Residential property has become steadily more attractive to investors since the beginning of last year due to weaker property prices and rising rents.

Interest.co.nz matches the REINZ's lower quarter selling prices for the main property types - one and two bedroom apartments/units and three bedroom houses, with the median rents sourced from bond data for the same property types, to produce indicative gross rental yields for each of those property types in 41 major urban districts around the country.

A gross rental yield is a property's annual rental income expressed as a percentage of its purchase price and is a common measure used by investors to compare the income earning potential of different properties on an apples-with-apples basis.

The actual return they receive will depend on variables such as how much debt they take on and the terms of that debt, how much maintenance a property requires, vacancy levels and any other outgoings the investor faces.

However a gross rental yield is a useful tool to assess the relative attractiveness of rental property and how that changes over time.

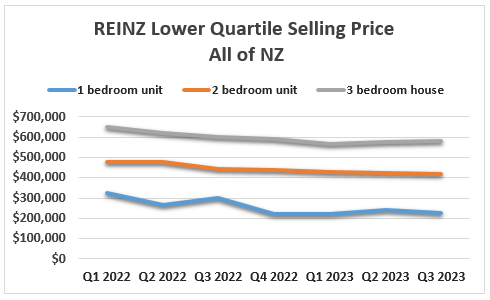

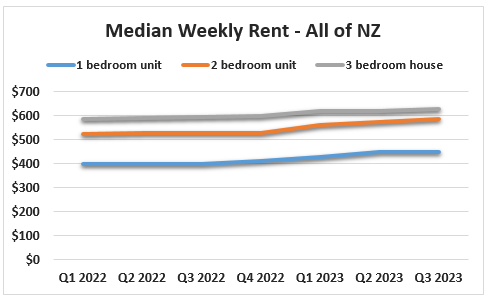

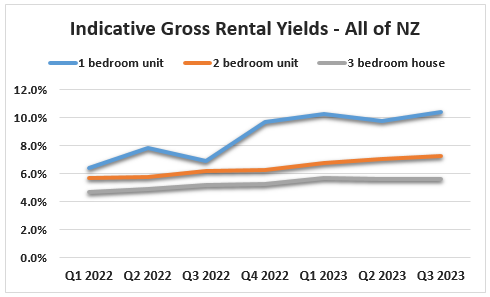

Interest.co.nz has been collating the data since the beginning of last year. Between the first quarter (Q1) of last year and Q3 this year, the national lower quartile price of three bedroom houses has decreased from $650,000 to $580,000. Over the same timeframe the median rent for newly tenanted three bedroom houses has increased from $589 to $630, pushing the yield up from 4.7% to 5.6% in the process.

The same trend is evident for multi-unit properties with the yield on one bedroom unit/apartments rising 6.4% to 10.4%, while the yield on two bedroom unit/apartments increased from 5.7% to 7.2%.

Those trends can clearly be seen in the three graphs below plotting the movements in lower quartile prices, median rents and gross yields for each of the above property types.

Similar trends are evident throughout New Zealand, with softer property prices and rising rents pushing up rental yields.

In Auckland, the country's largest rental market by far, the gross indicative yield on three bedroom houses has increased from a paltry 3.5% in Q1 2022 to a still modest 4.4% in Q3 2023. One bedroom units/apartments have gone form 6.2% to a whopping 12.5%, and two bedroom units/apartments have increased from 4.4% to 6.0% over the same period.

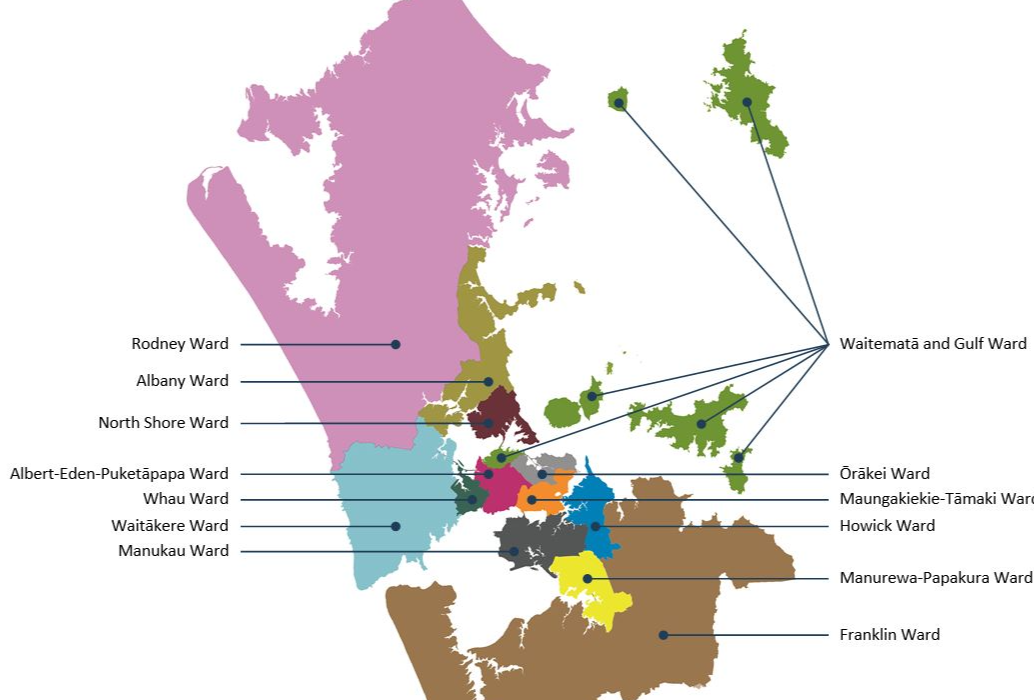

The table below shows the indicative yield trends by property type in all 41 urban areas monitored, including all of the council wards areas within the Auckland region.

Rising yields indicate an improvement in the income earning potential of a property. From that perspective, residential property has become a more attractive proposition for investors since the beginning of last year.

However, the currently high level of mortgage interest rates means it's likely to be investors with significant amounts of equity who are best placed to take advantage of that trend.

The comment stream on this story is now closed.

| Indicative Rental Yields | |||

| Gross rental yields for residential rental properties purchased at the REINZ's lower quartile selling price and rented at the median rent for each type of property in each district | |||

| Quarter | 1 bedroom unit/apartment | 2 Bedroom unit/apartment | 3 bedroom house |

| Whangarei District | |||

| Q1 2022 | 7.3% | 4.9% | 4.5% |

| Q2 2022 | 6.2% | 5.1% | 4.9% |

| Q3 2022 | 7.1% | 5.2% | 4.9% |

| Q4 2022 | 8.4% | 5.3% | 5.0% |

| Q1 2023 | 7.0% | 5.3% | 5.2% |

| Q2 2023 | 0.0% | 5.6% | 5.5% |

| Q3 2023 | 7.0% | 5.2% | 5.8% |

| Auckland Region | |||

| Q1 2022 | 6.2% | 4.4% | 3.5% |

| Q2 2022 | 13.6% | 4.5% | 3.7% |

| Q3 2022 | 7.2% | 4.6% | 3.9% |

| Q4 2022 | 11.2% | 4.8% | 4.0% |

| Q1 2023 | 11.8% | 5.3% | 4.2% |

| Q2 2023 | 13.4% | 5.6% | 4.3% |

| Q3 2023 | 12.5% | 6.0% | 4.4% |

| Auckland Council Ward Areas: | |||

| See map below for ward boundaries | |||

| Auckland - Rodney Ward | |||

| Q1 2022 | 0.0% | 0.0% | 3.5% |

| Q2 2022 | 0.0% | 0.0% | 3.5% |

| Q3 2022 | 0.0% | 0.0% | 3.9% |

| Q4 2022 | 0.0% | 0.0% | 3.7% |

| Q1 2023 | 0.0% | 0.0% | 3.5% |

| Q2 2023 | 0.0% | 3.4% | 4.0% |

| Q3 2023 | 2.6% | 0.0% | 3.9% |

| Auckland - Albany Ward | |||

| Q1 2022 | 4.1% | 3.4% | 3.2% |

| Q2 2022 | 4.5% | 3.6% | 3.4% |

| Q3 2022 | 3.8% | 3.8% | 3.6% |

| Q4 2022 | 4.2% | 4.3% | 3.7% |

| Q1 2023 | 5.1% | 4.5% | 3.9% |

| Q2 2023 | 6.0% | 5.0% | 3.9% |

| Q3 2023 | 4.9% | 4.8% | 4.1% |

| Auckland - North Shore Ward | |||

| Q1 2022 | 3.9% | 3.5% | 3.1% |

| Q2 2022 | 4.2% | 3.9% | 3.3% |

| Q3 2022 | 4.6% | 4.1% | 3.4% |

| Q4 2022 | 4.2% | 4.1% | 3.5% |

| Q1 2023 | 6.0% | 4.1% | 3.7% |

| Q2 2023 | 5.2% | 4.6% | 3.9% |

| Q3 2023 | 4.7% | 5.0% | 3.9% |

| Auckland - Waitakere Ward | |||

| Q1 2022 | 16.7% | 3.4% | 3.3% |

| Q2 2022 | 5.1% | 3.6% | 3.6% |

| Q3 2022 | 0.0% | 4.8% | 3.7% |

| Q4 2022 | 0.0% | 4.1% | 3.8% |

| Q1 2023 | 3.5% | 4.7% | 4.0% |

| Q2 2023 | 0.0% | 5.3% | 4.4% |

| Q3 2023 | 0.0% | 5.1% | 4.2% |

| Auckland - Waitemata and Gulf Ward | |||

| Q1 2022 | 9.1% | 10.6% | 2.8% |

| Q2 2022 | 26.4% | 10.0% | 2.9% |

| Q3 2022 | 16.5% | 10.4% | 2.6% |

| Q4 2022 | 24.2% | 9.9% | 2.8% |

| Q1 2023 | 19.4% | 10.5% | 2.9% |

| Q2 2023 | 25.0% | 11.0% | 3.7% |

| Q3 2023 | 21.0% | 16.0% | 3.3% |

| Auckland - Whau Ward | |||

| Q1 2022 | 5.3% | 4.5% | 3.2% |

| Q2 2022 | 6.5% | 4.0% | 3.3% |

| Q3 2022 | 3.3% | 4.2% | 3.5% |

| Q4 2022 | 4.6% | 4.1% | 3.7% |

| Q1 2023 | 0.0% | 5.1% | 4.0% |

| Q2 2023 | 4.5% | 5.8% | 4.0% |

| Q3 2023 | 4.8% | 5.3% | 4.2% |

| Auckland - Albert-Eden-Puketapapa Ward | |||

| Q1 2022 | 4.2% | 4.0% | 2.9% |

| Q2 2022 | 4.2% | 3.9% | 3.1% |

| Q3 2022 | 4.9% | 4.1% | 3.2% |

| Q4 2022 | 4.7% | 4.5% | 3.1% |

| Q1 2023 | 5.0% | 4.9% | 3.4% |

| Q2 2023 | 4.9% | 4.8% | 3.9% |

| Q3 2023 | 5.7% | 5.2% | 3.7% |

| Auckland - Orakei Ward | |||

| Q1 2022 | 5.3% | 3.4% | 2.5% |

| Q2 2022 | 4.5% | 3.5% | 2.8% |

| Q3 2022 | 6.7% | 3.6% | 2.7% |

| Q4 2022 | 6.4% | 3.8% | 3.1% |

| Q1 2023 | 7.8% | 4.4% | 3.3% |

| Q2 2023 | 5.2% | 4.0% | 3.3% |

| Q3 2023 | 6.8% | 4.6% | 3.5% |

| Auckland - Maungakiekie-Tamaki Ward | |||

| Q1 2022 | 4.1% | 5.0% | 2.9% |

| Q2 2022 | 5.2% | 4.3% | 3.3% |

| Q3 2022 | 5.5% | 3.1% | 2.3% |

| Q4 2022 | 5.5% | 4.4% | 3.6% |

| Q1 2023 | 8.4% | 4.7% | 3.8% |

| Q2 2023 | 11.0% | 4.8% | 4.0% |

| Q3 2023 | 5.4% | 5.6% | 3.9% |

| Auckland - Howick Ward | |||

| Q1 2022 | 4.6% | 4.0% | 3.0% |

| Q2 2022 | 0.0% | 3.9% | 3.4% |

| Q3 2022 | 5.3% | 4.6% | 3.2% |

| Q4 2022 | 5.1% | 4.0% | 3.4% |

| Q1 2023 | 5.0% | 4.4% | 3.5% |

| Q2 2023 | 5.6% | 4.8% | 3.6% |

| Q3 2023 | 4.9% | 5.0% | 3.7% |

| Auckland - Manukau Ward | |||

| Q1 2022 | 5.1% | 4.1% | 3.8% |

| Q2 2022 | 5.5% | 4.3% | 4.0% |

| Q3 2022 | 5.4% | 5.1% | 4.3% |

| Q4 2022 | 5.5% | 4.7% | 4.5% |

| Q1 2023 | 6.0% | 5.0% | 4.6% |

| Q2 2023 | 6.9% | 5.8% | 4.8% |

| Q3 2023 | 6.1% | 5.8% | 4.7% |

| Auckland - Manurewa-Papakura Ward | |||

| Q1 2022 | 0.0% | 3.9% | 3.8% |

| Q2 2022 | 0.0% | 4.2% | 4.1% |

| Q3 2022 | 0.0% | 4.2% | 4.2% |

| Q4 2022 | 0.0% | 4.8% | 4.5% |

| Q1 2023 | 0.0% | 4.9% | 4.8% |

| Q2 2023 | 0.0% | 5.4% | 4.6% |

| Q3 2023 | 0.0% | 5.2% | 4.8% |

| Auckland - Franklin Ward | |||

| Q1 2022 | 4.3% | 3.5% | 3.8% |

| Q2 2022 | 0.0% | 0.0% | 3.7% |

| Q3 2022 | 0.0% | 4.1% | 4.0% |

| Q4 2022 | 0.0% | 0.0% | 4.1% |

| Q1 2023 | 0.0% | 0.0% | 4.3% |

| Q2 2023 | 0.0% | 0.0% | 4.4% |

| Q3 2023 | 0.0% | 5.7% | 4.3% |

| Hamilton City | |||

| Q1 2022 | 3.6% | 4.6% | 3.8% |

| Q2 2022 | 4.5% | 4.5% | 4.0% |

| Q3 2022 | 4.8% | 4.6% | 4.3% |

| Q4 2022 | 4.0% | 4.6% | 4.5% |

| Q1 2023 | 3.2% | 4.8% | 4.5% |

| Q2 2023 | 2.9% | 5.1% | 4.7% |

| Q3 2023 | 0.0% | 5.3% | 4.7% |

| Tauranga City | |||

| Q1 2022 | 3.6% | 4.7% | 3.8% |

| Q2 2022 | 3.4% | 4.4% | 4.1% |

| Q3 2022 | 2.7% | 4.7% | 4.4% |

| Q4 2022 | 8.4% | 4.5% | 4.6% |

| Q1 2023 | 5.7% | 5.0% | 4.5% |

| Q2 2023 | 6.6% | 5.6% | 4.8% |

| Q3 2023 | 4.2% | 6.1% | 4.9% |

| Whakatane District | |||

| Q1 2022 | 0.0% | 0.0% | 4.2% |

| Q2 2022 | 0.0% | 0.0% | 4.2% |

| Q3 2022 | 0.0% | 0.0% | 4.5% |

| Q4 2022 | 0.0% | 0.0% | 5.2% |

| Q1 2023 | 0.0% | 0.0% | 5.3% |

| Q2 2023 | 0.0% | 4.4% | 4.9% |

| Q3 2023 | 0.0% | 0.0% | 5.2% |

| Rotorua District | |||

| Q1 2022 | 0.0% | 5.8% | 5.2% |

| Q2 2022 | 0.0% | 5.7% | 5.2% |

| Q3 2022 | 1.9% | 7.9% | 5.5% |

| Q4 2022 | 2.8% | 5.4% | 5.6% |

| Q1 2023 | 0.0% | 6.5% | 6.4% |

| Q2 2023 | 0.0% | 6.4% | 5.8% |

| Q3 2023 | 3.6% | 6.2% | 6.0% |

| Hastings District | |||

| Q1 2022 | 0.0% | 0.0% | 4.7% |

| Q2 2022 | 0.0% | 5.1% | 4.7% |

| Q3 2022 | 0.0% | 0.0% | 5.0% |

| Q4 2022 | 0.0% | 5.0% | 5.2% |

| Q1 2023 | 0.0% | 5.5% | 5.5% |

| Q2 2023 | 0.0% | 5.8% | 5.2% |

| Q3 2023 | 0.0% | 4.4% | 5.7% |

| Napier City | |||

| Q1 2022 | 7.0% | 5.4% | 4.1% |

| Q2 2022 | 7.7% | 5.7% | 4.6% |

| Q3 2022 | 7.4% | 5.6% | 4.7% |

| Q4 2022 | 0.0% | 5.0% | 4.8% |

| Q1 2023 | 0.0% | 6.9% | 5.2% |

| Q2 2023 | 5.4% | 6.0% | 5.4% |

| Q3 2023 | 7.1% | 7.3% | 5.6% |

| Taupo District | |||

| Q1 2022 | 0.0% | 4.6% | 3.9% |

| Q2 2022 | 0.0% | 3.4% | 3.8% |

| Q3 2022 | 0.0% | 3.7% | 4.1% |

| Q4 2022 | 0.0% | 0.0% | 3.9% |

| Q1 2023 | 0.0% | 4.3% | 4.6% |

| Q2 2023 | 0.0% | 0.0% | 4.4% |

| Q3 2023 | 11.1% | 0.0% | 4.8% |

| New Plymouth District | |||

| Q1 2022 | 5.1% | 4.4% | 4.7% |

| Q2 2022 | 0.0% | 5.3% | 5.0% |

| Q3 2022 | 0.0% | 5.3% | 5.1% |

| Q4 2022 | 7.6% | 6.1% | 5.2% |

| Q1 2023 | 0.0% | 7.2% | 5.5% |

| Q2 2023 | 0.0% | 6.7% | 5.9% |

| Q3 2023 | 4.8% | 5.9% | 6.2% |

| Whanganui District | |||

| Q1 2022 | 6.8% | 4.8% | 5.2% |

| Q2 2022 | 0.0% | 4.8% | 5.3% |

| Q3 2022 | 6.0% | 5.1% | 6.1% |

| Q4 2022 | 9.7% | 6.8% | 6.3% |

| Q1 2023 | 8.3% | 7.2% | 6.3% |

| Q2 2023 | 8.3% | 6.8% | 6.9% |

| Q3 2023 | 0.0% | 7.8% | 6.5% |

| Palmerston North City | |||

| Q1 2022 | 0.0% | 4.3% | 4.6% |

| Q2 2022 | 3.0% | 4.9% | 4.9% |

| Q3 2022 | 0.0% | 5.7% | 5.3% |

| Q4 2022 | 0.0% | 6.8% | 5.3% |

| Q1 2023 | 0.0% | 6.2% | 5.7% |

| Q2 2023 | 4.3% | 5.9% | 6.0% |

| Q3 2023 | 0.0% | 6.3% | 5.5% |

| Kapiti Coast District | |||

| Q1 2022 | 0.0% | 0.0% | 4.0% |

| Q2 2022 | 0.0% | 0.0% | 4.4% |

| Q3 2022 | 0.0% | 0.0% | 4.4% |

| Q4 2022 | 0.0% | 4.4% | 4.4% |

| Q1 2023 | 0.0% | 0.0% | 4.8% |

| Q2 2023 | 0.0% | 4.5% | 5.0% |

| Q3 2023 | 0.0% | 5.2% | 5.5% |

| Porirua City | |||

| Q1 2022 | 0.0% | 0.0% | 4.3% |

| Q2 2022 | 0.0% | 3.3% | 4.8% |

| Q3 2022 | 0.0% | 4.4% | 5.4% |

| Q4 2022 | 0.0% | 0.0% | 4.9% |

| Q1 2023 | 0.0% | 0.0% | 5.0% |

| Q2 2023 | 0.0% | 0.0% | 5.3% |

| Q3 2023 | 0.0% | 0.0% | 5.1% |

| Upper Hutt City | |||

| Q1 2022 | 0.0% | 0.0% | 4.4% |

| Q2 2022 | 0.0% | 0.0% | 4.7% |

| Q3 2022 | 0.0% | 5.6% | 4.9% |

| Q4 2022 | 0.0% | 6.3% | 5.2% |

| Q1 2023 | 0.0% | 5.7% | 5.6% |

| Q2 2023 | 0.0% | 6.7% | 5.3% |

| Q3 2023 | 0.0% | 7.2% | 5.2% |

| Lower Hutt City | |||

| Q1 2022 | 4.5% | 4.5% | 4.3% |

| Q2 2022 | 5.5% | 5.3% | 4.7% |

| Q3 2022 | 7.4% | 6.2% | 5.2% |

| Q4 2022 | 10.5% | 6.4% | 5.6% |

| Q1 2023 | 6.6% | 7.1% | 5.8% |

| Q2 2023 | 6.3% | 6.2% | 5.5% |

| Q3 2023 | 7.9% | 7.7% | 5.8% |

| Wellington City | |||

| Q1 2022 | 6.3% | 5.0% | 4.1% |

| Q2 2022 | 6.2% | 5.4% | 4.3% |

| Q3 2022 | 7.1% | 6.1% | 4.6% |

| Q4 2022 | 8.4% | 5.4% | 4.8% |

| Q1 2023 | 7.8% | 6.4% | 4.9% |

| Q2 2023 | 7.9% | 6.5% | 5.1% |

| Q3 2023 | 8.4% | 6.4% | 4.9% |

| Nelson City | |||

| Q1 2022 | 6.0% | 4.4% | 4.2% |

| Q2 2022 | 6.0% | 4.6% | 4.2% |

| Q3 2022 | 6.5% | 5.9% | 4.5% |

| Q4 2022 | 6.4% | 6.2% | 4.6% |

| Q1 2023 | 4.7% | 5.7% | 4.7% |

| Q2 2023 | 4.0% | 5.0% | 4.8% |

| Q3 2023 | 3.2% | 5.8% | 4.8% |

| Marlborough District | |||

| Q1 2022 | 0.0% | 0.0% | 4.3% |

| Q2 2022 | 0.0% | 0.0% | 4.2% |

| Q3 2022 | 0.0% | 5.1% | 5.0% |

| Q4 2022 | 0.0% | 0.0% | 4.5% |

| Q1 2023 | 0.0% | 6.4% | 4.9% |

| Q2 2023 | 0.0% | 0.0% | 5.1% |

| Q3 2023 | 0.0% | 6.2% | 4.9% |

| Waimakariri District | |||

| Q1 2022 | 0.0% | 0.0% | 4.3% |

| Q2 2022 | 0.0% | 0.0% | 4.2% |

| Q3 2022 | 0.0% | 0.0% | 4.4% |

| Q4 2022 | 0.0% | 0.0% | 4.3% |

| Q1 2023 | 0.0% | 0.0% | 4.8% |

| Q2 2023 | 0.0% | 0.0% | 4.9% |

| Q3 2023 | 0.0% | 0.0% | 4.8% |

| Christchurch City | |||

| Q1 2022 | 4.9% | 5.4% | 4.3% |

| Q2 2022 | 6.2% | 5.7% | 4.6% |

| Q3 2022 | 5.6% | 5.5% | 4.7% |

| Q4 2022 | 5.4% | 5.8% | 4.9% |

| Q1 2023 | 5.8% | 6.4% | 5.1% |

| Q2 2023 | 5.5% | 6.3% | 5.2% |

| Q3 2023 | 5.9% | 6.6% | 5.2% |

| Selwyn District | |||

| Q1 2022 | 0.0% | 0.0% | 3.9% |

| Q2 2022 | 0.0% | 0.0% | 3.9% |

| Q3 2022 | 0.0% | 0.0% | 4.0% |

| Q4 2022 | 0.0% | 0.0% | 4.4% |

| Q1 2023 | 0.0% | 0.0% | 4.2% |

| Q2 2023 | 0.0% | 0.0% | 4.4% |

| Q3 2023 | 0.0% | 0.0% | 4.4% |

| Ashburton District | |||

| Q1 2022 | 0.0% | 0.0% | 4.7% |

| Q2 2022 | 0.0% | 0.0% | 5.0% |

| Q3 2022 | 0.0% | 0.0% | 5.3% |

| Q4 2022 | 0.0% | 0.0% | 4.8% |

| Q1 2023 | 0.0% | 0.0% | 5.0% |

| Q2 2023 | 0.0% | 6.1% | 5.3% |

| Q3 2023 | 0.0% | 7.2% | 5.8% |

| Timaru District | |||

| Q1 2022 | 0.0% | 6.4% | 5.1% |

| Q2 2022 | 0.0% | 6.3% | 4.8% |

| Q3 2022 | 0.0% | 5.3% | 5.2% |

| Q4 2022 | 0.0% | 6.1% | 5.6% |

| Q1 2023 | 0.0% | 6.6% | 5.4% |

| Q2 2023 | 0.0% | 6.7% | 5.2% |

| Q3 2023 | 0.0% | 5.4% | 5.4% |

| Queenstown-Lakes District | |||

| Q1 2022 | 4.4% | 4.1% | 3.2% |

| Q2 2022 | 4.8% | 4.8% | 3.3% |

| Q3 2022 | 7.4% | 4.3% | 3.6% |

| Q4 2022 | 4.8% | 4.7% | 3.8% |

| Q1 2023 | 8.8% | 5.0% | 3.9% |

| Q2 2023 | 5.2% | 5.5% | 4.1% |

| Q3 2023 | 9.1% | 6.1% | 3.9% |

| Dunedin City | |||

| Q1 2022 | 5.0% | 6.4% | 4.7% |

| Q2 2022 | 4.3% | 5.6% | 4.8% |

| Q3 2022 | 4.6% | 6.0% | 5.4% |

| Q4 2022 | 4.2% | 7.4% | 5.6% |

| Q1 2023 | 5.8% | 6.6% | 5.9% |

| Q2 2023 | 5.5% | 6.0% | 5.9% |

| Q3 2023 | 4.9% | 5.0% | 5.8% |

| Invercargill City | |||

| Q1 2022 | 8.8% | 6.1% | 5.9% |

| Q2 2022 | 11.9% | 7.0% | 6.1% |

| Q3 2022 | 8.7% | 6.8% | 6.0% |

| Q4 2022 | 0.0% | 7.3% | 6.0% |

| Q1 2023 | 0.0% | 6.4% | 6.8% |

| Q2 2023 | 0.0% | 6.2% | 6.5% |

| Q3 2023 | 9.7% | 7.4% | 6.5% |

| Total - All of Aotearoa | |||

| Q1 2022 | 6.4% | 5.7% | 4.7% |

| Q2 2022 | 7.8% | 5.7% | 4.9% |

| Q3 2022 | 6.9% | 6.2% | 5.2% |

| Q4 2022 | 9.7% | 6.3% | 5.3% |

| Q1 2023 | 10.2% | 6.8% | 5.7% |

| Q2 2023 | 9.8% | 7.1% | 5.6% |

| Q3 2023 | 10.4% | 7.2% | 5.6% |

| Note: The price data used to calculate the yield figures in this report is provided by the Real Estate Institute of New Zealand (REINZ), home of the most complete, accurate and up-to-date real estate data in New Zealand. | |||

Auckland Council Wards Map

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

104 Comments

Getting better for investors but yield is still significantly below the cost of borrowing, then there are the OPEX. Only way to make money right now is to be able to add value and that's the way it should always be

Not just that but rates and insurance have also increased 50% over the last few years, and apartments have high body corporate costs as well. Its unrealistic to look at gross yields when its the net yield that needs to be compared with the interest rate you can get on term deposit (6.25%) or on shares (7%) for much lower risk and no danger of tenants trashing your investment.

When I did my sums the crossover where rental property became a better long-term investment than a term deposit was 0.32% Capital Gains p.a. Even the most ardent DGM would agree that is almost certain to be exceeded over the next ten years.

New Zealand law says that buying and selling land with the intent of capital gains makes those gains taxable as profit. Let's hope a bunch of folk aren't committing tax evasion.

Every investor: "No IRD, I bought this for rental income long term and never had any plans to sell until [insert any excuse here that developed post-settlement of taking ownership]"

(a) i guess this assumes debt-free purchase

(b) no, I don't think "almost certain to be exceeded". Prices are still clearly way above fundamentals, we're starting at a local recession at least, backed by substantial global risks. I don't think our crash has happened yet - if it does, good chance prices won't recover within ten years.

If you wanted to gear you can do so on shares, up to an 80% LVR on blue chips. And all the interest will be tax deductible. Plus the dividends are already tax paid and comes with imputation/franking credits.

a). No. b) 3.2% price growth over ten years is absolutely tiny in an inflationary environment.

Pretty hard to do the math, how do you factor in an empty rental for a while or tenants trashing the place and your insurance premium or them not paying and still living there and you certainly cannot price in the stress. Yes historically the capital gains made it worthwhile in the long run if you can deal with it, personally I didn't need to put up with the shit so opted out.

Fair enough. All investments have their risks and rentals are no different. However with such competition for houses you can be really selective on your tenant. Had over 50 applicants in 24hrs last time I had a vacancy. The tenant we chose has become a great mate. The risk of a tenant trashing a place has never been lower. To do so could mean they become homeless.

Gross yield percentages are very deceptive, and can make people think property can bring them a yield annually. They should publish net yield, which would be minus 2% or worse.

I agree in principle with much of what you are saying, but when it comes to shares you should also consider your investment horizon - while shares are an excellent investment in the long term, they do provide potentially significant short-term volatility, which might not be suitable to some investor profiles. If you have some money that you think you may need within the next 10-12 years, shares might not be your best option, unless you want to gamble and get into the dangerous game of trying to time the market.

Also no labour involved. ZERO. If you’re a “mum and dad investor” there’s a good chance you run a business or work decent hours as a bare minimum. Who wants to deal with tenants for less?

Buy a one bedroom flat in whangarei then Yvil

7 percent yield

One bedrooms seem to be the goldmine everywhere as our nations housing was always 2+bdrm historically

Oh great. Just what the FHB market needs. Another wave of frothy mouthed knuckle dragging property speculators. 'Me buy house'...'Me be rich'... who was the guy on here saying he was packing out bedrooms with mattresses and immigrants? It's wrong on all levels.

Me just shows your intelligence in nor reading correctly what I said was that I don't build large bedrooms because j don't alot mattress beds in the room as new immigrants want to not me. Shows your IQ

Off topic, Colin - but in a previous post you indicated that you did not do concrete floors. Why not ?

Several reasons concrete floors are hard to level when an event happens Christchurch prime example the old 60 weatherboard iron roof houses stood upto the earthquake than modern concrete floor brick and tile did yes you can pump the foam under to relevel but I have heard that fails over time. Secondly the concrete floor rib raft is full of polystyrene what happens to that when in a 100 yrs that house gets removed polystyrene is highly pollutant and exspensive to get rid of thirdly when more modern things come along way easier for tradesman to go under floor and either put new services in or repair bloody hard to fix a cracked pipe in the concrete floor finally I can lay the floor joists etc whereby if laying a concrete floor I would have too get other trades in it works out way more cost effective for me there are several other minor advantages in my opinion as well

I love the Interest.co comments section on a Friday morning.

Oh please be quiet. There's nothing wrong with investing in property. If you think there is then I presume either you're a big fan of homelessness or want the state to own all rentals.

[ Insult removed. Just not necessary. Ed. ]

Remove the insult from OP then too Ed? It's identical?

Consistency not

People who insult landlords view ads too.

the state owning them all is a great idea.

Kainga Ora lost the taxpayer an average of $21k per house. A gross yield of NEGATIVE 2.5%. Private Landlording is far more efficient for our country than KO.

How much did private lsndlording receive in welfare ? Accom supplements etc. I'd guess, as far as the taxpayer is concerned, it would be equally crap. It pisses me off that we socialise private losses.

How much did private lsndlording receive in welfare ?

Less than the tenants of social housing. Because a great deal of private renters aren't being directly subsidised.

Fact is we have a population that needs housing, and lack the coffers for the state to provide it all themselves. And the state is less efficient than the private market, because it usually has more intensive management.

How much did private lsndlording receive in welfare ?

$2,411,065,000 (yes, billion) in 2021/22.

Sorry the link to that Treasury (Vote) document which I got that number from no longer works;

https://budget.govt.nz/budget/2022/by/vote/socdev.htm

Which is a bit strange!

But anyway, it's in the Vote: Social Development file for the 2002 budget - wherever that might be posted now :-).

Well to be fair what does the average rental property claim in interest deductions (when 100% deductibility is in place)? A $400k loan at 5% deducts $20k a year in interest. Doesn't sound very efficient to me.

Nothing wrong with investing in property. But it also shouldn't be a state-supported welfare scheme, instead of an investment with risk and free market price discovery. Nor should commonplace tax evasion by people buying and selling with the intent of capital gains (taxable under NZ's income tax act) be tolerated.

Buying existing property and renting it out does stuff-all to reduce homelessness.

I’ve got rental out south, 3 bedrooms. I’ve got 3 bunks per room, so 18 immigrants paying $100/wk each, brings in $1800 a week. So the yields are there, you just need to squeeze for it. I call that rental my sardine tin. Might do more, it’s good business. Immigration is a good thing, we can make a lot of cash from it.

BTW, this story is a complete lie, and is written for the purpose of entertaining the viewers.

However, some Stuff journalist will soon publish that statement as fact.

Then newshub will screengrab it and run their own story.

Actually I think the current path for news to travel is that someone will post this comment to Reddit, then Stuff will take it from there and post it as factual news, then its picked up by Newshub.

Or hunt down the one guy doing things like this in the whole country and state that it’s common practice.

But I thought the market was going to crash and everyone is leaving NZ because it's so bad. And anyone who buys a house is just going to lose money.

Inertia.co commenters have stated that for last 10 years or more.

They are leaving. Highest migrant departures since Feb 2012. I am sure next months data will break record and will highest departures for 25 plus years.

At the moment they are rubber stamping visa's as fast as they can.

Quantity over quality?

Could also be alot of newly stamped kiwis leaving here using here to get into Aus and these were the quantity over quality a couple of yrs ago if your scenario is correct.

Coming off the most anti-LL government in a generation I'm not surprised. Tens of thousands of homes exited the rental market and are now social houses.

Source on the "tens of thousands of homes exited the rental market"?

Yes I am interested too and I think it’s wildly inaccurate, having seen stats a couple of months ago on the number of houses added to the social housing stock over the past few years.

That's KO housing though, I think.

What nktokyo is talking about is landlords who've pivoted from renting to the private market, to renting to any number of government entities, doesn't even have to be social housing, can be housing for a fireman or a health patient. This is because in such instances the interest is still deductable.

This is most people I know with rental properties. Hard to say an exact figure though, but it's government stupidity in action.

Intuitively this didn’t feel right, and…. Not sure it’s particularly robust matching lower quartile house prices with median rents?

I think the assumption is that rental properties are heavily concentrated across the bottom half of the property market, and therefore median rent ~ lower quartile price... Which is probably a bit rough, but about right, especially for SFH. For townhouses and apartments I'd think rental properties are probably concentrated more across the bottom 3/4 of the market, given that these property types do tend to be dominated by rentals to a much larger degree than SFH.

Dp

Good comment, and yes it’s a bit rough and I guess an indication. But in my view painting a slightly rosier view than the reality. I think a lower quartile house price should equate to lower than a median rent - probably somewhere between lower quartile and median rent.

6% for 2 bed townhouses and apartments in Auckland? That’s way too high, more likely around 4.5-5% MAX

Just to use the block of 7 new 2 bedroom townhouses (built by a high volume developer so not high quality) on my street as an example. Cost $725k and rent is currently $540 a week. That's 3.9% gross yield.

Yep that’s much more typical. I have also seen rents at about $600-$625 for similar priced properties.

I think this article is pretty misleading to be honest. Predicated on some questionable assumptions.

Yes in otahu, an improvement on otara though

Locally this might hold (although even then I suspect the median rental is a little above the lower quartile property). On a national level I highly doubt it's true, aren't most rentals concentrated in the cities where prices are higher? I'm in Wellington and most of my friends rent - very few of us are in sub-$1m properties. Those that own mostly had to move out of town to buy and are living in cheaper properties than the renter crowd. Suspect nationally the median rental would be closer to the median property than lower quartile.

Surely any comparison should be baselined against the risk free rate of return?

FYI, the NZ 10 year government bond yield is currently 5.2% p.a.

Remember, it also has no associated expenses, ownership cost that unleveraged residential property has (rates, insurance, maintenance, property management fees, etc)

True, however a good number of landlords wouldn't be able to put their purchase price into a government bond because many probably bought leveraged 100%. Paper rich and very cash poor.

Unless the bank will allow them to sell and rather than set off the mortgage put it all into a Government bond.

Yes, current bond yields of government debt are extremely appealing, very difficult to resist indeed.

the national lower quartile price of three bedroom houses has decreased from $650,000 to $580,000. Over the same timeframe the median rent for newly tenanted three bedroom houses has increased from $589 to $630, pushing the yield up from 4.7% to 5.6% in the process.

So median rent is 630, 630 X 52 = 32,760. lower quartile house 580,000, so 32,760/580,000 = 5.65%.

the trouble is:

- interest rate is 7.3%,

- TD rate is 6.25%.

- more importantly, a lower quartile house can never get that $630 weekly rent.

yes, the house price has dropped, but no, property investment sucks at this moment. you are losing 1.65% just for interest payment alone, on top of that you need to pay tax, rates, insurance and kept told how dirty filthy landlord you are by the greens.

Are you charging "the greens" rent for the space they occupy in your head?

No, I don't really want to deal with them. They can enjoy the rentals growing in the trees.

Highest yields on the 1-bedroom properties - and lowest dwelling prices. Reason being, it's easier to fleece the most disadvantaged in the poorest neighbourhoods as the Salvation Army research has routinely found;

https://thespinoff.co.nz/the-bulletin/17-02-2022/its-a-housing-catastrophe

It's absolutely true. the most vulnerable part of New Zealand is always one get hit first, and hardest.

Interestingly, in building new developments it’s hard to get good yields for one beddies. Easiest on 2 beddies. It’s simple math - floor area is typically only 1.3 -1.5 times bigger, but rent is usually 2 x more!

I suspect the predominance of one bedroom shoeboxes and leasehold properties in Auckland pushes that yield quoted in the article up quite a bit.

Hence why I build 4beddies the cost a sqm is not that much more as most of the cost is in the wet and service areas and 4 beds are in such high demand as I have stated before that the bedrooms ain't big nothing under 3m by 3m with a wardrobe but you have 3 of them with a 4th master at 3.6 m to 5m with ensuite people are wanting them. I feel to many one and two bedroom shit boxes on the market now and going to see rent drop and resale price as well especially when a seller of one is in dire straits so that sets the benchmark

3-4% gross yields before expenses - must be one of the worst investments. This isn't even covering the cost of depreciation - and the owners time, which is never factored in - why anyone would risk their money on such a loser beats me, and thats before taking into account the negative effect of any borrowing on cashflow. If you are speculating, that 'may' be a different matter in the very long term (10-15 years +), but please don't call speculation investment.

All investment is speculation.

Can't say I've met too many destitute landlords, looks like it works out for most.

"Can't say I've met too many destitute landlords"

How many landlords willingly tell people that they meet that they're destitute or have gone bankrupt?

How many of those highly leveraged property investors who had mortgagee sales in the 2009 - 2011 period that have not recovered are telling people willingly that they are destitute or bankrupt? Most are likely to be embarrassed - had close family relatives who lost all their property previously and they weren't willingly telling people.

A couple of names have come up in that 2009 - 2011 period, due to media reports.

Property promoters that have gone bankrupt

-

Phil Jones of Propertymastery - https://www.stuff.co.nz/.../Bankrupt-called-before-Assignee

-

Dean Letfus of Massive Action and ProprtyGurus - https://www.stuff.co.nz/.../Property-Guru-declares...

-

Don Ha - https://www.stuff.co.nz/.../Property-high-flier-bankrupted

Have those 3 stayed down, I dont think so

How many of those are tactical bankruptcies though? A la https://www.nzherald.co.nz/business/moneys-no-worry-for-krukziener/YQBQ…

Many are not risking their own money. A lot of it is just leveraged purchases from paper wealth, so none of their money went into it. They literally had no other real avenue to invest. Paper rich and cash poor, but still entitled to "have a go".

Agree but if you can add value which alot of these one and two bedroom stack tight on a section you can't so yes total spec. But if you can uy a 3brm on a 1000 sqm section and in the future develope that then it's worth paying that extra to get hold of it.

Numbers don't match up with what I'm seeing, maybe it's due to the way you use lower quartile purchase prices and median rents to compute the yields?

54 Hadlow Tce, Grey Lynn: asking $1.16m or $750 p/w = 3.36%

6/32D Ballarat St, Ellerslie: asking $650k or $490 p/w = 3.92%

22a Dublin St, Pukekohe: asking $650k or $595 p/w = 4.76%

2/55 Great South Road, Papakura: asking $831k or $750 p/w = 4.69%

The only properties listed on trademe for both sale and rent that have a yield north of 6% are apartments, so enjoy paying leasehold and body corporate fees out of that amazing yield.

More good evidence. The article is flawed. It’s poor stuff, I expect better.

On what grounds? This is par for the course.

Ok how about these I brought 3 brm home 11 mths ago for 328k rented it out at 400 aweek. But it had a 1000 sqm section which I have subdivided cost total of subdivision 35k everything. I live at the back section in my caravan while building a 4brm basic weatherboard iron roof house 124 sqm with single garage will come out a little higher than I thought around the 230k I was working on around 250k for everything subdivision the lot. Will rent out for 550 aweek also if law dosnt change will still have 100 percent tax deduction (that's a bonus which I don't take into account). But here is the really silly thing subdivision went thru I got a building site for 35k you would think the old existing house would drop in value nope its now valued at 350k. The new house will value in the mid 500k so approx 200k to my bottom line on paper plus since I live in the caravan also no mortgage. Once finished will do again

Uhhh, I'll take imaginary dartboard figures from guesstimators over someone doing it for a living thanks.

Note that residential property development / construction is a very different business activity from the long term residential property leasing business and the short term property rental business.

They also have different risk profiles, and tax rules.

True but all my assets are left to the dogs home (true) anyhow I do what I do cause people say I can't so when I am not here then the tax man can have it like I can't complain then

How many places in NZ can you buy a 3 bed on 1000sqm for $328k? And I assume you are building the new house yourself, otherwise 230k/124m2 = $1855/sqm seems pretty cheap. But at least you are adding to the number of houses available in the country, rather than just buying up existing stuff

True but it's like all investing you go where the yeild is do you buy shares cause they are all pretty and dressed up or do you buy the share that supplies the portaloo which is where the yeild is and also where you can add value That's why my debt to asset level is very low and when you have someone on here say I am an over leveraged developer I laugh. Still the money is where the s..t is. And yes it allows me to do it all hence keeping costs down.

And you don't have to commute to work! I like your initiative - well done (and as someone previously mentioned, you are adding to the housing stock) - great.

$35,000 sound a lot lower than subdividing would cost in Ak.

Just the services would cost something like that esp watercare.

you are like a locust, taking perfectly good NZ properties that had a back yard for a garden and area for kids to run round and wrecking them for your own self benefit. Honestly people like you make me sick.

Change is a constant !

Colin if he speaks truth, seems like a good example of someone who does things efficiently with good outcomes.

That's why I use my real name rather than hide behind a pseudonym all cloak and dagger. Easy enough for somebody to check that way to see wether I am all mouth and trou like alot on here are or wether it's truthful

Bet it's not even your real name. I could say I'm Chuck Norris and claim everyone else is hiding behind pseudonyms.

But can you do a spin kick?

He does seem pretty legit. All the armchair experts here are doing super rudimentary sums, as if buying a GJ Gardner house and renting it out at 3% return is something that's been viable for the last 15 years.

If you want to make a dollar, whether it's housing or any other sort of commercial enterprise, usually you're going to need a formula that's finding some sort of niche, or adding value where most people either can't see it or know how to implement it. Super hard to generate a surplus going through the motions.

Do the people who buy properties with small backyards also make you sick? They enabled Colin's behavior after all.

Most people don't have a garden nowadays way to busy on their ph kids hardly play outside rather on their computer games. And what I do think about it a 1012sqm section halved is still a bigger section than what most want as it is its hard to get the tenants to mow that. And they would perfer I either pave it or put raised gardens in. So please don't spoil my lawn go be sick somewhere else

Crayhunter, we cannot supply everyone in NZ the quarter acre dream of old, it is not feasible or sustainable. Just look at Auckland traffic and spread and tell me this is a good idea to keep spreading out. We need to adapt like all other modern cities by having well planned and efficient infrastructure in terms of public transport, and to build up from the inside out of our major cities to allow those who wish to live closer to the CBD or in it to do so, but with the tradeoff being size of property or space.

The number (and quality of kit/amenities) in parks, playing fields, cycleways, etc. has increased significantly in the modern urban planning era. And some researchers say that large, grassed backyards have become less important for child wellness/wellbeing. Additionally, fewer children per household than in generations before, so not the number of siblings at home to play with - hence the reason visitor numbers are increasing in parks, sports fields and cycleways/walkways.

Hence, I think your concerns about yard-size are not as valid in today's urban environments.

That said, the degree to which we have converted pervious surfaces (grassed yards/gardens) to impervious surfaces (buildings, patios, driveways) through infill has thrown our storm water systems into chaos. Big problems in that respect.

High immigration aint all bad...

Do the sums for renting a room out to a flatmate and the gross yield can be anywhere between 10-30% depending on how you measure it. If you don't mind boarders it's a great way to go. With my first house my two flatmates rent covered the mortgage repayment on a 15 year term. Boarding Is the new renting

Congrats on thinking outside the sqr. It is the only way to get ahead is finding a side hustle these people that think 40hrs aweek is going to provide a great lifestyle/or allow them to get ahead need a wake up call

"the gross yield can be anywhere between 10-30% depending on how you measure it"

Just want to make sure I'm understanding you correctly.

What is the denominator in that equation?

1) your equity deposit?

2) total purchase price?

3) market value of the dwelling?

4) other?

You mentioned home and income in another thread. So gross rental yield would be:

A) total gross rental income of your property

1) in the property you live in, the equivalent rental of a similar property located nearby (if a 3 BDRM house, then another similar 3 BDRM house in the same area)

2) plus the rental income of your boarders

B) purchase price of your property

The gross rental yield would be the ratio of A divided by B.

Given where rental yields are currently, difficult to see this ratio being 30% for a property in Auckland (unless its a leasehold).

In my area, 3 bdrms sell for 1million whoch is what i need for my home. A 4 bdrm sells for a 1.05m. Renting a room out at $300 pw gives a 30% gross return if you keep the 'home' cost above the line.

Just an example. I'd rather keep my personal finances out of the public thread

the case I am referring to above was my first home. 195k for a 3 bdrm. Rented two rooms for $180 each. Obviously that was a few years ago but there are still opportunities.

"In my area, 3 bdrms sell for 1million whoch is what i need for my home. A 4 bdrm sells for a 1.05m. Renting a room out at $300 pw gives a 30% gross return if you keep the 'home' cost above the line. "

Thank you for your clarification.

Let's just assume that this is someone else's house that you know the details on.

So $300 per week x 52 weeks = $15,600

$15,600 / 30% = $52,000 is the denominator

The $52,000 is the difference between the price of a 4 bedroom house ($1,052,000) and the price of the 3 bedroom ($1,000,000) which you live in.

Is that how you got to 30%?

For your information.

According to B&T, the average rental on a 3 bedroom house in Auckland is 656 per week, that is $34,112 per annum

https://www.barfoot.co.nz/market-reports/2023/september/quarterly-renta…

So total rent equivalent would be

1) $34,112 per annum equivalent 3 BDRM house

2) $15,600 per annum for income from boarder

Totals gross rental of $49,712 per annum.

Market value for 4 bedroom house is $1,052,000 (as above)

Gross rental yield (as calculated by most property accountants) on this property would be 4.72%.

Thats a fair calculation but it includes the 3bdrm in the equation as well. If that cost is kept above the line as that is a cost you will incur regardless of wether you own or rent, the return of the fourth bedroom in isolation is 30%.

It is worthwhile considering when looking to buy, as paying a bit extra for more rooms can change the outlook.

Thank you for sharing your example and for your clarification and perspective.

According to B&T, the average rental on a 3 bedroom house in Auckland is 656 per week, that is $34,112 per annum

$656 per week in AKL for a 3bdrm? Hell many are struggling to find a 3bdrm across Nelson bay for less than $650 due to the sheer shortage and competition. FB pages are constantly full of families pleading as their landlord is selling up, it’s a daily occurrence.

Yes, Baptist, I like the idea. It really needs to take off with the elder set too. So often one partner is left living alone in their family home after their partners death. Another elder for company (and the safety of living with someone on hand if there is an accident, or similar medical emergency) is a really good thing.

I'd like to see some rental agencies taking up a tenancy/boarder specialisation in this elder living/companion area. Elderly on their own will want a professional vetting of potential elderly/retired age boarders. It's a really needed option for elders who do not own their own home when entering retirement.

Returns are rising across asset classes, this needs to be considered within the context of relative performance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.