Sales volumes and selling prices both dropped sharply at Auckland's largest real estate agency in February, while new listings and stock levels rose strongly.

Barfoot & Thompson sold 785 residential properties in February, down from 824 in January, a drop of 4.7% for the month.

However, the agency's January sales were particularly high and while that level of momentum does not appear to have continued into the following month, February's sales were still the strongest they have ben for the month of February since 2021.

While sales levels showed mixed results, median and average selling prices both posted substantial falls.

Barfoot's median selling price declined by $96,000 (-9.6%) in February, to $904,000 from $1 million. That was the lowest the agency's median selling price has been in any month of the year since July 2020.

Barfoot's average selling price took an even bigger hit, dropping by $155,797 (-13.3%) to $1,013,976 in February from $1,169,773 in January, the lowest it has been in any month of the year since September 2020.

Ominously for the Auckland market, while Barfoot's sales levels and selling prices declined in February, the available stock of homes for sale was building up.

Barfoots received 2252 new residential listings in February, up 8.6% compared to February last year. That pushed the agency's total stock of homes for sale up to 6159, up 2.7% year-on-year. That was the highest level of stock the agency has had on its books in the month of February since 2010.

These figures clearly suggest that buyers in Auckland remain spoiled for choice when looking for a home and that is being reflected in lower prices.

"The attraction that is drawing buyers is current price levels," Barfoot & Thompson Managing Director Peter Thompson said.

"With the median sales price in February at $904,000, down 9.6% for January, and the average price at $1,013,976 down 13.3%, these are among the lowest monthly median and average sales prices since in Auckland since prices peaked in 2022," he said.

"Effectively, housing supply is starting to meet housing demand and the prices are starting to draw in buyers who once felt priced out of the market," Thompson said.

The comment stream on this article is now closed.

Barfoot Auckland

Select chart tabs

51 Comments

More listing, lower prices, throw in lower rents to boot equals a triple specvestor negative. All before the bun fight for capital gains tax even gets going on the run into the election. And before the war fueled gas prices pump inflation and interest rates again.

How do you spell yield again... oh yeah minus another 30% on price just to stack up.

Last week: Banks forecast a flat market for 2026

This week: Auckland records price falls of circa -10%

Probably Nothing

Central West Auckland outperforming.

Not suffering the 'Townhouse Curse' in these preferred leafy suburbs!

🥂

Where is Central West Auckland? Mt Albert? No townhouses?

Westmere, ponsonby, herne bay, gay lynn etc.

These would all be on a map old boy!

😅🥂

I thought you were spruiking Riverhead for a bit there, Having owned in Summer Street Ponsonby I never considered I lived out west....

I can't hear the humming of the economy which the ASB talked about. Nevermind because every economist and financial commentator is saying" the economic recovery is well underway".

The NZ property crash is accelerating downslope, without doubt!!

- I think the crashing market has got inspiration from the Olympic downhill slaloms.....:)

Worse still, for the Coteyyourselfin PonziDebtVior peeps, this is a 100% crash confirmation, reported by the "most property Ponzi positive" Barfoot's Property Ponzi benefactors.....

Its look out below folks, this market bottom in a very deep cracking V....and still not in sight.

The next report from FRED, will be very interesting for Ponzi gamblers!

Real Residential Property Prices for New Zealand (QNZR628BIS) | FRED | St. Louis Fed

The chart doesn't get updated often unfortunately. Its still only got Q3 2025 as the latest data point.

So the real time real inflation adjusted price falls are actually worse now than what this chart shows. ie we are now back down around 2016 prices in real terms.

Not to read into one data point too much but......there has been a pretty obviously trend of flat prices for Auckland for a few years now. e.g median trading in a band of $930,000 - 1,000,000. This is the first data point that is a significant anomaly to that trend.

If technical analysis were true for housing markets, then this is showing strong weakness to the downside. If true, the next floor might be around the $800 - 830K mark. Another low read next month might be a breakout into a new trend into the downside.

I wouldn't be rushing to buy into this market - so don't be quick - patience may actually be a virtue in this market now.

On this topic...

I still don't understand why the banks are issuing so much debt at low LVR's with this much downside risk - it would be easy for prices to fall another 10% from here and all those buyers (and mortgages) to be in negative equity. Almost looks to me like desperation by the banks to try and prop up prices at current levels. If I were working at a bank and somebody said to me looking at the chart above - 'do you think its a good idea to issue people loans at 10% LVRs in this market with these economic conditions and this level of geopolitical uncertainty?' - my answer to this would be hell no, the risk is way too high.

Banks have never been that responsible.

Its all about making big cash today, bonuses today.

When all the newbys (bank cannon fodder) get captured at 4.5% mortgages rates or so....then/when/if we see 6 to 8% mortgage resets in 2027, the poor newby sods will need to fold.

The NZ ARM mortgages, are indeed the very risky end and a big stage setter for the GFC:

The Big Short (2015) | Ninja Loan (No Income, No Job, And No Assets) | Steve Carell, Max Greenfield

Many NZ home sellers - are now becoming increasing- VERY MOTIVATED!

All lending is risky. House prices could have fallen by 10% at any time in the past as well.

Market conditions look nothing like they have over recent decades - and market conditions and risk do change over time - although by the nature of your comment it would appear that you don't agree with this.

Happy to be convinced otherwise if you have valid points to say that the current risk profile for the NZ housing market is just as it has always been. I don't see it.

People should have to come up with a 20% deposit, for their own protection and for the banks. I don't see why we should be using low LVR lending in a time like this.

I would have said the risk was higher at the peak.

A 20% deposit would lock many people out of the housing market. More people going to Aus. And even 20% isn't fool proof if they lose their job.

Probably the bigger risk is interest rates. I suspect all low equity loans should be 3 year fixed or more.

ITS AN ARM SETUP FFS!

Banks are lending to buyers with low LVRs because the numbers add up. If they deem a client to have a sufficiently solid income with disciplined spending and a reasonable deposit, they know they will be be able to service the mortgage for decades to come. Trust me when I tell you that they do a LOT of investigating in to their clients' finances - I've just been through it myself and can confirm they know as much as my proctologist. Unlike many people on this forum who obsess with the month-by-month comparisons, banks take a long-term view, as do their clients. Most people who buy a home don't intend on selling it 12 months later and can cope with a short-term "loss" in (paper) value because they don't care what the house is worth next year - they're more interested in what it will one day be worth when they decide to downsize or retire or step up to a better home.

This is BS, banks issue low equity loans because that's all the client has as a deposit.

Because they have a smaller deposit, they have to satisfy more stringent criteria with regards income and expenses. No responsible bank is going to lend to someone who's likely to default - it's bad for their bottom line and it does a dis-service to the clients who want to get on the property ladder. Don't believe me? Well, then take a look at the average New Zealander's ability to pay their mortgage. Mortgage arrears in New Zealand were at 1.42% of the active population (approximately 22,600 home loans) as of January 2026. That's 1 in 70 people. Not exactly a disaster (though I do feel for those people all the same). The point I'm trying to make is that Banks do a very good job of making sure their clients have the very best chance to buy their first home, and to comfortably be able to service the debt on it.

hamishk1

Sounds like you may have just bought your first home. If so, Congratulations.

I agree with you totally. Homeownership is that owning one’s own home and with many intrinsic values and less about a financial investment that one flips off as the market fluctuates. Owning your home is a life-long term and you will buy and sell a few times in your lifetime buying and selling on the same market without loss or gain whether the market is high or low. Over a thirty year time span, given inflation it is likely to have appreciated in value. To those who scream about real value rather than nominal value, they over look that your mortgage will inflate away as you salary inflates upwards. My first mortgage was $30,000.

Unsurprisingly, there is all ready a response from a financial illiterate who do not understand that homeownership is long term. They also have no understanding that banks are in the business of making a profit and are not going to lend if there is risk with either the borrower or the longer term market.

I wish you well, and that comes from one who is very comfortable in retirement after a life time of homeownership and interest in property. When in investment properties, I experienced four periods of declining house prices but made gains on each of investment properties.

And to counter those who call me a lucky boomer, I have four sons, aged 37 to 43, and all are financially very comfortable while being in their own homes without my financial help.

Thanks, Printer, for your positive response. I usually get my head bitten off here whenever I write anything positive about the housing market. Your comments have really lifted my spirits :-)

Printer works for the bank (no shit) so you are his debt slave. Hence his encouragement. The used car salesman is always going to tell you he's sold you a little beauty of a car even if its a shit box.

Independent Observer

You know that is not correct - just like many of your pathetic DGM claims proven wrong time and time again. I'm happy to post these if you are going to indulge in baseless slagging off. Pull your head in.

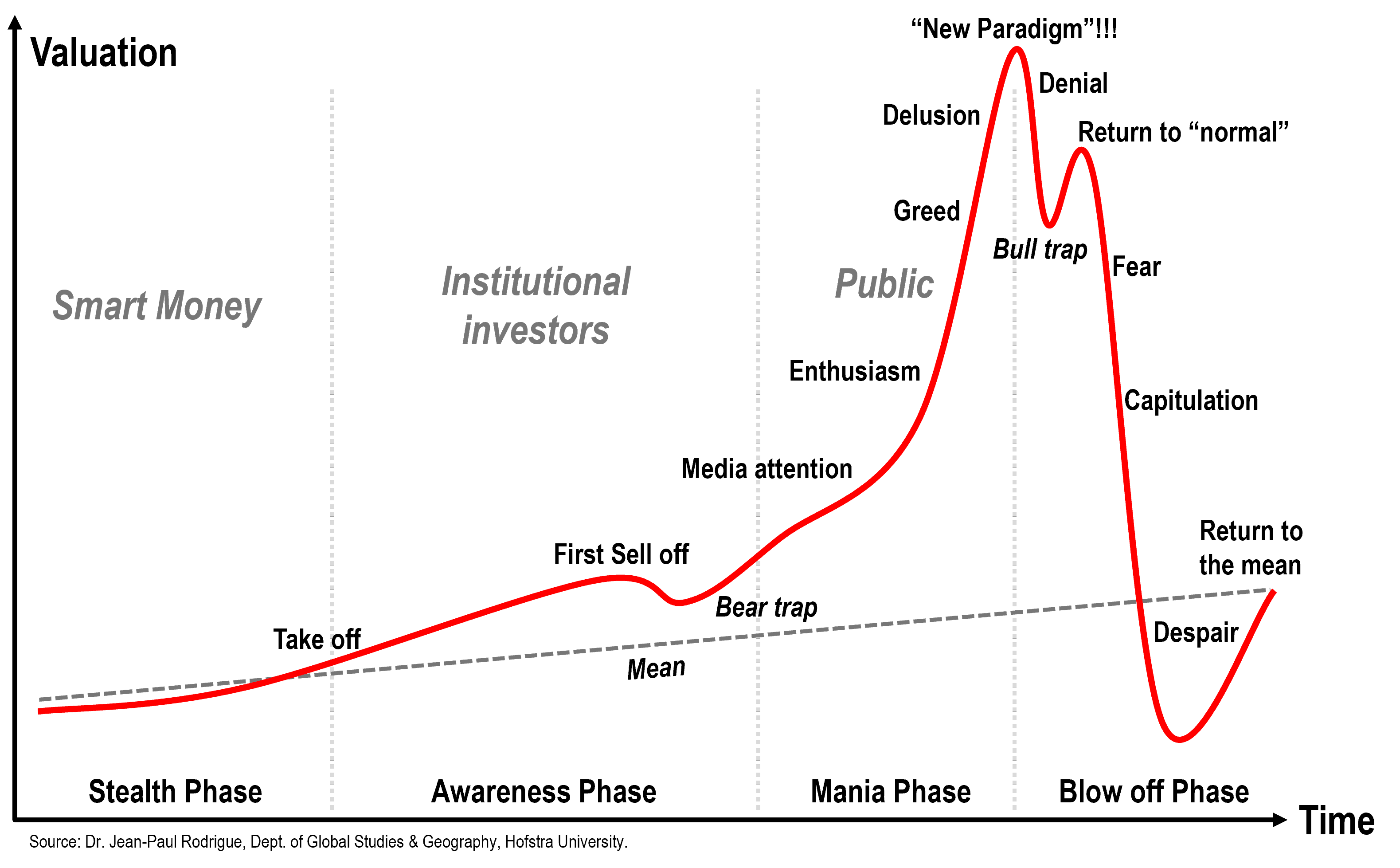

Think we might now be moving from the 'back to normal' to the 'fear' stages of an asset bubble.

https://transportgeography.org/wp-content/uploads/main_stages_bubble.png

{kind=link}

People trying to push 'green shoots' was the back to normal psychology and now people seem to be waking up to the fact that there are no green shoots and on an income/yield basis/cash flow basis, houses are still waaaaay overpriced. ie fear.

It's taking time here in Ham's northern suburbs. A lot of properties advertised above 2021 peak, some by a couple hundred ks. Not selling of course.

Also followed the usual Wednesday's auctions, 75% passed in with what I thought were solid bids at +10% of CV...

Patience is always a virtue

It's even the mother of them all.

DGMs if prices go up slightly: "its just that the bottom end of the market has collapsed and only top end selling"

DGM's if prices go down slightly for one month: "this is definite proof of the housing apocalypse"

NZ Housing Apocalypse and likewise continuing trend proof ! - your Honour JJ.

Real Residential Property Prices for New Zealand (QNZR628BIS) | FRED | St. Louis Fed

As I have said for a while now, house prices have been flat and will probably continue that trend, which does mean losing value after inflation. This erratic Barfoots data hasn't changed my mind at all, although if it continued on a downward trend for a few more months it might.

It's irrational loss averse buyers that drove up prices, and irrational loss averse sellers that hold them there. Unless a significant number are forced sales by the bank or put up for true $1 reserves by desperate owners, I wouldn't expect prices to decrease in a hurry - and certainly wouldn't expect the masses rush in to buy at ever higher prices, driven by the self-reinforcing myth that the price can and will always go up. Myth busted

Holding steady for the foreseeable future is probably the sensible forecast, but inflation/opportunity cost/interest and the rest makes it a losing "investment" for many that view it as such going forward.

The 13.3% drop in the average sales price represents the largest single month percentage decline in average price for Barfoot & Thompson in at least 25 years.

Probably nothing...

It went up by 11% the month before, what did that mean?

It meant that prices would need to decline by 9.91% the next month to wipe out those gains.

However, the average price only went up by 2.58% in January, not 11%

Just a tinsy winsy gully...

What's so gloomy about house prices going down. I'm delighted about it.

This boomer thinks it's wonderful for young New Zealanders.

I'm a PPM. Pleased as Punch Merchant.

Me to, but GenX.

No net immigration = no property party

Add in future renters exiting west in mass, council rates up a lot, rents down, available rentals up a lot (options), building maintenance costs up a lot.

CRASHFLOW...

As a yield based investment houses have another 20-35% to fall to make them worth buying.

What if the house also retains its value (keeps up with CPI), which is probably a reasonable expectation over the long term. Then it’s made its yield on top of inflation, and the inflation part is tax free unlike some other investments. So it’s maybe not terrible considering how safe it is compared to other investments. Not saying I’d go there.

No net immigration = housing affordability party 🥂

Net migration is still positive so, please, enough of the disinformation.

1000 people per month is well below the average.

With the quality of immigrants we get, they do not buy a property straight off the plane.

The drop in sales volume is surprising and speaks of weakness in the markets

Vendors will have to reduce their price expectations or they simply won't sell

(Also agents need to stop giving inflated expected prices = no sale)

Add in the surge in building consents and prices are on a slippery slope for sure.

So many posts, nothing like house prices crashing to get attention

Face the music time...

Slip sliding away

Know when to fold em

Down down down in the funky town

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.