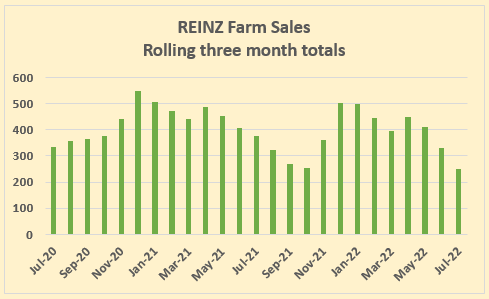

The rural property market is in the doldrums with the number of farms and lifestyle block sales both well down on a year ago.

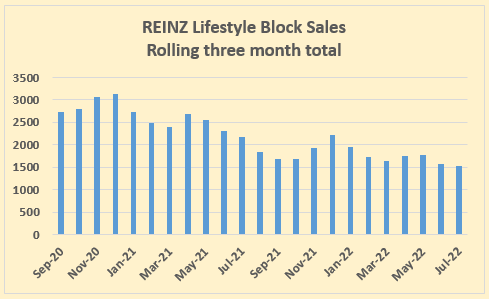

According to the latest rural sales figures from the Real Estate Institute of NZ, just 1518 lifestyle blocks were sold in the three months to the end of July, down 30% compared to the same period of last year.

The decline in sales is no monthly aberration - lifestyle block sales numbers have been steadily declining since late 2020.

Farm sales numbers have shown a similar trend, with just 249 farms selling in the three months to the end of July, down 34%.

The slump in sales has affected all farm types, with the sale of horticultural properties in the three months to July down 55%, while sales of dairy farm were down 39%, grazing farm sales were down 35% and finishing farms down 18%.

The graphs below show the trends in both farm and lifestyle block sales. The slump in sales appears to have affected the prices being achieved for lifestyle blocks more than farms.

The rolling three month median price for lifestyle blocks was $1,015,500 for the three months to July, down by $72,000 compared to its peak $1,087,500 achieved in the three months to April.

The median price for bare land lifestyle blocks was $455,000 over the three months to July, down $55,000 from its April peak, while the median price for farmlet lifestyle properties was $1.2 million over the three months to July, down by $100,000 from it's peak at the start of this year.

However farm prices have been more resilient, with the median price per hectare for all farms sold in the three months to July coming in at $27,220/ha, barely changed from $27,180/ha in the same period of last year.

The REINZ All Farm Price Index, which adjusts for differences in the mix of properties sold by size, type and location, was up 13.9% in July this year compared to July last year, suggesting prices are doing better than the price per hectare figures suggest.

The REINZ Dairy farm Price Index, which adjusts for differences in the mix of sales by size and location, was up 1.8% compared to July last year.

"The combination of the wettest July for many years and the mid-winter temperatures clearly impacted on the enthusiasm within the rural sector to transact, and when the external factors of inflation, rampant cost escalation and increasing interest rates are added to the mix, the outcome was somewhat inevitable," REINZ rural spokesman Brian Peacocke said.

The comment stream on this story is now closed.

38 Comments

Lifestyle block or death sentence block. Its a whole lot of work that people need to do....unpaid.

Ever wondered why ride-on lawnmowers have headlights? LOL

In case another one is coming the other direction silly

Anyone thinking a LSB is like an urban property with a bigger lawn is in for a rude shock. I advise people considering buying one to get used to living in a mess. If you bring in livestock, be prepared to deal with unpleasant and dangerous situations. It's a supremely fulfilling lifestyle if you don't mind hard work, but it's not for the majority of townies.

When it comes to earning income from the typical LSB, it's a lot like motorsport - you can make a small fortune, as long as you start with a large fortune. Once you've got livestock and/or crops onsite, you need most of what a larger farm needs in terms of equipment, albeit not so large. Your accountant will likely treat himself to a new boat too.

No need for an accountant unless incredibly serious, maybe involved in hort

You can lease out your land for horticulture rather than doing it yourself. You trade off size of income for security.

There's plenty of ways to skin a cat. More options than a 1/4 acre anyway.

You can, but only if your land is suitable, including being large enough. We lease out for cropping, however there's the other 7 months of year to take care of as well, which is why we graze over the off-season.

Wouldn't swap our LSB for town living. Yes there is a lot of additional effort involved and usually a longer commute, but the rewards are well worth it. For me, it is no neighbours, an abundance of firewood and meat that I know exactly how it was reared and dispatched. Mostly though it is the ability to connect with nature and improve the land through tree planting which benefits the wider public through carbon sequestration and visual appearance.

Any thoughts?

At the moment, the market is going down at all levels.

We left Auckland some years ago and are renting out our Auckland house. We bought a house here in the provinces. Whilst we have lovely tenants in Auckland and a good relationship (Christian family, low rent), it is increasingly cumbersome being a landlord. I am interested in buying a piece of land here in the provinces, to hunker down, so to speak. Our tenants have indicated they want to move to Australia next year.

My Auckland neighbor has offered to buy our house in Auckland, with a nine-month settlement term (May 2023). He is an investor and owns both properties around ours, so buying our house would give him about 5,000 sqm of land in a big rectangle. He therefore offers a price (unconditional) that is about 10% above the current market price. He says he needs a long settlement so he can sell two houses to buy ours. This seems plausible, I know he is highly leveraged.

It is not easy to sell our house on the open market. I spoke to a real estate agent, it does not look good. Whilst our tenants are lovely, the house has been run down a bit since they rented it two years ago. They live there with seven people, we used to be three people. Also, I would have to give 90 days notice, then renovate, and who knows what the market may look like in three months.

So my neighbor's offer is tempting. But my concern is this: If I sell now for today's reduced prices (significantly below peak) whilst looking to buy land in nine months, I am effectively going short on the property market, i.e. I would be betting on prices to fall further from now until May.

How likely is that?

My worry is: The housing market and the economy will crash in the short term due to the OCR having been hiked up too much, then the RBNZ will come in with massive amounts of QE or lower interest rates to pump the system back up, to catch a collapsing economy. As usual with the RBNZ, too late, and then heavily oversteered.

So, I would be shot in the foot twice: I am now suffering capital losses from falling prices (selling at today's prices), then when the time comes to buy land in nine months, I might be facing heavy inflation, higher prices and another bout of FOMO, especially for rural land here in this lovely region (which is becoming a so-called ZoomTown).

I am not very speculatively minded so I would normally be hesitant to go short on the housing market, especially with a large amount. Of course, if prices would fall further, I could benefit from all this. Although I think in this case my neighbor may find a way to wiggle out of an unconditional contract, not sure...

Any constructive and helpful thoughts would be appreciated.

I personally think the days of low interest rates have gone. I’m hoping the reserve bank has learned a massive lesson about over stimulation. Based on that… I’d say the up cycle of the property market is years away. I’m also hoping the government (both of them), are seeing the difficulties that come with in affordability and crazy high prices. I think the landscape will be very different moving forward… even if National win. Property will likely fall another 20% and then stagnate for 2 or 3 years. Just my opinion, base your decisions on what GOOD advice you can get. Please don’t listen to the FOMO spruikers out there, get someone impartial and informed. Good luck

Markus, if you don't ever think you'll go back to Auckland, then maybe sell it. Just on the proviso you may never be able to go back - likewise you may never get the opportunity to borrow for another rental again (nor would be motivated to, from the sounds of it).

If I were you, I'd be looking to sell Auckland and invest in some sort of income producing property where you are, a farm, some sort of industrial/commercial, that sort of thing. There aren't many bargains out there though, you'd probably need to buy a project.

I personally think the days of low interest rates have gone.

I think they're hiding, but at some point the state will pull the lever again in times of need. Might be a few years though.

How many more times they can do it is anyone's guess, but probably a couple more.

Thank you, dear all who who have commented so far, this is highly appreciated!!

God bless!

My worry is: The housing market and the economy will crash in the short term due to the OCR having been hiked up too much, then the RBNZ will come in with massive amounts of QE or lower interest rates to pump the system back up, to catch a collapsing economy. As usual with the RBNZ, too late, and then heavily oversteered.

I wouldn't think that would happen over the next 9 months.

I can't see any actions that would save the housing market. Either the economy is doing OK, unemployment is low, in which case interest rates stay as they are or go higher. If there's a filthy recession that causes the RB to unleash another round of easing, unemployment will be high, there'll be mortgagee sales and lack of income to leverage up on property.

I guess maybe National could think of a few more stimulating measures should they get in, if increasing migration and removing Labour's tax changes don't do the trick.

while I too believe the powers that be will resort to QE again, that definitely wont happen before inflation is back in the band.

You are best to sell the Auckland property if you can, nobody knows where the bottom of this Akld market is but as I keep saying, its reasonable to expect the excesses of the last 2 years to be unwound which would mean a 35% drop from peak

Oh and BTW there is no guarantee that the developer will complete the contract, so if you take that option, insist on a high deposit, like 20%+

This is a No Brainer surely

Take 10% above market value now and you are getting top dollar.

Buy 9 months from now and enjoy at least another 10% drop in values by then, it is win-win for you just on that, plus your tenants are leaving anyway and you dont have to spend any money on reno. Just Do It

Always had a hunch you were a landlord there Markus who was afraid property prices might fall, impacting the value of your property portfolio - hence why the vocal attacks on central bankers raising interest rates.

If you are concerned that more QE is inbound, then we will need to have high unemployment and/or risk of deflation. Either way, I think you will be more worried about holding onto your job at that point, than where house prices are at.

One thing I learned from the housing bubble burst in the GFC in the US, is that if you are going to make a decision, make it before the masses realise what is happening.

... don't let the door hit you on the butt ... head out the exit well before the sheeples wake up & some twat yells " fire ! " ...

IO, you are misrepresenting me a little bit here. Yes, I have been worried about the sharp interest rate hikes, because I think this has the potential to destroy our economy.

Under the specific circumstances, please note, I would actually personally benefit from falling property prices over the next nine months!

That said, I agree with you, if we are facing a New Zealand GFC, we will be worried about jobs etc.

Who knows what may happen, the market may go down or up from here, the market turning back is now my personal risk.

But the wider economy, I definitely think the RBNZ are tinkering with it and I am very uncomfortable about this.

For your circumstances, I know of friends who have just sold their house in Auckland an intend to rent for the next year so see where prices are at.

For them, they've decided that the market is going down and they will look to buy again next year.

Its a big risk, but each to their own. If its comes off, they could be set for retirement....if it doesn't....well thats the risk huh...

But if that becomes a more widespread pattern of though/narrative, then such as it was in the US when I was there, fear turns into panic as people everywhere try to sell up their investment properties....people acting in herds...crazy stuff.

Yes, this an ever bigger risk than I am taking, the risk being that the market may go up again. Thank you for your insights into the U.S. after 2007, very helpful. Thank you to all others who have commented here as well, I have carefully noted each single post.

God bless!

I would exit now if you can. The fools who buy now are going to eat it when we get more property taxes + hit hard economic conditions. Rent Yields aren't going to push much higher, no one wants to pay 750 a week for a shitbox.

No sympathy for landlord boomers getting rekt by the market for drinking the blood of the productive economy to enrich themselves. Pray to the money god for deliverance because this market isn't going to give you anything. Current interest rates imply a 40-43% price reduction for equivalent weekly payments.

@Markus Just sell it, before he becomes bankrupt. You not gonna get Stupid 10% plus offer.

Markus, forget about what the market is doing, you're not selling the market, you're selling one specific house. Anyone telling you to make a decision based upon what the market is going to do, firstly doesn't know for sure what the market is going to do (although they think they do) and more importantly, they are armchair, popcorn eating commenters who have not actually bought/sold anything. Make your decision on your house in Auckland and the price you're getting for it now, the rest is guess and fluff. Just make sure your S & P Agreement is tight (checked by your lawyer) with the late settlement, and don't accept it without a 10% deposit now, so that if it all turns to custard, you still keep the 10% deposit.

Good luck

It's hard because on one hand, anyone with any experience in this realm is a spruiker and biased, but anyone who's not, probably doesn't have much alternate success in anything commercial.

Dear all who have commented, thank you so very much, I have read every post with great interest. I still feel very uncertain about all this, as I do think the USD and consequently the NZD is at risk of going to custard within 9 months, and also my buyer has only offered a minimum deposit (has no cash before selling). I will speak with my lawyer on Monday (she has been on leave), then make a decision. Once again, I very much appreciated all your input. Stay strong in these difficult times, and God bless!

If the developer looking to buy your place is highly leveraged and needs to sell a couple of properties to buy yours, there’s a decent chance he’ll be wiped out by middle of next year….

I'd sell it now and put the leftover money in some good rate term deposits available now. There's 4, 5 up to 7% (depending on amount and length) available at the moment.

we bought a lifestyle block in the early 80s,cleared the gorse and fenced it.we raised the odd bobbycalf,a few sheep,goats,chickens.laid down some good memories for my four kids and sold it for 3 times what I paid for it.but yes,dont buy one if you are workshy!

Yeah if you want easy living, a lifestyle place isn't a larger version of a terraced house with a patio.

Free entertainment though, otherwise you'd end up with a money pit like a boat or something.

You can arrange it to be lower workload if you desire - buy a bush block without grazing, or lease your paddocks to the farmer next door.

Misquote of the month

'the rural property market is in the doldrums"

Sure farm sale numbers are down - but I'll bet a box of beer to a doughnut every single farm about to come onto the market will be at a higher price than 2 years ago. Some farms will be up in value 50% or more in 2 years. Partly demand by carbon farmers but also confidence in dairy long term. Where is the gloom when rural service providers such as PGG Wrightson and Skellerup make significant profit upgrades?

The reason for the lack of sales is mostly because farmers are making good money on the back of record commodity prices and don't want or need to sell. How bad is that?

I agree! The bottom of the market has been laid down by the carbon investors.

My mates prime waikato LSB has been rezoned to resi from rural. He will grow houses on his land

Lamb market rather than Ram market?

Clever is it a play on ram raids. Btw ham market is an option

There are currently a lack of listing, I own two finishing blocks, I have agents and private people asking and making offers constantly....my urban house has dropped in value…statistics in the aggregate hide the real reality…quality listings are in demand snd selling for a premium.

Where and what size

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.