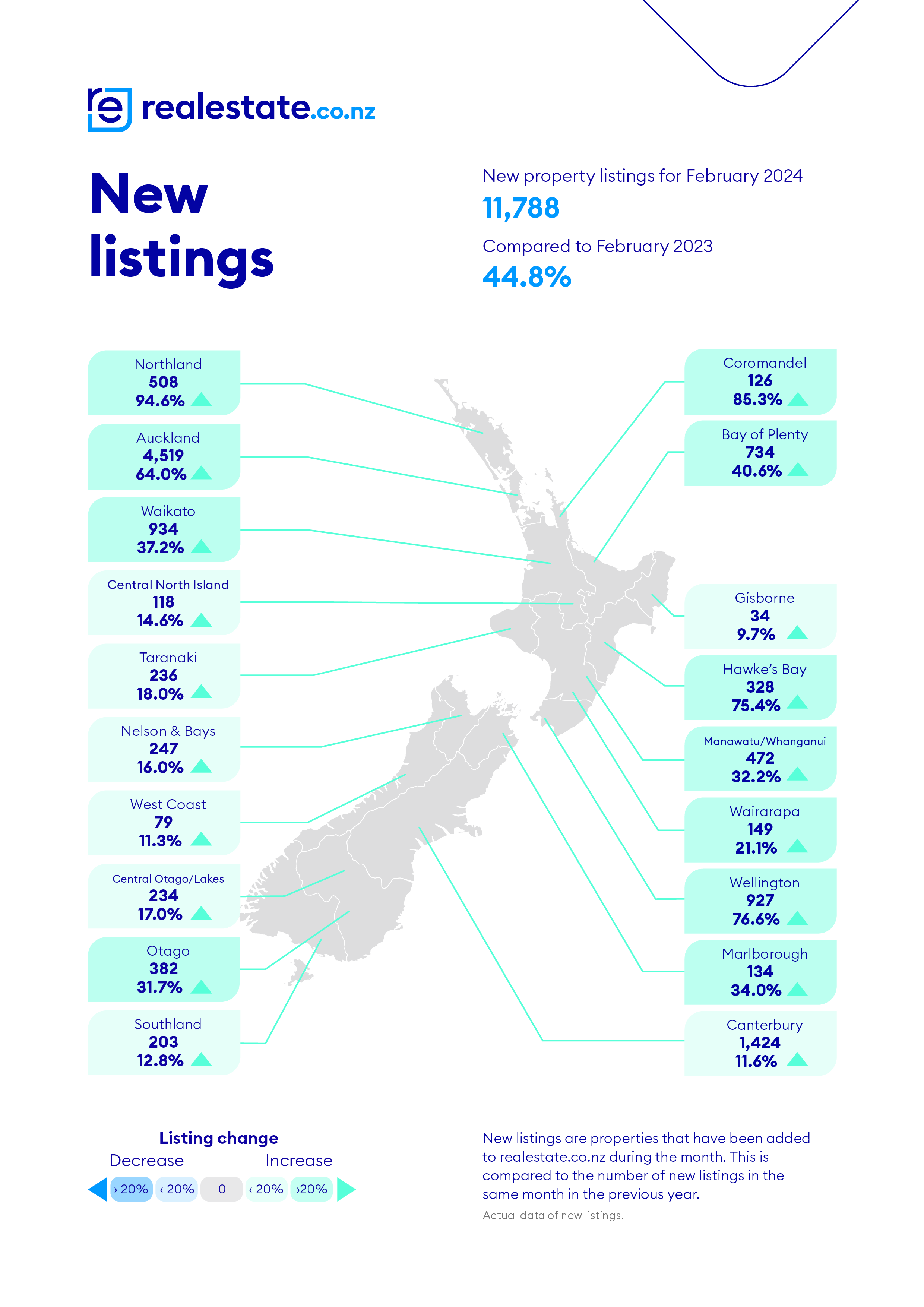

The housing market was flooded with new listings in February, giving buyers plenty of choice.

Property website Realestate.co.nz received 11,788 new residential listings in February, up 45% on February last year and the highest number of new listings the website has received in the month of February since 2017.

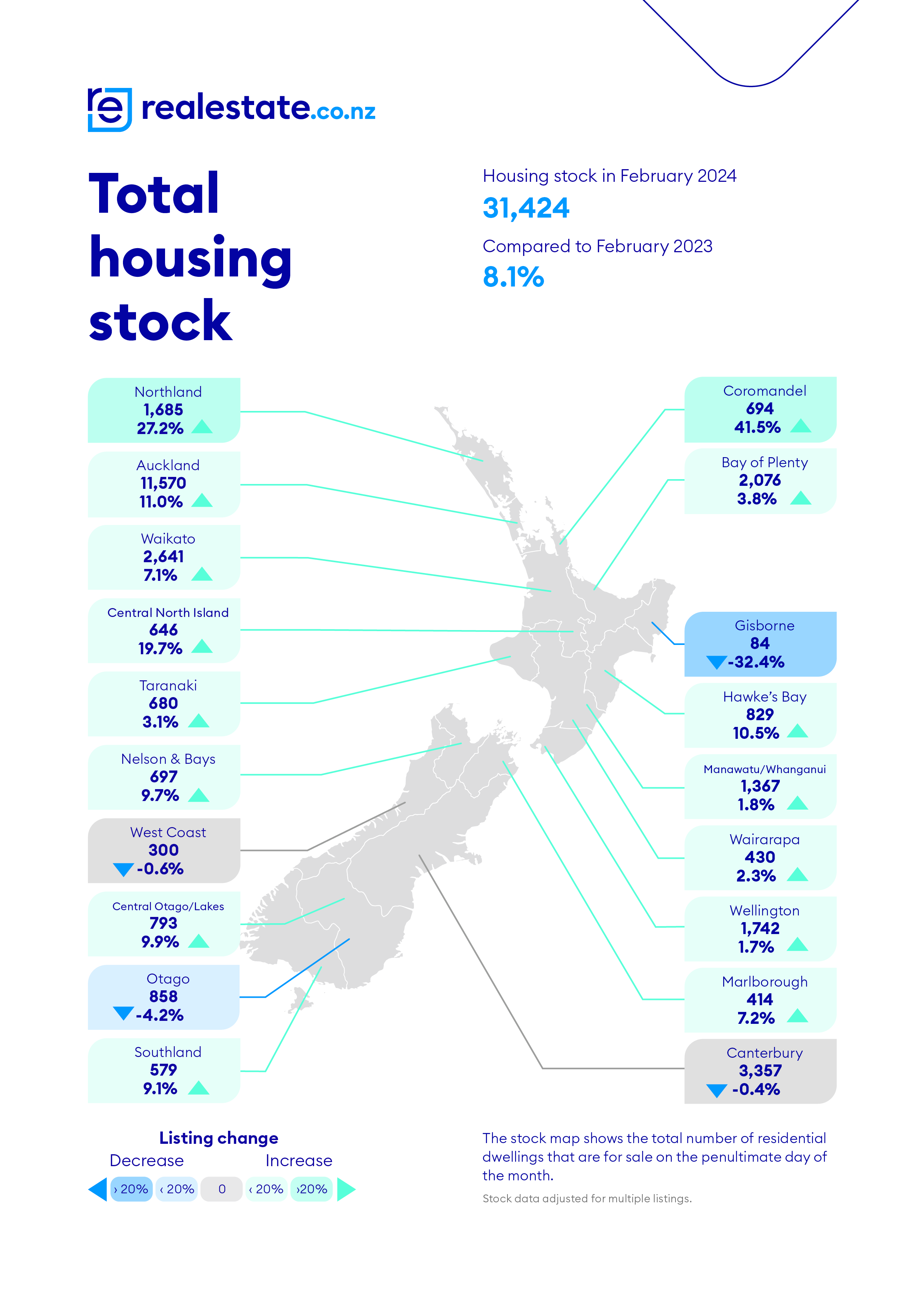

That pushed the total number of residential properties available for sale on the website to 31,424 at the end of February, up 8.1% on February last year.

That means the amount of stock on the market at the end of February was the highest it has been in any month of the year since June 2015.

It was also the only time since November 2015 that the total number of residential properties for sale has been above 30,000.

The increase in stock for sale compared to February last year was almost nationwide, with only Gisborne, West Coast, Canterbury and Otago recording annual declines in stock levels.

That gives potential buyers plenty of choice and reduces the pressure on them to commit to a particular purchase.

It is also likely to make them very cautious on price, which means vendors will need to be realistic in their price expectations to achieve a sale.

However it appears that message may be slow getting through to some vendors, with the average (non-seasonally adjusted) asking price on Realestate.co.nz shooting up to $927,312 in February. That's up 4% compared to January 2024, and was the highest it has been since October 2022.

The comment stream on this article is now closed.

Note: Auction results delayed.

The Auction Report which is usually published each Saturday has been delayed this week due to technical difficulties. We expect to publish it on Monday.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

175 Comments

It’s hardly ‘plenty of choice’ when the prices are still at ridiculously high levels.

"Choice" and "Price" are two different things. With more vendors out there, there is indeed more "choice" and as a result, a buyer is more likely to find a vendor who is prepared to accept a lower offer, hence reduced "price".

Finding that one vendor doesn't equal plenty of choice though.

Not sure the point in your response. Choice is obviously directly related to what you can afford.

Is it really?

Choice relates to the number of properties available for sale, it has nothing to do with what Pete, Jane and Tracy can afford, which is likely to be very different from each other.

Affordability is totally independent of the number of properties for sale, it is specific to the person wanting to buy. Also it can change over time, independently of the number of houses for sale.

Yvil, "choice" and potential choice are two different things.

Unload the specu houses before the prices drop. Gonna be scary come mid year and the flipper tax is shorted.

Will the rush to the exit become a stampede.

Want to sell isn't have to sell. Index up 1.6 percent in 3 months

Sell and live where ? If there is a stampede then rent prices will skyrocket.

Spec box's generally rented. Don't tell me landlords put tenants need for shelter over tax free cash out?

Sell the rentals so for lower prices and renters will be able to buy. Less renters in the market so no pressure on rents, and a more sustainable future for all. In an ideal world anyway.

Many renters will never have the financial means to buy, there is a sub prime section.

Yes that's true. And many do have the financial means to buy at lower prices. Like all the hard working people that would have had no problem buying if they were born in an earlier decade.

For sure I feel sorry for the trapped middle..... many of which are leaving for aussie

For sure I feel sorry for the trapped middle..... many of which are leaving for aussie

If they're "trapped middle", IT GUY, then they wouldn't be able to move to aussie. (Trapped means Trapped.)

TTP

Imagine trying to sell a new build in 4 months time, when all the 3-5 year old townhouses hit the market for $100k-$200k less, and they all rent for the same amount of money as the new build. The investor market (if there still is one) will be dead for new builds.

"Imagine trying to sell a new build in 4 months time"

Current number of newbuilds listed for sale on trademe: 5,891

This newbuild has been listed sine June 2023 & still unsold (9 months so far)

https://www.realestate.co.nz/42373336/residential/sale/3-33-stanley-ave…

@Averageman - that is true - i listed my Te Atatu house on Friday its rented 2 days later - most people was saying their landlords are selling, a majority of them stated they lived in town houses, I feel townhouse are going to be difficult to sell or buy in future, imagine you buy house 2 of 4 and house 1 and 3 is badly maintained it will drag your house price down right? (if no body corporate) ............In addition due to house prices levelling I just landed my dream home in Grey Lynn. Your statement above might be a silver lining rather than a dark cloud.

Some of the figures would be more comparable if adjusted per capita IMO. Since 2015 population has risen 600,000

Why would 'per capita' be helpful. Wouldn't 'by total number of dwellings' be better?

That goes hand in hand one would think. Confirms that some relativity is needed

If you look at the two sets of data in conjunction with each other, you can get some context. You can consider each area/city as a reservoir, the new listings filling it up…. Then the housing stock level gives indications of how the listings are selling……how the reservoir is clearing out.

Some local knowledge is helpful, Wellington has had low stock levels most of last year, so excess listings have just topped up stock, Christchurch appears to clear well - listings in clearing out as sales. Aucklanders will know best the context for Auckland, but Barfoot and Thompson reports plus auction sales suggest sales volumes are low, therefore high listing numbers will be resulting in excess stock as shown.

This data is compared to 12 months ago, which was not really a normal market, but hard to look at any time in the last 15 years and say which part of the real estate market was the “normal” bit.

TradeMe tipped over 43,000 listings this week. Over 32,000 in NI alone.

My prediction for the year was flat nominal house prices. If this surge continues, mortgage stress keeps rising and there is an exit with the tax changes, then that prediction will be very wrong.

Highest stock level and highest asking price = few sales. Vendors are going to have to be more realistic to achieve a sale.

It's likely that prices in April will drop, as some vendors will accept lower offers after if not selling at the usual peak selling month of March.

QV HPI shows prices up 1.6 percent over 3 months. Strong performance 6.4 annual. Im looking further afield to get a good place

REINZ HPI, the gold standard, shows flat for NZ over 3 months and a 1% drop for Auckland.

Lies, damn lies and statistics 🤣

I think it is still a good time to buy the right property. I can't believe that maralago is valued so high when it is so close to the waterline. Could be washed away oneday.

Step 1: vendors realizing interest rates are not dropping anytime soon, so might as well list now

Step 2: houses market is slow, forced to drop asking prices

Or at least that's what some people want. And so tell themselves that must be what's going to occur.

Keep fighting forces as long as you wish.. gravity will have the last laugh

Luckily, we're not talking about gravity!

Cope.

Don't prove that you're a moron, everyone else understands what is being referenced here

Hmmm, you always revert to name calling and being rude when you don't have a proper argument. Yes gravity pulls objects down, but RE has nothing to do with gravity, you're just making a silly comparison between two unrelated matters. Gravity has pulled matters down long before Newton discovered it, yet Real Estate values have gone the opposite way for all this time.

So so boring.

No counter argument either then...

Comparing RE to gravity is as silly as comparing RE to rockets in order to conclude: "it can only go up"

Ok, it's like lecturing a school kid..

A rocket can only go up provided the payload is at an optimal weight.. else GRAVITY takes over.. even elon musk can't override that...

Back to RE , fundamentals (affordable housing/ interest rates/ inflation) is the gravity being referred here

Gravity of RE affordability. I don’t understand the antagonism on this website.

Good points Yvil

Step 3: Wealth effect evaporates as vendors realise and finally internalise that those numbers on an REA’s screen mean nothing on terms of real value for their property unless someone offers that figure to them. Spending drops even further, job losses increase, recession hits full swing

@DGM @yvil

Step 1: vendors realizing interest rates are not dropping anytime soon, so might as well list now - I just rented out Te Atatu property cross leased however free standing for what I thought was good price i had listed Friday had 7 viewings the very next day and property is now rented ie sunday - everyone is stating land lords are selling due to all reasons mentioned - point being don't sell there is some really good tenants out there very grateful for homes.

Step 2: houses market is slow, forced to drop asking prices - Yes however stabilising I think it is a good time to buy and I just did. So taking my own advice. No sprooking

I feel with a bit of common sense and going a bit against your advice might be a good solution. DGM I feel your notes are not 100% accurate there is a way here to make hay, not easy however I believe my strategy is paying of given the negative feedback i am about to receive I am hesitant to mention how property investing has really helped me.

I wonder how many are ex-rentals?

Browsing through the latest listings show a lot of 'not really loved' homes with recent internal 'bare minimum' makeovers.

Un-rented ex-rentals with mortgages will be costing the owner. We could see some sharp price movements as owners exit quickly rather than accumulating more losses that will only get greater if prices fall further. That said, some (many?) owners may just be testing the water and the property could be withdrawn and reenter the rental pool. There's one way to find out I guess. (Starts phoning agents of what look to be ex-rentals ...)

It is the marginal buyers that set the prices. The ones forced to sell at whatever price clears the mortgage.

"The ones forced to sell at whatever price clears the mortgage"

The ones forced to sell at whatever price.

Some sellers will sell at a price below the outstanding mortgage - these are people in negative equity. After sales proceeds are repaid to lenders, if there continues to be a shortfall, these borrowers will still owe amounts to their lender.

Lenders may be unable to collect outstanding amounts which will mean writeoffs.

Or the borrowers may find they can afford to pay off the $100k or so they still owe on the mortgage at $150 per week.

Cheaper to rent @ $700 and pay $150 than to pay $1200 per week on the mortgage.

"Or the borrowers may find they can afford to pay off the $100k or so they still owe on the mortgage at $150 per week. "

Yes, you are the correct.

Those in negative equity are likely those that have taken on high amounts of debt relative to the current valuation of the residential dwelling.

Many of these borrowers may be in cashflow stress as they took on mortgages that now take a large proportion of household income.

Borrowing 6x debt to income at 7% mortgage interest rates is 42% of the household income on an interest only basis before any principal reduction. At say 4% mortgage interest rates, that is 28% of household income on an interest only basis.

Household wage and salary increases are unlikely to have increased to offset the increase in mortgage payments.

Some households may even experience declines in household income, which increases cashflow stress. How can household incomes have fallen in an environment of rising wages and salaries? Some ways that household incomes may have fallen:

1) waged households - fewer hours worked as their employer experiences a decline in revenues - e.g retailing

2) commission earning households who have experienced lower sales volumes - e.g real estate agents, mortgage brokers, car salespeople, boat sales people

3) bonus earning households

4) job loss

5) for business owners, profits may have fallen

6) some business owners have now closed their business due to the business activity being cashflow negative. Business owners who took out loans to finance the business and had to use the family home as security for that loan. So the business has closed down and the mortgage is still outstanding. Not a good place to be in, if the LVR was high & has increased even more due to falling house prices. Some borrowers could be in negative equity.

The next 6 months will be an interesting case study. My suspicion is that house prices are not that sensitive to supply for a number of reasons:

- Interest rates dominate as people tend to reach for the best house they can afford (which is capped by the mortgage payment cost). When rates start to fall over the next few months, prices will go up because...

- School zones, public transport, amenities, etc make competition for some houses fierce despite the expanded supply - keeping prices high

- Every sale is basically an auction and people overcommit to the house they want (and realtors are expert at creating bidding wars)

- Prices won't drop below the level that yields a decent rental income as investors will step in

- Kiwis basically expect house prices to always go up over the long-term

"When rates start to fall over the next few months, prices will go up"

If you're so confident of this, why are you always arguing that we need a lower OCR? Do you disagree with the consensus that our elevated house prices are a disaster for society?

His usual OCR opinion is based on minimising the impact of a recession and the spiralling effect of high OCR on business debt cost which flows through to the public in the cost of Goods and Services. Housing is a separate issue

My argument is not 'OCR should be higher / lower', it is that wiggling the stupid interest rate lever up and down to 'control' a ridiculously complex economy is next level dumb.... Want to get the perfect balance of house prices, growth, worker / business bargaining power, wages, rental supply? No problem sir, just push this lever up or down and say very serious things.

Our house prices are criminal - locking in generational inequality and providing a profits feast for the banking and real estate sectors. But, if we want to get house prices down we need to fundamentally restructure our economy. Our tax system would need a complete overhaul - land taxes, inheritance tax. capital gains tax, incentives for safe saving (National Savings, Green Bonds etc) - all designed to stop houses being used as stores of wealth. Our welfare system would need rebooting to enable older people to live well and get the care they need without relying on selling houses / land. And, if that wasn't enough, lower house prices would mean mortgages would be paid off faster than they were being taken out, removing the flow of credit stimulus that sustains our economy. We would have to have an actual economy - where we broadly balanced our trade with the rest of the world, made strategic investments in infrastructure, business growth, energy self-sufficiency etc.

Too bad the phoney, fake ‘leftists’ of the previous government chickened out from proper tax reform. Talk about a massive missed opportunity.

Oh but they tweaked the tax settings for property investors.

Whoopdee doo

Would it have mattered? This govt would have repealed it immediately on ideological grounds. Now we're left with a govt that is reversing the very minimal progress Labour made.

I'm getting the distinct feeling people who voted for this coalition are getting more desperate as "their team" continue to take us backwards. It seems to be all about critiquing Labour, where is the great stuff the govt is doing to get us back on track. Tobacco laws? rinsing the taxpayer by taking dubious entitlements? Foisting more costs onto Local Govt to try to avoid blame for cutting services? Come on HM, pony up some of the good stuff your team is doing rather than critique the previous govt.

I think like your calls on interest rates and the economy you made the wrong call at the election. Man up and own it.

Many of the best comments I’ve read here are from people who seldom comment.

But polls say approval of this government is improving.

locking in generational inequality - so true - so sad.

Not good for the older folks now trying to sell family homes either - as the cost of retirement villages is so high the family home even at these prices won't get them enough to move into residential care facilities. New residents coming in has stalled.

Was talking to someone in that industry - and he said none of the big players are building/expanding at the moment, for this very reason. They remain profitable, but (he thinks) not for the long term.

Bit depressing.

As house prices have been falling, close relatives at one Ryman retirement village have heard that Ryman have cut their selling prices on existing dwellings as well as quality of services.

The aged care sector is a property development business with a side line in caring for old folk. Once the big financiers get involved and start leveraging the equity ita the beginning of the end. Also means that their fortune rises and falls with property values

I've been involved in building elder care and retirement villages so know the cost of construction & maintenance. I also have a fair idea of what they pay the staff that operate the facilities.

The difference between their input costs and what they charge is criminal, should be up there with supermarket and power company cartel behaviour IMO. My father in law slaved 60 years building a profitable business and home only to have it sucked out of him in 5 or so years by these parasites.

... Here for each other...

"My father in law slaved 60 years building a profitable business and home only to have it sucked out of him in 5 or so years by these parasites"

Is that when your father in law was no longer living independently and required assisted living? I think assisted living costs can get extremely expensive - a family friend's mother has health issues and will be requiring assisted living and the cost was in the region of $2,000 per week ($104,000 per year). At that rate, any wealth can be spent quite quickly.

Yes I should have said assisted living, he's in a dementia ward, very sad. About $75k per year, so about $375k in to date, but probably not long to go now. Not much left over for my mother in Law who probably still has 15 years or so to go. The family exhausted quite a few avenues finding the best fit solution for them both.

My retired sister living in her own home in the US pays a monthly charge simply to reserve a spot if/when she needs assisted care. It's a racket for sure. Will only get worse here, I suspect.

A bit like daycare - we need to get back to a social condition where one parent/caregiver stays home and raises the children - and as for aged care - we need to get back to a social condition where one child or grandchild stays home and cares for their elders.

So, how do we achieve that social condition?

To me, this is the way we need our governments to start viewing enabling policy for that future and actioning the levers that will achieve that end goal/social change.

Improving your yield is easy, all you have to do is accept the value of your property is less.

Definitely worth revisiting this post in 12 to 24 months. (Nothing indicative will happen in just 6 months IMO.)

My suspicion is that house prices (outside the top end as you likewise recognize) are very sensitive to supply.

With recent history showing house prices do fall, I expect buyers will be more cautious in maxing out what they can borrow for 5+(?) years. And yields for 'real' investors suggest prices need to fall further before they'll be interested. 'Pretend' investors banking on capital gain must see that a capital gains tax has to come soon (within 10 years?) and they should be more circumspect. Hopefully they take on my comments about intensification too. Absurdly low mortgage interest rates won't be coming back (albeit they currently cloud many people's thinking). DTIs are coming and they'll be ratchetted down to more sane levels over time.

I believe most people are sick and tired of how the market has operated since the 80s/90s when the Nats made tax changes that started the free money tree and they will continue to demand change.

We live in interesting times.

Very fair and all plausible outcomes - although I am not as confident about the foresight of buyers (capital gains) nor that the same dynamics that keep top end prices up don't apply at the affordability tiers beneath.

My key question really relates to the money tree. Without that net flow of credit (around 5% of GDP) our economy will tank. Perhaps we will get back to what we did between 1930 and 1990 - use the govt balance sheet and infrastructure investment instead?

I'm likewise concerned about what stable property prices would have on credit creation. But less concerned if construction of new dwellings ramps up again as that's a source of credit creation. (It could be quite significant in fact.)

re ... "I am not as confident about the foresight of buyers (capital gains)".

Me too. Kiwis have shown over and over again that they're terrible mathematicians. I mean, really, really bad. And worse, easily swayed by the fake wealth those involved with property love to spout. All we can do, with assistance of sites like interest.co.nz, is keep presenting the facts and numbers so that Kiwis wise up.

I live in hope that media will take a good hard look at the maths that people like CN and others present, and they finally realize there is quite another side of the story to tell. A far more truthful side.

And of course, it is becoming clear that voters in NZ are getting very tired of NZ governments that do little or nothing to adjust settings to improve how we utilize capital so they can remain 'safely' in the middle and upset (beneficiaries excepted) as few as possible. I'm also beginning to see far more ire directed at the RBNZ's behaviour too. I expect this anger will grow likewise, more so as their actions during covid has created a permanent group of people who have lost out (big time) that is unlikely to forget their ineptitude.

I remain, as ever, an optimist. ;)

1) "Kiwis have shown over and over again that they're terrible mathematicians. I mean, really, really bad."

Financial literacy is low in general globally.

2) "And worse, easily swayed by the fake wealth those involved with property love to spout."

There will always be property promoters with their vested financial self interests as they need to earn income to pay for the living costs. Property promoter businesses need to earn revenues to keep the profit focused business operating.

3) "I live in hope that media will take a good hard look at the maths that people like CN and others present, and they finally realize there is quite another side of the story to tell. A far more truthful side."

The vested financial self interests in the media dominate as these profit focused businesses need to survive.

Look at the findings out of Ireland -

https://inquiries.oireachtas.ie/banking/hearings/julien-mercille-on-the…

"I believe most people are sick and tired of how the market has operated since the 80s/90s when the Nats made tax changes"

Can you expand on the specific tax changes are you referring to?

126,000 people coming into the country each year means house prices won't drop that much. It's done on purpose for that reason I reckon.

Looney Left did not want to go into election with a sinking economy

Does mean much when they are 20+ to a house......

I'm sorry you have to live in such crowded accommodation Gecko, this is unacceptable. I hope you find more space to live in soon.

Stop the attempt at comedy Yvil the DGM's are at breaking point and cannot take it. Gravity is in fact having the last laugh as they leap off a bridge.

Geez.. you're getting desperate..

Overcrowding isn't funny. Talking today with an extended family of 8 living in 82m2 - no garage, no dining room - hence no dining table. One very small bathroom, no separate toilet. Unless you see it and experience it for yourself - it's pretty hard to imagine. Children's oral health suffers because teeth just don't get brushed in amongst all the other competitive uses for the tiny bathroom. It really is so very sad - kids are always sick, so parent/caregivers lose their jobs because the kids need so many sick days and someone has to be at home with them.

I feel truly guilty. Have got to find a way to help - high rents and high house prices are the most cruel thing a society delivers.

"Overcrowding isn't funny. Talking today with an extended family of 8 living in 82m"

Unaffordable rents, and unaffordable house prices have other unintended consequences.

Reduced cash in households (due to unaffordable rents, unaffordable housing) can lead to couples having children at older ages, fewer children or even no children. So organic population growth is lower.

This results potentially in a lower tax base (excluding immigration) in the long term.

Unaffordable housing leads to lower home ownership rates, higher number of households requiring social housing, higher number of households requiring housing subsidies.

As government spending on housing increases, less money is available for other government spending such as health, infrastructure, etc Depending upon government policies, this might lead to increased government deficits, increased government borrowing, decline in government services or increased taxes.

Lee Kwan mentioned that he believed higher home ownership rates also led to safer communities, with lower rates of crime.

Lower rates of home ownership also leads to increased wealth inequality and the consequences of that.

Yes, to all of that. I've written to Chris Bishop re-introducing my regulatory proposal for the rental market (last year put it forward to a SC who didn't take it up) - perhaps this new government will see just how devastating all of these unintended consequences are.

A circuit breaker is needed - just as the Lange/Douglas knew was needed on their arrival at the 9th floor. They had guts (went too hard, too fast) but still "shocked" us into a new beginning. And from all the economists I've spoken to or read - it was needed. But that time has passed - this next new beginning (oddly enough) to my mind calls for more regulation (perhaps we should call it re-regulation) to curb the excesses of capital.

Thank you for your continued efforts for improving the quality of life for the most vulnerable.

Oh good on you Kate, I admire your moral sense of duty I really do. Unfortunately, anyone who has represented the tobacco industry is not going to share your social conscience.

The house price explosion has been New Zealand's biggest social disaster.

I don't have a neat solution. But a population target and increasing home ownership (somehow?) over rental would help.

Most of those people are low skilled workers on low incomes, working holidaymakers, and international students, who cannot afford to buy a house even if they were legally allowed to (which they are not, as immigrants without permanent residency are included in the foreign buyer ban). What it will do is drive rents ever higher as investors look to sell up come June and the supply of rentals starts to shrink.

The only reason housing hasnt crashed yet is because of the 210,000 brand new permanent residents that Jacinda blessed with the ability to go buy houses using NZ taxpayer funded FHB grants and Kainga Ora loans in 2022-23. Once that huge bulge of buyers is digested the market will begin to reflect the real lower numbers of buyers.

Strange. When I put my home on rental last time, the vast majority of applicants were Kiwis who I assume cannot afford to buy a house..

re ... "Most of those people are low skilled workers on low incomes, working holidaymakers, and international students,"

What a load of b.s.

If my tenants are anything to go by, almost all are kiwis! And none would be classed as "low skilled", nor "working holidaymakers'.

Be Quick

Been saying for ages the market will stay flat for 12-18 months.

You've been right for ages, then.

So in one article I read big drop in price that FHBers are paying, and next article big rise in houses for sale... this seems to point to further price drops ahead... That is if the vendors really want to sell, perhaps they just like laughing at "Wasting everyones time" level offers..... while the buyers are laughing at "Wasting everyones time" ask prices.

Oh well Real Estate agents have nothing better to do then sit in the gaping chasm of bid/ask spread

The trouble we have in our area is that houses purchased at the height of the market are now resisting, but vendors are trying their luck at getting back what they paid for it. That is they are asking the new purchaser to make a donation to them to cover the $200,000-$500,000 that they overpaid during the peak time, because they didn’t understand how to judge the true value of a property.

Wait one minute, the banks will hit em right between the.... then step up

FH I don’t want to buy at mortgagee sale, far from it. I don’t want to get involved in someone else’s misery. But seems that with many hundreds of people not paying their mortgages and the banks not doing anything about it for prolonged periods the market is less likely function in a normal way.

It cannot keep going up and it must come down. Buyers don’t have to buy, but some sellers have to sell. The sooner we set new price levels in the market the sooner the market will begin to function correctly again. Buyers are not going to, as is currently being hoped, pay the extra price because someone made a foolish purchase in 2021.

You have just detailed why the issue is humans and their resistance to change behaviour and viewpoint based on real evidence and cling to a reality that no longer exists. Like paying one credit card off with another and another while smiling and sweating, the party comes to an end eventually.

re ... "cling to a reality that no longer exists"?

You sure that applies to all of them? Most I spoken too understand the reality but are 'hoping against hope." Hope that the RBNZ could have provided had the RBNZ not been so backwards looking.

The “Hoping against Hope” is that some foolish uninformed buyer will come and pay the old, high price? That just pushes the problem on down the line. It feels really unethical that houses are being pitched so high by agents, valuation sites and previous sale information are being turned off so buyers can’t even see the property history. During the upturn prices were quoted verbally and published immediately as deals went unconditional, now they are all hidden for as long as possible. I wish this was a more regulated market

Yes I recall the other week seeing an old newspaper snippet from the 90s of house prices. Every single house had a price. Not "BEO" or any other nonsense, just a price.

You must be over it by now, ready to throw the towel

Buyers don’t have to buy. We will sit out until the market is right. We now have a list of around 10 properties that we can choose from when the prices are more stable - they are not going to sell currently. We are just very happy to have not bought and then seen $500,000 of our cash been eroded by this “blip” in the market.

👍

"We are just very happy to have not bought"

Good for you.

"and then seen $500,000 of our cash been eroded by this “blip” in the market."

If the purchase had required an extra $500,000 mortgage compared to today, then the current owner has the following impact

Extra $500,000 mortgage at 7.34% interest rate for 30 years is $41,678 per year. (this is the extra amount compared to a buyer today with a mortgage of $500,000 less)

30 years of extra payments of $41,678 is $1,250,342 over 30 years. So the previous buyer pays $1,250,342 over 30 years for the same house.

If the buyer today saves $41,678 per year and deposits into a bank account at an after tax rate of 4% (33% tax on 6.0% deposit rate). then at the end of 30 years, a buyer today would have $2,345,336 in 30 years available for retirement.

The numbers are significant and potentially life changing.

Also refer in this thread my example of Dec 2021 buyer vs Buyer today example

"During the upturn prices were quoted verbally and published immediately as deals went unconditional, now they are all hidden for as long as possible"

Price transparency can be one sided. In a environment of rising prices, this influences buyer house price expectations, and can create extremes, due to fear of missing out - conditions which real estate agents like and want (i.e aggressive bidding competitions between multiple bidders).

Wellington was revalued in September 2021. So many properties being offered way, way below RV. The new valuations are due this year - I just can't see QV dropping the rateable values to reflect current market prices.... but they really do need to, sadly. I just don't know whether the banks will want them to.

Why wouldn't they? Their job doing the rateable valuations is to assess the current market values (though desktop based) so that rates can be proportioned out amoung us. Are you saying they complete rateable valuations to suit the banks?

No I don't think so, but as the poster below observes, most QV estimates of market value are running around 25% below the 2021 RV. Think of the billions in value that will be wiped out if they re-value downwards. It must have implications for the way banks assess/account for portfolio risk. But I really have no idea as I'm not a banker or an economist. I do also wonder about insurance policies. If one insures for more than an asset is worth, I can't see them wanting to pay out a number based on unrealised capital gains from the market peak once asset values drop?

Again, no idea as I've never seen anything like this in all my time owning homes in NZ.

Or they can just do impartial valuations whether values are increasing or decreasing

I take your last point. I haven't seen this scenario before either. What are the unintended consequences ....

Hmmm hadn't thought your other points too. Thanks for explaining.

I wonder how many mortgage free people that are would pay to have their rateable values reviewed if they don't like the QV one (as in its too high). Then it lowers their rates. Used to be the other way around - valued too low don't like it as im selling - but if rates are exploding like they look like they will and you could save yourself several hundred $ per year and are in your home for decades to come....

Probably an unlikely scenario - little thought experiment.

We objected once about a review being too high. Lived on a postage stamp of a cross-leased section on the beachfront on the Kāpiti coast. Calculated that our land value was the highest (a real outlier) in the district on a per square meter basis. Didn't get my way on that one.

I think they have to. The role of QV is set out in legislation and is overseen or at least audited by the Valuer General.

They do a good job of updating estimates on each address ( for residential property) on their website, in a steady market these updated estimates are often bang on the subsequent sale price - in these crazy up and down markets they can be a good benchmark to indicate early drops or rises. So if you search a Wellington property the site will show you the valuation struck in 2021 and the current estimate - at present the estimates look to be at least 25% lower than 2021 RV. I suspect this estimate data becomes or at least forms the basis for the new RVs when they are struck. QV are delaying the release of RVs at present, it may be quite a complex task in the current market with such tiny sales volumes.

by Beanie | 7th Jul 22, 10:08am

My friends went unconditional on their next house before even listing their old one. 2 months later it still hasn't sold. Don't be like my friends.

Update on my post of 20 months ago: It's been a disaster for them. The first house is still unsold as they are waiting for someone to pay too much for it. The second house was paid for on settlement date only by liquidating all other assets and borrowing the difference. It was then damaged in the cyclone a year ago and so they had to borrow more to help pay for repairs. The financial stress added to other problems and one of them has moved out and into the second house. This has also been on the market for a while now, but buyers are put off by the slip above. To drop the price on either house to meet the market would crystallize their actual financial position to one far lower than 2 years ago, such that I wonder how they will both manage to start afresh on their own.

Some did it right some did it wrong. I watched a house sell that I put in an offer for it was just over a $1M and was pipped by like $20K, this went on to be sold again like 18 months later at the market peak, they walked away with an extra $500K.

Flipping .... heck

One on my street sold for $1.6M in May 2020, then again 13 months later in June 2021 for $2.4M - an $800k gain in a year. And it was in the exact same condition for both sales.

"One on my street sold for $1.6M in May 2020, then again 13 months later in June 2021 for $2.4M - an $800k gain in a year. And it was in the exact same condition for both sales."

What's the address of the property referred to above?

Would be interested to see the current valuation.

2 dream street

KW heads

Fantasia

Not sure why you don't believe it, want my address I have for the one that had $500K+ gain in under 18 months ?

"want my address I have for the one that had $500K+ gain in under 18 months ?"

Yes please.

Thank you in advance.

100 Oriental Parade, Papamoa Beach

Thank you.

Some numbers worth highlighting and noting

100 Oriental Parade, Tauranga - QV

1) Buyer at Dec 2021:

A) Dec 2021

i) Purchase price: $1,565,000

Mortgage 80% LVR: $ 1,252,000

Equity: $313,000

ii) Mortgage payment at 3.577%

1) interest only - $44,784

2) P&I 30 years - $68,731

B) February 2024

i) Market valuation: $1,300,000 (-16.9%)

Mortgage 80% LVR: $ 1,252,000

Equity: $48,000 (-84.7%)

ii) Mortgage payment at 7.29%

1) interest only - $91,271 (increase of 103%)

2) P&I 30 years - $103,849 (increase of 51%)

2) Buyer today (BT)

If the buyer had chosen to wait and buy at current valuation

A) Buyer at Feb 2024

i) Purchase at current market valuation: $1,300,000

Equity: $313,000 (same as equity of Dec 2021 buyer)

Mortgage: $987,000 (decrease -21% compared to Dec 2021 buyer) - LVR is 75.9%

ii) Mortgage payment at 7.29%

1) interest only - $71,952 (lower than Dec 2021 buyer by 21% or $19,319 per year)

2) P&I 30 years - $81,868 (lower than Dec 2021 buyer by 21% or $21,980 per year)

If BT saves the $21,980 additional payment that the Dec 2021 buy has to pay due to the larger mortgage and invests for 30 years at 3.9% (after tax bank deposit rate), at the end of 30 years, this will be $1,212,355 that will be available for retirement. This is money that the Dec 2021 buyer will not have.

Remember at the end of 30 years, the house price will be exactly the same for both the Dec 2021 buyer and BT.

100 oriental pde, sale 27 July 2020, $1015000

Sale December 2021, $1565000

Current Estimated value $1380000

Someone did very very well selling the peak

"Someone did very very well selling the peak "

Given the short term holding period, it is likely the seller was a property trader. Property traders are in the business activity of making profits from their buying and selling activity.

I choose to focus on the plight of owner occupier buyers (i.e end users) who are hard working and may have taken years to save their deposit (and to see it potentially evaporate in 3 years), rather than short term oriented property traders who bear the risk with those economic activities.

In effect, there was a wealth transfer from the current owner (assumed to be an owner occupier buyer) to the property trader due to the transaction and transaction price. In the Dec 2021 transaction, the current owner occupier transferred the bulk of their savings (used as a deposit) to a property trader.

This is how owner occupier buyers can become collateral damage when there is a large number of speculators in the residential property market and house prices are at extremely elevated risks. Residential dwellings (i.e basic human need of accommodation) have become objects of price speculation for speculators.

Owner occupier buyers: CAVEAT EMPTOR

Wonder if they pretended not to have bought and sold for capital gains, for tax reasons.

They must have a very understanding bank. I'm surprised they haven't called in the debt on the sellable house.

Did the first house have biggish land, if so they are better to hold for now. CB just announced plans to zone 30 years of growth with more details to follow later in the month.

The 30 years of growth is already zoned. All he's said is that council's must retain it if they want to get rid of MDRS.

I have never heard of such a thing, councils have ten year plan.

Over 30 years that is 500 to 600k homes in Auckland and 60 to 70k homes in Hamilton. If half are greenfield at a rate of 10 per hectare allowing for roads, reserves, shopping and workplaces, it is a massive amount of land. 3000 hectares in Hamilton, which is only 11000 hectares total. Hamilton population has grown by less than 3000 per year since 2001. Last year that was 6000 new residents and could double in size in 20 years

Well get reading up on Auckland's Unitary Plan, the NPS-UD, and MDRS.

NZ is Auckland and Auckland NZ. I think CB is referring to more than Auckland. Sure the AUP does allow for a lot of growth but that was written over 10 years ago

The whole of the Wellington region had to plan for 30 years growth some years ago. I think it was a planning requirement in the John Key years? Google 'future urban growth nz' and it will likely bring up lots of hits from councils who put these types of zones in place.

The MDRS applies to Tier 1 cities (Auckland, Hamilton, Wellington, Christchurch and Tauranga).

And from memory more than those 5, someone can clarify. Hamilton and Christchurch both rejected MDRS, chch was outright refusal and Hamilton adapted a wide range of exclusions.

Listening to the words of chris bishop he talked about flooding the market, though I'm sceptical whether he will achieve it. Processes take forever, then there are owners either not in a position to do anything or those large landholders who hold and hold as a nest egg knowing they will reap big gains long-term

Beanie - they would be better to bite the bullet and start over. A total financial disaster can be recovered from particularly if you are younger. It happened to me so im talking from experience. It’s amazing how things can change.

"A total financial disaster can be recovered from particularly if you are younger"

Those under the following circumstances are less likely to recover from losing a large proportion of their net worth

1) nearing or in retirement

2) low income earners

3) single income earner with children

Problem is vendors still don’t realise how extreme the cuts required will be for FHB’s to bother in a meaningful way.

They’re in the drivers seat and can wait much longer than the over leveraged crowd.

Vendors are trying to dump without realising the extent of price discovery to come…..

There is not enough borrowing capacity to settle on the houses for sale.... many are trying to downsize and release equity for other purposes... its a mess and always ends in tears. Not every seller is going to re-buy, especially investors.

💯

When cost of living is up, renters are the first to pay the price. If this trend continues, we might see 800 and even 1K for 2/3 bedies accordingly

Expect an increasing number applying for social housing.

Likely to see numbers on social housing waiting lists increase.

Isn't the current govt making things look better on the books by cutting the lists down?

And there will be extreme pressure on government to put the accommodation supplements up (raise the supplement dollar thresholds and adjust the income qualifiers).

MPs will not lack for eagerness to increase taxpayer contributions to their rental yields, that's for sure. Deeply entrenched Speculator Entitlement Mentality will ensure that, just as such entitlement has driven stone's tendency to grasp for taxpayer money at every opportunity while tut-tutting at the poor getting any.

Rats off a sinking ship.

Great time to leave being a Bank Chairman.... at the top of profitability

JK always had great timing, what made him a top trader as well as pollie

Right on que comes another flood of listings at a time of stretched affordability (restricted buyer pool). This is a precursor for the next leg of the downtrend in prices. There is a glut of overpriced homes out there and Spruikers have well and truly spun up a suckers market to protect their pride. This aside, the minority of FHB's who placed their lives on hold since the dizzy heights of 2021 have every reason to celebrate their fast growing deposits buy more house by the day. I think its looking increasingly likely house prices will continue falling well into 2025 (trusted REINZ HPI measured) on delayed impact of ever rising costs of home ownership.

Looks like its ollowing the classic housing bubble phases. Last few months have been the bull trap phase, now entering the fear stage. Final steps are the capitulation phase and then return to norm.

Do we have to have same platitudinous phrases every housing article, pure Agent can’t?

As in shed load of listings equates to more choice.

listings are at record levels precisely because buyers are scarce. People are hard up and mortgage rates for fixed deals are sucking away more disposable income. No rate cuts this year and real rates rise as inflation falls. Please get with the programme

No stats seem available on what % of existing stock of property is on sale at this time compared to 2015 or 2019. Is it possible to take the total dwellings figure for 2015 and then add all new builds since to it? The see what % you reach

"... amount of stock on the market at the end of February was the highest it has been in any month of the year since June 2015."

In 2015 NZ had population of roughly about 4.6mil and now has a population of 5.3 mil. That's 700k more people, but the housing stock available for sale is still around what it was in 2015, right? In theory, this is inflationary for house prices.

Even if many more houses will come up for sale this year reducing the ratio of 'for sale' numbers to the 'amount of people needing to buy' to the 2015 level, then house prices might still go up as they did in 2015/2016 and beyond.

One major variable that's severely out of whack this time around is that many people (especially single people) simply can't afford to pay for houses in NZ's biggest cities at current prices/interest rates.

Regardless of what will happen, I feel that house prices can't fall too far because there are too many willing buyers waiting to pick up the falls.

Only if the number of potential buyers has increased in sync with population, IMHO many immigrants have increased population but are not yet buyers...... In AKL you need about 150-200k to by as a deposit. I think the rental pool has increased much more then the buying pool, seems to me to be A LOT of homes for sale at high prices vs affordability. IMHO this always results in lower prices, I think this is why we are seeing low sales numbers... vendors are wanting too much for their house so not many paying up..... what other explaination for such low sales with so many for sale?

Next stop FONGO

The flood of "once were fishermen" from the Philippines are 25x to a house at the guys mates place, that suckered them into giving them their 15K of their entire life's savings.........THEY ARE NOT buying anywhere in NZ and will live in the kitchen cupboard, if needed....while they learn to paint the house systems of kiwistyles.

So those that pluck the "high immigration figures" to support higher house prices....are the suckers mug, just like the poor fisherman from Asia......

Yeah someone who grazes their horse at my place had a great Philipino guy as a flatmate. he asked if he could move entire family into his room, IE 2 kids and wife, inbto a 3 bd rm house with one bathroom, was told best to find a house, trust me thats 3 new NZers but no way in hell can buy, can hardly afford to rent their own place.... They are real nice and a great addition to NZ but have no money, he and wife be $28 per hour workers

Not going to help this market stay up at all....

the clowns who do not see whats going on at ground level are going to get screwed this recession, its brutal ... no lube

Am getting a Filipino production manager next month, who is paid less than the current one who is from SA. But tbh the current manager is overpaid and doesn't throw himself into the work. I end up having to clean up so am glad he's off

Done 5s?

Yes all new arrival PH (and most Asian) workers are all great people and no bones about it, they all have great work ethic and will be great new additions to NZ.

They just have no immediate resources to buy the old Kiwi dream of your own house and "some little patch" of land. Littler and littler by the day....

They may afford this after 10 to 20 years of hard graft at lower rung wages and living many people to a house .......unless housing continues to drop much further.

Good rant

true tho how can you save 150k on $28 per hour while paying a landlord?

why dont you post here how you can have a familly of 4 school fees uniforms cars etc and save $150k best estimate please of number of years, oh and property doubles every 10 years so in 10 years you will need double the deposit....?

its so not credible ...... do you not have worries about who you will sell too?

You can’t. They provide an opportunity for their kids and then hope the kids do well enough to buy. It’s a long game.

Immigration is not only failing to support house prices, I think we will see rents come back too. I have noticed around me that rental stock is lifting and know of a few houses that have been rented due to financial stress.

Utilisation of housing in NZ may finally improve.

I know that this familly can make more in Aussie and will go once they can, they have no ability to even save here, but they are really nice and the kids will do well

This is what pretty much everyone on a wage/salary should be doing. The worst outcome is you save faster in Australia and come back to buy a house here. Australia is a big life upgrade for Kiwis.

There is no poverty in Oz and everyone who wants to do well does so easily, they have spare houses for everyone

Where I live the nice lifestyle properties and executive homes are piling onto the market. I assume some of the vendors are not coping with their debt levels and general cost of living. The problem is they are not selling. Some have been on the market for two years or more.A mate who is an RE sales manager recently told me anything above$1.5m is dead in the water. At some stage one of the Banks will pull the pin and start a mortgagee sale. They don’t want to do that for obvious reasons but at some stage the accruing debt will get too high and we all know the Banks very rarely lose. They are your enemy not your friend.

It seems the banks are still being very lenient with bad debt. Which explains why your still not seeing many mortgagee sales coming up. The storey of the lady who hadn't paid anything in two years comes to mind.

The banks obviously don't want to force mortgagee sales as it drops the market and shows instability, putting their other debt at risk. The problem comes as soon as one of the large banks blinks the others will have to as well to protect their interests. No doubt there are conversations going on behind doors.

The question will be can they be lenient enough till an ill economy starts showing signs of life again... or will it be a sudden change of tune and a fire sale if things get properly bad.

I Am in the LSB band, around here the big ones are selling 2.5-3.5 mil its the small 1H ones at about 1.8-2mil that are not moving, if you are going to move rural best to get enough land that you can have a horse cows and a few sheep, if its sub-dividable people asking a lot of money...

Under CCCFA The banks had a duty to not allow you to overcommit yourself, if they test you at say 5.8% test rate and rates now 8% did they do decent testing... if found wanting they cannot collect interest and principals can be fined 250k..... In some case clearly the banks have not excercised all care and attention....

For investors the gloves are off.

Many borrowers and their lenders did not put their mind to the possibility that interest rates would rise to where they are now. The borrowers wanted a particular home and were willing to borrow big to get it. The lenders wanted to lend as much as possible to maximise their bonuses. Greed all round.

I agree that many buyers and banks "did not put their mind to the possibility..." when borrowing/lending out huge mortgages in 2021. BUT, we all forget the prevailing idea in the markets back then. From what I can remember, almost EVERYONE was talking about how we are living in the "new normal" where Covid will be here to stay for a long time and likewise - interest rates are going to be low for a long time too. People made decisions based on that prevailing idea.

The fact that interest rates went up so high and so quickly is not something that most people were forecasting, if I am not mistaken. It's always easy to 'point the finger' at someone in retrospect, but the decisions people made at the time were guided by the information they had at the time, without the benefit of the 'crystal ball'.

Some of us saw the top and sold.

Much was valued based on land alone ie 4k per sq m, but only developers would pay that in general, they got shafted at the top.

"Many borrowers and their lenders did not put their mind to the possibility that interest rates would rise to where they are now."

A question to ponder - what is going to be the unintended consequences of that?

150 comments. Nothing gets the commentators posting more than bad house price news!

It amazes me how the spruikers put a spin on everything.... be quick

Behind closed doors the banks are all shissssting bricks as to whats about to occur and become reality for many stressed borrowers.

The banks know of their own complicity in this total banking mess!!.....so the rope gets fed out.....all in the Hope of Tony A'holes forlorn hope of 10% gain this year......ITS NOT GOING TO HAPPEN TA! You cannot levitate this heavy lead anchor.

Banks know how bad it is, but are keeping mum on it.

JK leaving ANZ speak volumes. If I was in charge of a bank, during our previous "drug pusher like Debt sales" I would be out last week too.

This figure of toxic homeloans will eclipse 25,000+ households this year.

Those that need to sell, must quit the DDDEDT by April 2024.....or accept much lower when forced to do so!

Tick tock.....

"My father in law slaved 60 years building a profitable business and home only to have it sucked out of him in 5 or so years by these parasites."

I'm about to turn 40 in a few weeks and i really worry about the boomer generation and the quality of care they are going to get in homes from low paid immigrants whilst the property / care homes vultures circle.

Its going to be a brutal and hard lesson that we are all going to have to watch and learn from as they dont seem to be getting it.

It will teach us that we need to make housing / food / schooling affordable for our children so they can afford to not leave us to rot with a bunch of others in a similar situation, finally departing this earth both lonely and surrounded by people they dont know.

Completely agree. With the misallocation of capital directed at speculating on tax free capital gains called shelter/housing, nothing will change here unless that does. The concept of less tax for working offset by a universal land tax making sure local and foreign capital pay it share remains a fantasy. Everyone had a chance to vote in the land tax with TOP for the last two elections and it was resoundingly defeated both times.Unless this changes we will continue to export our children and gran-children elsewhere, and be doomed to life out your grim future

"to rot with a bunch of others in a similar situation, finally departing this earth both lonely and surrounded by people they don't know"

It'll be sad for sure, but remember who worked hard to build this society we have today.....

Perspective of realestate.co.nz

https://news.realestate.co.nz/blog/new-zealand-property-market-2024-feb…

Looks like the REAs must just spruik spriuk spruik.....Their narrative is just soo predictable.

Like Tony and Ashleys polishing the "forever turd of NZ property" since late 2021.....

Tough time for FHB still but a great time for 2nd house+ movers. We just landed our dream house we will never move again. Heaps of land, landscaped gardens land sea views, 10mins walk to the beach and decile 10 schools all the way through. A year or 2 ago this house would have been 400k more and out of our budget.

my experience at auctions the last 6 months has been that they’re a dogfight. These were all highly desirable properties that had multiple bidders outbid us.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.