The latest figures from Trade Me Property suggest people selling their homes appear to be becoming more realistic in their price expectations.

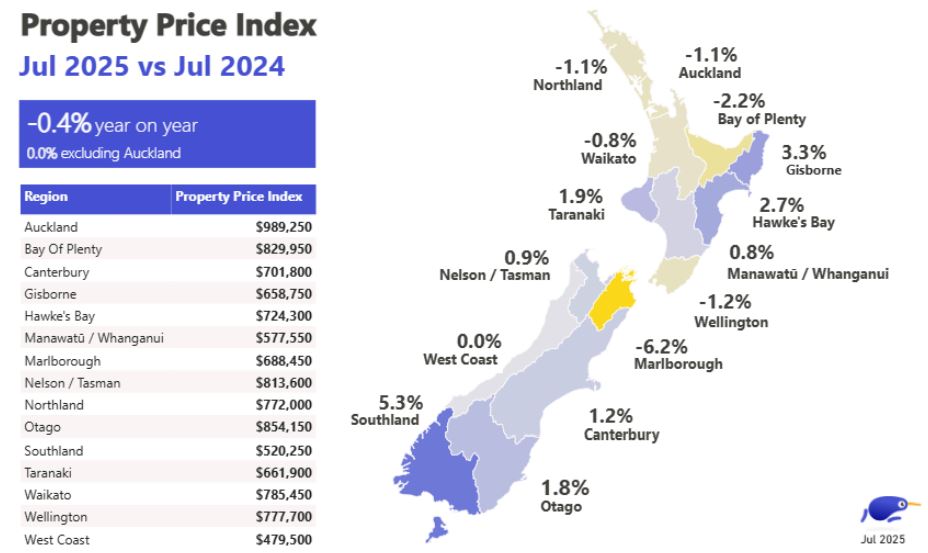

The national average asking price of residential properties advertised on Trade Me Property was $821,750 in July, down by 1% compared to June.

In Taranaki the average asking price fell 4.1% in June while asking prices in the Bay of Plenty dropped 3.0%.

In Auckland, the country's largest housing market, the average asking price dropped below $1 million for the first time since September last year to $989,250 in July.

That's down by $17,000 (-1.7%) compared to June and the average Auckland asking price has now declined by $68,050 since March.

There is often a dip in prices over winter, however Trade Me Property's Customer Director Gavin Lloyd said this year's dip in Auckland's asking prices could be more prolonged than in previous years.

"This dip has occurred earlier than last year, suggesting that we may see a more prolonged period of prices [in Auckland] below the $1 million threshold in 2025," Lloyd said.

"Last year, prices remained under $1 million for two months and we anticipate this year's trend could last a little longer, creating a unique opportunity for buyers," he said.

The comment stream on this article is now closed.

49 Comments

Great news. The NZ property crash, enters its next major down leg.

DTIs of 3 or 4x, by the market bottom, come 2027 or 2028?

4 x is definitely a possibility by 2028, but you'd have to have a 250k household income for that to happen - closer to 300k if you live in Auckland.

Your assumption then is that prices will not continue to fall? I believe the figures above say otherwise.

No, I don't believe that real estate prices will continue to fall. I appreciate that my views are contrary to 95% of the people who frequent this comments section. I just don't buy into the narrative that we're on the cusp of a major real estate meltdown. Sometimes it's best to filter out the emotions of this debate and just sit down with a calculator and run the numbers. My view is that high inflation is behind us. Energy costs are on a downward track. Shipping rates to NZ have fallen dramatically over the last 12 months - I know this because my boss imports millions of dollars worth of product into NZ each year. Ships are sitting idle thanks to the general downturn in the world economy and more recently because of Trump's Tariffs. Costs will continue to fall and inflation will fall off a cliff, leading to big interest rate falls in 2026. I believe that we will see retail mortgage rates fall below 4% in the next 12 months or so and I see rates hovering around the 3.5 - 4% mark for many years to come.

How big is your housing portfolio?

Just one at this stage (my own home), but I'm investing in a new-build property in Dunedin later this year.

Fair enough - are you factoring in unemployment trends and migration trends into you thinking above? Or do you think unemployment has peaked?

I think unemployment is close to peaking but there's always the risk that it could edge higher, which is a deflationary risk. Net migration should stay in positive territory for the time being, but not at the high levels we've seen in the past.

The US 10 year bond yield is indicating that we are returning back to the world that existed prior to the GFC. ie it isn't saying extremely low inflation and interest rates. The trend from 2020 to now is upwards, not downwards - the complete opposite world from the 1980's through to 2020.

OK, that's interesting. It will be fascinating to see how this all pans out. I see much lower rates of economic growth in the next decade which will require some stimulus.

More stimulus with low growth could mean more inflation - ie more money chasing limited supply of goods and services, which could see rates continue to creep higher.

Eventually you can only throw so much stimulus at markets/economies (at least in my opinion, based upon my reading/study) before you realise productivity has peaked and all you do is create inflation instead of growth (resulting in falling GDP per capita - what we've witnessed recently). Eventually to increase growth you need to increase productivity, not just give people more easy money which only drives up prices. But I don't see where this productivity is coming from to improve GDP? Are people going to start working more hours for less pay? Are we going to educate people better? Are we going to attract more talented and educated migrants (instead of diary owners, nursing home workers and uber delivery guys?)

Sounds highly inflationary - that degree of wage growth....which in turn would see very high interest rates (due to the high inflation caused by high wage growth)...which in turn would put large downward pressures on house prices.

More and more vendors by the day realising that they were holding on for a price increase that never eventuated. I personally know 3 already who were hanging on and in turn, they have lost more money than if they sold when they initially intended and took a reasonable price at the time.

Prices sliding and this is BEFORE tariff deflation hits! Rents ↓11.6% Wellington, inventory ↑93%. Debt/income plateaued at 170%, but debt servicing doubled from 5% to 10%+ since 2021. When servicing costs↑ + prices↓ + debt stays elevated = balance sheet recession locked in.

Global forces incoming: US tariffs → trade destruction → deflationary vortex. Watch unemployment & liquidations, not price noise. Real bottom when unemployment spikes (not there yet), liquidations surge, credit freezes. Resistance futile when debt mathematics kick in.

How do you get a deflationaey vortex from tariff increases? Just because you can't afford something, doesnt mean it's price will fall.

How do you get a deflationaey vortex from tariff increases? Just because you can't afford something, doesnt mean it's price will fall.

Good question. Let me suggest that in the case of Aotearoa / Aussie, China dumping on markets could definitely lead to some price deflation. So the price of some goods would become cheaper for the hoi polloi. That would potentially drive a collapse in the health of the retail sector, thereby causing 2nd-order deflationary effects - land prices, supply chain pressures to lower cost / margin. That ultimately would funnel through to the cost of services and price of money.

Good question! Here is how it works => tariffs crush trade volumes (history shows -70%) → company revenues tank → mass layoffs begin. Someone's spending = someone else's income, so when jobs go, it all turns to custard pretty quick.

Sure, tariffs raise prices initially, but that's self-defeating => higher prices → people buy less → stuff piles up → prices crash → more redundancies. The deflation from mass unemployment swamps any tariff inflation. Reagan nailed it https://youtube.com/shorts/Mj6N-WBPrVw. Those who forget history are doomed to repeat it. Check out 1930s Smoot-Hawley ~15% tariffs led to -10% DEFLATION, not inflation, for years. Reckon it takes about a century for these lessons to be forgotten. 2025 meet 1930!

What you are really saying is tariff increases reduce our standard of living (correct), but the case for lower prices is not made. Yes, spare capacity may lead to deflation eventually, but that means ignoring the inflationary increase in prices from the tariffs themselves.

We did just live through the longest/deepest yield curve inversion since the lead up to the 1930's depression - so anything is possible. But would the Fed allow -10% deflation to ever manifest itself in the US economy with what they know now, as a result of what happened in the 1930s? I don't think so, I think it will be a repeat of 2020 where when they get scared, they overdo the stimulus again and we see inflation roar once more as they are far more afraid of deflation, than inflation (what was more painful - the 1930's deflation or the 1970s - 1980's inflation?).

We haven't recovered from the Covid over-stimulus. Wages just will not pace prices higher and our standard of living falls even further.

Exactly - just made a similar comment above. More stimulus does nothing to improve GDP per capita - see whats happened COVID to now. You just throw money at the economy, increasing money supply, but without increasing productivity. You just get increasing demand for a set supply of goods and services.

Result is:

1: higher inflation

2: higher interest rates

3: lower GDP per capita/aka living standards.

If the intention is to dramastically increasing money supply via stimulus the government need to have plans on how they are going to increase the supply and goods and services that this increased demand can 'gobble up' (no better term came to mind) - otherwise (in my opinion) we will see inflation tick up again and rates on the rise again and potentially house prices falling even further in real terms and potentially even in nominal terms as well.

Spot on! Fed will definitely try the money printer go brrrr strategy. But Japan tried for 30 years - only got inflation from COVID/supply shocks, not QE! Today's setup worse => $80T private debt vs $27T GDP. Fed can't bail everyone at the same time. The math doesn't work! They'll panic-print for sure, but when everyone's paying debt or scared to spend, that money just sits there doing nothing. 2008-2015 proved it → trillions in QE, barely moved inflation. Sometimes the medicine doesn't work

Yeah I read Dalio's 'Changing World Order' a few years back and it talks about what you mention above. I think a lot of people completely underestimate how precarious the global monetary order is right now. The US is at a precipice which if they don't act very carefully, could see everything crumble. US deficit spending is still at 6% of GDP which is insane - they immediately need to cut that in half to avoid debt levels and the associated drag of the interest cost of debt from overwhelming their ability to pay (ie their interest expense is going to grow faster than their domestic economic growth - ie their costs will go up faster than their incomes - which is the path to bankruptcy). But I think if they cut their government spending by 50%, they will immediately enter a really nasty recession (or even depression).

So yeah I think they could well be damnned if they do (print money) and damned if they don't. 2008 appears to have put them on a completely unsustainable path - but one that has happened to every previous reserve currency nation. Young people should start to think about what the world would (or will) look like if (when) the US doesn't have global economic and military supremecy. Because I think in the decades ahead the US is either going to have to pull back by choice, or be forced to do so by internal fighting over the state of the local economy and its out of control finances.

Disaster looms. They need to go into surplus and pay some back.

They won't do it. Soon they won't have the choice either.

The property price index has changed 0.0% (excluding Auckland) in the last 12 months. This is huge news. How will the country cope with such a change?

An investor friend of mine who repeatedly told me "I would never sell any of my rentals" has put one on the market.

Is the party truly over this time?

Short-term-thinking property investors appear to be exiting the market at the moment. However, this is probably the worst time to get out because there's so much negative sentiment out there. Unless you're in way over your head with debt, I think it's best to hold, as things will improve going forward. Property is a great way to build wealth (long term) IMO. Those that freak out every time there's a dip in the market aren't cut out to be a long term investor. The phrase "Be fearful when others are greedy and greedy when others are fearful" comes to mind.

Depends if the numbers stack up. At current prices it still doesn't stack up to buy due to poor yield and ability to borrow due to DTI introductions has limited the rebound as investors cannot access the leverage they used to be able to. Without such availability of leveraged credit, and with a govt who has been in cut back mode for a couple of years, the recession is dragging on.

Yip gone were the years where investors held a property for a few years, got 30% capital gain and then used that equity as a deposit for the next rental. That was crazy stuff. We really should have enforced cash deposits only for new rental lending - otherwise it becomes ponzi like where 30% capital growth gives everyone holding a rental a deposit for a new rental (causing extreme artificial demand on the market...driving prices way above intrinsic/fundamental cash flow based values) without any savings (and in theory it is real savings that drive future investment - not vapour equity). That vapour equity could just vapourise and keep vapourising meaning all those who thought the gravy train would continue forever get caught with their pants down.

Great news. More affordability. Long needed for level 1 of Maslow’s Pyramid

95% of the listings in Central Auckland have no price. Until they list with a price, they are not motivated vendors.

You have to enter a price when you list a property for the price bracket search params, it's just not visible on the public facing listing....... Well that was the case 5 years ago when I was mucking around writing a program to figure out the price of listings.

I think we might be approaching the fear and capitulation phase of an asset bubble

Most have spent the past few years with the denial and 'its about to return to normal' thinking. Prior to that we've had ample greed, enthusiasm and delusion (can't lose with property maaate, property doubles every 10 years even if wages don't).

But what if 'normal' was actually an extreme anomaly?

There are a couple of properties in our area for sale that would have been snapped up quickly in the past but are not moving. Good sized do ups on good sized sections. One just reduced their price another 50k. It actually has an asking price (meaning they actually do want to sell), the price seems reasonable to me (although there is a lot of work to be done). I think Auckland just went down another gear in the last month or so.

And each day that goes by approx 100 NZ'ers die, leaving either a home empty or another widow or widower living alone in a house that is too big for them. My street is around 75% widows living in properties too big for them (3-4 bedrooms) and will all likely sell and downsize in the next 5 years I'd imagine (some in the next 10 - although one across from me who I thought was healthy just had a heart attack and and spent two weeks in hospital so who knows..). If this theme is consistent across the country, there are going to be a lot of 3-4 bedroom homes hitting the market in the coming years.

I think there are some huge demographic shifts happening right now.

Spot on IO.

The Overleveraged must be fearing that their positions becoming very untenable over coming years, in this paradigm shift. If not, they should be.

Yip we've just lived through two decades of boomer and millennials (the two largest demographics) competing for the same homes - millennials want 3-4 bedroom homes to raise families, while the boomers didn't want to downsize early and thought buying a 3-4 bedroom rental was also a good idea in addition to their owner occupied home.

Now in the next 10 years 50% of the boomer generation will die (average age 80-90 born 1940's - 1950's) which is going to be a huge shift on the demographics of the nation - let alone the housing market.

Many millennials will be setup with their own homes in the coming years already, and then the boomers will all try and sell their 3-4 bedroom homes at the same or similar time as they downsize, die or move into care. If we don't have very high migration levels, there is going to be a lot of excess stock sitting on the market.

Agreed. We have run the demographics race that multiplied values. This same demographic pattern is why Retirement Villages have boomed targeting downsizers. Perhaps we will just open the immigrant floodgates here again without electoral mandate.

If we let in enough in, from a specific county, that group could vote to make NZ a satellite state and military base for their county of origin.

Democracy at work or self stupidity.

In the U.S., Redfin reports that millennials with children own less than 15% of all homes with three or more bedrooms nationwide. In contrast, empty-nest baby boomers own twice as many large homes as millennials with children.

https://www.housingwire.com/articles/empty-nesters-own-twice-as-many-la…

Yeah, I’d say that the theme of people dying is most likely going to be consistent 😂

I can’t see house prices not going up again in the medium term, mildly (not that 40% over two years kind of BS), if the economy improves…if the predictions of house prices capitulating (further) then I am assuming the economy will also stay 💩?

Hate it as much as many do, but surely our economy & house prices are too tightly coupled to see any other outcomes?

"Yeah, I’d say that the theme of people dying is most likely going to be consistent"

Jokes aside (funny haha) - it is the concentration of death relative to the total population which is important. Boomer generation dying is going to be a big deal given how big they are (or were as a total % of pop) and how much capital they have and where it is invested. If they all rush for the exit at the same time (ie over the next 10 years approx 50% will be dead as I say, this is a significant event) - and remember the marginal buyer or seller sets the price of the market and thus the value of that whole generations equity/net worth. So if there is a flood of listings as they downsize and die, their collective net worth all simultaneously takes a hit. It could completely undo the trends of the past 30-40 years.

Yep, I got the math…more dead folks, more empty houses…maybe the kids/grandkids of these boomers move into the houses instead of selling & it has bugger all effect on listings?

I still think if the economy improves then house prices rise, & it’s a fair assumption to think there will be an effort to improve the economy. Cause-and-effect relationship of housing & the kiwi economy?

My pick, prices to bounce along for another year with these tiny jumps/drops, & hopefully if everything has been done right (DTI/LVR) then when our economy finally fires a shot again the inevitable price rises don’t outpace income rises.

I’m just not sure the armageddon is arriving with a further 30-50% drop.

"I think there are some huge demographic shifts happening right now" - if so, its funny how quickly that has happened. Housing market was on fire 3 years ago.

Things happen slowly and then quickly there Jimbo, don't ya know? And then you say...'how the hell did that happen....the housing market was on fire 5 years ago?'

Stories about lots of early boomers trying to sell do-up homes for top dollar above market value to get into their desired rest home.

They may not be aware how tired their kitchen and bathrooms are, especially compared to well presented new homes, finely staged. Nor they may not know how much it actually costs to replace kitchens and bathrooms.

Rest home on sales are struggling. I'm picking major problems lie ahead for the likes of Rymans and Sumerset. Their model is now broken.

Last week the Fed quietly published an article discussing gold revaluation noting that the idea has come up in the context of helping to establish a strategic bitcoin reserve or a sovereign wealth fund.

Interesting timing and an admission that USD has fallen from 1/42 oz to 1/3300 oz of gold in the past 54 yrs - that's a CAGR of 8.4%. For those that care about economic data accuracy, this CAGR is MUCH higher than the official reported inflation rate over the same period

The ol' rat poison has gone from $0 to $100K+ and the streets do not resemble Mad Max. If gold went north of $20K+, there would also be no Mad Max scenarion or hyperinflation.

https://www.federalreserve.gov/econres/notes/feds-notes/official-reserv…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.