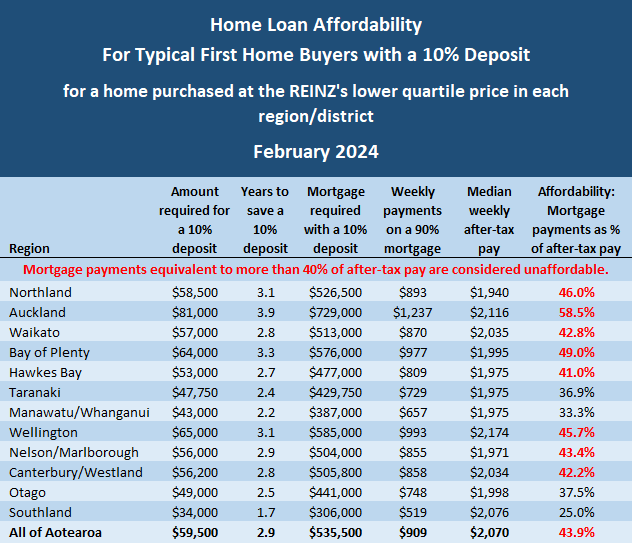

Home ownership is likely now out of reach for typical first home buyers in most parts of New Zealand unless they have a 20% deposit.

The latest affordability analysis by interest.co.nz shows Rotorua, Whanganui, Timaru and Invercargill are now the only urban centres in NZ where it would still be affordable for typical first home buyers on average wages to buy a home with a 10% deposit.

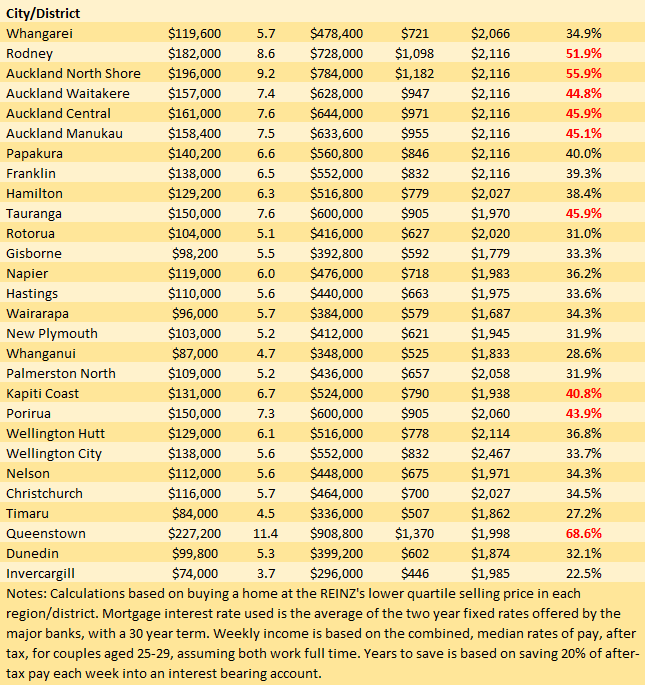

In all other areas the mortgage payments they would have to make if they purchased a home at the lower quartile price for that district with a 10% deposit, would eat up more than 40% of their after-tax pay, the threshold at which mortgage payments are considered unaffordable.

In Auckland, the country's most populous region, mortgage payments on a lower quartile-priced home purchased with a 10% deposit would devour a whopping 58.5% of the after-tax pay for a typical first home buying couple.

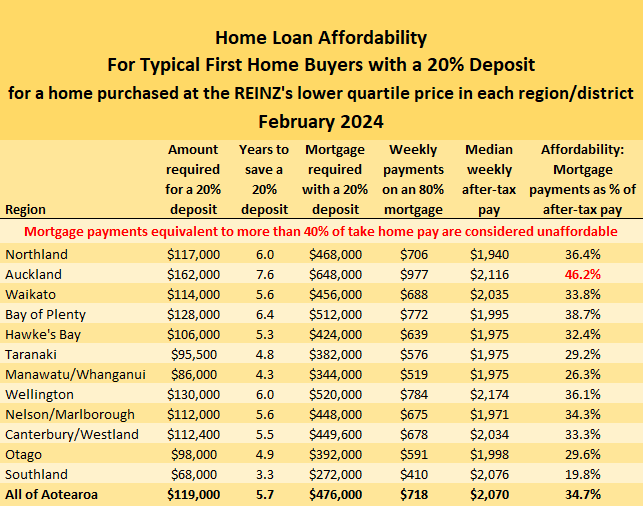

Affordability improves markedly for those first home buyers who can scrape together a 20% deposit.

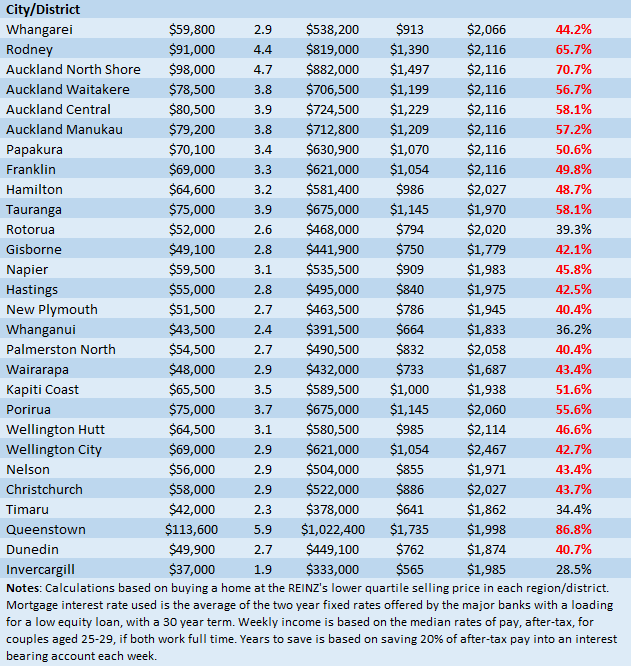

Auckland, Tauranga, Kapiti Coast, Porirua and Queenstown are the only urban centres that remain unaffordable for typical first home buyers even if they have a 20% deposit.

Within the Auckland Region, Rodney, North Shore, Waitakere, the central suburbs and Manukau would all be out of reach for typical first home buyers on average incomes, even if they had a 20% deposit.

Papakura would be marginal, with mortgage payments there eating up exactly 40% of average after-tax pay. So even a slight deterioration in affordability there would push it into unaffordable territory, while Franklin on Auckland's southern fringe would be considered affordable at 39.3%, but only just.

So getting a deposit together is the key to home ownership.

The trouble is house prices are now so astronomically expensive that getting even a 10% deposit together may not be possible for many aspiring first home buyers on average wages, and a 20% deposit would likely be out of the question.

The Real Estate Institute of New Zealand's national lower quartile price, the price at which 25% of sales were below and 75% were above, representing the most affordable end of the housing market, was $595,000 in February.

That would require $59,500 for a 10% deposit and $119,000 for a 20% deposit.

In higher priced regions such as Auckland, those amounts increase to $81,000 for a 10% deposit and $162,000 for a 20% deposit.

Interest.co.nz estimates a couple working full time on the median rates of pay for 25-29 year olds, would need 3.9 years to save a 10% deposit for a lower quartile-priced home in Auckland, if they managed to save 20% of their after-tax pay each week into an interest bearing account, or 7.6 years to save a 20% deposit.

Unfortunately, even if they saved a 20% deposit, they probably wouldn't be able to afford the mortgage payments on a lower quartile-priced home.

Which means home ownership in Auckland is now largely restricted to people earning higher than average wages.

Increasingly, home ownership is not just out of reach for low paid folk, it is out of reach for those on average wages as well.

The tables below show the main affordability measures for purchasing a lower quartile-priced home with either a 10% or 20% deposit, in all urban centres around the country.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

129 Comments

Why is affordability getting worse? Retail interest rates haven't risen, nor have house prices. At the same time, wages are slowly increasing.

Get real Yvil, wages never keep up or else we wouldn't have an affordability problem in the first place. I look at the industry I was in and wages never even tripled over the years and house prices have gone up like ten times.

You're talking long term, but Interest writes these Affordability pieces regularly. Since their last Affordability report, retail interest rates haven't risen, nor have house prices. At the same time, wages are slowly increasing. So my question is valid and stands: why has affordability worsened ?

Yeah the article doesn't mention why its changed so much.

Presumably because house prices have ever so slightly increased

Lets face it FHB are pretty much screwed, back in the day we could have bought a house that's about 1/3 of the prices today on a 5% deposit and we managed to get 10% together no problems. Wages in this country suck, my pay would have had to be like $180K now to be where I was back then.

Where I live in 2002 Median Priced house was slightly less than 4x's Average Median Family Income. At market peak in 2022 it was 12.2 x's that basis, and now with a 20% collapse in the Median Price the factor has fallen down to 8.7 x's Auckland Median Family Income of $129,636. That's the Cost of bringing in 1 Million Immigrants in those 22 years coupled with building costs quadrupling, and people pressure forcing bare land to increase even more than 4 fold without pushing out the Urban/Rural boundary further to create more subdivision land. That supply of ample land back when Manukau was being populated coupled with far cheaper labour and building material costs (not to mention compliance costs) created the Housing Bonanza for the Boomers.

This month's Home Loan Affordability article does not say that affordability has worsened, nor does it say it has improved. It doesn't mention changes in affordability one way or the other at all. It is a snapshot of current affordability levels around the country right now.

Yvil being Evil

Auckland, Tauranga, Kapiti Coast, Porirua and Queenstown are now unaffordable for typical first home buyers even if they have a 20% deposit

Rotorua, Whanganui, Timaru and Invercargill are now the only urban centres in NZ where it would still be affordable

Don't you think these headlines lead to believe that affordability has worsened, Greg?

...it would appear only you led yourself to believe it had.

I read that it had worsened with the words "are now". They were, or continue to be but if you change to are now unaffordable it makes be think they were affordable/doable. Of course the question then is when that was.

I can see both sides :)

Zwifter, while I think it's a valid argument that in times of heightened inflation wages do indeed lag, it's also true that once inflation falls and in times goes negative the relief often returns for the majority. I feel you're conveniently omitting that a period of 2.5% mortgage rates combined with low equity purchasing, temporarily increased the jumbo mortgage serviceability power of the "wage". Nobody with any influence predicted COVID and the unprecedented steps that would be taken to protect monetary system.

Now that the cost of money has clearly risen and will likely remain somewhat elevated, it's all slowly unwinding hence the persistent unaffordability crisis this country endures. In short, the reset we need to have (I personally hope is happening) will take time to play out. All going well interest rates slowly track down and wages on average catch up there will be a degree of relief for many victims of this cost of living crisis.

Had it transpired all this debt had added more productivity to the equation, wages would likely be even higher. Having said that, that would have possibly altered a host of considerations made by RBNZ regards inflation and monetary policy and therefore house prices.

You missed a key statement in the article: Affordability improves markedly for those first home buyers who can scrape together a 20% deposit

Price of basic items/non-tradables (rent, food, energy, power, etc.) outpacing wage growth for young Kiwis means saving up for a deposit is becoming harder, therefore worsening mortgage affordability.

"Affordability improves markedly for those first home buyers who can scrape together a 20% deposit"

You have taken this sentence out of context, it's meant be understood that affordability is improving over the FHB's with only 10% deposit, but not compared to previous affordability reports.

1. Inflation still too high.

2. Insurance costs increasing anywhere from 20% to 100%

3. Rates increasing between 10% to 20%.

4. Wages have not increased in real terms.

5. Home prices have still not dropped enough to make a dent in affordability.

Points 2 & 3 are included in point 1.

Point 4 is just not true. Here is an exert form Dan Brunskill's article of today: "Most wage measures showed an increase in 2023 that was greater than the 4.7% inflation rate". This makes point 1 moot.

Point 5, houses prices would have to have increased in value in order to make affordability worse.

They have gone up in the last 6 months or so...?

Yes that was what I was going to say. Clearly (or not clearly for some….) the authors wouldn’t have access to data showing wage changes, if any, since the last report.

If three people are employed at $60k each, one looses job, two get a $10k rise.

Have wages gone up?

"If three people are employed at $60k each, one looses job, two get a $10k rise."

Should read "... one looses job, two get to work more overtime so earn $10k more."

So no - Wages haven't gone up.

Because fiat money/currency units are worth less.

You're a goldbug..right?

Hi Yvil, I was wondering the same. So, I compared regional affordability from today's article to the same regions in last month's affordability report article: Lower house prices at the bottom of the market meant a significant improvement in affordability for first home buyers last month

Looks like prices improved somewhat from January to February for houses in the lowest quartile, at least in some regions? Remember, January provided a really low base (median price) for the affordability calculation.

So in February, the required deposit for Auckland grew from $154,500 to $162,000 for a FHB with a 20% deposit. Mortgage required also increased by $30,000. Some suburbs in Auckland showed a slightly stronger increase in prices, e.g. North Shore and Central Auckland. Meanwhile, Manukau's prices and affordability fell a little (not enough to offset the slight rise of other areas).

Thanks for "getting" my question, Tui. So it seems that affordability has worsened because house prices have increased since the last Affordability report.

Oh, so it's a good news story after all?

Nobody was putting a value of "good or bad" in this thread. We're simply trying to understand the cause for the unaffordability problem.

-

I can tell you a few reasons why affordability's getting worse. I've spent $60,000, and they've scraped a bit of dirt at my building site . Extortionate counsel fees, engineers inspections, surveyors, stormwater inspection, architect and structural design check.

Who says new house prices are going to drop? It's crap.

Don't forget Project Managers as well.

"Who says new house prices are going to drop"

Market prices can and do fall below construction cost.

An Auckland agent says a flood of under-pressure developers coming forward to sell discounted developments in one go are likely to make big losses.

https://www.oneroof.co.nz/news/cruel-reality-developers-offering-huge-d…

Yes...boxes. Probably not selling because not many want to live jammed together like sardines. Like at Westgate...OMG!!!

Go and have a look.

I laughed when i read this "not many want to live jammed together like sardines"

If true (which it's not), it would also mean they're damn near impossible to tenant too. There will be buyers for these "boxes". The price just needs to adjust to where the demand awaits. At the moment, there exists a glut of overpriced homes and that's why unsold inventory continues to pile on during what is supposed to be the peak selling season.

I also believe the restoration of 2-year Brightline will be an added catalyst for price downside whilst bringing tears to the eyes of the once besotted. Such an outcome, whilst unfortunate for those caught in a bind, provides a positive life changing experience for others.

Spruikers will come up with the darndest theories for what's happening out there.

For the benefit of owner occupier buyers. Make a fully informed decision.

This is something most people do not realise. The property promoters with their vested financial self interests won't tell you this.

Peaker vs Buyer Today

How does this compare with a Peaker and a Buyer Today (BT) in NZ?

1) Peaker

a) Nov 2021

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

b) Feb 2024

REINZ median House price for Auckland: $975,000 (-25.0%)

Mortgage: $1,040,000 (assumed to be interest only for comparison purposes)

Equity: NEGATIVE $65,000 (-125%) (i.e negative equity)

2) Buyer Today ("BT")

The current REINZ median house price for Auckland is $975,000

For a buyer who waited, and used the same $260,000 equity used above, the mortgage at this price would be $715,000 (an LVR of 73%)

The Peaker has a mortgage which is higher by $325,000 (mortgage of $1,040,000 for Peaker vs $715,000 for BT)

As a result of that additional borrowing, at a 6.8% mortgage interest rates over 30 years, Peaker is paying $770,000 more over the 30 years than BT (30 years x $25,667).

Assuming same incomes, and same living costs (food, travel, etc except mortgage), BT can save the $770,000 in payments that Peaker is paying.

The annual payment on the additional mortgage of $325,000 is $25,667 per year.

1) Peaker pays $25,667 more per year than BT.

2) BT instead saves that same $25,667 per year. At a deposit interest rate of 5.8% (after 33% tax is 3.9% p.a). Saving $25,667 per year and earning 3.9% per year in net interest after tax for 30 years comes to a total of $1,415,685.

$1,415,685 - this is money that BT has available for retirement after 30 years that Peaker will not have.

Remember that at the end of 30 years, the house price will be exactly the same for Peaker and BT.

BT will have more money available for retirement than Peaker.

Here are the respective cashflows for Peaker and a Buyer Today (in Feb 2024)

1) At Nov 2021

a) Peaker:

i) Mortgage: $1,040,000

1 year mortgage interest rate: 3.47% p.a

Mortgage payment: P&I 30 years: $56,348

ii) Rates, insurance: say $6,500

iii) Total payment $62,848

b) Buyer in Jan 2024 rents until Jan 2024:

i) Rental per year $33,800 (2.6% gross rental yield on Peaker's purchase price of $1,300,000)

ii) Saves: $29,048 (this can be added to their deposit and can reduce their mortgage even more than $715,000 mortgage used in these calculations)

iii) Total payment: $62,848 (same cashflow as Peaker)

2) At Feb 2024

a) Peaker

i) Mortgage: $1,005,618 (reduced due to principal payments)

1 year mortgage interest rate: 7.32% p.a

Mortgage payment: P&I 28 years: $85,421 (increase of 51% from 2021 payments)

ii) Rates insurance: say $7,166 (due to inflation)

iii) Total payment: $92,588 (this assumes that the Peaker can continue to hold on - in many cases the increase in payment may be too much of a burden on household cashflows and need to sell (and realise their loss of savings as noted above)

b) Buyer today

i) Mortgage: $715,000

1 year mortgage interest rate: 7.32% p.a

Mortgage payment: P&I 30 years: $59,482

ii) Rates insurance: say $7,167 (same as for Peaker)

Total payment for housing: $66,649

iii) Additional amount to reduce mortgage principal: $25,939

iv) Total payment: $92,588 (same cashflow as Peaker)

Some mathematics:

For every $50,000 in additional borrowing to purchase a house today vs a cheaper purchase price in the future, this represents

1) a total of $125,034 over 30 years (at a 7.34%p.a mortgage interest rate)

2) At a 33% tax rate, this requires pre tax income of $186,618 over the next 30 years.

Additional payments to purchase the SAME house. Remember, that at the end of 30 years the house will have exactly the same market value.

3) reinvesting the mortgage payments on that additional $50,000 borrowing at 4.02% p.a (6.0% deposit rate and 33% tax rate) is $234,534 in year 30, that the lower priced purchaser can have available for retirement that the higher purchase priced buyer will not have.

Doing repetitious posts earns a ban, at least it has for others

You've posted these and similar, multi times.

"You've posted these and similar, multi times."

There are a multitude of other readers and many may be new. Those interested in becoming more informed are the target audience. You are free to choose to scroll past and ignore - it's entirely your choice.

Should uninformed / uneducated / misinformed / miseducated owner occupier buyers remain uninformed in making the biggest purchase in their life? They are paying anywhere from 500% - 2000% of their entire net worth on this single purchase (80% - 95% LVR). They are paying more than their entire net worth on this single purchase and could lose a large chunk of their entire lifetime savings or even go into negative equity. Financial literacy is low and people should become informed.

Owner occupier buyers should be informed of decision making frameworks to avoid being collateral damage and changing the entire future trajectory of their financial future and retirement from this one single decision. The value of housing stock at the peak was $1.7 trillion. Despite the house price falls so far, there are still areas with elevated house price risks.

To assume that owner occupier buyers have read any of the previous posts and become informed would be extremely presumptuous. Not every reader is tuned in to learn the lesson at that time but may now be tuned into learning the lesson. There are new waves of owner occupier buyers. An owner occupier buyer may be new to searching for a owner occupier property.

The property promoters repeat their marketing messages frequently and often. How often have the following marketing messages been repeated by property promoters?

1) house prices double every 10 years

2) you can never lose money with real estate

3) buy land because they’re not making any more of it

4) the best time to buy property was yesterday. The next best time to buy is today.

5) Does anyone regret buying a property? I've never met anyone who ever regretted buying a property.

6) house prices go up with inflation

The reason the message is repeated frequently and often is to reach a new audience and to reach readers who were previously not ready to tune into their message.

People are free to choose to scroll past their comments.

The property promoters keep promoting to buy property under all conditions due to their vested financial self interest. This is how house prices rose to extremely elevated house price levels in NZ. There will be more collateral damage, collateral fall out - there will be thousands of affected households.

"Doing repetitious posts earns a ban, at least it has for others "

Feel free to choose to campaign for that. It's entirely your choice.

The moderators should definitely ban behaviour that is disrespectful of others including bullying, name calling, and comments that are derogatory.

Commenters in this community should call out unacceptable disrespectful behaviour. This will raise the standards of behaviour and conversation amongst the community.

If people want to be treated with respect, then treat others with respect.

"Spruikers will come up with the darndest theories for what's happening out there."

Property promoters are highlighting recent house price growth trends and extrapolating that into the future.

People forget the warning commonly used in investing - "Past Performance Is No Guarantee of Future Results"

That same house price growth extrapolation technique was used right up to Nov 2021, and look what has happened to house prices in Auckland and Wellington since.

Extrapolating recent house price growth into the future by property promoters is motivated by their vested financial selfish interests (so that they can earn their commission by getting the unsuspecting buyer to transact) and is an attempted distraction from the basic fundamentals of supply and demand.

Current market conditions in some markets

1) Former Our First Home winner turner property trader Jono Frankle is offering the buyer of 25 Eccles Place, in Otara, an overseas holiday worth $10,000 once the property goes unconditional.

2) "Meanwhile in East Auckland a developer who has one remaining townhouse in a row of six that is for sale is also trying to entice attract buyers by giving away a free luxury trip to Fiji worth $10,000.

Bayleys salesperson Lawrence Liew said there were so many new builds for sale in the area and they wanted this one to stand out."

https://www.oneroof.co.nz/news/sellers-offering-overseas-holidays-worth…

I live not far from Westgate and I can tell you for sure, it is true.

I went for a drive into a subdivision opposite Westgate shopping centre a while back, and was appalled at some of the rubbish they're building there. Up against each other with little or no parking, and the streets jammed with parked cars.

Maybe that's for you, but it certainly isn't for me.

Ah but that is what it's like in the UK and everyone raves about it as the place to be and houses are so much cheaper apparently yet everyone wants to live there

"Yes...boxes. Probably not selling because not many want to live jammed together like sardines. Like at Westgate...OMG!!!

Go and have a look. "

So we can conclude that Wingman has never been overseas?

Or perhaps they have never even looked at how the vast majority of people in large and successful overseas cities live? Or considered that people in these cities are far more upwardly mobile than people in NZ cities? If the wingman actually did look - they concluded the rest of the world are wrong and only the wingman is right.

How many other kiwis are as arrogant as the wingman? I shudder to think! Is it any wonder we have massive problems with housing in NZ?

Im wondering if the plan isnt to crush /push the FHB's / rattle Owner- occupiers elsewhere so specuvestors can clean up in the good locales...Houses are not to live in...they are for profit extraction...lol I see many hopeful of interest rate drops while the FED is still holding.... some saying our RBNZ will be feeling the pressure...but are they? Banks here are probably reasonably happy with the current settings...

"So getting a deposit together is the key to home ownership"

Exactly! The bigger the deposit, the more interest received whilst saving and the more interest saved once the mortgage documents are signed. Adjusted for inflation, house prices are still falling and for the foreseeable future, they will continue to do so. It's a well known fact that renting IS still cheaper than owning. This IS how FHB's can be winners! It's a much anticipated window of opportunity for the disciplined and focused.

There need be no rush to buy. With a bloating inventory, saving FHB's are steadily gaining the upper hand in this well documented Buyers Market and this development will only be well received by those who care.

Clear to me this Govt isnt interested in FHB's or affordability ...its fully supporting Landlords .... burning everyone else ... its gonna be a tough ride for those that cant get mum and dad to go guarantor ... Individuals wont be able too play in the same sandpit as those with corporate/syndicate like backing.... Interest rates narrow the playing field...

I totally agree - this Government doesn't care, especially this one. This aside, market forces are about to weed out the leveraged and overdue. This is an unfortunate reality post extended periods of debt fueled over indulgence with little added productivity to pay our way forward.

Do you have anything to back that assertion up?

So, you think this Government cares for FHB's?

Very much so... aiming to improve affordability

Starting by giving 3 billion to landlords. Hmm, wonder what they might do with more cash? Bid for another rental?

Indeed they will. They'll read CN's analysis above and will be straight off to their bank.

Yes, between now and whenever the OCR is dropped. As soon as that happens I fear everything just shoots back up. At that point it'll be specuvestor vs specuvestor all over again, the guys with the deeper pockets jacking it all back up.

A lot of these articles seem to leave out the stats of the West Coast lately. I notice a rise in listing's in Westport - like there's some sort of a mass exodus from there. Greymouth has been rather flat, and Hokitika overvalued..

I thought Rotorua has a housing crisis? How is it one of the most affordable cities in NZ?

Like all the other crisis areas, no shortage of homes, just untouchable tenants.....

The takeaway...the learnings are, high house prices destroy/reck economies...you can't put it more simplistic then that. NZ is the perfect example.

"the learnings are, high house prices destroy/reck economies...you can't put it more simplistic then that. NZ is the perfect example."

Those who fail to learn from history are doomed to repeat them. Each new generation of investors learn the same lessons learned by previous generations. Most people learn through personal first hand experience.

There are lots of lessons littered throughout history if people look. For example, in terms of significant property price falls, there are lessons to be learnt from:

1) 1582 - 1810 Amsterdam property bubbles

2) 1890's NZ land bubble

3) 1880's Melbourne, Australia land bubble

4) 1920's Florida land bubble

5) 1930's US

6) 1980's Netherlands property price falls

7) 1990's UK property price falls,

8) 1990's Swedish property price falls,

9) 1990's Norwegian property price falls,

10) 1980's Finland property price falls

11) 1998 - Hong Kong

12) 1998 - Singapore

13) 1998 - Indonesia

14) 1997 - Thailand

15) 2008 - Ireland

16) 2008 - Spain

17) 2008 - Portugal

18) 2008 - Netherlands

19) 2008 - Italy

20) 2008 - Greece

21) 2008 - Denmark

22) 2008 - Cyprus

23) 2008 - Latvia

24) 2008 - Estonia

25) 2008 - Lithuania

26) 1990's Australia property price fall

27) 1990's central Auckland property price fall

28) 1989- 1990's property price fall in Toronto, Canada

29) 1990's Japanese property price fall

30) 1980- 1990's US savings and loan - California

31) 2005-2006 US

32) 2008 - Perth, Western Australia

33) 2009 - Queensland, Australia

There will be no property crash in NZ and certainly not in Auckland.

It's a pipe dream. The last lot of turkeys that ran this country have allowed hundreds of thousands of immigrants in. What's that going to do to rents and house prices?

"There will be no property crash in NZ and certainly not in Auckland.

It's a pipe dream."

Don't know what data you are looking at or referring to.

REINZ HPI since peak for Auckland suburbs:

1) Manukau: -21.5%

2) Waitakere: -20.99%

3) Papakura: -19.7%

4) Franklin: -19.6%

5) Auckland City: -19.1%

6) North Shore:-15.6%

7) Rodney: -12.0%

The price changes above are:

1) nominal prices (i.e excludes the impact of inflation since the price peak)

2) before the impact of leverage

Many buyers in the 2020 -2022 period are likely to have experienced a loss in equity. Those who chose to finance their purchase with high levels of debt may be in negative equity.

Perhaps there is a vested financial self interest involved?

Record breaking immigration. Thank you Comrade Arden, and her obeisant apprentice Chippo.

https://www.1news.co.nz/2023/12/12/immigration-figures-show-record-brea…

And still happening today.

Wingman, you’re starting to sound like a desperate RE agent…wink.

Nah, he's bought a piece of land over by the floodplains or something, does seem very desperate though.

He bought it cheap because as you say, a floodplain. Was also banking on the Botanic Riverhead retirement village going ahead and providing value uplift, but is sadly opposed by the trifecta (Auckland Transport, Auckland Council and Waka Kotahi).

https://www.nzherald.co.nz/business/waka-kotahi-auckland-transport-oppo…

The Botanic Retirement Village has already been approved....so you're wrong. 422 units...

https://www.scoop.co.nz/stories/AK2303/S00537/consent-granted-for-botan…

Approved for resource consent, then rejected by the council 3 months later. Please stop.

Figure 1 shows the development site: https://www.epa.govt.nz/assets/Uploads/Documents/Fast-track-consenting/…

Rejected area in yellow: https://www.stuff.co.nz/national/politics/local-government/300869525/au…

TLDR; it''s the same area. It's not happening.

The retirement village has not been rejected, it's subject to the normal consent process, not the fast-track as originally approved.. I've just been talking to The Botanic. . The minor flooding area is in a different location. I live not far from there.

I doubt a Fletchers consortium who already own the land will be deterred by a minor flooding area.

You need to do more homework old chap.

And then here's all those other things happening in that area. Road widening on SH16 and Riverhead-Coatesville H/Way, SH16 bypass, the intersection at Boric's, new subdivisions, school extension and additions to Westgate.

https://findoutmore-supportinggrowth.nz/connecting-north-west-aucklands…

https://gregsayers.co.nz/wp-content/uploads/2022/06/Update-Huapai-Map.j…

{kind=link}

Who wants to be a millionaire?

I've haven't made too many mistakes in decades of real estate speculation, and the countryside near Riverhead certainly won't be one of them. I've done more homework on this one than I would normally do because of the amount of money involved. And I got a $300k discount. Nice.

Go and have a look if you live nearby, everything's selling. Check out the amount of local construction and road works, and this is only the beginning.

Dip your toes in the water boys...and get rich!!!!!! Oh, that's right, I forgot, socialists don't believe in taking chances and getting rich. They like to whine about being poor, and how 'rich people' should be gouged with more taxes.

Wingman, pause for a sec, and ponder why others are so keen to spend their time commenting on your business? You are because, well it's your business. They are because….. it's none of their business, but they can't stand that others take a chance in their lives, whilst they are too chicken to risk anything and therefore they have nothing better to do than tear others down. These are the same people who later on, claim they were "born at the wrong time"

You must be so embarrassed looking back at your views and comments now you can see you have been oh so wrong.

FYI, here is an example of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/2012/09/20/your-money/property/ove…

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

Wellington house price is about to take another hit with the government job cut coming.

about 7.7k in total as a line bet, about 4 months ago I was up for a contract deeply related to MBIE, I am so, so, so so glad I side stepped that one......

Early 2022 I estimated up to a 40% fall in prices from peak for Wellington. I now wouldn't be surprised if we hit 50% in real terms (less likely than not, but still).

Not a great measure, but a couple of houses I am familiar with have seen very substantial drops in their respective homes.co.nz estimates. $1.8m at peak to $1.17m today and $1.6m to $1.07m today. Both about bang on 40% falls in real terms.

People who think we haven't or aren't witnessing a monumental crash are just not paying attention in my opinion.

The effects of these deep, steep falls hasn't even properly filtered through to the wider economy.

using Homes.co.nz to formulate rationale is definitely "not a great measure"...

Agreed. A slightly better, though still inadequate measure might be the homes.co.nz suburb averages. For each of the houses mentioned the respective suburb estimates are $1.39m to $0.99m and $1.44m to $0.99m. Closer to 35% falls in real terms.

Like you say, still an "inadequate measure"

Homes website holds prices up higher than they actually are. You can find a whole bunch of anomalies where every house sold in the suburbs in the last few months sold well below the overall suburb price trend (they get tagged as outliers to keep the suburb price up).

"Homes website holds prices up higher than they actually are. You can find a whole bunch of anomalies where every house sold in the suburbs in the last few months sold well below the overall suburb price trend (they get tagged as outliers to keep the suburb price up)."

Homes.co.nz valuations can be 'influenced' by external opinions

https://www.stuff.co.nz/business/127537672/homesconz-criticised-for-all…

homes.co.nz data is a few month behind real prices. in a downfall market, the key is to survive through the worst and not being forced to sell at the lowest point.

How long do you expect a recovery to take?

My estimate is around 5 years with some generous new version of QE and much much longer if another round of QE proves impossible or backfires. I think QE will be attempted but weakly and with less effect than previously. As such, at this point I think expecting a price recovery to previous peak in real terms within 10 years is overly optimistic. Fundamentals are all wrong and putting them back in place may prove impossible.

Slight upturn in a couple of years when the OCR is back to circa 2.5-3%

old "I reckon" again...The constant voice and authority on real estate predictions, seeking affirmation. 😂

my gut feeling is that wellington has reached price bottom more or less, and likely stay there till 2027, then modest rise from there.

one thing particular about wellington is that, the median price is about 6.5 times of median household income, one of the best figures in the country comparing other main centers.

rent however is another story. depending on population swings, rents need to go up much more to make sense for landlords. rent return is particularly important in period with no/little meaningful capital gains.

If Wellington Council's 'up-zoning' stays on the books then the best Welly can hope for is a long 'flatline' in dwelling prices. I.e. they could follow Auckland between 2016 and RBNZ inspired covid madness.

Of course, prices could fall and Welly might just become the most affordable place to live in NZ. (And public servants won't need such huge salaries to work in Welly. And - by golly - government won't have to pay so much in wages and salaries so will have more money to spend on other things ... like ... I don't know ... tax cuts?)

"in a downfall market, the key is to survive through the worst and not being forced to sell at the lowest point" - unless it keeps going down that is! If we're past peak boomer house ownership, and if we keep building lots, and if interest rates never go that low again, then house prices may never recover, particularly in real terms.

Sometimes the key to surviving is to sell as quick as you can!

"People who think we haven't or aren't witnessing a monumental crash are just not paying attention in my opinion."

Many don't know:

1) Residential real estate is the largest asset class in NZ.

2) At the peak, the total value of residential real estate was estimated to be $1.763 trillion.

3) Prices of residential real estate are 13.5% off their peak - this is roughly a decline of $239 billion before inflation (note that this decline is 146% of the entire current market capitalisation of the companies listed on the NZ Stock Exchange of $163 billion - https://www.nzx.com/markets/NZSX)

Wellington is feeling like the epicentre of the whole thing, lead the initial falls, now seems to be an exodus and severe job losses. At 50% down in real terms, rent still does not compute.

Hardly surprising. The new government emptying out the government departments that have hired 15,000 more civil servants since Labour took office.

PLEASE Greg, write a story on the internal dynamics of the housing market. Anyone reading the headlines will see small price rises and think all is fine. Anyone delving deeper into the stats will see a big storm brewing. And even REINZ median prices in many “blue-chip” Auckland suburbs show 50% falls in median prices. The only way I can see that happening is that the mix has shifted to lower-priced houses and higher-priced ones just aren’t selling. I’ve attended 5-6 open homes every weekend for months and never seen so many agents saying “make an offer! vendor is VERY keen! etc etc. And some sales are going through at below 2017 CV! yes - 7 years with zero capital gain. Seems to me like a few dozen forced sellers in a low-volume market will result in published average falls of 5%+ in a single month.. anytime now..

Record numbers of houses for sale in Auckland’s eastern bays.

It's nonsense, all those absurd predictions of a housing crash are just that...predictions.

Has it happened?

"a housing crash"

How do you define a "housing crash"?

In stock markets, a crash is a sudden fall in prices of more than 10%. Given that stocks (shares) can be traded in milliseconds, it all happens very, very fast.

Housing markets move more slowly. And many places throughout NZ are down more than 20% in nominal terms and much more when inflation is included.

So yes. It has happened. The better question now becomes ... Is it over?

Once again, looking back in history at similar falls - where the market appeared to bottom and then resumed falling - it would be a brave fool that says it over in NZ. ... Especially as we've been in a shallow recession for over a year and now all indicators suggest it's going to get a lot worse. Once unemployment starts rising, the house of cards is likely to crumble.

Wingman, like the song goes: "You need to know when to hold 'em, know when to fold 'em." Take care. Bull-traps are not uncommon.

Feudalism here we come

I’m interested where the average income data comes from. Given the large number of small businesses / sole traders and trusts in NZ I wonder if this should be re-named average declared income.

All of NZ operates under the same housing rules, differing only in the timing of supply and demand.

Every NZ city and town is just an Auckland Cluster*%^# waiting to happen.

Not every nz town and city reached an average of over 1m and had the top end shoot to $3m+

I said, 'waiting to happen.'

It wasn't that long ago all cities and towns were historically always 3x median income multiples.

"All of NZ operates under the same housing rules, differing only in the timing of supply and demand."

Not so. The housing rules are very different between our cities.

Local Councils make the bulk of zoning rules that dictate what can be built where. Central government make national statements of "intent" / "expectation" (and very rarely force rules on local government) but local Councils have a fair amount of leeway to "interpret" them as they choose.

As an aside - Auckland has been doing it quite well since 2016 when the new Unitary Plan enabled a huge amount of land to be upscaled.

(A tragic shame they didn't do it 20-30 years earlier. Nimby voters being the main reason why they couldn't.)

Hold. Hold. Hold....

Let’s move to Rotorua, Whanganui, Timaru and Invercargill - said no one ever

Aww go on. What’s wrong with wongas, timmas and invergiggle? I’ve met some lovely folk in every one of them.

They are affordable in a technical sense only, they are still way overpriced.

You are wrong about Whanganui. One of my young relations moved there with his family two years ago. Amazing weather, great housing at more affordable prices as stated, great architecture (they have kept their old buildings) and a thriving artistic/ cafe culture. In fact young families have shifted there from all over NZ and the world. Go and have a look. You will be amazed. And take your sun glasses as you will need them.

Where is this dreaded housing crash I keep hearing about here? My neighbour has just sold for $1.75m, CV $1.5m.

"Where is this dreaded housing crash I keep hearing about here? "

How do you define a "housing crash"?

I don't know, ask the property 'experts' here. The general opinion seems to be 40 - 50%.

No.

A crash in any given market is a drop of 20% or more.

So both the Auckland / Wellington housing markets are "crashed" in nominal terms already.

To assess real housing market prices, you have to factor it for inflation.

Housing gains have to go up (match it) at the rate of inflation, for it to just stay steady.

It has been the worst asset as an inflation hedge over the last 3 years! Stupid old gold has done much better!

So REAL FALLS of 20 to 48% are now seen nationwide.

The worst losses since the 1970s, when inflation last roared unchecked

This is amongst the biggest crashing property markets in the world currently.....and this is only part way through - the biggest pricing reset in most people's living memory.

Watch out below!

In stock market parlance a crash is a sudden fall. i.e. over minutes, but up to a few days as bull-traps form support levels which get wiped out with another 'crash' that is all part of the main crash that is usually part of a bubble being burst. A sudden fall of even 5% can be called a crash but more usually it's 10% or more.

The larger falls - 20% or more - occur over longer time periods and are usually called 'corrections' as prices adjust to the earnings being made in the economic cycle. Corrections - when economic conditions are very bad can be huge - 40% or more.

Longer corrections get called bear markets. Even when prices stop falling the bear market continues as shares have become very unfashionable. Bear markets - when measured from the first downturn - can last for years.

Obviously these definitions get used by all and sundry and their meanings get confused and used interchangeably. Those who do know the meanings can spot the novices handing out stock tips almost immediately. ;-)

The Bears claws have well and truly become embedded and shredding into the once iron clad, NZ property market.

My neighbour has just sold for $250k more than CV, so doesn't look like a crash here.

Maybe where you are.

Who, in their right mind, would squander their hard-earned cash on a non-yielding chunk of metal like gold?

I see this time as different. In 2007 when the Reserve Bank pushed the OCR to 8.5% that Spring the market topped out by summer, and then by winter of July 2008 was in hibernation, then came the GFC in October 2008, and like the FED the Reserve Bank responded with emergency rate cuts. By June '2009 the OCR has dropped to 2.5% and stopped the crash-but market was still down 10%, and it moved then sideways for the next 5 years. The new 30 year plan in Auckland put the catalyst back into the market about 2013, but then interest rates were still much lower than now. This time around Median Price to Median Family Income is stretched to its zenith (or was prior to the Auckland Median falling back) and I don't see any quick 6 point drop coming from the Reserve Bank to rescue the House Market this time. My observation of this market is now the fundamentals revolve around the "building". the better it is the less that property falls back, whereas the opposite is true for all the subpar buildings out there. The 30% increase in building costs over past 4 years are supporting the better buildings pricing and causing havoc to buildings needing updating. The great Covid tidal wave has gone out, and now we can see who was swimming naked. Already 2021 and 2022 buyers who need to get out and don't have the prime properties are facing severe losses.

I now have 2 neighbours who have sold recently. The latest one, the sold sign went up this afternoon. One sold for $250k over CV, the other, $300k over CV.

What property crash? Maybe where you guys are....certainly not here.

wingman, you sound very very very desperate...... It's a slow motion train wreck, mortgage rates are 7.25%, test rates 9%....

hardly anything is selling above cv, you should study stats so you can read the reports.

Wingman is either extremely lucky or he's good at spinning a tale on the internet. A man of many implausible talents.

You obviously live in an insulated goldilocksland. ........

Most of the Auck region has seen REAL falls of 30 to 40% in the last 3 years.

- It is no way over yet!

Auckland council to rezone the non-flood prone fringes for much more housing coming up soon.

- At the same time outlawing anything but low value farming/horticulture on anything likely floody.....

I have just amended my previous post. One sold for $250k over CV, and the other, my immediate neighbour, has just sold for $300k over CV. The sold sign's just gone up today.

Property crash..who do you guys think you're kidding?

All that flooding you dudes refer to is in your mind. Right now, where I live the average rainfall is down by about 80mm so far this year. And there's no rain in sight. And no violent storms......as predicted by the meteorological 'maestros'.

It's the global warming BS rearing its ugly head again.

It not in anyone's head. It a geologic fact and has been underwater in the past.

Flood Plains | Flood Plains | Auckland Council Open Data (arcgis.com)

It's what the council will enforce for No Future development, only low value activity.....

Dream on old chap. Everything's quite normal here...the weather, the rainfall, the temperatures and the traffic...LOL

Auck Council...ever had anything to do with them? I have.

There's a floodplain just below where I live. It floods about 4 times a year, it's a wonderful sight. But it's caused by weeds in the river and more roof water flowing into it. Not fictitious global warming.

they cannot let you as the liability will be with them for OKing developement, you are now stuck owning a floodplain....

bit stupid really

If the flood waters get to me just about all of NZ will be underwater. I don't own it, it's farmed for grazing and silage.

Global warming....for dupes only!!!

"One sold for $250k over CV, and the other, my immediate neighbour, has just sold for $300k over CV. "

Just out of interest, what are the addresses?

Why don't you start with this one?.

Not my neighbour.....33 Awatiro Drive, Kaukapakapa

LOL. See my comment above.

Never mind The Block - more cash-strapped first-home buyers are spurning doer-uppers to seek homes with “everything done... or no issues”, a Tauranga agent says.

Tall Poppy Real Estate Tauranga owner Janet O’Shea said she believed that could be due to tougher lending restrictions for homes that required more than minor renovations.

“Buying something you can fix over time has always been a great starting point for younger buyers but structural or consent issues are now factors in finance deals falling apart, and limiting options for buyers.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.