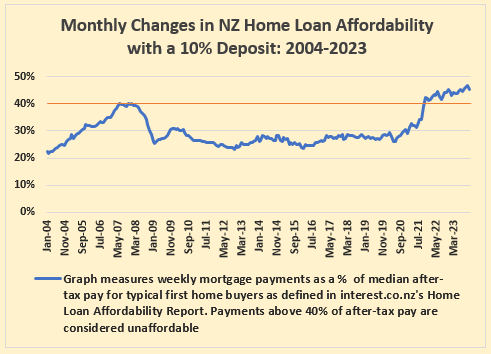

Wannabe first home buyers ended last year neither more nor less able to afford a home of their own than they were at the beginning of the year.

For those aspiring to own a home of their own, 2023 was a year in which nothing much changed.

The simple explanation is there was no significant movement in house prices at the bottom of the market last year. And although there was a moderate increase in interest rates, that was more or less offset by the increase in wages.

So overall, not much change.

That was the big picture stuff. Here's the detail.

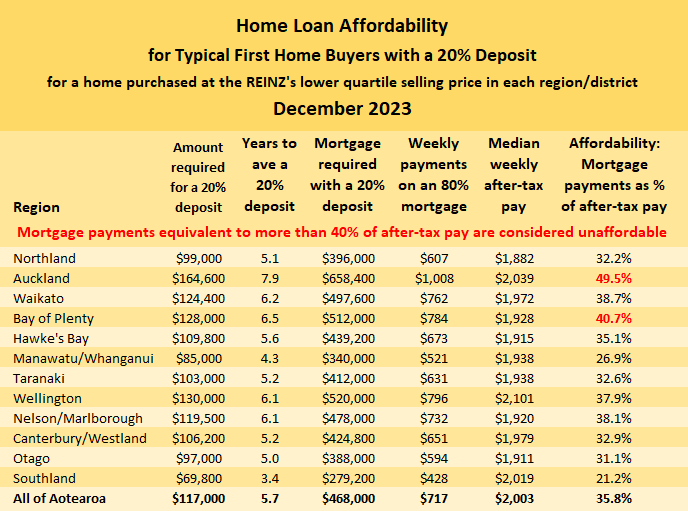

House prices

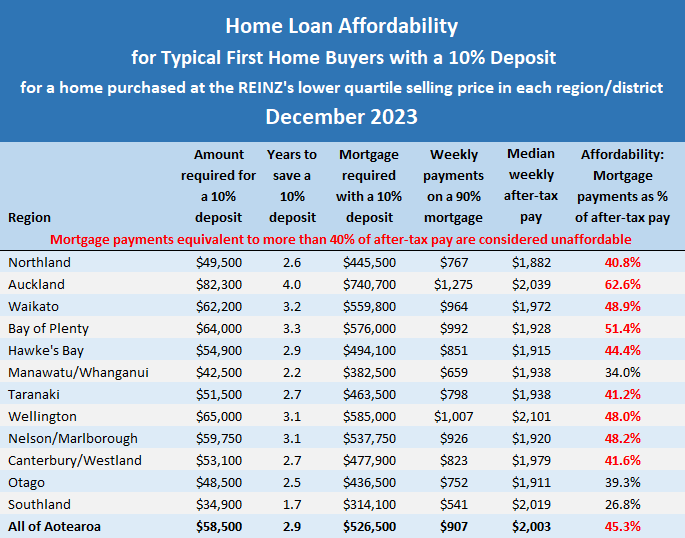

The Real Estate Institute of New Zealand's national lower quartile selling price ended last year at $585,000.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing the bottom end of the market that is usually of most interest to first home buyers.

At the end of 2022 the lower quartile price was also $585,000. So at the end of last year it ended up exactly back where it was at the end of 2022. Sure it bounced around a little bit from month to month during the year, but the movements were small.

Overall, the best way to describe the bottom end of the housing market last year was flat. As a pancake.

Which meant there was no change in the amount of money aspiring first home buyers needed to save for a deposit, or to borrow to get into a home of their own in December 2023, compared to December 2022.

Mortgage interest rates

However there was some movement in mortgage rates.

They rose slowly but steadily for most of 2023, with a tiny bit of downward momentum at the end of the year.

The average of the two year fixed rates offered by the major banks was 6.58% in December 2022. This had increased to 6.98% by December last year.

Although house prices hadn't moved much during the year and the amount a buyer would need to borrow to purchase a lower quartile-priced home had stayed the same, the rise in interest rates would have pushed up the repayments on the mortgage to $907 a week in December 2023 from around $872 a week in December 2022 if they purchased with a 10% deposit, or to $717 a week from $688 if they purchased with a 20% deposit.

So an increase of around $29 to $35 a week on the mortgage payments for a lower quartile priced home.

However affordability isn't just about costs, it's also about incomes.

Incomes

Interest.co.nz tracks the median wage rates for workers aged 25-29, because many people in that age range are likely to at least be thinking about saving for a home.

If a couple in that age group were both working full time at the median wage rates for their age group, they'd have been left with about $1930 a week between them, after tax, in December 2022.

By December 2023 that would have risen to around $2003, giving them an extra $73 a week.

So once the extra mortgage costs are deducted, the first home buyers would probably have been around $35 to $40 a week better off at the end of last year.

If we only look at the costs associated with buying a home, you could say first home buyers were marginally better off at the end of last year than they were at the end of 2022.

Unfortunately it wasn't just mortgage costs that increased last year, with the price of transport, rent, food and just about everything else, also on the rise.

How much that would have affected first home buyers would of course depend on their living costs and spending habits.

But it's probably a reasonable bet that those extra costs would have gobbled up any extra money they had in their pay packets compared to a year earlier, once the mortgage was paid.

Which means things probably didn't get much better for first home buyers in 2023, but probably didn't get much worse either.

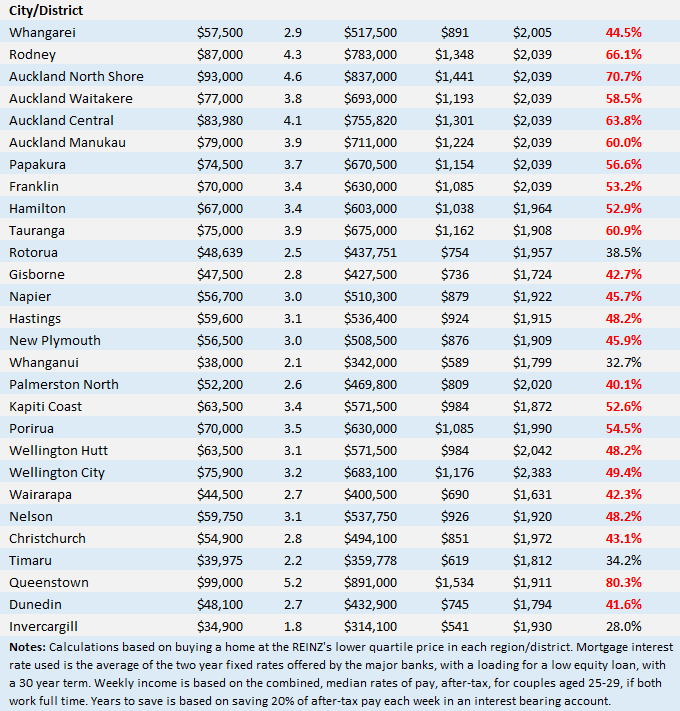

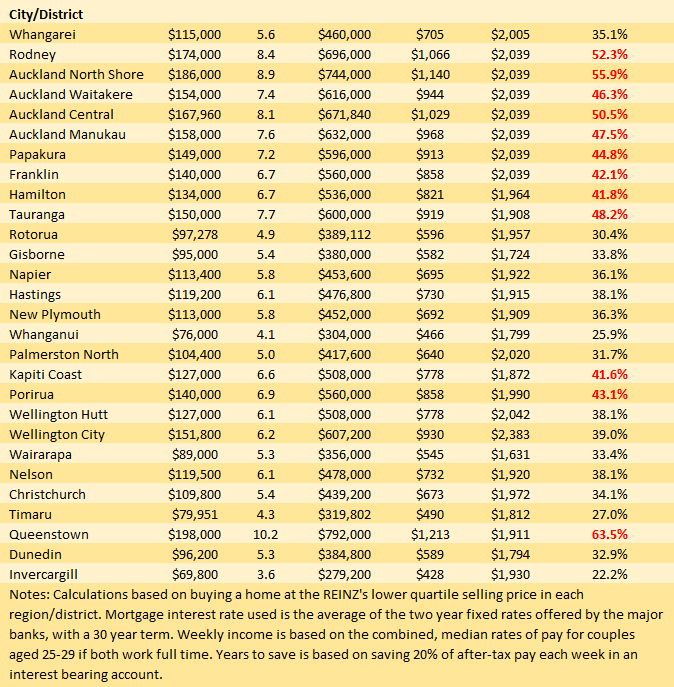

The tables below show the main affordability measures in December 2023 for typical first home buyers in the main urban areas, with either a 10% or 20% deposit.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

101 Comments

Owning a home of your own... better security, stability and privacy count

Its too hard for the accountants to quantify

I just found out my good mate is today working on a public holiday. He is not rich but he raises his children and here he is having to earn to bring home the bacon for the landlord. That ain't gonna change for the rest of his life

Thats the wonder of owning that in your retirement you can have a freehold home

I'm in my own home but working this weekend to pay the mortgage. I get what you are saying though. Renting might be cheaper in the short term but those who get their own place are generally better off in the long run.

Can we stop with the bs idea that anyone who has missed or passed on an opportunity to buy is now stuck renting for the rest of their life? I don't know your mate but maybe he's building a nice deposit and can buy in a few years time, with less risk than many who bought during the recent hype. Right now my renting friends are cruising and watching their savings pile up, whilst those who bought recently are struggling to stay afloat. In ten years time I expect the renters will all own, and be generally better off than those that rushed into ownership early.

Yes, compared to the last few years, decades?

Higher interest rates and declining, flattening prices could see present renters better off.

The Coalition, as well as tackling land supply and council consenting issues, is also meant to tackle material costs.

Of course all Govts. want to make housing more affordable, but hardly delivery.

Agreed. While it would be stupid to buy a home if it puts you at risk of defaulting, I suspect some people are focusing too much on the cost differences between renting and owning.

I could sell up tomorrow and go renting, save 40% on household costs renting a similar property nearby. But not everything in life needs to be based on maximizing opportunity cost/profit, otherwise everybody should be living down at the local camp ground and push biking everywhere.

Short term pain for long term gain. Pretty hard work for the first 10 years but there are windfalls later in life. I look out the window now at people paying $780 a week in rent, that's $780 a week I don't have to find anymore.

Here's how I see it from a financial perspective.

- Buying:

- Locking in outgoings at today's price, aside from interest rate fluctuations your "rent" is inflated away with time

- 20% down for 100% of an asset's value. Over time the asset should loosely track general inflation.

- Rent + Invest Difference

- At the start, investing the difference can be huge, potentially $300 - $500 per week.

- Over time the difference you "invest" narrows as rents generally increase with inflation but mortgage repayments don't.

- Your investment capital + returns are constantly fighting against the time value of money

A summary which suggests that, for young people with a small deposit, the best option should be to rent and save / invest a little longer, then buy a house in a few years time with a larger deposit and smaller mortgage.

Spruikers pushing FOMO have convinced a lot of scared young people that their only options are buy NOW with 10% equity and a crippling mortgage, or rent for the rest of their lives. A false dichotomy that is depressingly ubiquitous and unchallenged, including in this comment section.

I agree in general. However I wonder if the Japanese would say the same thing? At some point we will probably end up like them - declining population, decreasing housing demand and prices. It may even start soon.

Interestingly I was in japan for a month in December and stayed with NZ friend who made Japan their home 20 years ago. Tokyo is now much more affordable than Auckland and plenty of jobs for ex-pat.

Buying a house in Japan is a novelty rather than an investment opportunity, prices in major cities have been flat or slightly trending downward in the last 20 years. We saw a 3br apartment in Asakusa selling for 640k with two bathrooms and a carpark, admitelly it's small for NZ standard but more roomy than a usual Tokyo apartment size.

Tokyo is now much more affordable than Auckland and plenty of jobs for ex-pat.

I've worked corporate in Japan. Honestly speaking, if you're not there on an expat package, it can be grueling if you don't really understand how it works. Expat package workers get something of a free pass because they will be moving on eventually and are usually in positions of power.

Owning a home of your own... better security, stability and privacy count

Selling boomer dreams and ideals to the kids is getting much harder. And those dreams and ideals do not make much economic sense, except to a small minority who may find themselves with a reasonably strong income stream. But those income streams are getting few and far between.

In reality, it's the boomers who need to be taking stock here. 'Cashing in' on their home is not a given anymore. And the reality is that the boomers do not really own scarce assets beyond property.

The point Mr JC was that the qualitative factors of owning get ignored by the number crunchers.

These subjective factors could likely lead to a more stable and healthy life. Not to mention wealthy life.

Anyway who you name calling a boomer when you are one... ok boomer?

These subjective factors could likely lead to a more stable and healthy life. Not to mention wealthy life.

Not sure how you reconcile the avo-munching generations being more stable, healthy, and wealthy considering they're more indebted than any other generation before even getting on the ladder in the biggest debt-driven bubble in history. They're far more vulnerable, which is why I claim that boomer dreams and ideals don't fit with their reality.

There was a time where every town or suburb had a street or block that was affordable for FHBs. Now there are regions that might be affordable. 70% of your disposable income on housing in the North Shore?! The only way to get your own place will be to move away.

Owning a home for many FHB's will likely mean investing in the more undesirable parts of town or in towns that have low employment prospects. One of the benefits to renting is you are not tied into long term debt nor are you stuck in a residence with neighbours you dont like . FHB's might also find the properties available to them are in flood /risk zones and insurance premiums will be higher. The concept that many older folk live happy and joyous lives in their retirement as owner occupiers free of debt is dependent on individual circumstances. There are bonuses to renting particularly if you have saved liquidity such as rent rises /costs can be offset by TD or investment returns. Do not underestimate the power of savings because eventually you will reach a point where owning a house will be possible but even then one must determine is now the right time to buy ? Buying a home requires diligence and wisdom mixed with timing... Are you buying in a peak or a trough ? Are the mortgage rates likely to trend up or down in the next 5 years? Is the location one that shows promise? Can you get a better deal if you sit tight and keep saving? Is the build structurally sound? ...so much more to consider before you jump on the ladder...Why are they selling?...... Consider this also ...there will be some that bought at market peak and they may currently be under the pump in the present market . Are you sure now is the time to buy?

Go upmarket and aspire big... sarc. Unless it's worst house on good street

You still can make the house a home in Mangere/Otara or Sunnyvale, Bader, Porirua, Papanui.

Thoughts Nzdan?

I wouldn't suggest someone jumps head first into a property in a rubbish area, higher chance you'll have shit neighbors. But if that's someone's only option, they should do a few drive-bys of the property. Tuesday night @ 8 - 9pm (dole pay day) and maybe Friday/Sat night.

Can definitely make the house a home in any location, but everyone's different. If someone's ready to buy now but would rather rent because it's cheaper then all power to them. I personally don't think comparing the price to rent vs own is a prudent thing to do, particularly in the long run (even if house price inflation remains fairly subdued).

Sometimes the bad areas turn into good ones through urban renewal aka gentrification. Its not guaranteed as good areas can go backwards, depending on social trends

It is good to hear the stories within my family circles of the 20 somethings stepping up and buying a house

Or if they are young professional couples, skip Mangere/Otara or Sunnyvale, Bader, Porirua, Papanui and head West to Adelaide, Melbourne, Brisbane..

And retain the NZ home... ??

You aren’t getting it 😂

In jurisdictions with more stable housing markets, they have more disposable income, and these are the very types of questions they can ask themselves.

However, in NZ, you can be financially ignorant, buy a property, and look like a financial genius by doing nothing or not adding any value to the property whatsoever. It is far more difficult to make any unearned capital gain in a stable market without adding value.

The question NZers need to ask themselves is, if they were not going to get the unearnt returns that they previously had in property, and had that money to invest in other asset types, where would they invest it?

Any suggestions?

Pawn broker...? theres plenty more ... some are med / high risk like sports betting... some folk are living on the edge.... lol

That's my point. Under NZ's present system, the returns from housing have been great and the nearest other equivalent, for the low risk, is what?

But assuming house prices stabilize and no further capital gain other than at the rate of inflation, and that over time the housing affordability ratio is improved, and you have excess cash to invest, does NZ have the financial intelligence, or any local markets in which to invest it into to give them the return needed?

And if you want to live on the edge, become a property developer.

"? Buying a home requires diligence and wisdom mixed with timing... Are you buying in a peak or a trough"

I respectfully disagree. Succeeding with property has more to do with longevity than timing the market. The same with the share market or any other investment. Those who bought at the 2021 peak may feel down about it at the moment. But it is unlikely to matter in five years time. Time has a way of healing most bad investment decisions.

Why is 40% of your household income considered unaffordable in NZ when it's 28% in the rest of the developped world?

40% should be the maximum of all of your loans (mortgage, student, car, etc.).

This is a very good question. If it were indeed approximately 28%, it would make the affordability chart look even more horrendous.

Can the author elaborate as to why 40% was deemed to be the unaffordable threshold? Are we different and somehow a special case in NZ, compared to universal measures?

40% seems reasonable to me when buying a first home. 28% would be a walk in the park. But I wonder what you are buying for 28%? 1 bed flat?

Most people in NZ jump into the market with an actual house, often detached That is a luxury in many markets.

You're seing things the opposite way.

Are houses cheaper overseas (in regards to incomes) because of that 28% limit (often by law/regulation) or are they more expensive here because we allow 40%?

The real indicator missing is whether any capital growth is only at the general rate of inflation, ie neutral.

And if it is, how long will this go on (the new norm)?

This has implications for speculators, plus all those who are expecting to be the future beneficiaries of these super capital gains, ie all homeowners.

Coalition policy is to stabilise house prices so that over time wage inflation will make them more affordable.

This will allow more people to own a house and give 'extra' savings due to the more affordable price AND lower mortgage debt obligations.

However, it is not clear where these 'savings, can be invested in other investment types, and earn the same super profits that would have been earned in owning property. But they may not have to as your future expenses are lower also.

Labour also made this promise, but 'blind Freddy' could easily see that their policies would not work.

‘Coalition policy is to stabilise house prices‘

Haha. Is it now….

Yes, it's that same promise Labour made, but each has a different methodology, and ability to deliver. Labour blew their chance, and the Coalition have yet to blow or achieve theirs.

All parties want to make housing more affordable, but none of them want to do that by crashing the market.

Labour does too much of the wrong thing.

National does too little of the right thing.

What we need of course is a party/Coalition that does just the right amount of the right thing.

Do you really think the politicians want to make housing more affordable? Even those who are personally hugely invested in them being unaffordable, and are supported by donations from industries who want the same?

I think for a lot of them, politics is just a game and they say what they need to to get elected, to get what they really want.

For example: https://www.scoop.co.nz/stories/PA0708/S00336.htm . John Key campaigned and won on the platform of making housing more affordable. When in power he then suggested there was actually no housing crisis, and then made a crazy amount of profit selling his own mansion as it's CV increased 50% in three years. He was raised in a state home and then sold off a lot of state houses, and resided over the horrible 'meth contamination' debacle where hundreds of state house tenants were kicked out, and all their possessions were destroyed for no good reason. John Key is now a top banker who gets larger bonuses when house prices go higher.

Of course they don’t

Yes, John Key was a sellout.

As I have previously said the difference between National and Labour is that National doesn't do enough of the right thing (JK), and Labour does too much of the wrong thing (Kiwibuild).

But I think you are confusing politicians not wanting house prices to fall to make them more affordable as to make them more affordable by restoring the ratio between income and house prices.

If they can stabilize price rises to no more than the general rate of inflation, then wage growth over time will restore the balance. The best time to do it is at natural troughs in the cycle ie in the last two decades that was after the GFC with JK, and the second best time is to do it now, while prices have also fallen a bit.

National came in promising change, so let's see if they do 'enough of the right thing.'

"Coalition policy is to stabilise house prices so that over time wage inflation will make them more affordable."

How did you get this impression that this is their policy? I've never herd them say anything like that and their policies are unashamedly trying to get house prices to go up.

Labour's policies have been working - Investors pulled back and first home owners stepped up to a higher share of the market. Just wanting them to fail doesn't mean they did.

Under Labour housing affordability, on a like-for-like basis, has gotten worse.

If you read the Coaltions housing policies and understand the first principle land use policies they are trying to achieve, it is obvious they are trying to reduce restrictions to supply.

But no party, past or present, could afford to make housing more affordable by having an absolute fall in value. The way any party tries to make housing affordable is the relative difference between house prices and wages. You first start to achieve this by stabilizing the price of housing.

Any absolute fall in house prices is due to poor Govt. policies and/or execution, or other 'world' events over which they have no control. But no NZ Govt. in their right mind would deliberately introduce policies that caused absolute drops.

There is a lot I don't like about their policies in the fine-tuning of them, but they make far more sense than Labour's policies ever did.

"Under Labour housing affordability, on a like-for-like basis, has gotten worse." This is a convenient truth for those that don't like Labour but it's also ignoring all the details as to why it happened. If the pandemic hadn't happened then it would probably have been a different story.

National had backed off from supporting higher density housing - how is that helping with supply?

We've had an absolute fall in house prices and the world didn't end like so many vested interests like to scaremonger. There was nothing wrong with Labour engineering a fall after a short term blow off top except that property owning voters didn't like it.

The gnats introduced SHAs. ACT in coalition with the gnats created the supercity and the auckland unitary plan

Yes good points

Not quite correct.

Yes - the NACT set up SHAs. The Special Housing Areas (NACT got in 2008, but the SHA took until 2013, disestablished in 2017) resulted in lots of resource consents being issued but few buildings were actually built where they were needed. Lots of greenfield land suddenly became McMansion areas and roads quickly became clogged. It did however set the scene for what came next as enough apartment buildings were built using SHA provisions and people could see they weren't so bad and met many needs. (Many SHA consents sat on the shelf as the height limits mean just 4 storeys if my memory serves. The AUP went to six in many 'hub' areas.)

The NACT had little to do with AUP of 2016. The detail was led by a substantial left-bloc on council under Len Brown (elected Oct, 2010). The mantra, "go up, not out" became firmly established and huge tracks of land - where it was needed - became eligible for higher densities. AC did a good job (in the face of very tired arguments from NIMBYs) in communicating the benefits. The AUP 2016 is far from perfect IMHO. But it was a good start. The NPS-UD added impetus and the MDRS more. The NPS-UD in particular will change the face of Auckland for the better and we may even end up with a half decent public transport system thanks to higher densities.

The true measure of supply meeting or exceeding demand is that prices will, on a like-for-like basis, become more affordable.

This did not happen.

Allowances, both up and out are needed, but the policies are badly thought through and badly implemented. You can see the perverse outcomes that would happen from land use theory alone, let alone having to wait to see the result, and people are correct in rejecting them.

I doubt you’d ever get like for like price falls in bigger cities through increased supply. All new dwellings will either be on much smaller sections or in poor locations miles from the centre. Surely that makes the existing dwellings worth more.

The price of all housing is set at the fringe, if that falls, it will fall, relatively, all the way in. The evidence in any city in the world is very clear on this relationship.

But that is why the comparison should always be made, at least acknowledging, the like-for-like basis, otherwise, it is a false comparison to build a house at half the size and three-quarters the price of a comparable in quality larger and dearer single house.

If the acknowledgment is not made then it distorts the facts and hides larger systemic problems.

100 years ago an average person could probably afford a decent plot of land very close to Auckland CBD. There is no way that would be the case today no matter how much sprawl they built. The greater the population, the more the good land is worth.

I think it is natural for the average house to become less as a city increases in population - either smaller or further.

You are conflating issues.

In simple terms, you can't build a house half the size of another house and say they are equivalent comparisons regarding saying housing prices are falling.

The other comparison is that for the same house type, why are there differences in price between jurisdictions? The best measure to use is the median multiple house price to income ratio.

In many jurisdictions with far larger populations, the housing at any location or house type is way cheaper on a median multiple basis than the Auckland.

So if you are a multiple millionaire or first home buyer, you can buy the same equivalent for your income anywhere along the land curve from CBD to fringe far cheaper than you can in Auckland.

And the main reason for this difference is land use policies, that is all.

"In simple terms, you can't build a house half the size of another house and say they are equivalent comparisons regarding saying housing prices are falling."

Of course you can, that's why the tv programme is called location location location.

You're basically saying a Ferrari can't be worth more than an estima because it has less seats.

If you had read the thread I said on a like for like basis.

Your analogy is not relevent.

And the main reason for this difference is land use policies, that is all

Elaborate more please Dale

In summary, Jurisdictions with restrictive land use policies have expensive less affordable land and housing, and jurisdictions with less restrictive land use policies have inexpensive more affordable land and housing.

It's basically a land supply and demand issue explained by the likes of Adam Smith, Alan Evans, Alain Bertuad, NZ Productivity Commission Report on Housing et al, and the annual Demographia report. http://www.demographia.com/dhi.pdf

Yes, there are a lot of other factors that go into making land and housing affordable or not, but the degree they influence the price is a multiplier based on the land availability.

As the old developers saying goes, if the land is wrong, everything else is wrong.

The easiest way to check whether a land and housing system is dysfunctional or not is to compare median income ratios.https://www.interest.co.nz/property/house-price-income-multiples

Jurisdictions that have good land use policies have lower median multiples and those that don't have higher multiples.

Prior to 1993, NZ's median multiple was 3x median income. At our present multiple of 7.13, approx. 1/3 the value of an NZ house comprises non-value added costs due to monopoly mainly land use restrictions, which if removed would make housing that much cheaper, without changing the amenity value of the house. This amount is also that amount less you would have as a mortgage and pay interest on.

It should be noted that the median multiple figures can be manipulated to cover the real cost, in that todays smaller houses (in trying to keep the price lower, even if it also reduces the amenity you want), and two-income families (in trying to earn extra income to afford the smaller house), hid the true extent of the problem. If you were to compare it on a like-for-like basis to the 1993 ratio and house and income makeup, today's median multiple would be approx. 10x, and to the 1973 median multiple, today's median multiple would be 14x.

Lots of incorrect statements there Chris. Where shall we start?

The SHAs weren’t just greenfield areas. They applied to large parts of Auckland’s brownfield areas, and effectively brought forward the density under the *Proposed* AUP, in 2015/2016.

Secondly, the National Party had a HUGE amount to do with the AUP. For one, they established the legislation that required it. But more importantly, they introduced the NPS-UDC midway through the AUP process that set huge statutory expectations for the AUP in terms of development capacity. Then the National government of the time, through its agencies ( KO) made submissions on the proposed AUP, leveraging off the NPS-UDC. Because of these government submissions, the final operative AUP enabled MUCH more density and development capacity than the proposed AUP.

so actually the National government of the time had a major influence on the AUP.

Kiwibuild is Labour's signature engineering attempt at how they do things, which had nothing to do with the Pandemic.

They gave money in the Pandemic for it to be pumped into the wrong areas like housing which again is just poor policy and administration.

And then between them and the Reserve Bank needing to increase interest rates the trendline between top and bottom still shows housing has been getting more unaffordable, especially taking into account the increasing sacrifices people are having to make in compromised lifestyle choices and raiding the likes of Kiwisaver etc.

Housing, and in tandem rents, have to progressively get more relatively affordable otherwise if you think it's bad now, just wait. Increases in wages will have no effect as long as restrictions remain in the system that just allow any savings made to be recapitalized back into mainly non-value-added land price increases and council costs.

The solution is to allow more up and out, but the housing density rules introduced are poorly thought out and are a breach of the social contract that Govt. and council have an obligation to uphold.

There are far better ways of introducing higher-density provisions, but they are not smart enough or care enough to implement them. That's what the voters voted on in part.

I do wonder if a valid option is to hold off buying and pump a shitload of salary each week into Kiwisaver - like say 10-15%.

if you are age 25, you will have a lot of money by age 50. You could then buy then, or not.

probably not a great plan if house prices inflate like they have over the past 20 years. But will they?

i guess the other issue is rental tenure security, but hopefully that starts to get addressed by the burgeoning build to rent sector.

The BTR sector is going to run into headwinds, as it is not following the principles of a true BTR and is only a reaction and a rebranding of the present rental policy by most developers.

Some have a better understanding than others, but I have yet to see figures that show that are fit for purpose, for the occupant, long term.

Wow you are constantly bagging share markets with regular posts of negative returns. It comes across as anti shares. Meanwhile you also weigh up whether or where you can buy a section and do a t/house development hoping to make a killing. Flip flop.

Which advice do you tell your children or does it depend

Anti shares? Yeah, nah.

I have posted several times that I did very well with shares, selling up pretty much at the peak in 2020

But yes, I have been bearish / skeptical since then. But as I have said before, I will look at shares again.

As I have said before, I have been in a cash account in KS for a couple of years. That’s what I advised my son. In a year or two I will likely move to a balanced fund. Longer term I sit between bear and bull on shares.

Which peak in 2020? The S&P is up 30% from the 2020 highs, 35% from the pre-Covid high.

Getting out of the market is easy, picking the right time to get back in is extremely hard.

The numbers are a little gentler on a world index - VT would be +12% and +30% respectively. NZX has been pretty poor but I think it'd be unusual to invest your KS purely (even mostly?) in NZ.

I pumped the money that would have been going into Kiwisaver into the mortgage instead. Guaranteed return of 8% at the time.

Depends on family/life priorities I guess? As you say, rental tenure security when you have kids? I guess not all kids will mind moving schools a couple of times growing up, take one for the team for Dad's long term financial goals (gamble?).

Why move schools? Even if a landlord turfs you out, usually should be able to find another flat in the same general area / school zone.

I rented for 20 years with our kids, they never once had to change schools due to us moving rental property. In fact we never left a rental property unwillingly.

True, but *should* doesn't necessarily mean can. It worked for you over the last 20 years when the housing market was...less sick, not guaranteed to be the same going forward.

But hey, if someone is keen on making that gamble because it makes financial sense then that's their prerogative. Personally I'd prefer to do what I can to negate the potential of that happening, and if it means potentially forgoing making bank in shares then sweet as I'll take the house/asset.

Yes but the point I am making is that, in lieu of being able to buy a house, at least at ‘traditional’ house buying age - which is increasingly unlikely for a growing % of young people - you can still work towards something decent in terms of financial security.

For reasons both inside and outside my control I wasn’t able to buy a house until I was 47. But by doing quite well with shares, and being committed and disciplined with Kiwisaver, I am now in the position where I should be mortgage free by my late 50s. That will free me up to put huge effort into retirement savings for the last 7-8 years of my working life.

A related point - despite how things are portrayed, I don’t think there is only one path in both the financial and non- financial journey of life. It would be nice if this could be conveyed more often, it might give more people some hope and optimism.

Well of course, in lieu of buying you'd make the most of what you can financially. The NZX50 returned an avg of 8.8% pre-tax over the last 20 years. Back of the math calcs you'd have approx $2m compounded in 20 years w/ start deposit of $200k, so you could buy that $1m house if it only inflates by 3.5% p.a.

When presented with a choice between the two, it's prudent to look beyond solely a cost vs cost basis. There are likely plenty of people that could quite easily buy and intend on doing so, but are micro-analyzing the costs of rent vs buy and trying to time the market using a snapshot of today.

Well of course, in lieu of buying you'd make the most of what you can financially. The NZX50 returned an avg of 8.8% pre-tax over the last 20 years. Back of the math calcs you'd have approx $2m compounded in 20 years w/ start deposit of $200k, so you could buy that $1m house if it only inflates by 3.5% p.a

These returns don't make sense anymore considering that the boomers are hitting their twilight years. Asset ownership is concentrated in the demographic. You believe that the skint, broke avocado munchers are going to fork out ever-increasing prices for boomers' equities that arguably will be no more profitable than they are now? Possibly. But those young people will be little more than drones without the ability to think for themselves.

Great. Two 30 year olds

One buys for just 200k and the bank lends the rest.

The other 30YO waits 20 years to buy. That same house then costs them two million dollars as banks don't lend to 50 year olds because of their age

Yet some still label the young buyer as dumb as they did nothing to earn the capital gain 🤣👍

Such a boomer thing to say. If the fountain of wisdom is the water coolers of the world, you may be right.

Yet in overseas jurisdictions (like Austria) that both Labour and National want to model ourselves on with housing, this is exactly the scenario both people can do, with both of them ending up in the same place financially, even if they never choose to purchase.

Housing is more affordable, owning or renting. And most house buyers are older, closer to 50, and have large amounts of equity so banks will lend to them.

And the person who chooses to rent longer can put the funds that would have gone into servicing the mortgage into other investments that on maturity give them the money to buy a house at any future time and be no worse off than the person who bought now. Or the funds to keep renting in retirement.

It has to be remembered that there are good reasons why renting, at least for certain parts of your life, is more preferable to owning, even if you can afford to own. Research has shown that mobility is linked with increased income, and conversely that those who are 'tied down' with a mortgage are less likely to be able to move to improve employment and income prospects.

This 'buying too early' is one of the reasons for NZ low productivity rate.

Of course, NZ is not set up like this, although this has only happened over the last thirty years, so the main way we have been making our 'equity' is through capital growth through housing.

This is not sustainable.

Well put

100% agree Dale.

200k? When, 20 or 30 years ago?

But let’s say it’s 900k now. It ignores the fact that many CAN’T afford to buy, even if they wanted to. You seem to have this massive blindspot on this.

BTW, I bought when I was 47, if not 50. The bank lent to me, albeit I had a high (30%) deposit.

200k = 20 percent deposit for a million dollar home. Probably can find one cheaper but that was based on the example set by Nzdan.

Pay the deposit then 'rent' from bank. Pay 20 percent and get the rest for free

You had $210,000 of a 700k terracehouse ? 500k mortgage. If you'd bought 20 years earlier you'd only need 40k, but now have close to 700k equity of the whole house with most of the 160k mortgage paid. What were you saying about not buying young so that you would be better off. I suppose you still can't see it

You said ‘buying for 200k’. Work on your English if you don’t want to confuse people. Anyway I am pretty bored with your nonsense and the antagonistic approach you take, have a lovely day

Buys for just $200k, bank lends the rest, is what he said. So you put in $200k, bank puts in the remaining 80% and you pay rent.

HM could've got a headstart on himself so now doesn't want to understand. 🤣

No. If you buy something for $X then that is the total purchase price. not the deposit you put down. For heaven’s sake.

If I buy a car, and it sells for 50 k - I put down 20 k and borrow 30 k - I have bought it for 50k. Not 20k.

But again, wasting my time with nonsense.

Now you're just focusing on pointless off-track semantics. Both the renter and the home owner, assuming practically identical people, start off by putting in $200k. That's their "buy in" to their "investments" if we want to call it that.

For the purpose of this comparison, we are looking at the potential total costs incurred by the renter and the home owner over the course of 20 years. Arguably the home owner has spent more than $1m on the "purchase" because you're forgetting about interest costs.

As you say, 20% down, rent from the bank. Start with an asset worth $1m that will likely rise with wages. If the owner smashes the $800k mortgage in 20 years, they'll have paid $730k in interest working on 7.5% average.

Meanwhile the renter, if they start @ median rent of $580 pw with increases at just 3% p.a. ($20 pw), they'll have paid $834k in 20 years. Factor in rates/insurance costs for the home owner @ approx $250k ($8k + 5% p.a. compounded increases), throw in another $50k in maintenance, the renter is approx $200k ahead on expenses

All going well, the renter will have about $2m in 20 years (assuming 8.8% return pre-tax), so as long as rents/house prices only increase 3% p.a. they'll be in a position to buy the $1m house for $2m and will have saved $10k p.a. in doing so.

You're very good with presenting figures matey

What about send that to Mary Holm at the nz herald

A huge flaw in my workings too. The median house price in New Zealand is $800k, not $1m. Should be comparing median rent and median house prices, it's only fair right? So that $600k mortgage @ 7.5% over 20 years, the home owner has paid $550k in interest. That's $180k less than my previous calculations.

So.....with all these numbers in mind, the renter has saved $1k p.a. on their journey.

If you look at my previous comments, I'm talking about people that can afford to buy but are seemingly holding fire because on a cost vs cost or cashflow vs cashflow basis using today's numbers it doesn't stack up to buy. They're ignoring the long term numbers and how inconsequential it actually is over the life of the mortgage when compared to renting.

It depends where interest rates end up. If they stay around the current level, house prices won’t increase any time soon, so yes you would be better off investing elsewhere. If interest rates go down then house prices will go up and the mortgage repayments will go down so owning would be better.

The 2 biggest expenses for an average kiwi family will be housing and retirement savings. Most neglect the latter. Do everything to free yourself from the renting trap and paying the minimum on a mortgage.

It feels like many overestimate retirement savings. I keep hearing you need so many million to retire, but if you own your house you probably only need say 200k to bump your pension up by 20k a year until 75. After that you can probably live on the pension?

If you retire owning a decent 4 bed home, you can probably get that 200k just by downsizing. So you can probably have a good retirement with nothing but the family home. Appreciate comments from those with experience.

I also feel that retirement savings seem overestimated. I guess if you want to go on overseas holiday 1-2 times per year and lead a luxurious lifestyle you want $1 million plus.

I guess things like health insurance are very high when you are retirement age, but still…

My dad (83) seems to cope fine on the pension plus the 15-20k per annum he gets from dividends. And he manages to travel overseas once a year.

Bumpy ride ahead for some .... likely some will want out ... soon we will see how legitimate a few values are?

Half of mortgages in New Zealand are set to refix over the next 12 months and many - if not all - will shift to higher mortgage repayments thanks to the incessant rise in interest rates.....If you fixed your mortgage of $500,000 at 2.58% back in 2021 and are looking at having to refix that at 6.99%. That’s close to $500 per fortnight - or $13,000 for at least the next 12 months - extra you’ll make in annual repayments. (stuff 21.10.2023)....

Yep. At today's rates could be increasing payments by close to 3x. Don't forget council rates and insurance all way higher than inflation. Truth is coming in 2024.

Catching fire...

Surely most people are already on fairly high rates? I don’t think the 5 year rate gets much market share.

Once again we see the rent vs. buy argument surfacing. I'll just leave this thought here.

To be comfortably off come retirement it matters little whether you choose to rent or buy. What matters most is what you rent or buy. What matter most is constraining your wants so that you pay for only what you need. (An example is not spending every dollar the bank will lend you if you can spend less and pay it back faster. Or not renting something flash when ordinary will do.)

I disagree. 20 years ago you would have been significantly better off buying than renting. However that may not be the case for those buying right now.

I think you missed my point.

Mustachian?

Had to google that. But, no.

Evergrande just hit the wall, it will be interesting if this sends out any ripples.

I've noticed an auckland multilevel resi developer "Evergreen". Probably no connection, hope not

Tavi valve, $60k at The Heart Group. Not reimbursed by Southern Cross.

Med Insurance $1000/month for my parents (83yrs). Yes, $1000. When I look at the use my parents have had it’s been a break even.

Add in a few European trips, across the ditch to escape winter?

Conservatively you need 20k/yr on top of the pension, preferably more. Now kiss goodbye to the pension.

Massey Uni published recently how much they think you need: Single vs couple, rural vs urban, basic vs comfortable. IIRC the top amount was $1m. I think that underestimates by a margin

Sure if you have health insurance you will need a lot of money, it gets very expensive as you age. I’m not going to spend my whole life saving for that, I’d rather spend more now and cross my fingers with the public system.

Mortgagee sales back up to pre-Christmas levels.

Current 53 nationally - around the top number listed last year. Remember that mortgagee sales generally run to a fixed sales timeline so they they don't sit around unsold until they sell. I expect this number will climb quite a bit as we move through the year.

https://www.realestate.co.nz/residential/sale?by=best-match&k=mortgagee

To be fair 34 out of 53 are apartments in 1 building.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.