa.

Yip - oddly it will be the people who have been name calling others 'doom gloom merchants' who will soon become the doom gloom merchants.

Even guys like TK are saying that property prices in some places could well fall by 50%.

I've been saying that has been a possibility on here for many years but if I ever said that it was because i was a just 'a doom gloom merchant with no credibility' (lol).

Very happy that when I bought my first home last year that I:

1) kept 30% of wealth in global equity markets

2) shorted treasury bonds to hedge against inflation & interest rate rises - to me at the time this seemed like the only real risk to house prices that could eventuate. It certainly has now! Fortunately this strategy has paid off by more than the value of the home has fallen...

Not a useful strategy for most. Even leaving aside the financial sophistication required, everyone else has to stretch themselves so much to buy anything half decent that there's no resources left for this sort of thing.

More than a year's worth of capital gains have evaporated

It’s a good start.

Anyone know if the retirement villages have dropped their prices in line with real estate or is the greed kicking in?

I wouldn't be surprised if they have. They typically price units at X% of the median market price in their target catchments.

Interesting to look at new townhouse developments. Some seem to be marketing at prices about 7-8% lower than 6 months ago, but some not.

If the business case was built on land values of 1 or 2 years back. There is only so far prices can drop before profits evaporate.

There has been a noticable surge in advertising by the villages. Spending big on it.

Which suggests they are not attracting customers as easily as in the past. Plenty more villages to choose from now.

So the old saying 'house price will double in every 7 years" will that be 7 years and 14 days now?????

Good to see Christchurch start its dive

Fascinating chart showing NZ housing market as a leading indicator for US housing market. Is it our turn to outperform on the downside this time?

https://twitter.com/AvidCommentator/status/1557887251492716544?s=20&t=A…

HPI graph…..I can see Rangitoto emerging!

50 percent home price falls? In secondhand homes obviously as new build costs are increasing and no builder will work for nothing.

So will section prices tank? Somebody needs to pick up the falling value!

Sections are non-yield earning so in a falling market unless you have paid them off, then they are a real drain on your finances.

Also when people get to the point where they need more money coming into service debt, they have two choices or a combo of, ie lower the debt, or increase the income.

So people start lining up all those things that they now can't use, eg boats, caravans, etc, and/or can't afford to own like sections, etc. with the house over their heads being the last asset they normally will part with.

After the last GFC, up to 2017 I know of sections that were selling at the same price as they were purchased for in 2006 or even some types that were selling at up to 50% less than they were purchased for. And the sellers were glad to get rid of them.

Are you suggesting the build costs i.e. materials are based on what it actually costs? So second hand homes increased by 30% in a year, yet new homes also followed the same lead, but that wasn't due to the availability of credit etc it's because products like GIB somehow became 30% more expensive to manufacture.....not that Winstone Wallboards saw the market increase by 30% and adjusted their wholesale price accordingly?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.