The fundamental attractiveness of residential property as an investment tended to flatten out at the end of last year, after 18 months of steady improvement.

Interest.co.nz tracks the theoretical rental yields that would be achieved on the three main types of rental properties (one bedroom units, two bedroom units and three bedroom houses), nationally and in all of the main urban districts around the country each quarter.

Using lower quarter selling price data for each type of property from the Real Estate Institute of NZ and matching that with median rent data from bonds received by Tenancy Services each month, provides an indicative rental yield for each type of property in each district.

This allows us to track the relative attractiveness of the rental property market each quarter, using a standard measure based on actual market movements.

A rental yield measures a property's income earning potential relative to its purchase price, making it a fundamental indicator of the rental market.

But it is not a measure of individual cash flows, which are affected by such things as how much debt an investor takes on, movements in mortgage interest costs, vacancy rates and outgoings such as rates, insurance and maintenance.

Over the last couple of years most of the attention has been focused on the costs of owning rental property because they have been steadily increasing.

But what has often been missed is the fact that the fundamental attractiveness of residential investment property as an income producing asset has been steadily improving.

That's because property prices have been generally declining, while rents have been generally increasing.

In the first quarter (Q1) of 2022 the Real Estate Institute of New Zealand's national lower quartile selling price for three bedroom houses was $650,000, while the median rent for three bedroom houses in the same quarter was $589 a week, giving a gross yield of 4.7%.

A year later in Q1 2023, the national lower quartile price for three bedroom houses had dropped to $566,050 while the median rent for the same type of properties had increased to $620 a week, pushing the gross yield up to 5.7%.

It dropped back down to 5.6% in Q2 2023 and stayed there for the rest of year, suggesting a period of relative stability in the rental market, with prices and rents moving in tandem.

However 5.6% is not a particularly attractive gross return for investors looking for income, especially when they are facing significant increases in outgoings and uncertain prospects for capital gains.

However better returns are available on multi-unit properties such as home units.

The national yields on two bedroom units increased from 5.7% in Q1 2022 to 7.2% in Q3 2023, before dropping back to 6.8% in Q4 2023, while yields on one bedroom units rose from 6.4% in Q1 2022 to 10.4% in Q3 2023 , then dropped back to 8.7% in Q4 2023.

There are also major differences in yields depending on location.

For example, in Auckland, where property prices are extremely high relative to rents, the yields on three bedroom houses rose from a paltry 3.5% in Q1 2022 to a measly 4.4% in Q4 2023, so good luck to anyone trying to squeeze a decent income out of that.

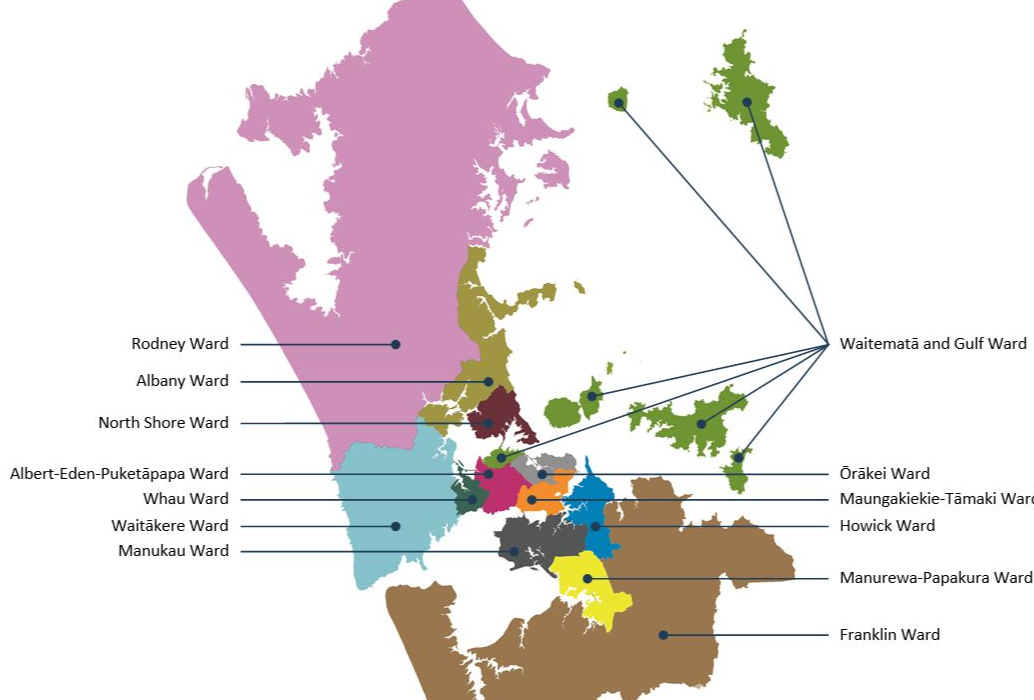

The table below shows the quarterly movements in indicative yields for the three main rental property types in all of the country's main urban districts, including each of the council wards within Auckland City.

The comment stream on this story is now closed.

| Whangarei District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 7.3% | 4.9% | 4.5% |

| Q2 2022 | 6.2% | 5.1% | 4.9% |

| Q3 2022 | 7.1% | 5.2% | 4.9% |

| Q4 2022 | 8.4% | 5.3% | 5.0% |

| Q1 2023 | 7.0% | 5.3% | 5.2% |

| Q2 2023 | 0.0% | 5.6% | 5.5% |

| Q3 2023 | 7.0% | 5.2% | 5.8% |

| Q4 2023 | 0.0% | 6.0% | 5.6% |

| Auckland Region | |||

| Separate figures for each Auckland Council ward area are at the bottom of this table | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 6.2% | 4.4% | 3.5% |

| Q2 2022 | 13.6% | 4.5% | 3.7% |

| Q3 2022 | 7.2% | 4.6% | 3.9% |

| Q4 2022 | 11.2% | 4.8% | 4.0% |

| Q1 2023 | 11.8% | 5.3% | 4.2% |

| Q2 2023 | 13.4% | 5.6% | 4.3% |

| Q3 2023 | 12.5% | 6.0% | 4.4% |

| Q4 2023 | 9.6% | 5.3% | 4.4% |

| Hamilton City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 3.6% | 4.6% | 3.8% |

| Q2 2022 | 4.5% | 4.5% | 4.0% |

| Q3 2022 | 4.8% | 4.6% | 4.3% |

| Q4 2022 | 4.0% | 4.6% | 4.5% |

| Q1 2023 | 3.2% | 4.8% | 4.5% |

| Q2 2023 | 2.9% | 5.1% | 4.7% |

| Q3 2023 | 0.0% | 5.3% | 4.7% |

| Q4 2023 | 6.5% | 5.3% | 4.7% |

| Tauranga City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 3.6% | 4.7% | 3.8% |

| Q2 2022 | 3.4% | 4.4% | 4.1% |

| Q3 2022 | 2.7% | 4.7% | 4.4% |

| Q4 2022 | 8.4% | 4.5% | 4.6% |

| Q1 2023 | 5.7% | 5.0% | 4.5% |

| Q2 2023 | 6.6% | 5.6% | 4.8% |

| Q3 2023 | 4.2% | 6.1% | 4.9% |

| Q4 2023 | 6.6% | 5.4% | 4.8% |

| Whakatane District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.2% |

| Q2 2022 | 0.0% | 0.0% | 4.2% |

| Q3 2022 | 0.0% | 0.0% | 4.5% |

| Q4 2022 | 0.0% | 0.0% | 5.2% |

| Q1 2023 | 0.0% | 0.0% | 5.3% |

| Q2 2023 | 0.0% | 4.4% | 4.9% |

| Q3 2023 | 0.0% | 0.0% | 5.2% |

| Q4 2023 | 0.0% | 0.0% | 5.1% |

| Rotorua District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 5.8% | 5.2% |

| Q2 2022 | 0.0% | 5.7% | 5.2% |

| Q3 2022 | 1.9% | 7.9% | 5.5% |

| Q4 2022 | 2.8% | 5.4% | 5.6% |

| Q1 2023 | 0.0% | 6.5% | 6.4% |

| Q2 2023 | 0.0% | 6.4% | 5.8% |

| Q3 2023 | 3.6% | 6.2% | 6.0% |

| Q4 2023 | 0.0% | 6.2% | 6.0% |

| Taupo District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 4.6% | 3.9% |

| Q2 2022 | 0.0% | 3.4% | 3.8% |

| Q3 2022 | 0.0% | 3.7% | 4.1% |

| Q4 2022 | 0.0% | 0.0% | 3.9% |

| Q1 2023 | 0.0% | 4.3% | 4.6% |

| Q2 2023 | 0.0% | 0.0% | 4.4% |

| Q3 2023 | 11.1% | 0.0% | 4.8% |

| Q4 2023 | 0.0% | 7.5% | 4.8% |

| Hastings District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 4.7% | |

| Q2 2022 | 0.0% | 5.1% | 4.7% |

| Q3 2022 | 0.0% | 0.0% | 5.0% |

| Q4 2022 | 0.0% | 5.0% | 5.2% |

| Q1 2023 | 0.0% | 5.5% | 5.5% |

| Q2 2023 | 0.0% | 5.8% | 5.2% |

| Q3 2023 | 0.0% | 4.4% | 5.7% |

| Q4 2023 | 0.0% | 0.0% | 5.5% |

| Napier City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 7.0% | 5.4% | 4.1% |

| Q2 2022 | 7.7% | 5.7% | 4.6% |

| Q3 2022 | 7.4% | 5.6% | 4.7% |

| Q4 2022 | 0.0% | 5.0% | 4.8% |

| Q1 2023 | 0.0% | 6.9% | 5.2% |

| Q2 2023 | 5.4% | 6.0% | 5.4% |

| Q3 2023 | 7.1% | 7.3% | 5.6% |

| Q4 2023 | 6.8% | 6.3% | 5.4% |

| New Plymouth District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 5.1% | 4.4% | 4.7% |

| Q2 2022 | 0.0% | 5.3% | 5.0% |

| Q3 2022 | 0.0% | 5.3% | 5.1% |

| Q4 2022 | 7.6% | 6.1% | 5.2% |

| Q1 2023 | 0.0% | 7.2% | 5.5% |

| Q2 2023 | 0.0% | 6.7% | 5.9% |

| Q3 2023 | 4.8% | 5.9% | 6.2% |

| Q4 2023 | 7.1% | 6.7% | 5.9% |

| Whanganui District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 6.8% | 4.8% | 5.2% |

| Q2 2022 | 4.8% | 5.3% | |

| Q3 2022 | 6.0% | 5.1% | 6.1% |

| Q4 2022 | 9.7% | 6.8% | 6.3% |

| Q1 2023 | 8.3% | 7.2% | 6.3% |

| Q2 2023 | 8.3% | 6.8% | 6.9% |

| Q3 2023 | 7.8% | 6.5% | |

| Q4 2023 | 6.2% | 6.8% | 7.0% |

| Palmerston North City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 4.3% | 4.6% |

| Q2 2022 | 3.0% | 4.9% | 4.9% |

| Q3 2022 | 0.0% | 5.7% | 5.3% |

| Q4 2022 | 0.0% | 6.8% | 5.3% |

| Q1 2023 | 0.0% | 6.2% | 5.7% |

| Q2 2023 | 4.3% | 5.9% | 6.0% |

| Q3 2023 | 0.0% | 6.3% | 5.5% |

| Q4 2023 | 0.0% | 6.8% | 5.8% |

| Kapiti Coast District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.0% |

| Q2 2022 | 0.0% | 0.0% | 4.4% |

| Q3 2022 | 0.0% | 0.0% | 4.4% |

| Q4 2022 | 0.0% | 4.4% | 4.4% |

| Q1 2023 | 0.0% | 0.0% | 4.8% |

| Q2 2023 | 0.0% | 4.5% | 5.0% |

| Q3 2023 | 0.0% | 5.2% | 5.5% |

| Q4 2023 | 0.0% | 5.4% | 4.9% |

| Porirua City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.3% |

| Q2 2022 | 0.0% | 3.3% | 4.8% |

| Q3 2022 | 0.0% | 4.4% | 5.4% |

| Q4 2022 | 0.0% | 0.0% | 4.9% |

| Q1 2023 | 0.0% | 0.0% | 5.0% |

| Q2 2023 | 0.0% | 0.0% | 5.3% |

| Q3 2023 | 0.0% | 0.0% | 5.1% |

| Q4 2023 | 0.0% | 0.0% | 5.6% |

| Upper Hutt City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.4% |

| Q2 2022 | 0.0% | 0.0% | 4.7% |

| Q3 2022 | 0.0% | 5.6% | 4.9% |

| Q4 2022 | 0.0% | 6.3% | 5.2% |

| Q1 2023 | 0.0% | 5.7% | 5.6% |

| Q2 2023 | 0.0% | 6.7% | 5.3% |

| Q3 2023 | 0.0% | 7.2% | 5.2% |

| Q4 2023 | 0.0% | 0.0% | 5.4% |

| Lower Hutt City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.5% | 4.5% | 4.3% |

| Q2 2022 | 5.5% | 5.3% | 4.7% |

| Q3 2022 | 7.4% | 6.2% | 5.2% |

| Q4 2022 | 10.5% | 6.4% | 5.6% |

| Q1 2023 | 6.6% | 7.1% | 5.8% |

| Q2 2023 | 6.3% | 6.2% | 5.5% |

| Q3 2023 | 7.9% | 7.7% | 5.8% |

| Q4 2023 | 7.5% | 6.8% | 5.6% |

| Wellington City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 6.3% | 5.0% | 4.1% |

| Q2 2022 | 6.2% | 5.4% | 4.3% |

| Q3 2022 | 7.1% | 6.1% | 4.6% |

| Q4 2022 | 8.4% | 5.4% | 4.8% |

| Q1 2023 | 7.8% | 6.4% | 4.9% |

| Q2 2023 | 7.9% | 6.5% | 5.1% |

| Q3 2023 | 8.4% | 6.4% | 4.9% |

| Q4 2023 | 7.4% | 6.3% | 4.7% |

| Nelson City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 6.0% | 4.4% | 4.2% |

| Q2 2022 | 6.0% | 4.6% | 4.2% |

| Q3 2022 | 6.5% | 5.9% | 4.5% |

| Q4 2022 | 6.4% | 6.2% | 4.6% |

| Q1 2023 | 4.7% | 5.7% | 4.7% |

| Q2 2023 | 4.0% | 5.0% | 4.8% |

| Q3 2023 | 3.2% | 5.8% | 4.8% |

| Q4 2023 | 4.1% | 5.6% | 4.7% |

| Marlborough District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.3% |

| Q2 2022 | 0.0% | 0.0% | 4.2% |

| Q3 2022 | 0.0% | 5.1% | 5.0% |

| Q4 2022 | 0.0% | 0.0% | 4.5% |

| Q1 2023 | 0.0% | 6.4% | 4.9% |

| Q2 2023 | 0.0% | 0.0% | 5.1% |

| Q3 2023 | 0.0% | 6.2% | 4.9% |

| Q4 2023 | 0.0% | 6.1% | 5.3% |

| Waimakariri District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.3% |

| Q2 2022 | 0.0% | 0.0% | 4.2% |

| Q3 2022 | 0.0% | 0.0% | 4.4% |

| Q4 2022 | 0.0% | 0.0% | 4.3% |

| Q1 2023 | 0.0% | 0.0% | 4.8% |

| Q2 2023 | 0.0% | 0.0% | 4.9% |

| Q3 2023 | 0.0% | 0.0% | 4.8% |

| Q4 2023 | 0.0% | 0.0% | 4.8% |

| Christchurch City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.9% | 5.4% | 4.3% |

| Q2 2022 | 6.2% | 5.7% | 4.6% |

| Q3 2022 | 5.6% | 5.5% | 4.7% |

| Q4 2022 | 5.4% | 5.8% | 4.9% |

| Q1 2023 | 5.8% | 6.4% | 5.1% |

| Q2 2023 | 5.5% | 6.3% | 5.2% |

| Q3 2023 | 5.9% | 6.6% | 5.2% |

| Q4 2023 | 6.2% | 6.0% | 5.1% |

| Selwyn District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 3.9% |

| Q2 2022 | 0.0% | 0.0% | 3.9% |

| Q3 2022 | 0.0% | 0.0% | 4.0% |

| Q4 2022 | 0.0% | 0.0% | 4.4% |

| Q1 2023 | 0.0% | 0.0% | 4.2% |

| Q2 2023 | 0.0% | 0.0% | 4.4% |

| Q3 2023 | 0.0% | 0.0% | 4.4% |

| Q4 2023 | 0.0% | 0.0% | 4.6% |

| Ashburton District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 4.7% |

| Q2 2022 | 0.0% | 0.0% | 5.0% |

| Q3 2022 | 0.0% | 0.0% | 5.3% |

| Q4 2022 | 0.0% | 0.0% | 4.8% |

| Q1 2023 | 0.0% | 0.0% | 5.0% |

| Q2 2023 | 0.0% | 6.1% | 5.3% |

| Q3 2023 | 0.0% | 7.2% | 5.8% |

| Q4 2023 | 0.0% | 0.0% | 6.1% |

| Timaru District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 6.4% | 5.1% |

| Q2 2022 | 0.0% | 6.3% | 4.8% |

| Q3 2022 | 0.0% | 5.3% | 5.2% |

| Q4 2022 | 0.0% | 6.1% | 5.6% |

| Q1 2023 | 0.0% | 6.6% | 5.4% |

| Q2 2023 | 0.0% | 6.7% | 5.2% |

| Q3 2023 | 0.0% | 5.4% | 5.4% |

| Q4 2023 | 0.0% | 5.6% | 5.8% |

| Queenstown-Lakes District | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.4% | 4.1% | 3.2% |

| Q2 2022 | 4.8% | 4.8% | 3.3% |

| Q3 2022 | 7.4% | 4.3% | 3.6% |

| Q4 2022 | 4.8% | 4.7% | 3.8% |

| Q1 2023 | 8.8% | 5.0% | 3.9% |

| Q2 2023 | 5.2% | 5.5% | 4.1% |

| Q3 2023 | 9.1% | 6.1% | 3.9% |

| Q4 2023 | 21.5% | 5.9% | 4.0% |

| Dunedin City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 5.0% | 6.4% | 4.7% |

| Q2 2022 | 4.3% | 5.6% | 4.8% |

| Q3 2022 | 4.6% | 6.0% | 5.4% |

| Q4 2022 | 4.2% | 7.4% | 5.6% |

| Q1 2023 | 5.8% | 6.6% | 5.9% |

| Q2 2023 | 5.5% | 6.0% | 5.9% |

| Q3 2023 | 4.9% | 5.0% | 5.8% |

| Q4 2023 | 5.6% | 6.1% | 5.6% |

| Invercargill City | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 8.8% | 6.1% | 5.9% |

| Q2 2022 | 11.9% | 7.0% | 6.1% |

| Q3 2022 | 8.7% | 6.8% | 6.0% |

| Q4 2022 | 0.0% | 7.3% | 6.0% |

| Q1 2023 | 0.0% | 6.4% | 6.8% |

| Q2 2023 | 0.0% | 6.2% | 6.5% |

| Q3 2023 | 9.7% | 7.4% | 6.5% |

| Q4 2023 | 0.0% | 6.7% | 6.9% |

| All of Aotearoa | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 6.4% | 5.7% | 4.7% |

| Q2 2022 | 7.8% | 5.7% | 4.9% |

| Q3 2022 | 6.9% | 6.2% | 5.2% |

| Q4 2022 | 9.7% | 6.3% | 5.3% |

| Q1 2023 | 10.2% | 6.8% | 5.7% |

| Q2 2023 | 9.8% | 7.1% | 5.6% |

| Q3 2023 | 10.4% | 7.2% | 5.6% |

| Q4 2023 | 8.7% | 6.8% | 5.6% |

| Auckland Council Ward Areas: | |||

| See map below for ward boundaries | |||

| Auckland - Rodney Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 0.0% | 3.5% |

| Q2 2022 | 0.0% | 0.0% | 3.5% |

| Q3 2022 | 0.0% | 0.0% | 3.9% |

| Q4 2022 | 0.0% | 0.0% | 3.7% |

| Q1 2023 | 0.0% | 0.0% | 3.5% |

| Q2 2023 | 0.0% | 3.4% | 4.0% |

| Q3 2023 | 2.6% | 0.0% | 3.9% |

| Q4 2023 | 0.0% | 4.0% | 4.3% |

| Auckland - Albany Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.1% | 3.4% | 3.2% |

| Q2 2022 | 4.5% | 3.6% | 3.4% |

| Q3 2022 | 3.8% | 3.8% | 3.6% |

| Q4 2022 | 4.2% | 4.3% | 3.7% |

| Q1 2023 | 5.1% | 4.5% | 3.9% |

| Q2 2023 | 6.0% | 5.0% | 3.9% |

| Q3 2023 | 4.9% | 4.8% | 4.1% |

| Q4 2023 | 4.5% | 4.8% | 4.0% |

| Auckland - North Shore Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 3.9% | 3.5% | 3.1% |

| Q2 2022 | 4.2% | 3.9% | 3.3% |

| Q3 2022 | 4.6% | 4.1% | 3.4% |

| Q4 2022 | 4.2% | 4.1% | 3.5% |

| Q1 2023 | 6.0% | 4.1% | 3.7% |

| Q2 2023 | 5.2% | 4.6% | 3.9% |

| Q3 2023 | 4.7% | 5.0% | 3.9% |

| Q3 2023 | 5.2% | 4.5% | 3.9% |

| Auckland - Waitakere Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 16.7% | 3.4% | 3.3% |

| Q2 2022 | 5.1% | 3.6% | 3.6% |

| Q3 2022 | 0.0% | 4.8% | 3.7% |

| Q4 2022 | 0.0% | 4.1% | 3.8% |

| Q1 2023 | 3.5% | 4.7% | 4.0% |

| Q2 2023 | 0.0% | 5.3% | 4.4% |

| Q3 2023 | 0.0% | 5.1% | 4.2% |

| Q4 2023 | 0.0% | 5.0% | 4.2% |

| Auckland - Waitemata and Gulf Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 9.1% | 10.6% | 2.8% |

| Q2 2022 | 26.4% | 10.0% | 2.9% |

| Q3 2022 | 16.5% | 10.4% | 2.6% |

| Q4 2022 | 24.2% | 9.9% | 2.8% |

| Q1 2023 | 19.4% | 10.5% | 2.9% |

| Q2 2023 | 25.0% | 11.0% | 3.7% |

| Q3 2023 | 21.0% | 16.0% | 3.3% |

| Q4 2023 | 14.2% | 10.6% | 3.2% |

| Auckland - Whau Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 5.3% | 4.5% | 3.2% |

| Q2 2022 | 6.5% | 4.0% | 3.3% |

| Q3 2022 | 3.3% | 4.2% | 3.5% |

| Q4 2022 | 4.6% | 4.1% | 3.7% |

| Q1 2023 | 0.0% | 5.1% | 4.0% |

| Q2 2023 | 4.5% | 5.8% | 4.0% |

| Q3 2023 | 4.8% | 5.3% | 4.2% |

| Q4 2023 | 6.5% | 5.4% | 3.9% |

| Auckland - Albert-Eden-Puketapapa Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.2% | 4.0% | 2.9% |

| Q2 2022 | 4.2% | 3.9% | 3.1% |

| Q3 2022 | 4.9% | 4.1% | 3.2% |

| Q4 2022 | 4.7% | 4.5% | 3.1% |

| Q1 2023 | 5.0% | 4.9% | 3.4% |

| Q2 2023 | 4.9% | 4.8% | 3.9% |

| Q3 2023 | 5.7% | 5.2% | 3.7% |

| Q4 2023 | 6.2% | 4.9% | 3.7% |

| Auckland - Orakei Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 5.3% | 3.4% | 2.5% |

| Q2 2022 | 4.5% | 3.5% | 2.8% |

| Q3 2022 | 6.7% | 3.6% | 2.7% |

| Q4 2022 | 6.4% | 3.8% | 3.1% |

| Q1 2023 | 7.8% | 4.4% | 3.3% |

| Q2 2023 | 5.2% | 4.0% | 3.3% |

| Q3 2023 | 6.8% | 4.6% | 3.5% |

| Q4 2023 | 6.2% | 4.5% | 3.1% |

| Auckland - Maungakiekie-Tamaki Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.1% | 5.0% | 2.9% |

| Q2 2022 | 5.2% | 4.3% | 3.3% |

| Q3 2022 | 5.5% | 3.1% | 2.3% |

| Q4 2022 | 5.5% | 4.4% | 3.6% |

| Q1 2023 | 8.4% | 4.7% | 3.8% |

| Q2 2023 | 11.0% | 4.8% | 4.0% |

| Q3 2023 | 5.4% | 5.6% | 3.9% |

| Q4 2023 | 5.8% | 5.4% | 3.8% |

| Auckland - Howick Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.6% | 4.0% | 3.0% |

| Q2 2022 | 0.0% | 3.9% | 3.4% |

| Q3 2022 | 5.3% | 4.6% | 3.2% |

| Q4 2022 | 5.1% | 4.0% | 3.4% |

| Q1 2023 | 5.0% | 4.4% | 3.5% |

| Q2 2023 | 5.6% | 4.8% | 3.6% |

| Q3 2023 | 4.9% | 5.0% | 3.7% |

| Q4 2023 | 0.0% | 4.8% | 3.6% |

| Auckland - Manukau Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 5.1% | 4.1% | 3.8% |

| Q2 2022 | 5.5% | 4.3% | 4.0% |

| Q3 2022 | 5.4% | 5.1% | 4.3% |

| Q4 2022 | 5.5% | 4.7% | 4.5% |

| Q1 2023 | 6.0% | 5.0% | 4.6% |

| Q2 2023 | 6.9% | 5.8% | 4.8% |

| Q3 2023 | 6.1% | 5.8% | 4.7% |

| Q4 2023 | 0.0% | 4.5% | 4.9% |

| Auckland-Manurewa-Papakura Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 0.0% | 3.9% | 3.8% |

| Q2 2022 | 0.0% | 4.2% | 4.1% |

| Q3 2022 | 0.0% | 4.2% | 4.2% |

| Q4 2022 | 0.0% | 4.8% | 4.5% |

| Q1 2023 | 0.0% | 4.9% | 4.8% |

| Q2 2023 | 0.0% | 5.4% | 4.6% |

| Q3 2023 | 0.0% | 5.2% | 4.8% |

| Q4 2023 | 4.9% | 5.6% | 4.8% |

| Auckland - Franklin Ward | |||

| Quarter | 1 brm unit | 2 brm unit | 3 brm house |

| Q1 2022 | 4.3% | 3.5% | 3.8% |

| Q2 2022 | 0.0% | 0.0% | 3.7% |

| Q3 2022 | 0.0% | 4.1% | 4.0% |

| Q4 2022 | 0.0% | 0.0% | 4.1% |

| Q1 2023 | 0.0% | 0.0% | 4.3% |

| Q2 2023 | 0.0% | 0.0% | 4.4% |

| Q3 2023 | 0.0% | 5.7% | 4.3% |

| Q4 2023 | 4.3% | 5.7% | 4.5% |

| Notes: Indicative yield figures are based on the Real Estate Institute of NZ's lower quartile selling price for each type of property, in each district, for each quarter. Rents are based on bonds received by Tenancy Services for each type of property in each district. Units include all multi-unit properties such as apartments and home units. Where too few properties were sold or rented in a quarter to produce a reliable figure, the yield is shown as 0.0%. | |||

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

99 Comments

good luck to anyone trying to squeeze a decent income out of that

All is well - deductibility on its way to put downward pressure on rent prices according to Mr Man.

or ease the upward pressure in rent prices.

Or make the business case for new investment in new properties make sense.

At this stage, new dollar investment in existing properties does not make sense.

Luxon's interview yesterday was mildly aggravating. Going on an on about how "they're doing this for renters". Like cmon buddy, call a spade a spade your doing this for landlords at least be honest about it rather than trying to gaslight us.

And I guess it will technically have a downwards pressure on rents but the yields are so trash anyway that even with that cost eliminated landlords are still going to be putting the pedal down when it comes to rent increases. End result is forgoing all that revenue really doesn't end up helping renters at all and probably makes a lot of stuff worse indirectly.

"Going on an on about how "they're doing this for renters""

Political spin to make them appear they're helping.

I feel like they could at least try to come up with some better spin. It's so blatantly transparent that it's almost insulting.

I really feel like they could of just kept deductibility at 50 percent or something. I honestly think 100 percent is probably a bit much but having it at 50 percent evens out the advantage between FHB's and investors, as well as keeping the incentive to buy or build new property compared to just up buying existing stock. End of the day only building new housing stock is actually going to help the situation, which the rules were actually helping to incentivise to a degree.

Agree with the 50% or 60%. Similar to thin capitalisation rules for offshore investors. Should stop cross securitisation with non-investment property too. That way the deductable costs is a true cost. Unlike now where people load their mortgage on to the investment property.

True, one should resist so blatantly lying to the public when one has made political hay in the past from advertising one's Christianity. They know this is not for the renters.

I disagree. The non deductibility rule was just unprincipled. Or, to put it another way, if residential investors have an 'advantage' because they can expense costs that owner-occupiers can't, why stop at interest? Why not do the same for rates, insurances, maintenance expenses, etc.

As the policy was being phased in, we're at the point where it's effectiveness can be evaluated. Sure, it was very effective at fleecing investors with what was a surtax (a tax on expenditure), but has it helped FHBs very much, or even at all? I'd argue there are a host of factors that have contributed to a decline in property values that are unrelated to this.

There's another consideration - fairness. Ppl who don't have investment properties (i.e. haven't taken that particular risk with their available capital) might be tempted to shrug off the fairness of a surtax because it doesn't affect them. They might even be pleased to see their friends and neighbours having to pay more tax. But when a discriminatory policy like this is successfully applied once, it can be tempting for a future government to do it again and next time it might be you that feels the effect.

In the interview Luxon said he isn't changing his tenants rent as he isn't personally affected by this change because he is mortgage free. By that statement he shows that the market forces that are supposed to lower rents are fairly non-existent, and this money is not really going to help renters at all. As if anyone really believed that anyway.

The part where he laughed at the thought that a renter could ever buy their own house was pretty telling about how he sees certain classes of people, and where they belong.

I had to laugh when he inferred houses dissappear when a landlord sells one though.

The houses just cease to exist if a landlord decides to sell, this is a known fact.

It doubles down on the idea that property investors should be allowed to leverage to the moon and pass on all the costs, no risk. If I take out a million dollar loan, I should not be held accountable for repayment.

In real business, if your loans are not performing, you're out. Plus you're on commercial rates. Landlording is not even close to running a business in this respect.

To be fair though, the banks determine what interest rate they charge to landlords based on risk. Say we banned resi mortgages for rentals the banks would probably just create Landlord Business Loans at the same rates.

But I agree, to call Landlords "businesses" is a very big stretch and an insult to true businesses. How many businesses can lock in a single client for a guaranteed fixed income for 12 months, without having to worry about nearly as many of the challenges or overheads other small businesses deal with?

With you last paragraph, how is it different to many business? Some businesses have income contracts for 12 months. Landlords have to deal with expenses, currently increasing at a higher average rate than most businesses expenses (rates, insurance, interest, repairs), then they have to deal with the renters. If they're larger they'd probably have employees too.

Agreed. Don't forget extra weeks covid sick leave, and another public holiday, minimum wage increases, implied responsibility for staff arriving with mental health and drug problems, and staff requiring non performance pay increases as they get crushed by inflation everything. Don't forget the landlording class ramming in maximum rent increases every chance they get.

So yeah...business owners have their own issues.

I highly doubt you'd find a landlord with employees, unless you're talking about a service tenancy. Do you think rates, insurance and repairs are rising much slower for other businesses???? What about:

Wages, Paye, company tax, GST, commercial rent, commercial rates, commercial lending rates, employees with leave entitlements, loss/theft/shrinkage of inventory, electricity bills, health and safety compliance costs (fire alarm testing/extinguishers/PPE), a restaurant's kitchen needs to comply with the food act/council food grade. Could probably go on.

Not to mention an effectively guaranteed revenue from continued immigration, limited housing stock and the fact that rent comes out before any other discretionary expenses I think you'll find Landlords, despite many being absolutely oblivious to it, are in a very privileged position to call themselves a "business" and enjoy the tax advantages many other businesses actually need to survive.

Not to mention, small business owner with income ~$100k. What's their capacity for a business loan? $1,000,000? Absolutely no way. Meanwhile "yea I reckon we can get $650p.w. rent for this sheethole", banks everywhere: 🤤

NZ has many small businesses that aren't manufacturers or have to comply with food regs. How about comparing landlords to a one man operation providing, say, services, such as insurance, financial services, legal services. Also, landlords don't have a guaranteed income, and if the renter vacates, they may struggle to fill the vacancy.

Can that one man band leverage their insurance, financial services, legal services operation to the eyeballs, negatively geared? Can the buyer of said operation do the same?

Landlords can, but not all do, and if they do they're taking a business risk with interest rates possibly increasing, and their not being able to increase rent, as, I've read on here, rents are determined by what a renter can afford to pay. Disclosure, I do not own a rental property, just arguing for the fun of it.

A one man operation providing insurance, financial or legal services is highly discretionary, particularly when there are much bigger companies out there. They'll still often need to pay for regular marketing and compete with bigger players for market share. Unlike Landlording, their customers won't necessarily need to hunt around for an available broker and compete with other clients for that service.

What you're also forgetting is these one man operations are their primary job, so 8 hours a day to actually derive a profit so they can live. Not pretending to be a business by letting a house sit there with someone else living in it, while spending 8 hours a day elsewhere making a living.

How much capital gain will a regional broker from Mike Pero make when they "sell"?

I provide a service, as I described in my last post and run it through a company. I don't have any marketing or advertising costs. Landlording isn't as you describe above, it can take alot of time and effort. Your simplification is naive. Capital gain? Not if you started landlording in the last few years.

A lot of time and effort landlording? What are some examples? 8 - 10 hours per week of paperwork per property? 4 hours per week fixing plumbing issues? Sounds plausible, genuinely curious. I have relatives that are landlords, it's certainly not a lot of time and effort according to them but maybe they're the exception to the rule?

Sounds like the usual hyperbole that gets trotted out. Renting out property is hard work, a social service, we're mom and pop, but we're a business too, people would be homeless if our name wasn't on the title...previous governments told us to buy property to prepare for our retirement .etc

I said it can be a lot of time and effort, and have experienced it personally. I don't think you saying, you have relatives, gives me much confidence in your knowledge of this area. At the moment, alot of landlord's "businesses" are loss making, so any time and effort isn't generating at return. That's the "business" risk they took. Your full of generalisations and one box fits all. You're the same with your comments on boomers / retirees.

Anything can be a lot of time and effort if you make poor choices. Putting on socks can be a lot of time and effort, if I chose to do so while simultaneously riding a bike.

A lot of time and effort is probably because you bought a dump of a rental or you made poor tenant selection choices, doesn't inherently make owning a house to rent out a laborious venture. But here you are, taking your bad experience and making a generalization.. and to bolster your weak argument bringing up my past comments around non-means tested super. Must have struck a nerve with you 2-fold, I can guess your demographic.

Your guessing and making generalisations, have I wound you up? Struck a nerve?

Not at all. I think it's evident I've struck a nerve with you, hence you've continually challenged my comments and brought up my other comments about "Boomers / retirees" that are irrelevant to this article. In both cases it's clear I've offended you, which is why my guesses can be made with a reasonable amount of confidence.

Your confidence is ill-placed

Alright Norm. Don't fret to what us Millennials have to say. Just enjoy your twilight years, there's not many left. We'll take the reigns and clean up the mess you've left us.

I have good genes, grand parents and parents all lived into their 90's, two hit 99, one's still going strong, I'll enjoy watching the millennials fix everything for me. What party is it your going to vote for to do that? You'll have the same problem we had. No party prepared to bite the bullet and make some difficult unpalatable decisions. Good luck with that. And stop with the personal attacks and demeaning comments, your better than that.

My great grandmother on my mother's side lived to 104 so maybe we're related somewhere along the line.

Do you think maybe these political decisions were "unpalatable" because self interest got in the way? Our generation will have the benefit of "Boomer hindsight" to not make the same selfish and foolish mistakes as before.

As for my comments, they're barely personal. Yeah they might be sarcastic and demeaning but that's just how I roll. Grow a thick skin it's the internet.

Boomer hindsight, haha, good luck with that. I think the unpalatable decisions aren't made because the party that makes them won't get voted in next time, so self interest, yes. Nothings changed, no party had the balls back in the day, and none have it now. It makes no sense to not raise the super age, and not means test it. If National weren't in bed with NZ First, raising hhe super age might have been on the table, with cross party support from Labour, so again self interest has got in the way. Thick skin, your comments don't bother me, I've enjoyed the exchange. That's what this site is all about, different viewpoints and robust, healthy discussion.

But It's okay Norm, I don't hate you/Boomers/Landlords personally. I'm a net tax payer that doesn't like seeing a ton of tax payer funds going towards bludgers when there's so much that needs fixing. That includes those on the dole, but it's such a lazy group to target when there are much bigger drains on the tax payer purse. Subsidizing landlords indirectly through accommodation supplements, giving them tax breaks for their frivolous borrowing decisions and handing out super to people who don't need it are the the big ones for me.

Call it jealousy if it makes you feel better.

Care to explain the time and effort required in being a landlord? Do you simply mean looking for a tenant and maintaining a property? For one house, that isn't much work. So long as your house isn't a dump, and your rent is reasonable. Landlords always talk about getting passive income as the goal. Passive means you aren't working for it.

I can understand it causing stress around the financial costs and risks, but you don't get rewards without taking risk and you know what your signing up for there.

Looking for new tenants when there is a vacancy, lodging bonds, property inspections, paying bills, chasing rent arrears, gst returns, annual finances to accountant, organizing repairs, bringing the property up to healthy homes standard. Much of this is normal "business" stuff. Alot incurs cost as well. In addition, personally, I had a one off incident with damage to a fence, cross leased property, had to organise two other owners, three insurance companies as the other owners did like each other, almost ended up in court. Sold the place soon after as too much work and hassle.

None of those are overly regular. I mean, looking for new tenants? You're not hiking 3 days in a bush, you put a TradeMe listing up and wait. How long does it take to lodge a bond? Property inspections are what, an hour every 3 months? Chasing rent arrears, how time consuming is it to send an email/text/make a phone call? GST returns/annual finances is once a year. A couple of hours tops.

So much hyperbole. Worst case scenario 10 hours a year on $30k revenue? What's the hourly wage on that? Whether you make a profit or not depends on how frivolous you were with borrowing instead of saving for a bigger deposit.

I was answering a question honestly, not asked by you. 10 hours per year on $30k revenue? Where did you dream up that? You can minimise any occupation like you have. If you told me your occupation I could be equally demeaning. I actually enjoy many of your comments, on matters other than housing and the non means tested super, but my estimation of you has reduced after this exchange.

If you must, I am an Estimator/Quantity Surveyor in Civil Infrastructure. So go for it. Thankfully I don't seek validation from anyone on Interest.co otherwise you might have hurt my feelings..

I throw my opinion/ideas out there and can often be quite provocative. I wouldn't say I intentionally bait confrontation, you could say my use of sarcasm is a very low form of wit, but there's nothing wrong with a little bit of confrontational debate between a couple of anonymous monikers. If you're offended then my sincerest apologies and I'd suggest scrolling past in future.

As I said above, I've enjoyed the exchange, I won't scroll on. I'm pretty sure our paths will cross again, and look forward to that.

Interesting to see you're no longer arguing much said in your first comment.

Residential investors are simply small business like any other. They manage their income and outgoings, just as any other and if outgoings outstrip their income, they either have to top it up from savings or other income or go broke, again, just like any other business. The ability have fixed term tenancies doesn't change this reality. A tenant can sign up to such a tenancy and then, sometimes, they fall behind in their rent. It can be difficult to recover from this.

BTW, it's very common for commercial leases to have much longer terms.

I found the interview a struggle to get through on both sides, but the failure to address the $800m loss in revenue, added to the $740m (~?) loss in FBB revenue, increasing social welfare spend. We're about a hundred days into the "right track" and both metrics are heading in the wrong direction for the foreseeable future according to their own KPI. Next will be the release of the tax cut, an additional but accounted for cut to revenue. The vehicle registration double dipping won't be the last "clever" accounting trick.

The idea the the "insane" policy just allowed costs to be passed on to renters. In what world would any business survive by leveraging infinitely and just passing those costs on willy nilly? We can see businesses struggling with the costs now as they are unable to pass those costs on, where is the relief for them? Where is the aid in costs for farmers who simply cannot just pass on the cost to an infinite buyers market.

The justification was to grow the economy. By allowing tax relief for investors. Who operate in an already heavily subsidised market. We're not growing the economy, we want to expand the balance sheet without all the hoo hah about actually being productive. Rort.

Let's cut benefits because we can't afford them, but not my benefit.

Let's aim to reduce rental costs, but not my rental costs.

Absolutely. They rant about poor bludgers but are all too ready to carry bludgers via property speculation. Deeply entrenched entitlement mentality that continues to negatively impact society.

As you seem to be willing to accept 'indirect' effects of a policy, then it does make a difference. LLs are facing huge cost pressures, rates in the main centres look to rise by around 18%. Insurances have been increasing at around 25% for a couple of years, at least. The non deductibility of interest became a tax on expenses, not income and all these items involve cash outgoings that LLs pass on to their tenants. I can't speak for others, but in my case, I started adding what was, in effect, a surtax, to my annual rent reviews when Labour's policy was introduced (in addition to the aforementioned rates and insurance increases). I had intended to ramp it up year-on-year, as the non-deductibility ratios increased. But I stopped doing this last year when it became clear that Labour wasn't going to win the election. (Which is just as well for my tenants because just covering the rise in rates and insurances last year came to around $30 p/w per property). You're right that yields aren't flash, but that's largely due to property values chnaging over time.

The 'downward pressure effect' on rents occurs in another way; the biggest influencer for rent levels is competition. The more rental properties there are, the better for tenants, it gives them more choice and forces LLs to compete with each other. This policy may see more investors return, in which case there will be more competition. There's no denying that Labour's (frequent) changes to the RTA saw a big drop in availability of rentals and contributed to rising rents. National has a lot more work to do to undo those changes and restore investors' confidence.

Sigh, its almost like nobody here has ever studied economics. Restoring interest deductibility WILL lower rents, just not in the way people with no economic understanding thinks it will happen. Rents on existing tenancies wont go down. However by restoring interest deductibility on older properties, investors will be back buying older units and houses instead of building brand new ones. Older units and houses rent for LESS than brand new properties. Therefore, renters will have a greater choice of much cheaper properties and will not be forced to pay 25%-50% more for a brand new one. The increased supply of rental properties will also put pressure on those new build rents, and rents will reduce as they compete with older properties for tenants. Thus rents "go down".

Replacing cheap older units and houses, with brand new units and houses is what has caused the explosion in the public housing waitlist - as low income tenants are simply priced out of the rental market which is now full of brand new townhouses while the supply of older units has dried up. So there should be a corresponding drop in the amount taxpayers are paying for emergency and social housing as low income tenants find more places to rent that they can afford. This saves taxpayer dollars.

In addition, FHB looking to build a new house will also benefit. The price of new builds will drop as FHB will no longer have to compete with investors for new builds, and the premium for interest deductibility (which is of zero benefit to a FHB) will be removed from the price of a new build. Ergo, FHB will also get cheaper houses.

Ahh yep, back to the old "buying existing houses increases the supply of houses" trick.

It changes the makeup of the rental housing stock - reweighting it towards cheaper housing and away from more expensive housing. How hard is it to get this concept?

Which creates artificial competition in the existing housing stock. If new builds are too expensive for property investors, then how are we arguing that this is a great entry point for FHB into home ownership.

We have tax incentives and subsidies which directly benefit a market segment in order to create artificial demand and higher rent. It does not matter the makeup, entire generations are being shut out. This is Victorian era class warfare stuff.

It's not hard to see the damage of these kind of policies, and claiming investing in an asset is a business. Imagine the uproar if the accommodation supplement was instead directed at bitcoinz? Dollar demand for rental properties would plummet and investors would bail, dropping the cost of housing and allowing young people the same opportunity to own that was given to many previous generations. The existing housing stock would not go anywhere, and there would be more money available for maintenance and rates due to not paying economic rent.

And aside from all of that, rent prices in real terms have dropped since Labour brought in these policies. Rent is lagging behind general CPI and wage inflation. So we can ecomonics as much as we like, in the real world things are diffrunt.

Because FHB are not buying for a return on investment, but to provide them with a home. They are not buying for best value for money, but for best forever family home, with a mortgage that they will pay off over the next 30 years regardless of any capital gain expectations. As as I pointed out, currently there is an interest deductibility premium built into the price of new builds that benefits investors but is worthless for FHB (even though they still have to pay it), so removal of that makes new housing less expensive.

there is an interest deductibility premium built into the price of new builds that benefits investors but is worthless for FHB

Is this premium still built into the price after a new built (along with its rows and rows of buddies) has been on the market for months on end and with no end in sight? Is the premium still built in after the price has been reduced once, two, three.. times?

You started all this bollocks with the words: "Sigh, its almost like nobody here has ever studied economics."

Pro tip: Read up on the law of supply and demand. You'd find it in Economics 101 and it could help prevent some future drivelous, egg-on-face posts.

Shouldn't investors be the ones increasing the housing stock, considering they're providing such a valuable service to the community? Why should they be able to outcompete FHBs on existing houses? Your argument makes no sense to me - not from a point of benefitting society and FHBs, anyway. Sure, your argument would benefit landlords, of course.

Why not? Whats wrong with FHB buying the nice new houses that they plan to live in for the next 20 years, while investors buy the less nice older properties to rent to people who only plan to stay there temporarily? Most FHB dont want to live in old houses that need work done on them, while investors are forced by law to spend money to do the houses up to the HHS standards, thus improving the quality of the rental stock over time.

Secondly, the proliferation of tiny 2 bedroom townhouses are not FHB material - you cant raise children in them, or even have a dog. So why are we incentivising the build of inappropriate homes, that only serve to benefit higher income renters at the expense of low income renters? Also this policy means the pool of family homes available to cater for population growth is stagnating or declining (as family homes are torn down to be replaced by half a dozen tiny townhouses) which puts pressure on the prices of those family homes, making housing more expensive for everyone. We should be building more family homes that will last 100 years, not townhouses for high income renters.

I have so many issues with your post that I'm not even sure where to start. I should just let this one go and not waste any more of my time, yet..

Whats wrong with FHB buying the nice new houses that they plan to live in for the next 20 years, while investors buy the less nice older properties to rent to people who only plan to stay there temporarily?

Aren't FHB supposed to buy the cheapest possible houses just so they can get on the 'ladder'? You know, those houses in seedy, dodgy suburbs, miles away from any schools? Since when can they even think of buying a 'nice' house, let alone afford one? Then, once they have equity, they're supposed to move to the 'next rung'..?

As for renters staying only temporarily? Aren't landlords (and Luxon) always going on about the fact that many if not most renters will never be able to buy? So why would those renters stay temporarily? Oh wait, because the landlord is going to hike rent to where they can't afford or kick them out for putting up a painting in the lounge?

Most FHB dont want to live in old houses that need work done on them

Do you have a source for this? Or is this your opinion as someone who is clearly not a FHB? For many FHBs, home ownership is but a dream and they'd be happy to live in any old house that needs work done rather than their current crap, rotten rental.

the proliferation of tiny 2 bedroom townhouses are not FHB material

Yet, you're the one saying FHBs are supposed to buy all those nice new homes? Now you're talking about the proliferation of new homes that are not suitable for FHBs?

So why are we incentivising the build of inappropriate homes, that only serve to benefit higher income renters at the expense of low income renters?

Just remind me, please, how are we incentivising the build of inappropriate homes? By 'encouraging' landlords to buy new homes? How do you figure this?

Face it, the bottom line is that new homes are expensive, more expensive than old ones. And they should obviously be more expensive than new homes. You wouldn't pay more for a second-hand car or a second-hand anything than for a new one, would you? So why should new houses be more affordable than old ones? And if old ones are or were the more affordable option, then why should we give landlords a leg-up in terms of competing for those with FHBs? Surely landlords should be 'encouraged' to increase the housing stock and the supply of new homes, rather than just buying up all the existing houses from under NZders?

But wait! I've seen how landlords complain about new builds, how they won't have good capital gains due to new builds being tiny sh!tboxes on post-stamp-sized plots. And how they'd much rather buy old houses that will most likely appreciate more in 'value' (as in price)..

It makes sense that NZ is seeing the biggest wave of outward migration of its young generation ever. Until the current boomer generation is lying in residential care (having their diapers changed by immigrants from 3rd world countries) nothing is likely to change, as older generations and NACT seem determined to not even throw FHBs any crumbs.

For many FHBs, home ownership is but a dream and they'd be happy to live in any old house that needs work done rather than their current crap, rotten rental.

Landlords claim FHB don't want a house that needs work to deflect any heat they get from displacing FHB from the property market. It's ironic when those FHB end up renting these houses from landlords, where the biggest improvement is painting over dead flies on the window sill.

Thanks for taking the time to draft this. It is fantastic and can be cut and pasted in the future.

The idea that the tax cuts for landlords are for the benefit of renters is hilarious.

Labour's policies were having exactly the desired effect, more housing supply, restricting capital gains speculation and bringing land prices down. All of which help renters. Worse National leader in living memory.

Here's an idea, why don't tenants get to claim back the interest deductibility instead of their landlords? Much simpler and less paperwork for the landlords and this way they definitely get the savings.

Bit like making sure you tip the wait staff directly rather than adding it to the bill at the EFTPOS machine (which goes straight to the business owner).

Sheer brilliance, Agnostium. You have my vote for PM!

Proposing this would be a good test of Luxon and Seymour's honesty levels.

You are massively overstating the impact of this policy. Yes it will have a slight downwards pressure on rents. But nowhere near the extent that you have stated. Look at Australia for example, they have turbocharged interest deductibility that can cross income streams, and guess what, their rents are both higher and have increased at a faster rate than rents have here.

The primary driver of rental prices is demand and the ability to pay. Subsidising landlords to lower rents is a fools errand and will have very little effect due to the fact that the fundamentals are so cooked anyway that the upwards pressure on rents is still enormous.

will not be forced to pay 25%-50%

Do you have any data to back this up as I have never seen an older property being that much cheaper to rent. FHB's are likely fine with older housing as well, and more willing to put the time and effort in to make them comfortable places to live compared to landlords who are looking at it through a more commercial lens where they are wanting a return rather than a comfortable home.

A 1970's 2 bedroom unit in my area rents for $450 a week, while a brand new 2 bedroom townhouse rents for $560 a week. Thats a 25% difference. Brand new 3 bedroom houses in my area rent for a lot more as no one is building cheap ones, the only people building new are building million dollar houses and they are not for rent. So the choice is an older house in the city, or a brand new house out in the subdivision sticks.

So a sample size of two and nowhere near your claimed 50%?

"investors will be back buying older units and houses instead of building brand new ones"

Would you buy under current conditions with interest deductibility restored? Does buying and renting out to tenants in the long term rental market make economic sense with current conditions and interest deductibility restored?

Would income oriented, cashflow oriented investors buy at current rental yields vs current mortgage interest rates? Having previously been a supplier of accommodation in the long term rental market, the numbers don't work in Auckland for cashflow oriented buy and hold investors in the long term rental market. It may work for someone buying existing and doing a conversion, or a development but most part time investors don't want to get into that game, only property developers, property specialists.

Given the negative cashflow on most properties in the long term rental market, the investors buying today are going to be capital gain oriented. Capital gain expectations may have fallen from the mantra of house prices double every 10 years.

Given the current conditions, numbers and negative cashflow in Auckland, it is difficult to see a sufficient number of property investors buying and supplying a sufficient number in the long term rental accommodation market and bring rental prices down.

Given the yields for Auckland above, for a 100% equity financed buyer, it is makes more financial sense to put the money on time deposit at 6.0%.

Great article Greg, thanks

Apart from some regional areas, rental yields are cashflow negative in most areas, especially when considering outgoings such as rates, insurance and maintenance. This is only likely to improve, when interest rates drop.

It's grasping at straws a little to assume lower interest rates alone will save the day.

Interested to know what the market rates would need to be to make all these figures stack up, and how long they would need to stay there, and how we could manage to keep them there, pouring money on the economic fire while productivity is in the trash and resources to produce more in this country are fairly limited.

The obvious metric out of all of this is lower prices. The promise of future income to repay even current debts are looking fairly bleak at the moment, it would take a major global shift to change that outlook.

"Interested to know what the market rates would need to be to make all these figures stack up"

It's not just the interest rates, it's going to be a combination of lower rates, lower house prices and higher rents, which will, at one point make the cashflow equation positive again.

yay you will all be able to sell at todays prices once rates get back to 2.5%

Until then lets pretend you don't want to sell anyway, if you need to sell you are going to have a nasty experience with the reality of the new investor buyer. I guess you know this as you are not buying more here.

Do what a trader would do and shift your property portfolio into the LONG book, ie hold to mortgage maturity....

Why the anger IT? (btw, I don't own any rentals in NZ any more)

People are allowed to be frustrated with the situation successive governments (and voters to extent) have, and continue to put us in.

When compared to relative risk free TD yields, these yields are extremely poor. Now that short term or "guaranteed" capital gains have had to be removed from the equation and fixed costs such as Council rates and insurance piling on, it very much exposes this form of investment (from a wannabe Landlords perspective) to the light of day.

On a positive front for FHB's, more downside of house prices ahead.

How many landlords over the last 5 or so years have had money to chuck in TDs? Sure there'll be some, but suspect many just topped up their owner occupied mortgage with a deposit for a rental property and borrowed the rest. TDs are not really an option for them unless they can lock in a rate higher than their mortgage.

When rates where 2% many older NZers purchased property for a decent cash flow with low to no debt.... still got the same cashflow..... but more risk now to get the capital back. Some may sell to transfer to TD....

truth is, the remove of the interest deductablity affects nothing on rentals with no mortgage or little mortgages, but it affects all the wanna be landlords, who are usually younger people.

and yes, the rent returns are extremely low if looking at it as a business. even a 6% gross return sucks, as one must deduct insurance, rates, maintenance, possibly 6% -7% agent fees, interests etc. then return rate before tax is only 3%-4% if you are lucky with no mortgage on it. in comparison, one year TD rate is 6%, a 2% higher than rent returns.

It's way too low, for the hassle one takes. on top of that, landlords will be seen greedy money hungry monsters, what's the point.

Correct the current crop, at current prices, are the bag holders, they cannot get out now even if they want.

It's too late in an auditorium to look for the exit once you smell the smoke, only to find its locked once you get there.

Love you long time bag holders - https://www.nzherald.co.nz/nz/ray-white-real-estate-agent-linh-yee-warn…

"they cannot get out now even if they want."

They can get out if they want. Time constrained, cashflow constrained vendors can get out at a lower price. There are bids at lower price levels.

What you mean at a loss ?

https://www.interest.co.nz/property/126256/quarter-all-apartment-sales-…

"You can't lose money buying residential property" is something that's often heard from property spruikers, but losing money is exactly what happened to 10% of the people who sold Auckland residential properties in the fourth quarter of last year.

According to property data company CoreLogic's latest Pain and Gain Report, 10% of the Auckland residential properties that sold in the fourth quarter of 2023 were sold for less than their purchase price.

Around the main centres the percentage of properties selling at a loss ranged from 3.5% in Christchurch to 10.0% in Auckland.

Outside of the main centres, the area where properties were most likely to be sold at a loss was Carterton where 18.2% of sales were made at a loss in the fourth quarter (Q4), while Timaru had the lowest percentage of loss-making sales at 0.7%.

Nationally 6.7% of sales were made at a loss in Q4 2023.

Whoever believes in "You can't lose money in ......... (whatever)" is a fool.

So I guess most of the population are fools.

The average person is not very smart compared with the top 10%, by definition 50% are even thicker than that person.

Still better to be lucky then smart aye....

Some make their own luck.

"So I guess most of the population are fools. "

This is what some commentators on interest.co.nz were saying at the peak. They may or may not have vested interests.

Names omitted intentionally (but these commenters are still active on interest.co.nz. One of the commenters made comments on this very article)

a) 9th Nov 21, 2:38pm

"I have always looked at this from the opposing direction - the risk in not owning a property? If you do not own a property you are short, not even square, but short"

b) 9th Nov 21, 5:52pm

"Or maybe right the opposite, don't hesitate, be brave and go for it, you'll be fine"

c) 23rd Nov 21, 8:52am

"It makes absolutely no sense for a couple like this to bank a capital gain now rather than wait two years and avoid 90k in taxes. The market is not going to crash 10% in the next two years."

d) 9th Nov 21, 2:38pm

"locally, I can not see anything in the near future that would decrease these current values."

e) 14th Oct 21, 11:25am

"Shrewd investors will capitalise on perceived price weakness - cementing their position for the next market upswing. Well located property remains a prime investment for the long term. (But you already know that.)"

If these commenters did not have any vested financial self interest, then they didn't know what they didn't know. They didn't know about the extremely elevated house price risks.

But you already know that.

This one in particular is Taking The Piss.

"So I guess most of the population are fools"

You said it, HM.

They can get out if they want....just not at the ponzi price expectation. Plenty of buyers at price based on the non speculative economy.

The reality is there are far better returns to be made in other businesses. I guess the difference with property is everyone in this country seems to think they understand it, banks were/are happy to throw the kitchen sink at it, and many would be incapable of running a non property business. There's also the perceived zero risk in property.

Sluggy - Real estate is the only highly leveraged investment available for most in NZ, hence most where donkey deep at the top, and are still in it. The Facebook groups are no longer unicorns and rainbows.

The spruikers played them like a fiddle, selling a leveraged retirement cashflow for nothing down but the equity in their current property....

"The Facebook groups are no longer unicorns and rainbows."

Several years ago the moderators of one particular group would remove any comments about the elevated house price risks so that the audience didn't see them. It became an echo chamber filled with confirmation bias.

Clearly they have given up as so many posts now about how they are sick of subsidising people to live in their houses.....

Suck it up princess thats negative cashflow

If they're sick of subsidizing people to live in their houses they should give them notice and leave the property empty. One less property in the rental pool etc..

Oh my bad that's just the idle threat they rolled out when healthy homes legislation was announced.

Someone used to post a great chart of NZs house price crash over time relative to other countries, can they post current chart post bull trap

Multi 1 bdrm and 2 bdrm units on a single title is the way to go. There are still plenty of cash flow positive properties out there for those willing to give more than a peripheral glance at listings.

The safer the investment the lower the yield and it shows here. Even accounting for the high captital gains in NZ (~7% year) it's still a poor performance in the spectrum of investments.

Ok - houses are currently deep in negative yield. Must be safe as... houses 😎

Start talking net yields, with no capital gains except to cover inflation, then we can have a conversation about yields and pricing.

The spruikers stoped talking net yield around 2013 when the numbers stoped adding up... its all about the double every 10 years and how much money you are going to have in retirement now days....

Things like discussing net yields and hurdle investment rates, risk free returns etc etc are not welcome in this club.

Spooky Spruikers must be very nervous now their Chief Deity is using the MUNTED word

Soon after MUNTED comes CAPITULATION

Yes, it is strange for a business to work in gross rather than net, like commercial.

More interested in selling the sizzle rather than the sausage.

Rents cannot come down in an environment where everything else (food, goods, petrol, rates, insurances and labour) is becoming more expensive! Again, rents will not come down but will be stable or increase at a slower rate from March 2025 onwards, once interest deductibility will return to 100%.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.