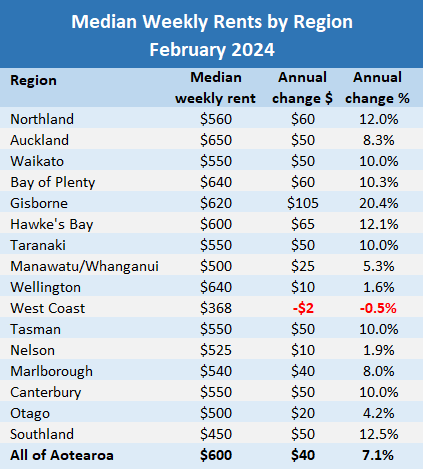

Residential rents increased by about $40 a week (+7.1%) across New Zealand in the 12 months to February, according to the latest figures from Tenancy Services.

These show the national median rent was $600 a week in February, up from $560 a week in February last year, although there were significant regional differences.

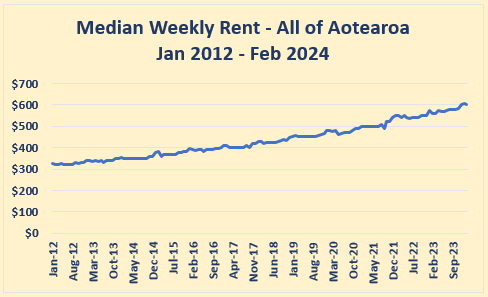

The figures also show rents were mostly stable in the first couple of months of this year, with most of the increases occurring in the second half of last year.

There was only one region where the median rent declined between February 2023 and February 2024 and that was the West Coast, where it dipped by $2 a week to $368 (-0.5%).

The biggest increase was in Gisborne, where the median rent increased from $515 in February last year to $620 in February this year, up by a whopping $105 a week (+20.4%) in 12 months.

That makes Gisborne one of the most expensive regions in the country to rent a home, more expensive than Waikato, Canterbury or Otago.

February's figures for Gisborne do not appear to be a monthly aberration because they show the median there rising steadily each month over the year to February, rather than a sudden steep jump.

In Auckland, the country's largest rental market by far, accounting for 38% of the bonds received by Tenancy Services in February this year, the median rent increased by $50 a week (+8.3%) between February last year and February this year. (See the table below for the full regional figures).

Interest.co.nz's rent data is sourced form bonds received by Tenancy Services each month.

That makes it a leading indicator of rental movements because it reflects the market rents currently being charged for new tenancies, and that data is also used by landlords to assess rent adjustments when rents on existing tenancies are reviewed.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

246 Comments

The funny thing is, it remains cheaper (by about 40% to 50%) to rent than to buy the same average house with 20% down.

What if you bought the house 5 years ago ? Rent has now exceeded what I used to pay down on the mortgage and at the end of the day rent money is cash flushed down the toilet, you have nothing to show for it, not exactly funny.

This is why capitalism is thriving, dog eats dog world!

Zwifter, if you cannot reconcile with the present, why not reflect on the past 5 or so years. Now, lets get back to present day realities. Rent is certainly money flushed down the toilet, much like interest, insurance and rates! If it's still currently cheaper to rent than to own, what's the hurry? Do you stand by your post that August to October 2023 was the bottom? Before you answer, be mindful that when adjusted for inflation, house prices are still falling. Over the short term, there are numerous and valid reasons falls will only accelerate.

Spruikers will always say there's a hurry. If you rent, you will rent for life. It's complete bullshit. Renters can be focused and disciplined savers to.

Yep August to October was a low point. The problem is most people cannot see or plan past tomorrow, this is really a problem with the next generation. I can partly understand it, house prices look so far out of reach that many of them just give up. The world is going to shit and they just live for today and don't even think about where they will be in 15 years time, I mean why bother its all just either getting blown to bits or Climate change is going to kill everyone. The problem is when in 15 years time when you find you are still renting and still waiting for Armageddon you finally realise you totally screwed up.

Don't say things like that. The Climate Change evangelists who are little more than modern day street corner preachers wearing a sandwich board saying "the end is nigh" have certain faith that they are the righteous while the rest of us are little more than carbon sinners.

Is there a place on earth or heaven that the climate change evangelists will all ascend to, while the rest of us die in all the earthquakes, floods, and cyclones "caused by climate change"?

No. Earthquakes have nothing to do with climate change. I'm not really worried about dying in a flood or cyclone.

I'm worried that the earth my kids will grow up in will be a much more hostile place, famine and conflict in previously peaceful countries, despots like Putin, Xi and Trump in power, large parts of our biosphere mounted, mass extinction of beautiful forest, jungle, river and sea life.

But yeah, just laugh, it's so funny

If you want to help your kids I suggest you stop sucking down the propaganda from US led mainstream media. Leaders that broad swathes of the citizenry support support (whether in the USA, Russia or China) but you (and corporate establishment interests) have a problem with are not necessarily "despots". Also increasing C02 is good for record grain harvests. It seems that plants actually thrive when there is more CO2 in the atmosphere. Go look it up.

I take my climate advice from scientists, not US media or keyboard warriors who don't want to face reality.

Said as if scientists haven't frequently gotten things wrong in the past, that scientific journals are neutral instead of being a huge for-profit enterprise and that scientists don't frequently rely on pay cheques and grants from large corporate interests. Further, the record grain harvests I speak of are actually a direct refutation that increased CO2 and accelerating climate change is leading to global famine and hunger.

lol - the data is out there for all to see - a quick look at the NASA website will show you this data in a simple form that a child can comprehend, I suggest you try again.

While Earth’s climate has changed throughout its history, the current warming is happening at a rate not seen in the past 10,000 years.

Oh dear they are already incorrect on this point. For instance, around ten thousand years ago sea levels rose by 70m to 80m. And there weren't even any coal mines or oil fields back then.

Weird take, but maybe it's a comforting belief system for you...

Assuming home ownership is the road to elysium. Its the current mindset thats the problem.

And the number of properties being listed is beyond anything I've seen before. Really weird given it's got to be one of the worst markets to sell into, particularly if you're not re-buying in the same market.

I am really interested in what QV is going to do on the revaluation of property values previously set in 2021 at the peak. Perhaps many in those locales are listing because they anticipate their on-paper wealth being wiped out?

You certainly don't want to be over-leveraged if your current valuation is dated September 2021.

The desire to capitalise falling discounted present values of cash flows associated with residential property assets diminishes as interest rates rise.

I wish I understood that - lol.

My translation would be: landlords are less likely to sell up when interest rate forecasts are for downward movement?

Roughly translates to: landlords have no desire to borrow $1m for negative 3-4% yield. Each increase to interest rates makes that equation less and less appealing. Then increases to rates and insurance too for that matter.

Right, I get that!

extremely roughly...

discount rate (associated with inflation and interest rates) is now a lot higher - future income is now discounted more - so a Net present valuation of an income producing asset becomes lower (although higher increases in rents offsets this to a degree, model a 5% p.a income increase each year (longer term average increases) and you'll almost certainly out pace inflation and counter the discount rate applied).

Hence - buy property.

Okay - but I don't see the market following that advice :-).

Because the net present valuation is much much lower than vendor expectations, and even going prices.

Hence - landlords have no desire to borrow $1m for discounted cash flow.

Hence - do not buy property.

Hence - pile up of listings, as you rightly observed.

Thanks, So, I got it right but didn't know why - lol.

Maybe I should become a Finance Minister - at least I'd be getting it right, eh? :-)

"Because the net present valuation is much much lower than vendor expectations"

Just out of interest, what is the discount rate that you are using in your calculations?

1) unleveraged basis

2) leveraged basis

I beg to differ on that Kate.

The best market to sell into as a home owner wanting to change is a declining market.

You get the cash in, you then have no pressure to re enter. You take your time to find what you want and then make the cash offer.

Selling into a hot market is fine if you have investment properties or a dog to dump.

you then have no pressure to re enter. You take your time to find what you want and then make the cash offer.

But most folks have to live somewhere - and rentals aren't that easy to find, particularly if you have a school district you want to keep your kids in - and, so many LLs are getting out of the business.

listings got to 750 in palmy in 2008/2009 post GFC and sat there until 2014 or so. Prices fell 10% over that period.

Currently 397 listings in palmy. Rebounding prices after 20% drop.

Rebounding perhaps but most advertised with prices generally selling below the 2021 GVs;

https://www.realestate.co.nz/42547489/residential/sale/21-langley-avenu…

https://www.realestate.co.nz/42547419/residential/sale/66a-ferguson-str…

https://www.realestate.co.nz/42546974/residential/sale/12-serenity-cres…

I'd suggest holding off in that market until such time as the GVs are re-calculated in the months to come. I expect downwards market valuations, but just how downwards, who knows?

I have wondered if the record high listings is actually having a short term push on rent increases. It is nearly impossible to sell a house with a tenant in it so tenants are evicted for the listing to take place. I sold a rental of mine last year and it was tough, but it would be tougher now. It was listed for 5 months. Thats 5 months of a 3 bdrm accommodation option that was taken out of the rental pool.

It's a good point.

"I sold a rental of mine last year and it was tough, but it would be tougher now. It was listed for 5 months."

Just out of interest, what was the reasoning for the sale of the investment property last year? Trying to understand your line of thinking behind the sale.

upscaling.

"Upscaling."

Just making sure I understand you correctly.

1) using proceeds to upgrade an owner occupied home?

2) using proceeds to upgrade to a higher yielding rental property?

3) other?

I had a rental house in hamilton while I was working in the Middle East. In 2021 I returned to NZ to work in Auckland and rented. I sold the hamilton house to raise liquidity to buy a home and income property in Auckland. Both as my own home and as a boarding rental that had higher yields than what my hamilton house gave me.

Thank you for your clarification.

Retired-Poppy: Over all the years you've been posting here, you've never advised people to buy a house. For you, it's never the right time to buy. The housing market is always about to plummet.

Unfortunately, anyone who's taken your advice/sentiment on board has missed out on large capital appreciation, along with a host of important non-financial (i.e. intangible) benefits. (The price of many houses have doubled [or more] since you started posting here.) Further, to add insult to injury, tenants have been exposed to hefty rent increases.

Notably, people who have bought houses are not a dissatisfied group. Despite the recent high interest rates, the evidence here (and everywhere) is that the vast majority of home owners (with or without a mortgage) do not regret their purchase decision........ Few of them, if any, aim to go back to renting from a landlord - or living back home with Mum and Dad.

TTP

he has a fixed limiting belief that he is unaware of thats hurting him financially, but will never change unless he has a very deep look at himself.

I think what he really on about is that property prices have pushed well past income support of average people. All fueled by near endless bank leverage , all chasing tax free gains for retirement and endless bank profit. The greed of the vested if you will. That was never going to last for ever.

Now its unwinding. One notes the potential to really unwind, aka 1987and the following decade, looks greater every week that goes by.

IN NZD terms it already has "unwound". You'll never in the future buy the average NZ property for less than today.

"You'll never in the future buy the average NZ property for less than today."

Are you referring to

1) nominal house prices from today's prices?

2) inflation adjusted house prices from today's prices?

I don't really care if someone has been wrong in the past, all I care about is are they right now. From my viewpoint, as a FHB, I don't see how anyone could be satisfied participating in this market unless of course you've owned property over the long term and ridden the market up. I'm assuming RP is referring to the former group not the latter.

Despite rent being painfully high, as you mention, I'm completely debt free, making good returns on my investments, watching the property market go sideways with no sign of interest rates coming down any time soon so what's the incentive for me to rush in and buy right now from an investment point of view?

Its curious that you feel strongly yet still "renting from a landlord" 🤣

blame the inflation. money has time value. yesterday's $$ is not the same as today's $$.

So the 100% interest you pay the bank over the lifetime of the average mortgage is not flushed down the toilet?

Some very basic crystal ball assumptions.

- $600k mortgage @ 7% = $921 per week. Add another $300 per week for rates, insurance etc. Call it $1300 per week.

- Rent $600 per week (up $40 = 7% increase) and assume rates/insurance also increase 7% p.a.

- By year 17 the home owner & renter's outgoings are the same.

- If the renter invested the savings difference with a gross return of 7% and a starting deposit of $150k, they'd have $850k by year 17.

- That $750k house, if it only increases at 3% p.a. is worth $1.2m by year 17.

How about doing these assumptions which could be a more accurate vision of the future.

House price rises only at the general rate of inflation, ie no speculative capital gains

Based on that

- What would the present rent have to increase to, to give you say a gross return of 7% (which is probably not high enough given increased insurance and rate costs)?

- Or what would the house price have to be revalued lower to, to give you a gross 7% at present rental prices?

If the Coalition policy changes happen as intended, there will be no speculative capital gains, and I'm picking point 2 as more likely than point 1.

50% more expensive to build in NZ than AU - economies of scale mainly and a boutique building market. Things no tweaks to certifying overseas materials will fix.

increase population is then added -> new builds needed -> if "too high cost to build for what can sell them for" they wont be built (happening now) -> housing shortage, surging rents, homelessness.

If you dont get it - im starting to think a mass number of people never will (capacity not there to think critically?)

One thing the coalition is doing right in looking at freeing up the building supplies industry - but they also need to bring the cost of consenting (and connecting) down.

As I pointed out in summary to the RMA reforms by the last government, I suspected that the costs to develop for small homeowner/developers wishing to subdivide and/or build a second unit on their property would come well down, but that the big projects would become harder to get through the consenting process;

https://www.interest.co.nz/public-policy/118581/katharine-moody-casts-e…

And isn't it funny how the new government has canned all those good things for little guys and put themselves in charge of granting the consents at the big end of town (the 'Three Ministers decide' Bill).

No, I don't read it that way at all. Reforms by the present Govt. will make it easier to build up and out. But councils will try to impede development due to their adverse risk modeling and appeasement of unreasonable NIMBY objections so Central Gvt. still needs the last say ability to override these.

It has to be remembered that no Govt. in the world has, without pain, unwound a housing bubble. All they can try to do is lessen how wet we all get while the horses are changed midstream.

Reforms by the present Govt. will make it easier to build up and out.

What reforms are those? A reform is not a reform until we see a Bill in the house.

Talk is cheap.

Consenting costs are obscene in this country. If I wanted to subdivide my 1/4 acre plot in Auckland into two lots the cost will be 180k plus 1 year of painful bureacracy. The new lot would be worth about 400k and my house value will decrease by 100k most likely. Its just not worth it atm.

Under the reform proposed by the last government - your problems would have been solved - doing that subdivision would have been a permitted activity (requiring no resource consent). So, you'd have had surveyor, title and connections to services costs only.

Why did you bring AU into your reply? It has nothing to do with the point I was making concerning NZ.

Home owner pays $1.15million over 17 years and now has an asset worth $1.2mil. plus ongoing rates, insurance and maintenance.

The renter has paid $530k rent and saved $630k (total $1.13mil) into savings which is now conservatively worth $850k. Plus ongoing rent.

*For rough calculations I have not factored in increasing insurance, rates or maintenance nor raises in rent.

House prices will not continue to double every 10 years without massive salary increases or near zero OCR. The decade from 2021 to 2031 could see *real* home prices stagnate as per Ireland.

House prices will not continue to double every 10 years without massive salary increases or near zero OCR. The decade from 2021 to 2031 could see *real* home prices stagnate as per Ireland.

Hence I worked on 3% house price inflation. Could be 0% house price inflation, could be 5%. But if rents and rates/insurance increase at 7% p.a. over 17 years, then one could safely assume that wages will also increase at least 3% p.a. and that house prices (supported by borrowing) would also similarly track 3% p.a. conservatively.

The last 30 odd years had several economic and demographic tailwinds that drove asset prices up, and none of these will be repeated in the next 30 years.

1. Continuously falling interest rates making borrowing cheaper

2. Women entering the workforce, turning what used to be single income households into double income households who could borrow more

3. The Baby Boomer generation entering their prime earning and investing years, whose savings were directed to the housing market.

As they say "past performance is no guarantee of future results". Especially when the tailwind of #3 is now a headwind as that generation enters their divestment of assets years, through dying, downsizing, or entering aged care. It pays to remember the eldest of the BB generation is 79, the youngest 60 years old.

Good points K.W.

As you've alluded to, I think this will affect most asset prices, not just houses.

"Continuously falling interest rates making borrowing cheaper"

Should read: Continuously falling interest rates meant people could borrow more

Also remember the equity release / deposit recycling techniques used under conditions of rising house prices, enabling property owners to buy investment property without the need for any cash savings (in effect, the property purchases are financed 100% by debt). This enabled non owner occupier buyers to outbid owner occupier buyers.

The advantages of non owner occupier buyers over owner occupier buyers enabling them to outbid owner occupier buyers

1) interest deductibility

2) interest only financing

3) equity release / deposit recycling financing techniques

4) buying syndicates

Also important to note that we can't double the labour market again as per point 2 and we can't magic up the volumes of easily extractable crude oil as per the1900's so we will never again see the growth and prosperity advancement at the rate seen last century by means of resources, including human resources.

One more suppressor to add: I find it really interesting that people seem to be ignoring the coming DTIs, there isn’t a thing to govt can do to stop these either. If house prices ever try to take off again, guarantee these will be slapped on and cranked down too if need be.

Be honesty mate it never pans out like this at the finish line. The typical renter ends up with zilch because the mortgage is a forced savings scheme and money in the bank just gets blown. I personally know a guy who 19 years ago should have bought the terraced house he was living in, he rented the same place the whole time and never moved anyway but he just doubled down on doing the wrong thing, finally got booted out a year or so ago because it got sold. Could have bought the place at the time or the identical one in the same complex for about $285K and still be living there rent free today.

Its good to see numbers rather than snide comments. I would make the following review marks to justify why I am personally more pro property.

- The $921 mortgage repayment you are quoting is interest and principal. The interest portion will only be $807 pw on week one. And this will decrease every week as you pay off principle.

- The $300 pw for rates/insurance is very conservative. My home is a $1.3m property and my rates/insurance is $125 per week.

- For the renter to earn 7% after tax on their savings, they are going to have to take considerably more risk than simply paying down the mortgage.

- A 3% capital gains average over 17 years might be about right, but it is very conservative for a longterm forecast.

- You have not accounted for the cost of having to frequently move when rental terms expire - the monetary cost and emotional.

- The 7% increase in rent is only the beginning as the inflated costs filter through to the tenants. It is also regional. Here on the north shore, rents have increased about 14% this year.

Good points.

- The renter's 7% savings calculation is gross, my calculation is a 5% net return (28% tax).

- I don't normally split interest from principal, but actually it makes sense. But yes principal payments are part of the home owner's "investment". The interest = rent, principal = equivalent of the renter's savings.

- $300 per week is inline with my expenses on a $1m property (rates/insurance/maintenance) in Wairarapa, but will obviously vary.

Big thing is the investment returns risk for the renter/upwards battle against inflation. And yes the intrinsic benefits of stable home ownership, particularly with children.

I ran your numbers but they show that the renter would have $1.4M at the end of year 17 (assuming tax free investment in NZ shares).

(Y1 savings: $700 x 52 = $36400, Y2 savings: $35308, ...)

(Y1 return: $168.2K x 0.07 = $11774, Y2 return: $15108, ...)

But on the other hand this sounds high for a $750K property:

$300 per week for rates, insurance etc.

It's probably more like $150/wk. Running with those numbers then the renter would end up with $1.16M, so less than the value of the owner's house.

That wasn't my situation. I stopped renting and bought a house with a granny flat last year. The rent from the granny flat covers the interest, rates, and insurance. My weekly cashflow is far better than when I rented. Granted, I had a 40% deposit and I was buying in an area with high rent. But just sharing this, as the calculation on what is cheaper will be different for everyone.

Hardly surprising.

The cost of new builds is going through the roof - architects, Council Consent gouging, Geotech, Engineers, legal fees, stormwater, surveyors, it's never ending.

It's only up for rents, who would build?

Just monitor this next 6 months. All my mates are in the building industry and their workload is falling off a cliff, they are now seeing jobs being quoted 50% down on this last year and they are losing jobs. Well they will need to match or look for alternative employment.

You need to be making 86k/year to be paying less than half your take home pay in rent for a median house (assuming 3% Kiwisaver, no student loan). Is this fine?

No, it's a recipe for disaster.

No, it's a recipe for disaster.

Correct. More share of wallet allocated to shelter, less Nescafe consumed. Even with brilliant creative, Nestle can't drive that incremental sales volume through advertising spend. So Newshub has to close shop.

It's all interconnected in modern consumer economies. But people don't think laterally.

That I understand :-).

I'm sure you do but I honestly think most people don't. Siloed thinking doesn't allow for it. This is one of our biggest challenges. And unfortunately, I think the public sector and ruling elite get it the least.

The internet killed journalism, not the property market lol

The internet killed journalism, not the property market lol

Not talking about journalism. I'm talking about the implications of how h'hold wallets are allocated when more is allocated to shelter.

Anyway, you are correct to some degree. But if you think Nestle is spending the equivalent of what they used to spend on TV advertising on digital advertising and getting the same ROI, you're wrong. Online advertising for previously big FMCG TVC spenders doesn't really work, despite what the likes of WPP, GroupM, Publicis say.

No and it's why more are deciding that the way forward is to not have kids.

It's not remotely ok.

Lol why is Gisborne going up so much?

People are flocking there to try and catch a STD.

Didn't Gisborne feature strongly in the post-Covid property mania? Maybe everyone who speculated on never-ending massive capital gains on a rental property in an isolated, natural disaster-prone, I-swear-it's-a-city is having their loans roll onto new rates and realising the hangover is just starting.

Or maybe everyone just wants to hit the beach with Jacinda and Clarke. You decide.

Record low listings as prices doubled from 2019 to 2021 - with all the landlords depending on beneficiaries and accommodation allowance paying the rent.

After effects of the cyclone taking rentals offline.

Plus ...

- the influx of people doing cyclone related work

- de-housed people - due to cyclone damage - needing places to live

With everything that’s going on with our economy, politics and housing at the moment, I feel like I am watching someone pumping up a tyre with a max pressure of 45psi and we are at 48psi and still pumping, waiting for an explosion but nothing is happening.

Housing is incredibly resilient in NZ, sure its going to turn to shit for a very small percentage of people, but otherwise it keeps on trucking along.

NZ's economy is not just housing ...

We have over $2 billion per annum of taxpayer money flowing into rental yield welfare subsidies for property speculators. And we constrain supply and overtax work in comparison.

Yep, startling actually - and that the subsidy is accepted by a (purported) right-leaning coalition is beyond the pale.

They have a plan however - stop subsidizing school lunches.

"One thing I will say is we will not be spending $350 million because we just can't afford it right now. We will do it in a way that will be more effective and efficient, and is a good use of taxpayers' money," Seymour told Newstalk ZB on Monday.

He forgot to add, but we can afford $2+ billion per annum in landlord subsidies. And David thinks kids these days are performing poorly in maths.

He should have stuck to dancing.

It's deeply entrenched entitlement mentality all the way down...

Indeed. Very odd these days that those calling themselves Christians (looking at you, Christopher) seem to despise the poor. Truly baffling.

As Luxon spent time in the USA, I expect he believes in this stuff - https://en.wikipedia.org/wiki/Prosperity_theology - and tries to ignore Luke 18:25 where Jesus said "it is easier for a camel to go through the eye of a needle than for a rich man to enter the kingdom of God".

Many of the poor are poor for very good reasons, which I won't expand on here.

I'm not going to invest my hard-earned money being a 'christian'.

Your comments point to an extreme, dear I say pathological, lack of empathy.

Actually wrong! I was a landlord for decades and gave my tenants the best possible deal, with any problems fixed instantly.

I never over-charged them and was very sympathetic to any of their complaints, which were few and far between.

But I'm over it, well and truly.

Jesus quoted in the Bible in Luke 18:25: "it is easier for a camel to go through the eye of a needle than for a rich man to enter the kingdom of God"

So I guess there's no chance of going to the kingdom of heaven for me then? I've worked, saved, looked after my family, led a crime-free life, done my best, and now I'm rich.

What a bugga.

I spent 4 years having Christianity rammed down my throat at boarding school......that was enough for me.

Well good on you, you're not a hypocrite like Luxon.

Luxon's done well for himself, a man to be admired, he was my boss, and I liked him.

Yes, I suppose some hypocrites can be likeable for other reasons.

High achievers like Luxon don't get there being soft touches.

He's good guy, many will disagree, but where I worked the only ones that didn't like him were the ones that were on the pig's back before he arrived.

He certainly isn't a sop like Chippy.

Still an entitled hypocrite, per the discussion.

High achievers like Luxon don't get there being soft touches.

No, they get there by taking personal taxpayer subsidies they don't need and by minimizing the tax they pay.

More carpetbagger than high achiever.

Anyone who pays more than the minimum tax is a dimwit.....100%.

So you dont needs road, schools, hospitals, police etc..?

You only pay the tax that's due, not one cent more.

Corporal Muldoon gouged me 66c in the dollar, so I quickly made arrangements to make some serious losses, along with many other NZers. I was doing a lot of night shift and it used to torment me that I was working 1/3 of the time for myself and 2/3 for the Govt. It set me on a new path, and I never looked back.

Many kiwis left NZ and went to QLD after the Premier, Joh Bjelke-Petersen, told them the taxes were much lower there.

Exactly.

Anyone who uses the system to minimize their tax obligations is a carpetbagger (or a 'free rider' in economic terms).

Incorrect, they're just not patsy's that are going to be screwed over.

The Botany Bludger, always with his hand out.

There's just a lot of entitlement mentality going around. People embody it at the same time as hypocritically ranting when poor people receive some help.

And they believe far too much their position is wealth is entirely of their own efforts. Suggests a lack of awareness.

That seems somewhat focused on his housing portfolio. I would make a case that may MPs are guilty of the same thing. Would that comment apply to Helen Clark and the like?

Last Pecuniary Interests list details here

Sure it would.

you were lucky then it was not rammed up the other end given the state of NZs boarding schools. Many of the kids there were severely physically harmed, mentally traumatized and had their lives and future careers upended with significant permanent damage leading them to be many of the poor. It was a well known thing that those schools were rife with sexual assault by many of the staff. It's also well known that level of trauma as children leads to severely negative life outcomes, including MH off a cliff and even physical long term effects; which in turn affects the ability to work, trust in others, future relationships etc.

I didn't see any hanky-panky in the 4 years I was there. There probably was, but if the guys found out, those involved would be hung out to dry. I never suspected any of the teachers.

The only hanky panky I heard about was one of the guys in my class getting up to some mischief in the Chapel at night with one of the teacher's daughters.

13 out of 15 in my class passed School Certificate.

To answer your question, read the next verse.

You are not rich. If you were rich you wouldn’t be so desperate to tell people you are rich on an anonymous forum.

I disagree with the landlord subsidy/accommodation supplement/whatever you want to call it (on a side note, wasn't there a National MP who was making some noise about it the other day?)

Let's say that the government wanted to do away with it - because ultimately it is a big waste of money that just inflates rents.

How would you realistically turn off the tap. I know you are passionate about rental issues, so what would your approach be?

For example, if the government said 'on X date we stop paying out the supplement' you'd have at least in the short/medium term a whole bunch of tenants who suddenly can't afford (or can't afford more than they probably can't afford now!) their rent. I'd imagine that rents would come down over time, as ultimately rents seem to be a function of what the market will sustain, for lack of a better term, but the immediate impact would be total chaos.

Opposition parties would go apoplectic, the media would have a field day, there'd be the potential for real unrest.

Same goes with WFF (which has always struck me as a glorified business welfare scheme insomuch that it allows employers to underpay/not pay proper living wages, and the taxpayer picks up the bill - plus the whole issue of potentially winding up out of pocket if you do increase your income and lose the credits).

These systems seem so entrenched that they can only ever be tinkered with!

if the government said 'on X date we stop paying out the supplement' you'd have at least in the short/medium term a whole bunch of tenants who suddenly can't afford (or can't afford more than they probably can't afford now!) their rent.

The Lange government removed agricultural subsidies overnight, if I recall correctly.

So, one could do the same with these supplements - no warning, just an announced withdrawal and a halt to all notices/terminations to move tenants on for the next 12 months, say. Same sort of measure that was taken on the rental market during the COVID pandemic (they also froze rents during that time).

All things are possible - and frankly necessary at times of crisis - and that's what Nicola Willis referred to our situation as when getting her first briefing from TSY.

Thanks for replying.

I'd agree with that approach. It will never happen - because both left and right benefit from subsiding renters/landlords for different reasons - and we will be having this same conversation this time next year, but I'd still agree with it.

A government with courage/fortitude to do the right thing and not back down could make it work (can you imagine how worked up the likes of John Campbell would be, with respect to the hand-wringing stories they could run, and Chloe Swarbrick would probably spontaneously combust in the parliamentary chamber over this declaration of war against the less fortunate) but if it was combined with strict measures that stop evictions on the basis of not being able to pay the rent for a period of time until the market normalises, it could work out well.

For what it's worth, I think if we dismantled the subsidy aspect, taxed capital gains (as that is ultimately where the business model of residential landlording seems to work, not yield) and taxed equity release for the purpose of property investment or required landlords to borrow via business lending e.g. secure a loan against their existing home but borrow at commercial rates, we could just get to the point of saying 'property investment is a business, it's now treated like a business' and move forward societally.

Dismantling the subsidy/supplement would be a great first step. After all, the government doesn't hand out money to struggling coffee buyers so they can keep cafes afloat.

Yes to all that. they key is to stop evictions until the market settles. Funny, we have such a mechanism where publicly listed company stock can be halted from trading. It never ceases to amaze me that the western world over, no one but no one government has taken a truly transformational regulatory approach to solving the issue of housing.

DT, great point. I ponder this all the time. On one end it shows rents are underpinned by wages, and those insufficient wages due to COL, have to be topped up. If it was reduced, then surely the bottom quartile of rental follows downwards with some time lag. It’s too politically dangerous to touch though, but a real structural issue.

Could fix it by transitioning the spend to subsidising supply instead of demand, while liberalising zoning and gently raising tax on the unimproved value of land while matching with lowering of income tax (reward value makers not value takers.

This would end up generating more supply of housing over time, while also incentivising work more than lazy speculation on exisiting assets.

All that makes sense - two decades ago. The accommodation supplement is now approaching $3 billion per annum - and that doesn't include government money spend on emergency housing; etc.

And with that approaching $3 billion per annum, David Seymour is complaining about $350 million a year on subsidized school lunches. He ought to be the biggest political joke around. He certainly used to be!

Who could forget two elections ago when the media spoke to him and he was half-pissed by 8pm XD

I have thought about this myself as a landlord whose tenants receive the accomodation supplement to pay me. It is a terrible situation to be in as a society. Unfortunately, I think turning off the tap could have serious ramifications. Most landlords at current rent levels have a smorgasboard of applicants to chose from for tenancies. Removing the supplement will not reduce rent, it will just mean those who need it cant compete. We will end up with mass homelessness and an ever increasing social housing waitlist.

accomodation allowance or social housing? pick your poison.

Social housing and affordable homes for first home buyers.

That was easy!

Supply, demand, ability to pay. Econ.

Then spend instead of supply rather than handing welfare to landlords.

Jacinda handed out a 45% increase to welfare benefits, to the point that the average family on a benefit now earns more than the median wage. With all that extra money why cant parents spend $2 a day to send their kids to school with a marmite sandwich and an apple?

Because that 45% increase (over not sure how many years) has all been eaten away by inflation, I assume.

And a marmite sandwich and an apple isn't going to be enough joules to fuel a child at school age. Such sarcasm directed at children is despicable - thought that kind of attitude went out with Oliver Twist..

Are you serious? Not enough joules? A sandwich and a piece of fruit was what everyone got for lunch 30 years ago. That was considered more than sufficient. Then again nobody was morbidly obese. If you think that amount of food is insufficient for a small child's lunch then that child probably has an obesity problem and reducing the joules would be a great idea to head off the epidemic of Type 2 diabetes.

I think people who have your attitude towards over feeding kids is why kids health is so appalling these days, and 39% of children are overweight or obese. Really, go take a look at how skinny kids used to be in old photos from the 70's and 80's. We all grew up just fine.

Split over 3 meals. Probably 4 if you include the after school snack. Not each meal, and certainly not all at lunch time.

I used to get a peanut butter and jam sandwich, a cake/cookie or whatever my Mom's home baking for the week was and a piece of fruit, along with a carton of milk. Never overweight as a kid.

Go to South Auckland and check out the obesity epidemic.

There's reputedly 40,000 empty houses in Auckland. If being a landlord's a such a lucrative business, why's there 40,000 empty houses?

Reputedly might not be accurate, but one reason for ghost houses in the past has been speculation for capital gains.

I don't blame them, who wants to be a landlord these days? I was for decades, but not anymore.

Dealing with tenants....no thanks...done my dash there.

Many would not meet the health homes to be able to rented out.

So owner would not even entertain the thought to spend more money to get it up to standard.

Thats why mine has been empty for 5 years. That, and not being able to remove a tenant on the expiry of a fixed term. If I'm going to go to the bother and expense of renovating my house, I'm not doing it for a tenant to trash, I'm doing it to sell it. So in the meantime I just use it occasionally for a weekender.

(and before anyone suggests that it must be a "mouldy and damp dump" there is nothing wrong with the house, I lived in it for 5 years without a problem, and zero inclination to upgrade it to HH standards while I lived in it)

Sounds like the system is far from being efficient, and capitalism is causing a huge waste of resources. Having a house almost completely unused when there is a lot of people who can't attain shelter.

Its not capitalism that is at fault - if we had a capitalist system I would be free to rent my house out as it is, to whomever I want, for however long I want to. But we don't have a capitalist system, we have a socialist one, where the Govt dictates how my house must be, to whom I must rent it, and for how long. Its the lack of a free market that is the reason why its empty.

But your only holding on to something very expensive that you don't need because it is capital that you believe will appreciate in value, more than its holding cost right?

There are also plenty of rules that limit the supply of housing which you benefit greatly from. Seems very capitalistic to me.

And we actually have the most extreme version of capitalism you can have - one where the capital isn't taxed.

If we had a free market without rules like you imply, I could buy a small farm with some mates and bang up 20 cheap houses without consents. How would you like that with the supply that would unfold?

" if we had a capitalist system I would be free to rent my house out as it is, to whomever I want, for however long I want to"

Let's not confuse capitalism with consumer protection.

If there were no consumer protection laws / standards, the house that you bought could be built with substandard materials or unsafe materials (eg untreated timber, asbestos, extremely flammable materials, etc), substandard construction (e.g leaky homes, unable to withstand earthquake, landslip, electrical wiring issues, etc). These manufacturers could use whatever they want in the manufacture of the house. A consumer would likely be up in arms when the product failed to meet minimum standards (e.g house collapses, flooding in house under normal rain conditions). Governments enact laws for consumer protection.

As a potential long term rental accommodation provider, there are minimum standards to protect consumers (i.e renters), such as no mould, sufficient insulation, fire safety standards, etc.

If there were no consumer protection standards and laws, then there would goods of low quality that could be dangerous for consumers. E.g

- cars that do not meet safety standards when constructed, collision test standards, warrant of fitness standards

- children's toys that do not meet safety standards - e.g a child could choke on the toy,

- food standards - use of carcinogenic substances in the ingredients

Pretty much what I was getting at but you said it much better :)

In the faux capitalist society he was imagining his neighbour would also be allowed to build an apartment block and fill it with Kainga Ora tenants or gang members and he could do diddly squat.

Faux libertarians are the worse.

Here are some examples where builders / developers failed to meet minimum product standards for their consumers:

1) Leaky building lawsuit: Decade-long legal battle finds Auckland Council breached duty of care | RNZ News

2) Builder loses licence over poor workmanship, leaving homeowner with $140k repair bill | RNZ News

Here are some examples of where the accommodation provider failed to provide minimum standards for their consumers

1) Tauranga boarding house fails healthy homes standards, owner ordered to pay tenants | RNZ News

2) Black mould and septic overflow: What tenants are dealing with | RNZ News

More personal accountability needed, perhaps.

Too much is enabled by not requiring people in companies to take responsibility for their work and their products. Too easy to close the company and start another.

Because tenants are a pain in the ass and trash the place. If you are not desperate for the money you don't need to rent it out and you don't need the stress. It was bad enough getting a decent flatmate over the years, as soon as I financially no longer needed one the spare bedroom stayed empty.

I hope you guys are being honest with the IRD about having invested for the purpose of capital gains. Don't go evading due tax when having bought and sold for gains.

If that figure is true, then let's find out who the owners of these 40k empty houses are. Not suggesting we dox them, but it would be interesting to see how many are owned by offshore interests. Money laundering comes to mind, park it in a property in NZ for a few years. Chuck another $50k or so in an NZ bank account and set up a direct debit to cover the rates/landscaper until they're ready to release the "clean funds".

Simple - like in Vancouver - charge an empty home tax if it's not lived in for over 6 months of the year 3% tax on the RV.

They also whacked on a similar property tax on any house being used for short term accommodation, gets rid of Airbnb and holiday homes removing rental stock.

Easily got around. There's ways around everything.

Yes effectively one person can live in many houses and do house sitting. There is nothing against more then one tenancy agreement being written for the same person. You can rent as many houses as you can. All then can be an address for you to use.

Not that easy. As you must provide proof of tenancy which requires govt issued ID for the bond form.

A person can only list one property as their principal residence.

Trying to avoid the tax, when due, is a criminal offence. So either pay up, sell up or break the law.

I shouldn't be surprised to see spruikers advocating breaking the law. A'la TTP, who is one of the few crooked folks, in the real estate industry, to get caught with his hand in the cookie jar.

Yep pretty sure builders have been putting their kids in the houses they just built for a couple of years rent free so they can avoid the GST. You seriously struggle to get ahead in this country if you follow all the rules.

Spoken like the true carpetbagger you so genuinely look up to, wingman.

Socialism is a scourge, I don't mind seeing those on the ropes getting a helping hand, but NZ is chokka with bludgers, and ain't that a fact!!!!

Look what's going on down in the motels in Rotorua...it's shameful. NZ, a bludger's paradise.

I think what you mean to say is that capitalism with rules/regulations is a scourge.

The definition of a socialist is someone who likes to spend other people's money.

I don't mind paying taxes, but I'm not going to be gouged....like hundreds of thousands of other kiwis who've departed these fair shores.

Who do capitalists get money from if not from other people?

Same definition of a 'free rider'.

Where does it come from then...da gubbermint?

No,

-

A free rider is someone who wants others to pay for a public good but plans to use the good themselves; if many people act as free riders, the public good may never be provided.

So, if you employ tax minimization schemes (i.e., do not pay all the tax you would otherwise pay), then you are free-riding off those that haven't got such minimization opportunities and/or don't use them if they could. You are free-riding off 'other people's money' - those other people making up a large majority of NZ taxpayers.

I used to travel down there once a month on business and stay in a motel called the Boulevard on Fenton, I bet you could have serious issues finding accommodation now down there now or worse still a pile of blungers in the thermal pool when you are trying to have a quiet beer after work.

That's why folk are so tired of Luxon and other property speculators freeloading off productive Kiwis. Bloody "socialists". And the universal pension...massive bunch of socialists...

Could get 'Pingers' on the case...

Fury As TikToker Posts Vacant Property Addresses

I especially love the bit at the end. "Would you do a land tax - a vacant land tax?" "No way. No. I think you could probably... you could probably force sales."

That's from the more conservative member of the panel!

Wow - that's a really cool initiative. Younger generations get it - and yeah, find clever ways to revolt. Most brilliant initiative I've seen in a long time.

"There's reputedly 40,000 empty houses in Auckland. If being a landlord's a such a lucrative business, why's there 40,000 empty houses?"

Relatives and friends who have their main residence outside of Auckland, also own a residential property in Auckland to stay when they visit Auckland. The reason they come to Auckland is due to business interests, visit family.

Note that these people may live elsewhere within NZ or may live overseas.

Would be interested in knowing how many of the empty residential properties in Auckland fall into that category.

Another stat that would be really interesting would be to break down these increases for 1 , 2 and 3+ bedroom homes.

I did a very small sample study - and the percentage increases were largest for 1 bedroom (by a huge margin), then followed by 2 bedroom - and least for the higher number of bedrooms.

Not sure why that is - but what really needs some serious thought by regulators is that many, many soon to be retirees do not own their own property - so will be renting for life. Big problem in coming as the level of the pension assumed homeownership on retirement was the norm. Yet another one for our younger generations to have to face unless a current/near term government starts thinking about it.

I'd say give it time and the demand will fuel the supply in the 1bdrm market. Already plenty of interest around in places with a granny flat out back or somewhere that can either be rented, or the parents can live in once they downsize so to prevent draining their wealth in old age to a rest home. After this reaches capacity, I predict much more conversion of 3 beds into split homes with 1 bed each to supply this demand.

so to prevent draining their wealth in old age

You might have misunderstood - point being that many, many will be retiring with no wealth to drain.

Market supply and demand won't help that issue at all. It's why we used to build OAP council-owned flats (and now even those rents are unaffordable to many pensioners living in those that are left!).

What we have had is past retires selling houses that they bought at 3x median income to present purchasers buying at 8 to 10x median income.

This has allowed those older homeowners to sell at inflated prices and take a huge amount of debt-free capital gains.

But as time has gone on it is now 6x median income homeowners reselling to 10x median income purchasers, so their capital gains is less, hence they have less to retire on than earlier retirees.

This is unsustainable, and change had to happen at some time. The longer it's left the worse it will be.

The change will cause problems, but if we don't do it now, then we can wait until we get to our mentor's position: Councils in crisis: Town Hall debt levels staggering, MPs warn (bbc.com)

Not saying that is wrong, Dale - but again - you ignore the elephant in the room, that being those retirees with no wealth/savings at all arising from past homeownership.

I feel a bit like Bob Dylan, asking the question: how many times can a man turn his head and pretend that he just doesn't see?

I'm trying to remember the figure put out by a gvmt dept recently. Something like 60% of retires by 2050.

Yep, I think it was the Office of the Retirement Commissioner that did the maths.

You missed my point entirely, it is the very system we have been using that not only means there are already some retirees with no wealth/savings from past homeownership, but 'you ain't seen nothing yet' (Bachman - Turner Overdrive)

Major Retirement villages are selling future development land because present retirees cannot sell their homes for what they need to buy into retirement villages and have enough cash to pay costs above their pension.

And the present Govt. has only been handled a hospital pass left over from the last three decades of Govt., but especially the last 6 years of Labour.

Yes, agree with all that. Which is precisely why land supply isn't our immediate problem.

And for how many years have so many folks been arguing that? I think I first read a Demographia report nearly 20 years ago now. Haven't read one recently, but I'm guessing they are still seeing the problem as being land supply constraints.

Yes, perhaps that was yesterday's problem, which has morphed now into a whole new strain of illness - and freeing up land supply (mostly in outer fringe areas) isn't going to address today and the decades to come problems.

Now you have the time, you really need to do some more reading, Start with Alian Bertaud, and then work your way back to Allan Evans.

It all starts and ends with the price of land on the fringe. It's not even Land Economics 101, it's primary first-principle stuff like the times table.

Today's problems are due to the land supply constraints both up and out, especially out, which in turn allow the continued thinking that leads to consenting and infrastructure supply constraints.

Every other problem like immigration, interest rates, and accommodation supplement, etc., either does not exist as an issue or is greatly reduced if the right land use policies are in place.

Oh, gawd - I've read everything he's written! And I didn't disagree with him when he started writing it.

Times have changed - we live in a far more resource (and wage) constrained environment now.

Read something current like: Against Landlords: How to Solve the Housing Crisis

I'll be doing a book review/analytical comparison to the NZ situation shortly.

Saying 'times have changed' concerning the universal principle of land economics and supply and demand drivers is like saying 'times have changed' since 2+2 first equaled 4, so you don't believe in maths anymore.

Adam Smith was saying in 1776 what I can see happening still today.

Universal truths are also universal in time.

And we have never in human history have had access to more resources and the wages that have come with that. It's the waste of the non-valued costs of these resources via restrictions that is the main driver of unaffordability rather than not getting enough income.

Our quarterly rent analysis breaks rents down by 1 & 2 bedroom apartments/units and 3 bedroom houses, and further by main urban districts including Auckland Council wards. The next quarterly report is due around May.

Great! Will be so interesting to see if my small sample translates to wider NZ.

The previous govt. let hundreds of thousand of immigrants into this country....now we're paying the price.

The notion that property prices are going to plunge is pie-in-the-sky. Meantime the NZD's tanking which makes all imported materials more expensive.

Homes are not purchased with cash. They are purchased with borrowed money. People can't borrow as much as they could in 2019 to 2021.

ELI5 where the money will come from to pump prices again.

As long as the OCR holds above 5% the property crash will continue.

What property crash? My neighbour just sold for $300k above CV.

"What property crash? "

FYI,

The current median sale price is $1,287,089

The median sale price was $1,524,222 in March 2022 (peak)

That is a fall of 15.5% in the median sale price.

The median sale price at the bottom was $920,301 was a 39.6% fall from the peak

Having said that, the current median sale price is 39.8% up from the bottom.

https://www.realestate.co.nz/insights/auckland/rodney/kaukapakapa

This one time in band camp

starrider property crash, where exactly?

Is a 20% downturn in akl and welly since peak - in real terms-not a crash?

I live not far from Auck and there's no property crash here. 2 of my neighbours have sold for more than CV recently. The crash is in your head.

2 of my neighbours have sold for more than CV recently

I guess that is the 18th time you've said that now....

Probably...it's a fact...the notion that there's some colossal property crash underway is moronic. I've also stated many times that every available subdivided piece of land in Riverhead has sold out.

So where's the crash?

A moment ago it was 1 neighbour, now it's 2. Red hot property market near Wingman, be quick!

It's more than 20% in real terms.

One bedroom places make for great airbnbs so they are often taken out of the regular rental market. It's certainly true in Wanaka where one bedder rentals are extremely rare then you can see a whole lot of them on airbnb.

I watched a new piece on DW (German news) recently discussing falling birth rates around the world and they said that western governments were all looking after the older generations at the expense of younger people.

You say that sort of thing in NZ and young people get told the problem is them eating too much avocado (when they probably aren't drinking or smoking as much as previous generations did).

and they said that western governments were all looking after the older generations at the expense of younger people.

So true.

Having children went from being a community and family virtue to being a planet destroying vice. So why should these intensely resource consuming/carbon emitting children be particularly valued now?

Why should they value older narcissists? Might be time to turn off the pension tap?

That's what euthanasia is. Now legalised in every western country and becoming increasingly popular. Ask yourself, why is this nihilistic culture being pushed upon all of us?

Previous government did think about it and their solution was to make it an order of magnitude more expensive to provide rentals.

There are only two solutions that will work. More houses, and local government provided housing. Local governments already can't afford to run pipes through their cities so they will not buy more housing.

Possibly because there has been a large number of brand new one bedroom units built recently. Williams Corp in Chch has built a lot - they were all aimed at the AirBnB market, but were put into the long term rental pool over Covid. There hasnt been a lot of one bedroom units built for a long time, so its just reflecting the recent jump from really old one bedders to brand new one bedders. Likewise, there are not a lot of 3-4 bedroom houses being built for the rental market, so its still mostly older homes that are available to rent.

Sounds inflationary.

A big rich waikato company wants to tap $10m from a govt fund to build affordable rentals that charge 80 percent of market rent. Give it 12 months and that 80 percent will be up anyway and meanwhile we are all paying the cost, on average 280k per unit.

I don't like how these rich big noters get on the gravy train

https://www.waikatotimes.co.nz/nz-news/350236085/city-blocks-affordable…

And this government likely doesn't even realize that 80% of what the market rent is charging, isn't affordable to greater than 50% of the renting population.

Based on my rent maximum formula, this 1 bed room flat needs to rent for $191/week to be affordable if no more than 30% of household income is the basis;

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

On an RV of $246K - that sounds about right to me. Yet this one is being advertised at 17% over what the tenancy.govt.nz market rent estimate is (and of course that market rent itself isn't affordable either - not unless you put a family of four into the 1 bed flat)..

Gisborne demographic means landlords are now deciding it is not worth the trouble there. Big sell off.

Guess we do need landlords after all.... else rents will keep climbing

Funny though how every time investors hit a small regional town the locals start finding affordability of both prices and rents gets worse... A recurring story in recent years.

Previous government decided to crush supply.

The average asking price for rent in Canada reached $2,196 in January, a 10 per cent increase from this time last year — marking another record high amid a deepening rental crisis.

https://www.cbc.ca/news/business/rentals-report-average-asking-1.7114976

Asking rents for houses and units have jumped to new record highs in Australia's major cities, according to Domain's latest rent report.In the March quarter, asking rents for houses saw their steepest quarterly gain in 17 years, and asking rents for units extended their record-breaking streak to 11 successive quarters of growth.

Canadian government decided to spike demand through record immigration.

Australian government decided to spike demand through record immigration.

Previous government decided to spike demand through record immigration.

They are looking at our births - record low - and the boomer generation about to start popping off in large numbers, and are making a logical move (to them). I'm not defending it, but I believe that's the reason.

They are looking at our births - record low - and the boomer generation about to start popping off in large numbers, and are making a logical move (to them). I'm not defending it, but I believe that's the reason.

By 'they' I assume you mean the ruling elite. They should be transparent of what they're doing and why. It's not difficult. Mad Albo in Australia has not been transparent and people on the lower socio-economic rungs are being sacrificed for his cunning plan. While luxury car sales are booming, there is unrest on the other side of the tracks.

That's $506 per week.

Cheaper than NZ.

Thanks to previous government policy, landlords have learned the importance of conducting annual rent reviews instead of waiting every five years.

The rent freeze that Labour imposed during Covid has ensured that everyone's rents go up at the same time now. So when the rent freeze was lifted in September 2020, landlords all put rent increases through in the last 3 months of the year. Then that pattern was locked in forever by the law change that restricted rent increases to once a year. Thats why the rent increases are most in the second half of the year, and not in the first half.

The question is not can renters afford to buy. It is now can renters afford to rent and we are past the point that for large sections of the community that answer is no even with subsidized rental housing. We are even past the point of van and hostel accommodation being affordable. But then the question becomes, what happens when people lose the sense of a home and become disengaged through a lack of belonging long term. We have ample study data but there is no one doing the studies on the real cost to society this has, (both in health, employment & tax takes, discretionary spending, and societal loss).

We don't even have income support for large sections of the disabled community and this is an increasing group as with rising & ageing population more will have disabilities as a % compared to a younger population. Post pandemic saw a rapid rise in disability. Yet nothing changed and Labour even admitted that what little support there was to some was not enough to live on for most people yet they still only treated those with work subsidies with dignity and trust. Something they specifically do not allow disabled people to have. Both sides of our 2 party system treat disabled people as chattels to this day. Not deserving of independence or rights to exist as individuals.

Woohoo.. well done Luxon, keep going

Hi Greg,

Just a question. All my tenants are on long tenancies from 2 to 5 years, and they usually renew for similar periods rather than move to a periodic basis. I usually increase the rents annually and usually by an amount so low my accountant gets apoplectic. I don't adjust the bond amounts when the rent goes up. (Too much hassle and by then I know the tenants are looking after the places. I've never not released 100% of the bonds ever.)

When a new tenant must be found the market rate is the starting point (not that that happens often as the tenants usually finds and recommends someone they know to take up the tenancy, albeit a new rate higher than what the previous tenant was on. My property owning family members do similarly.

How does that affect the validity of the figures? Could they in fact be overstating rises?

The short answer is No.

I think your situation illustrates the disposition of land lords in new zealand. Rather than being greedy fat cats, they are slow to up the rent because they desire to keep the income stream PASSIVE. A high turnover of tenants is a stress that I cant be bothered with. I know that I can charge $40pw or so more on my rentals, but I would rather not lose the good tenants that I have. When I do need a new tenant, I advertise a little below the median so that I can choose from a wide range of applicants.

I fear that this implicit discount that renters receive will be wiped out as the government seeks to regulate the industry more and more.

if you use a property mgr they always put rent up as that is their growth plan

Your pricing setting echoes mine. Always a good thing to have a pool of prospective tenants to chose from. Best way I know of to ensure one gets great tenants.

Clearly we need to tax landlords more in order to increase the supply, and iimport more immigrants to reduce the demand. That's how it works, right?

comment of the day :)

Just spoken to a colleague who has just been made redundant. A full third of her specialist consultancy (to private developers and local/central govt) is also being made redundant, with no guarantee there will not be more come June.

Her husband's small IT consultancy firm is also about to go under (under 20 staff). They haven't paid wages since Jan.

They locked in low rates 4 years ago and mortgage is up for renewal in 2 months.

They had to cancel an imminent international holiday.

SHTF

Good time to be in, or find, a recession proof job folks.

undertaker, though bad debts increase?

Horrible horrible situation.

"A full third of her specialist consultancy (to private developers and local/central govt) is also being made redundant, with no guarantee there will not be more come June.

Her husband's small IT consultancy firm is also about to go under (under 20 staff). They haven't paid wages since Jan. "

Think beyond the wife and husband couple. There are all the other people losing their jobs (other colleagues of the wife, employees of the husband's business) - these people may also have mortgages. These households may come under cashflow stress. Remember that most mortgages require two household income earners to be affordable. Those most vulnerable will be those highly indebted households.

From the Dec 2023 statistic, there are an expected tens of thousands more to become unemployed.

There is a long line of chickens coming home to roost... its past non linear, the RBNZ will be cutting very very soon.

the gov job cuts are NOTHING in scale compared to the cuts going on in private and corp yet TV news etc is quiet...

Panic in 3...2... 1

"Her husband's small IT consultancy firm is also about to go under."

Also if the business has a large amount of debt outstanding, this may be secured against the owner occupied house. The lender may wish to be repaid. A liquidator or receiver may need to sell the house to repay the lender.

Listing such a house under duress into a market environment where unsold housing stock is at a new record. Ugly indeed.

It's an undeniable fact that anytime the government tinkers with anything the price goes up.

Governments are colossally inefficient, and the previous 6 years of socialism was more than enough proof of that.

And yet prices had stated to fall under Labour with the policies they had just put in place that National are now unwinding.

Like what prices dropped?

All the imported prices over which nobody in NZ has any control.

Oh yeah - all those kiwi build homes dropped prices.

Inflation, caused by the previous govt, made what prices fall?

And yet prices had stated to fall under Labour

House prices which went up 30% under Labour then retreated 6% still corresponds to a net 24% rise under Labour. Unless you are a Labour supporter I guess in which case you ignore the dismal first three quarters of the game and focus only on the last twenty minutes of play.

Genuinely surprised Tauranga overtaken Wellington and is snapping on the heels of Auckland too. Followed not far behind by Gisborne of all places. Remote workers moving for beach life? Or just sign of how crappy their councils are at building new homes for their residents? It is baffling that our 3 biggest economies aren’t necessarily the highest rents here - a given in most other countries!

Predicted it a year ago at the end of Covid. Working from home has become possible with technology and Covid just sped it up big time. Auckland is now a Circus you don't really realise how bad it was until you leave. Better beaches, better weather and better bang for your buck houses elsewhere as long as you have work.

Yet the status quo keeps wanting to force everyone into the CBD.

They forget that the Christchurch earthquakes answered that age-old question, 'if a city did not have a CBD it could not exist, or would have no soul.'

Well within days/weeks of the Earthquakes, businesses had related to the suburbs and beyond and businesses got going again, most more efficiently than before.

It is no coincidence that people flee the cities for the countryside in times of emergency.

Rent might be cheaper now but will rent be cheaper in 10 15 20 years time? No.

If you only ever paid interest on a mortgage and never touched the principle in that kind of time period you would still be paying a fraction of the cost in interest compared to what the rent would then be.

Also all the psychological aspect of renting. We’ve all rented and it’s a ghastly experience.

'Median' does not mean the 'Average' rent

Median is simply the middle number, and often times the average is skewed to the left and lower...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.