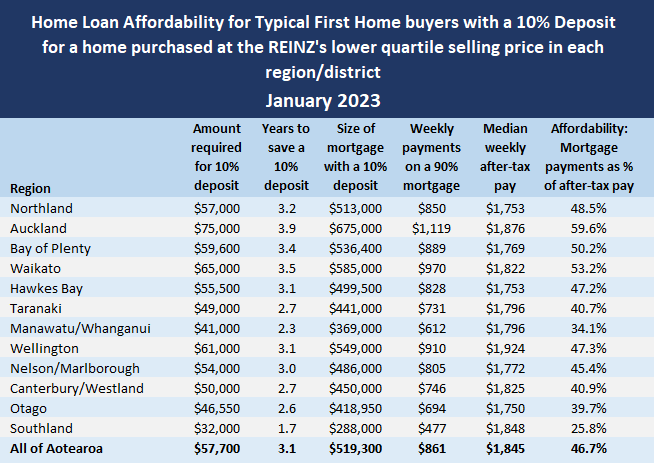

A dramatic fall in house prices at the bottom of the market last month considerably improved the prospects of first home buyers, according to interest.co.nz's Home Loan Affordability Report.

According to the report the Real Estate Institute of New Zealand's lower quartile selling selling price dropped substantially in most regions of the country in January. The biggest fall was in the Bay of Plenty where it declined by $96,000 (-13.9%), falling from $692,000 in December last year to $596,000 in January this year.

The lower quartile is the price point at which 25% of the sales in a month are below and 75% are above, representing the most affordable end of the market that is of most interest to typical first home buyers.

Following close behind the Bay of Plenty was Manawatu/Whanganui which recorded a $70,000 (-14.6) lower quartile price drop in January from December, followed by Auckland -$62,000 (-7.6%), Nelson/Marlborough -$42,000 (-7.2%), Southland -$31,000 (-8.8%), Taranaki -$30,000 (-5.8%), Wellington -$27,000 (-4.2%) and Canterbury -$20,000 (-3.8%).

The only regions where the lower quartile price increased in January were Waikato +$50,000 (+8.3%) and Hawke's Bay +$15,000 (+2.8%).

The latest drop in prices means there are now six regions around the country where the lower quartile selling price has declined by more than $100,000 since prices peaked in November 2021.

They are: Auckland -$216,000, Bay of Plenty -$104,000, Hawke's Bay -$107,500, Manawatu/Whanganui -$105,000, Wellington Region -$165,000, Nelson/Marlborough -$117,000, while the lower quartile price decline in Otago is just under $100,000 at $99,500.

Nationally the lower quartile price has declined by $93,000 from its peak in November 2021.

As well as benefitting from lower prices at the bottom end of the market, aspiring first home buyers were also helped by the fact that mortgage interest rates did not increase, with the average of the two year fixed rates offered by the major banks staying at 6.58%, the same as it was in December 2021.

However that pause in interest rates may not last much longer, with the Reserve Bank set to review interest rates on Wednesday.

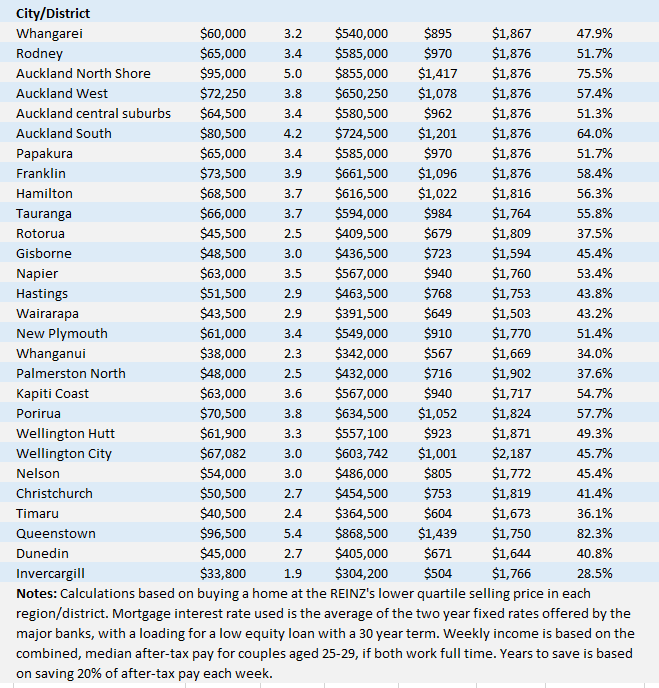

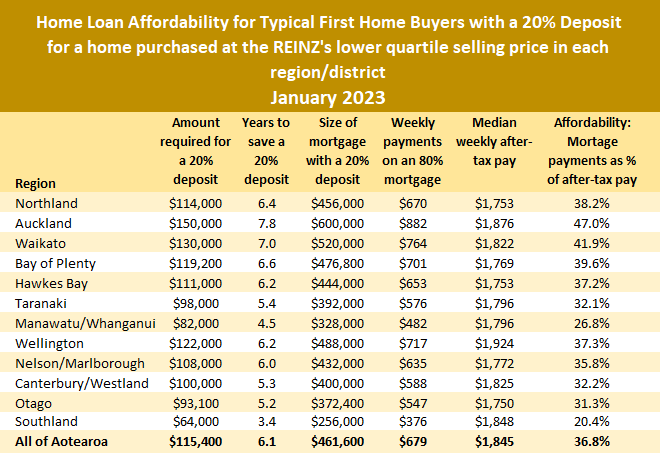

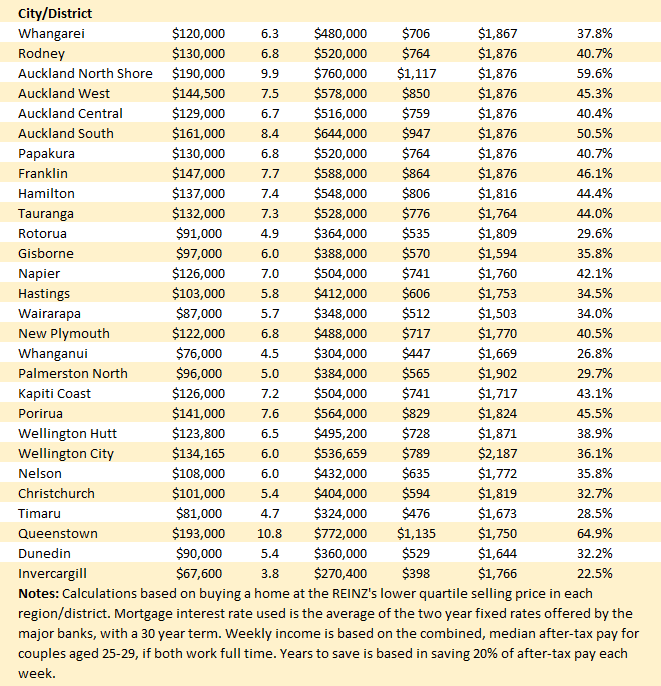

The tables below give the main affordability measures for typical first home buyers with either a 10% or 20% deposit, by region/city/district.

172 Comments

Alas, we’re never likely to achieve the utopian state of cheap house prices AND cheap mortgage interest rates. ☹️

TTP

New Zealand prides itself on being a lousy value proposition. That's why the best and brightest inevitably seek their fortunes abroad.

You know it's serious when Brock doesn't use the airplane and tick emojis.

I was so hoping both my kids would return from london to NZ this coming year after completing some further education. They are now telling me they will settle somewhere more affordable and financially secure. It’s so sad.

... if more people broadened their horizons from the tribal " I'm a Kiwi " to " I'm an Earthling " , a whole world of opportunities would open up to them ( I'm currently happy in Manila ! ) ...

Over the last decade New Zealand seems to have been on a crusade to try and make London look comparatively affordable.

Why are you still here?

So mortgage rates at 2% and LVR's at 0% for anything but a sole home per IRD number wouldn't do it?

It's not about 'the price of Debt', as such, but access to it and how it's allocated that's the problem.

Does a trust have an IRD number? Are there any trusts that own more than one property?

Trusts do not need to register with IR if they are not deriving income. Trusts can own multiple properties. If a trust rents a property it owns it must register with IR and return the rental income.

See https://www.legislation.govt.nz/act/public/1994/0166/latest/DLM6661704…

Surely an IRD for a trust will have a different identifier than say an Individual.

No, but cheap house prices and high mortgage interest rates are a much better option.

If rates stay this high then house prices will drop until affordability returns.

Yes, and the benefit for FHBs buying at (relatively) lower price and higher mortgage rates is that future repayments have both upside and downside risk, not only downside which was the case buying in 21. So while current affordability is worse, future affordability is better, and 30 yrs is a long time…

Having said that, this data simply confirms that prices have substantially further to fall given that neither FHB nor leveraged “investors” can afford current prices.

Throw in job losses galloping over the horizon, and it's all looking peachy.

It should have got to this, but it has, and the question that is about to be answered is "Who is going to lose from the residential property market? Current Owner or Future Ones?"

And given that Future Ones are being squeezed out by the day, that just leave one cohort - Current Owners.

Who needs buyers anyway...

Just sounds like sellers not meeting market to me. There's buyers out there but they're waiting for realistic asking prices

To me they're not expecting anything. Banks allow them to borrow X when lower quartile houses are worth 1.3X, FHBs still do as usual, that is taking the biggest mortgage they can.

So either mortgage conditions/incomes improve or sellers meet the market.

Not always the case, prices may be at 1.3X but some FHB can afford 2.6X and waiting for a 3X to become 2X...

The Labour Government could do a lot for their election chances by mandating that our "building systems" be brought inline with the USA and opening up for import. New Zealand is not special and we do not need custom-designed (read: expensive) anything.

Its actually the opposite, our "custom designs" are to make it cheaper. For example we use Gib for bracing which is very unusual, so our Gib has to be certified as a bracing element, theirs is just certified as a wall lining. Our cladding is the main waterproofing, in the US they seem to have another layer of ply or similar underneath.

Our 'custom designs' mean it's difficult to make at scale the big-ticket items like windows, because there is no standardisation for manufacturers to rely on.

Standard stick builds in North America is siding, then building/tar paper, then structural chipboard/plywood for shear strength, then insulation and framing.

Correct, so any money we save on cheap US plasterboard we would then spend on structural chipboard etc. Of course it makes a better house in the end though.

Do USA homes leak like ours?

Great article clearly showing we're nowhere near the bottom!

Buckle up.

Probably see some momentum building after Feb 22

Pardon my ignorance, what happens on Feb 22nd?

The bottom of what ? The toilet ? House prices come down, interest rates go up. The whole point of the article is you are no better off, at least not in the short term so you are buying with the hope that interest rates fall significantly again. Could be worth a gamble it depends if the RBNZ starts to cause high unemployment and your job goes tits up or not.

a dropping house price is only good if one does not need to borrow to buy, the cheaper house the better.

for most, be that FHB, SHB, investors-needs-to-borrow, they are screwed, as they are not in better position anyhow.

it's the mortgage lenders that bank the most.

Correct, I know of a few that have use the low interest rates to finish their mortgages off and will be debt free and an asset behind them (although that asset may of fallen in value) but debt free, with some cash reserves and good jobs. So for them if they looking at picking up another property or entering as an investor it's going to be about picking the bottom, hit it just right as interest rates start falling again. So some will be liking what they see.

Therein lies the issue. The one road to elysium, landlording.

A large percentage of the population are beige beyond belief.

It won’t be too hard to pick the bottom as there will be no bounce…will be flat for a few years as so much equity will have vapourised and banks will be more cautious about lending as they’ll be carrying significant bad loans by then

Houses are illiquid and it takes a while for price discovery to pan out. Houses have a way to fall yet to bring us back to the same level of affordability. In short, prices will fall further even without more interest rate rises.

What these assessments always miss is that the cost of home financing is not static.

First time homeowners who bought a year ago are definitely not in a better position than the current cohort as their repayments have also increased; especially if they were fixed for only 1 year.

In laymans terms; if you sign a cell phone contract with the first month at $10 and the next 11 months at $100/month you are definetely not better off than the person who is now being offered a contract at $80/month for 12 months (even if your first month was cheaper).

I'd rather pay less at a higher interest rate (as the rate is more likely to come down) than more at a lower interest rate (where the rate is more likely to increase)

I'd rather have a smaller mortgage with a higher interest rate because any payrises for the duration of the mortgage term take a much bigger chunk away from the principal amount. 30 year mortgage:

- $500k @ 8% = $846 per week

- $820k @ 3.5% = $849 per week

Say you get ONE $200 p/w pay rise and that's it forever. So you increase the payments $200 p/w. The $500k is gone in 17 years, the $800k in 22 years.

You are better off with a lower mortgage and higher rates because as your pay increases you can really start tackling the principle. If your mortgage is $200k and you pump an extra $20k a year into it you will pay it off much quicker. If it is $1mil and you pump an extra $20k a year in you won't make much of a dent.

I know this as we are pumping almost 3x the minimum payment into our fairly big mortgage and it barely feels like we are getting anywhere compared to when we did the same (but less) with our first mortgage 15 years ago which was lower value but higher rate.

According to the Home Loan Affordability Report, housing is now the most unaffordable it has been for first home buyers since interest.co.nz began compiling the report in January 2004.

Yet they still keep buying. Owning ones home is a pinnacle for many. The country really should do something to make it easier.

Easier like dropping house prices?

Easier like rapidly increasing supply at cheaper cost.

Labour had a Kiwibuild election policy in 2017 to scrap the Auckland Rural/Urban boundary, that could have done both of these things.

Labour was of course lying and did not implement the policy.

Councils stacked with greenies, stick their big noses into everything, end result no affordable houses for the working population.

I am glad the central govt has given councils a huge wake up call, with the housing supply amendment, and forcing them on the back foot

Easier like stopping parasitic speculation...sorry i meant 'investing' of course.

yep ban the investor bludgers who often funnily enough complain about dole bludgers getting paid for doing nothing...they also sanitise the scam by calling them 'mum and dad' investors...thats where government policy steps in and says "20% CGT on sale of second house, 30% CGT on third etc up to 100% on number 10 onwards...that'll fix the housing drama...I'll put it to Luxon...

Yawn said all this months ago along with the house prices not dropping as much as everywhere else in the country down here in Tauranga. So 60% of your pay to get into the club down here now, been there done that in Auckland years ago on a single income, its not fun.

Yawn all you want buddy, basic maths and inflation don't agree your precious TGA, or any of the market for that matter

"Here comes the aeroplane". (Like a toddler being served it's medicine)

Oh its starting to happen though. Been sitting on the sidelines for nearly a year now and am just starting to see a lot sit stale and some capitulating. There are 3 relatively similar properties on the same road not selling. One has just dropped price substantially from the pack...

At least the poor affordability will prevent some FHB's from entering the market now and getting burnt.

And herein lies the betrayal of ordinary kiwis by their politicians. it is in my view criminal that we no longer view housing as a basic human necessity, that a minority of people and business's can hold the rest to ransom, and that we condemn current generations to this level of pain.

the interest rate jump not only pushed away the current FHB, but for the was-FHB in the past few years, their down payment value has been wiped out too. I can appreciate many would feel stressed, even fear.

screwed.

FHB just need to hold the line they are not screwed. Its all about what sort of industry you work in going forward. As long as you stay employed you can adapt. You just have to change your attitude and get a flatmate or two like in the old days for 5 years or so. Most people these days only pull their heads in when they are forced to.

A FHB of 2022 who holds on until 2027 will have equity, where as I as a renter had 0 last year, 0 this year and will have zero in 2024.

I may even have a rental increase to look forward to maybe it might go from 44% of net pay to 50%!

Some reasonably priced rentals that arent a bed sit on trademe in the hutt valley have 250 watchers, that is not a good sign.

What about an FHB in Ireland 2007? When did they get their equity back?

I don't remember any of my parents friends having flat mates? And most of them were single income families as well. So yes having a new family and a couple of "flatmates" sounds like a winner?

What was the house like though. My parents friends bought boxes in new suburbs in Auckland where fairly small starter houses were probably finished inside but not always. The suburbs were known as "nappy valley" because they had to wash their kids nappies and hand them outside on the washing line to dry. No disposables and no clothes dryers. And none of the landscaping, driveways, paths or garaging was done. That got done when they had the money/time and usually with bit of help DIY style. That just wasn't fair to expect that of young people.

Yep try stuff like the old Keith Hay homes, even new builds would have people these days turning their noses up, wouldn't even make a beach batch standard these days.. Everything has changed people even want ready lawn and the house fully finished. We pretty much built the house when I was 17.

That was the type of house we bought for our first home. Stretched really far to get it too. But by being very tight and getting pay rises and promotion was able to put a garage in and concrete the drive. Bare bones projects though, did all the labour myself.

So you bought a new house for your first home?

Hell no! Third or fourth owner. The previous owners had done very little with it. The one before us put a decking on the front, but that was all.

True. So where do these houses exist today, that come partially unfinished so one can buy at a discount?

Does anyone have a link to StatsNZ tables where

- The combined median after-tax pay for couples aged 25-29.

is reported?

Cheers

Nearest I can find is in Infoshare, you go 'Work Income and Spending' -> 'Linked Employer-Employee Dataset' -> 'Sex and Age Quarterly', then you can select by Male/Female, Age bracket, what sort of earnings you are looking for and the time period.

Thanks!

I think it's wrong to define "affordability" as "ability to make monthly mayments". It's this thinking which got so many people into trouble when interest rates were low.

Agreed. You live a pretty miserable life but still make mortgage repayments. Whether you have adequate insurance, cash savings, retirement savings, a safe car for your family can all become fairly secondary a time when inflation is spiking food costs and interest rates are racing ahead, but on paper it all looks hunky dory because the mortgage payments look doable.

The editor of this website dislikes them, but I still think median multiples have a lot of utility.

It all comes down to supply and demand. If demand outstrips supply then people will have to pay as much as they can to beat the next person, and the amount they can pay is dictated by interest rates. Median multiples only seems to apply in places like some of the US with either low demand or high supply.

This is excellent news for the future sanity of the nation. Who knew that taking on million dollar mortgages at hysterically low interest rates on massively overpriced houses on average incomes might end in tears.

When a greedy 60 year old ( not being ageist but it's the common theme in NZ) wants a millon plus for a house they bought for 300k, then what hope does a young family have in this country.

You can hope when you reach 60, you sell your properties at 2 million $$$.

I'm sure ngutora will sell his house for the same "cheap" price he bought it for, 30 years earlier, because he's such a good guy, lol.

I don't buy to sell (period)

So you, or your estate, are never going to sell?

I think he's is very young and inexperienced, he doesn't understand that circumstances in life change, kids, divorce, career, upgrading to a better house etc...

I was not going to respond as i said period but young and inexperienced got me 😁😁.

Experience starts when greed is diminished. Otherwise mind is always clouded with wanting to have more and more.

Always buy after great thinking about how much you would need so you don't waste. So yes I don't buy to sell and if planned properly and with intelligence there would be no need for your estate to sell too. Also Need to ensure the next generation is also taught to swim before sending them into the Rip.

Without elaborating too much. I would say period.

oh well, the whole capitalism is built upon greed, while socialism is built upon super-greed.

I don't think greed will go away because you, or any of us, dislike it.

Experience starts when greed is diminished

Weird statement, experience has absolutely nothing to do with greed. Experience is simply living through an event, good or bad, and hopefully learning from it.

Doesn't matter what they want. What they are going to get is another matter altogether! Any market takes a willing buyer to match a willing seller.

Personally I can't understand why a rout hasn't occurred.

Duplicitous politicians and unaccountable, poorly performing central bankers wrote very big cheques to stop it happening at a time where it might be their problem. All well paid, I might add, at much higher rates than the average wage of the people who about to take the pain they have created.

No consequences, no mercy.

Totally agree with you.

When a greedy 60 year old ( not being ageist

Errr, yes you are being agist, right there!

So for Auckland FHB the current proposition is to put at risk 80k of yours or parents money or Kiwisaver or some combination of all 3. But real money none the less. To buy an 800k Sbox and pay 1200 a week plus outgoings to live there. When you could rent the same sbox for 6-7 hundred per week and save $500 week or just have a life instead. Meanwhile that Sbox you are renting is depreciating $1000 per week.

Why o why would you buy?

For the warm feeling of being on the ladder. hahah!

That's fine but don't whinge when you get older and are still having to find the rent when others are then mortgage free, quit work early and start having the life they planned on having.

And pay for it with what? You've tipped the money you earned over an entire working life paying down the mortgage. What do you retire on?

Superannuation and kiwisaver.

Plus of course you'll save more once the mortgage is paid off.

Dont wait for forever. 12 Months might do it. Just wait for signal that interest rates could be cut in near future and then start the house hunting process. In 12 months you could be $25000 in cash better off (than paying a mortgage) and your prospective house will be cheaper than it is now.. Just by waiting. Buying only makes sense when you have some capital gain to offset the interest cost. The government of the day will want a return to long term consistent moderate house price rises when they have the ability to engineer it again.

That's what we do in New Zealand.

Just wait for signal that interest rates could be cut in near future and then start the house hunting process.

While this sounds ideal, the second this sign is apparent all of the investors will pile in and then the chance of FHB’s getting the house they want will be diminished from once again competing with and getting outbid by those who already have multiple properties they can use as ATM’s.

The narrow thinking in this user is astounding.

Yes, you could use your deposit and savings per week to fund your lifestyle and retire early, while people are slaving away paying the bank.

A lot of noise and not a lot of action thus far across the board.

NZ falling faster then Ireland..... but its not a race.

There will be a lot of cheap townhouses for sale later this year. Builders will slash margins to survive. If I were a FHB I would be getting ready to pounce. It's not a 1/4 acre, but it's a start. I can afford a house 2-3x the value of the one I live in now. When I bought it I couldn't. You have to start somewhere.

I suspect that many of these developers are making more than 65% margin so i would wait for huge discounts. 50% discount?

25-30% is the norm.

If they are happy to reduce to say 10% in order to shift their developments then that might knock 15% off the sale price.

We got a townhouse as our first place too (admittedly a better-than-Williams Corp one, in both size and spec, but still plenty of our peers thought we were brain dead for not buying a doer-upper on a big section).

Guess who never has to spend their weekends mowing the lawn or queuing up at Bunnings to buy more DIY supplies?

Guess whose house is warm in winter and easy to cool in summer?

Guess who can get to work in under 10 minutes on bike due to living right on the outskirts of the CDB?

I agree that they are a good way to get started. Still overpriced in the current market, but relatively less so and townhouses could be the first to move bigly price-wise if the cracks widen.

Me too. With all the same benefits.

As long as you get a semi-decent one that is well designed and built well, and well located, I think it’s a good option. And as I say above, could be some good buys this year.

I agree. 2 bedroom townhouses advertised at 850k now might be 700-750k later in the year.

And that would still be massively over priced for what they are! I have looked at a number of town houses in Akl and they are consistently of average (at best) quality.

The greedy property investors in New Zealand with multiple rentals especially the boomer landlords have a lot to answer for. Some will hardly ever see their children and grandchildren as the children have chosen to live overseas where housing is easier to buy.

That comment doesn't make any sense. The parents can obviously gift or part gift some of their investment houses to their kids and grandkids, so they can all live happily close to each other.

If we live in a world where one couple has only one child. Extrapolate it exponentially and the worth is not much to share.

Well, we don't live in a world where there's only 1child per parents, so that's a moot point.

Zero kids more like it...

You would be surprised just how many parents are not willing to help their children into housing even where the parents are very well off. I am a boomer and I know some like that. Personally I have helped my kids a lot in terms of their housing needs. You helping them means they live in New Zealand and the grandchildren are being helped also. Why have more than you need and your children pay big bank payments.

I’m a long way from that stage of life but there are a few reasons not to:

• It’s an arms race, as with any arms race you only have an advantage if your opponents can’t do the same thing, everyone tapping parental finance just further over inflates the prices.

• The financial proposition needs to stack up, if all you are achieving is “helping” your children to take on more debt that isn’t real help.

But in principle I would assist. I just don’t think you should always assist, especially when the market is overheated. Much better to help now than 18 months ago. And I would help a child now if I had the resources.

Also, parent borrowing against their property is a bad bad idea.

Ha Ha...I'm bloody glad I didnt help. The whole thing was a bank con.

How many parnets are about to end up with a late in life mortgage as their kids default on the zillion dollar S##t box?

Grab cash from anywhere kids, cash up kiwisaver (remember when it was meant to be for retirement), have up your family, beg from anywhere ...you just have to keep this pumping for the banksters profits!

When this market has some sanity I might change my tune...but by then the family will be well positioned.

Don't bet on it. Trust me these are the same type of people who will sit on rental income not working and deny their crippled children housing when they are homeless, then call the crippled kids who look for work lazy behind their backs and to their faces. Who will try to take as much advantage of benefits and subsidies and government handouts but will then turn around and abuse said disabled children who cannot even access income support as being bludgers... It is a type and in NZ the kiwi way is the 'I have got mine jack screw you' type. The type that never learned about ethics in school. Don't worry our politicians and government department managers are the exact same type, cut from the same cloth. Except with more capital than most. hypocrites, liars with excess greed and only interested in growing their slice of pie while cutting those who are truly vulnerable of basic human rights. It does not take a genius to see that they only do things for vote winning and to secure lifetime benefits that mere mortals of general public cannot access. Sadly though the vulnerable are dying younger as they are being further crippled at such a high rate in comparison.

I get the point of this analysis and it’s valuable but there is short term and long term affordability. Short term affordability is a mirage. This guy knows that long term affordability is what matters but he bought based on an assessment of short term unaffordability.

https://www.nzherald.co.nz/nz/brings-tears-to-my-eyes-family-consider-s…

When prices go down relative to incomes then long term affordability has improved unless we know something about future interest rates which we don’t. If the last few months have taught us anything it is dangerous to make assumptions about future rates other than a broad historical average.

Exactly. Interest rates (2 years and longer) have almost certainly already peaked. I don't believe the neutral rate is as high as some would have you believe, although it's likely somewhat higher than it was a few years ago.

Analysing affordability against transient, abnormally high rates is not particularly helpful, except as an explanation for the gap we currently see between buyers and sellers.

We have reached peak negativity. Things are starting to turn positive, despite the best efforts of various naysayers and permabears. The market will likely bottom in the next few months as it becomes clear to the masses how interest rates are really driven. I'm not trying to convince anyone, just laying out a prediction.

Abnormally high ? Where they are now is normal, they were abnormally low.

The only thing this indicates is that the house prices still have a longgggg way down.

I agree. Affordability has actually been reasonably constant until this point. House prices have gone up as interest rates went down, and now we should expect the opposite.

How do you get a wage/price spiral if your income only rose 2.1% after tax?

As a renter I'm happy to leave this cooked market for you all to enjoy. :)

It's hardly an in-depth analysis article, using what is 'Lies, Damn Lies and Stats. facts.'

The main point is the purchase price debt is locked in, but the price of finance is not.

People are already paying debt on negative equity if they purchased 1 to two years ago, and their interest costs will double for many of them.

They are the ones that will be paying a high price and interest costs, They are the ones with the most unaffordable housing.

Things would always get worse before they got a chance to improve. There is no country in the world that can painlessly unwind from the bust following the boom.

But the trend (for any future FHB) is your friend as you will be able to buy at the still-descending bottom, and interest rates will fall.

What needs to happen, and what I want to hear from the Political party's policy, is when prices are at their bottom, and interest rates start to come back, how they will remove supply restriction so supply can keep up with demand and not cause another speculative price increase.

Lucky the interest rates/house prices only affect around 3.5% of homeowners in a meaningful way, or else the government could be in trouble.

You gonna cite the author of that work? Aka Granny Herald.

Given that both major parties are committed to the immigration/property price ponzie it is never going to improve.

Accordingly young first home buyers are very unwise to remain in New Zealand in the vain hope that at some stage things will change and they will be able to afford their own decent sized home. For many, this will never happen and all that they will experience is increasing bitterness as they enrich the landlords.

By far the best option is to leave New Zealand. Immigrants are very unwise coming here unless they have few skills and are desperate. There are far better options.

Given that both major parties are committed to the immigration/property price ponzie it is never going to improve.

Caught between a rock and a hard place. Immigration and the ponzi are symbiotic. Without both, the whole charade runs the risk of turning to dust.

And here is another thing.

At the end of the day it is the employers who have to pay for these stupid housing costs through wages or taxes. The money cannot come from anywhere else. Even if either the worker or government borrow, it still must be paid back from the income from the productive sector.

Employers as a group would be far better off not screaming for more cheap immigrant labor, who only add to housing demand and costs (ultimately from their pockets) and instead concentrate on increasing higher productive out put from our existing population and lobbying the government for cheaper housing. It is only going to hit the pockets of the property investors not the productive sector employers.

The National party are not really a business party. They are a party that is really only there to support non productive fixed asset investors. Labor are really not a lot better.

Not only that, employers are paying company tax, collecting and paying GST and all the other stuff that goes with running a business.

Meanwhile the property investors up until recently got a free ride and pretended they were businesses too.

This is with a combined salary, what happens if you split up or have a baby. 30 years ago rates were higher but you could still a afford to purchase on your own. The houses are way overpriced, another 30% drop and we could see average wage couples have a chance of buying a home. Unfortunately many who are over leveraged will start to come under huge financial pressure when they have to refinance.

The world is full of "What if's" like if the most wealthy top 1% only paid an additional 5% tax it would stop all the starving in the world, but will they ? No. Houses are not going down another 30%.

You may have to eat your hat on that 30% before 2024.

What’s stopping them?

but another 25% is doable???

House price’s will continue to fall until average wage couples can purchase. Carlos I am quite sure you don’t understand financial issues you are one of people who cannot grasp that the house prices have already fallen 20% in many areas and this is just the start of the crash. I you over leveraged because you seem worried that price’s are falling.

about 70% of the households already live in their own home in NZ, this means average kiwis either don't need to buy, or already can buy.

house prices have dropped a lot as you mentioned, all because interest rates change, not demand. as we are approaching end of rates hiking, I'd say house prices is close to its bottom, if not already there.

as for over leverage, there isn't any wave of panic sell yet, I'd say they are alright at the moment. Though there may be more stress sells later this year perhaps.

You've got it. Interest rates have already peaked (all but the very short/floating end).

I believe the bottom will be established over the next 3-4 months. I've been waiting a long time to say that with any confidence. I'm neither a bull nor a bear, just a data-driven realist. Let's see how wrong I am...

There's a veritable kournikova of reasons might need to sell or move. Divorce, ill health, career setback or transfer, pregnancy etc. Just because you own a house now is not an assurance you're 100% fine even if you have a low rate locked in.

He's basically TTP 2.0

Desperate to ignore the math of the situation, desperate to convince greater fools to prop up the printing press just a little longer even with extreme inflation and an imminent deep recession (23/24) definitively putting the final nail in the coffin of this market.

It's quite amusing.

I think its really important for me, to let you guys know that I don't come here for financial advice in the comments section because if I did I would be screwed right now. I'm here mainly for the human psychology and thought processes, it makes for an interesting insight into the way society is trending.

I think it's really important for me, to let you know that your drek is highly transparent spruiking dressed with faux objectivity.

As for the whole "human psychology" sure mate, you're "above it all"

You aren't influencing anyone, let alone the market direction. (Gravity will do that for you)

Carlos will have you know that his IQ is "125".

He's gotta be yanking your chain there Brock. IQ tests include maths and logic.

Constantly saying that will not make that so. There is a strong case for the covid 2% stupidity rate boom to be rolled back completely and then some, so 30% is not impossible.

If I had a mortgage I know I would rather have low house prices and higher interest rates. With lower house prices you can benefit from a large deposit and there is incentive for paying down the mortgage quicker. With crazy low interest rates like we have had it just encourages people to live beyond their means and end up in the insane debt spiral we are currently experiencing.

30 year mortgage:

- $500k @ 8% = $846 per week

- $820k @ 3.5% = $849 per week

Say you get ONE $200 p/w pay rise and that's it forever. So you increase the payments $200 p/w. The $500k is gone in 17 years, the $800k in 22 years.

The $200 goes to food and water. You can't live on oxygen only.

Come on, it was a simple mathematical example. I'm surprised you didn't come out and say "B-b-b-but interest rates won't be 3.5% for 30 years, you can't get a 30 year fix in NZ you dummy" etc.

The problem comes when the 820k goes from 3.5% rate to 820k at 7.5% rather than 849 per week it’s 1320 per week this is what happening now as people refinance and only just at matter of time before crap hits the fan.

even if you super cut back on expenses and can meet the bills/mortgage etc you are taking $24,492 of spending out of the economy right there....... Thats well more then most spend on smashed avocardo

Which is why I'd rather never get to an $820k mortgage to begin with. Take me back to 21% mortgage rates please, where you could only borrow 2 x your income. 21% mortgage rates = high inflation = wages go up = increased mortgage payments = bye bye principal amount.

That's true Dan, but I remember the high interest rate days also wiped some people out. All it took was an unexpected drop in income (usually through no fault of their own) and the compounding high interest quickly did its damage.

My wife, I and 2 kids came here from UK 20 years ago. One child went back for a holiday before Covid and got stuck there. She appears reluctant to come back. The NZ economy has gone down the tubes and should we get another 3 years of this government we will certainly be reviewing our situation. The big thing stopping a snap decision at the moment is it would be cruel leaving our daughter here.

Have you looked at the state of the UK lately?

The UK is really really bad and getting worse fast. My Cousin lives there and all I get is doom updates and the total number of illegal boat people turning up each day, record number just recently. Its a shit hole unless you are in the top 5% of the population with untold money. The average person over there leads a very poor quality of life.

Let chalk this nonsense up with other such Carlos67 gems as:

Australia will be unhabitable in 8 years

Bitcoin is going to zero

Carlos is wrong, Bitcoin won't go to zero ( a sucker is born every minute) but it will go down, down, down because it only has value to crooks and fools

Yet it's gone up ~40% this month. Lol.

and still down 50% over a year.

You failed to buy the dip. Schoolboy error.

Lets call it the RBNZ squeeze, Thanks from every NZer with a mortgage....

They made the mistake creating too much money - and now we are paying for it...!

Regardless we would still be have high inflation and hence mortgage rates. The problem is with the borrowers ignorance of history.

The housing market is laggy.

Add to that all those mortgages that are going to have to re-fix at higher rates this year and it's clear house prices have a way to fall.

Oh yes, and there's the small matter of 7.2% inflation. Amazing how excited some people were this week about it not having risen even higher than that.

In my experience pay reviews tend to happen later in the calendar year. The cost push results in a chain reaction of price increases peaking several months later.

House prices rising by the election....buy a house in 2023...

Hahaha

can you call the bottom, day week month i don't care, I just want to have a reference so I can laugh at you later.

My predictions (almost 100% plagiarised from GMO):

10 year minus 3 month US treasury build yields have a 100 correlation with the US going into recession when they are negative.

The have gone negative. Usually there would be a delay of 6 months until a recession, but because of the January Rally effect and the Presidential Cycle this might be delayed to December 2023. So if the US is in recession by the end of 2023 then NZ will follow.

The stock market bottomed out after the bubbles of 1972, 2000 and 2006 some 11, 15 and 19 months after the recessions started. So take the middle, and the NZ stock market bottoms out March 2025.

Property often lags by a year, so NZ property market bottoms out in March 2026.

Not good for some... How long before theres more like this in the news.Another OCR hike anyone?What is interesting is the comment about renting.Are you winning if your renting presently? Should they sell up and rent? Mortgage from $4000 to $6710.00 a month in 2 years...CRIKEY! A valid point is made, that being, If the finance rate exceeds the expected return its not financially viable.The RB and lenders should take note,push too hard and folk will figure out its just not worth it (Full article below) 'Elevated Risk'

"It may mean they have to sell for less than what they paid, but Aaron believed the extra money they save renting could help them save for their next house and come out ahead rather than paying so much cash to the banks."

https://www.odt.co.nz/news/national/mortgage-interest-hike-may-force-fa…

Maxing your borrowing at the lowest rates in history hoping it would last for ever.... Perhaps should have bought a cheaper house....?

We are at the bottom of the cycle. Time to start buying, lock in a short term rate, and wait for rapid interest rate falls. End of this year will be very different from now.

https://www.youtube.com/watch?v=7P8k6DwBu4U

Whoa. I could only dream of having your kind of courage.

Well at least you got the last sentence right...

Do we see a trend? First house inflation, then health catastrophe and now daily expenses inflation. The question is what the next one would be and if we have even learnt from the first one yet? I guess no. However, we know the motive is simply the money. Essentially, we have had it floating everything including our house, health and daily commodities on foreign hands. Therefore, I think our circular economy totally depends on mercy of foreign greediness. Apparently, this is not going to be stopped unless we enforce a brake in the circle and make it back mainly to New Zealand dependent. The good example is Canada, where foreign buyers are banned and the price has declined sharply recently. I guess the bottom-line is what we favour; for Kiwi or our own pocket? Due to globalization, I guess we are totally out of moral and careless about the consequences on our next generation. If the government does not regulate, I think we shall have to consider if we would call it a country of fare retirement or it would be somewhere else. It's time now to be strong and smart Kiwi.

Oh yes, start living with the virtual life. Would there have threat and hatred, let's re-think as what we would do in real-world. Enforce law and hefty infringement!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.