Residential building costs are starting to move up again, albeit modestly, after consolidating at high levels following the extreme 2022 cost run-up.

The industry expects an overall expansion in 2026 on the back of anticipated lower mortgage rates and increased ability for households to finance projects or buy off-the-plan.

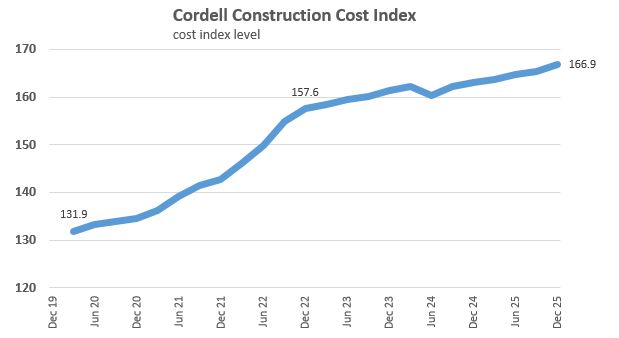

The latest Cordell Construction Cost Index (CCCI) shows that the cost to build a ‘standard’, single storey, three bedroom, two bathroom, brick and tile standalone dwelling (over a normal build duration) in NZ increased by 0.9% in the three months to December. That was the largest quarterly rise since 1.1% in Q3 last year, however still a touch below the long term average of 1.0%.

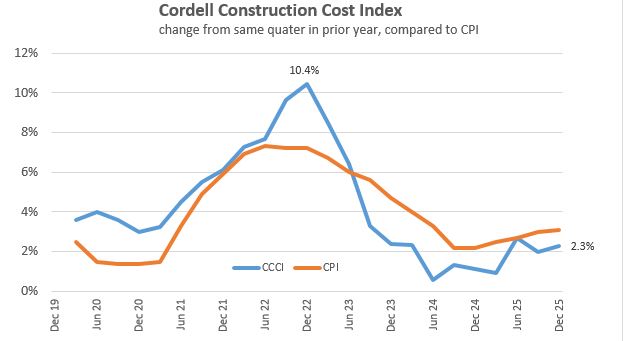

On the back of Q4’s lift, the annual pace of growth accelerated from 2.0% in the third quarter last year to 2.3%.

That might seem a little concerning, but again note that it’s still well below the long term average; which has been an annual growth rate of 4.1% since late 2012.

In other words, construction costs continue to increase, but the pace of growth remains contained – and certainly nothing like the inflation seen in the post - COVID phase, when the CCCI rose by more than 10% at its peak annual growth rate in late 2022. That was when plasterboard for example was in short supply and wages were rising quickly.

To be fair, there haven’t been significant falls either and after that previous growth phase the overall level of costs to build a new dwelling remain elevated (even though the growth rate has cooled).

Even so, households will be buoyed by the flatter backdrop for construction costs, and it’s reflective of the degree of spare capacity that is likely to have opened up in the aftermath of a downturn in workloads in the past three years or so. The CCCI is comprised of roughly 50% materials (which are better supplied than before), 40% wages (which are also more stable), and 10% for other costs such as professional fees and charges.

The most common measure for construction activity is the number of new dwellings consented, which is not a foolproof indicator for how many houses eventually get built, but it still illustrates the scale of the recent downturn in workloads. After peaking at more than 51,000 in the 12 months to May 2022, the number of new dwellings consented dropped to a low point in the range of 33,500 - 34,000 for much of the second half 2024 and first half of 2025.

More recently, however, that 12 -month rolling total has started to rise again, reaching more than 35,500 in October. That’s consistent with anecdotal evidence that builders are starting to get busier again, reflecting lower mortgage rates and increased ability for households to finance a project or buy a property off - plan. The loan to value ratio and debt to income ratio rules both also have exemptions for new - builds.

All in all, then, the construction downturn has seen building costs flatten off, after a previous strong increase. The latest CCCI figures for Q4 2025 remained relatively controlled. However, as the industry (likely) starts to recover more clearly in 2026, construction cost growth could pick up a bit again. All else equal, however, a spike similar to the post - COVID phase remains unlikely.

The Cordell Construction Cost Index (CCCI) is used to monitor the movement in costs associated with building work within particular segments of the industry. The CCCI indicates the rate of change in prices within particular segments of the New Zealand construction industry. The changes in prices are measured daily through the use of detailed cost surveys, and are reported on a quarterly basis. This ensures the most current and comprehensive industry information available. The index is based on a combination of labour, material, plant hire and subcontract services required to construct buildings within the particular segment being measured. The CCCI measures the change in the cost of constructing buildings, and as such does not provide the actual costs.

The CCCI is comprised of around 50% materials, 40% wages, and 10% for other charges such as professional fees.

The comment stream on this story is now closed.

2 Comments

House prices are flat or falling outside ChCh and QTN. Demand will not really pick up until that reverses. Why pay a premium otherwise.

Costs escalating from an already obscenely high base, despite no visible value add, and the expectation is that the customer will just pay up, no matter the cost.

How can a major industry be this broken and not collapse the entire economy? Oh. Wait...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.