Average asking rents continued to decline in February, according to the latest figures from property website Realestate.co.nz.

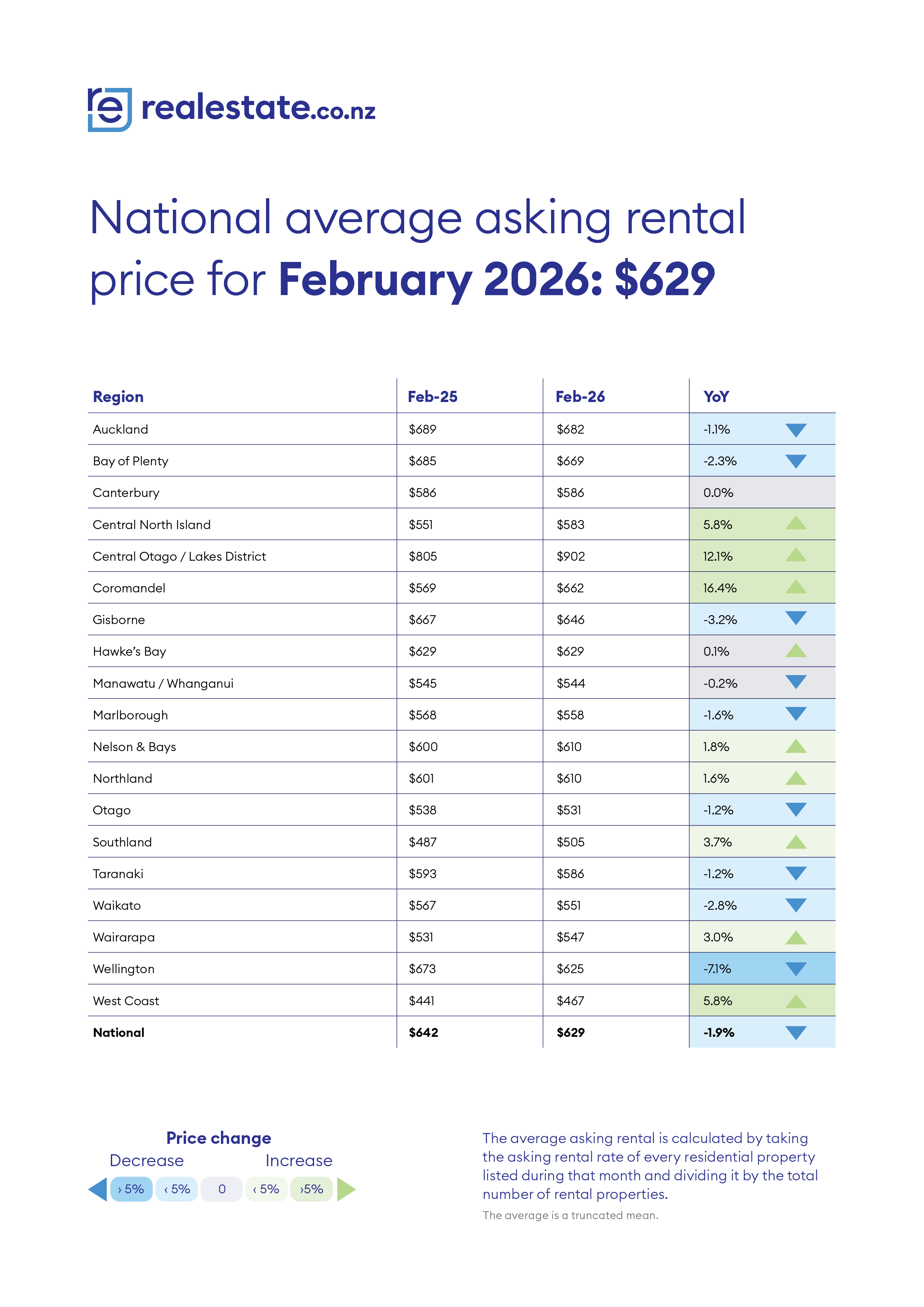

The national average asking rent for properties advertised on the website in February was $629 a week, down from $634 in January and $642 in February last year and $651 in February 2024.

That's a decline of $22 a week over the last two years, which will be good news for renters but will also mean less rental income for landlords.

The biggest decline last month was in the Wellington Region, where the average advertised rent dropped to $625 in February from $659 in January.

The average advertised rent in Wellington was $106 a week lower in February this year than it was two years ago in February 2024.

In Auckland, the country's largest rental market by far, the average advertised rent dropped slightly from $686 in January to $682 in February.

However, the average advertised rent in Auckland was down by $37 a week compared to February 2024.

Notable exceptions to the trend of falling rents were several holiday hotspots, with advertised rents rising in February compared to January in Coromandel, up by $32 a week, Central North Island (which includes Taupo), up by $17 a week and Central Otago up by $76 a week.

However, while rents continue to soften at the national level, the number of properties available to rent is going up.

There were 7504 properties advertised for rent on Realestate.co.nz at the end of February this year, up by 6.2% compared to the same time last year.

That suggests the current softness in the residential rental market will continue as it heads into the autumn season.

The comment stream on this story is now closed.

24 Comments

🥂

Asking prices have to follow yield, rates going up 7-10% everywhere and rents falling.

More rentals offered.

The investment property cohort for sale looks overpriced.

However, the average advertised rent in Auckland was down by $37 a week compared to February 2024.

ouchy ouch.... overhangs and not sold developer houses most probably the cause here.

What is the yield on gold or Bitcoin?

Who lets you borrow money to buy gold or BTC?

As you know assets with lower yield should be cheap, and at no yield need to be financed by the buyer as they are purely speculative play. How ever at the ASB. BNZ, ANZ etc, your loan has to be secured, by what looks like to be a rapidly falling cashflow. Anyway this thread is not about gold or BTC

Probably Nothing.

at 37 a week x 52 = 1924 a year and at 4% implies a drop of 48k on face value.....

nope nothing at all.........

I don't think people understand the impact that higher discount rates have on cash flows and then the resulting impact on the PV of the sum of those cash flows.

3-4 years ago I was pointing out the damage that was done to Bond ETFs because of rising discount rates as the Fed hike rates. They more or less collapsed 50% within months of the hiking cycle getting going.

See the TLT 20 year Treasury Bond ETF

It is still down 50% from its peak. This to me was a warning of what could happen to housing (also valued on the PV of discounted future cash flows - like bonds). And when I ran the cash flows on NZ investment housing using different rates of cash flows and discount rates to determine PV of future cash flows, no matter what I ran, it showed that housing needed to drop 40-50% before it made sense on a cash flow basis (my assumption was that if inflation was running hot requiring higher OCR, then rents would also always be rising in line with that). And that was with only positive growth on rents - never with falling rents (in my mind I never saw a situation where inflation would be >3% but rents were falling - like what we see now). With falling rents the drops in PV of sum of future cash flows would have been a more than 50% drop in prices. They only way to save the housing market from substantial falls in the PV of sum of future CF was for the OCR to drop back down to 0%/mortgages 2-3%.

And what I find interesting is that the PV of the Bond Fund ETF shown above (if you view the graph on max timescale) has return to its pre-GFC value. Which makes sense. The recent inflation and the expectations of future higher discount rates on cash flows because of the loose monetary policy post GFC, has caused the bubble in the Bond fund to pop and return to its baseline level - which makes complete sense. See how it was flat prior to the GFC and then turned into a bubble post GFC - but is now back to the same trading line. From a cash flow and valuation perspective these are the laws of finance playing out just how they should.

In my view, our housing market chart could well look very similar in time to that of the Bond Fund ETF when view in max time scale - its just that their is a time delay as a housing market isn't repriced in months, but years or even decades.

" How ever at the ASB. BNZ, ANZ etc, your loan has to be secured, by what looks like to be a rapidly falling cashflow" - with rapidly falling interest rates too remember.

Are NO I have mentioned it before it's an Adjustable Rate Mortgage situation, everyone expects rates to go up end of year!!!

If you buy now you are at the low, unless real crap happens then the house price will fall as well as interest rates.

You are talking about rents now vs February 2024. So surely you also need to factor in interest rates now vs February 2024. According to AI:

In February 2024, the Reserve Bank of New Zealand (RBNZ) maintained the Official Cash Rate (OCR) at 5.50%. Mortgage rates remained high, with average two-year fixed rates around 7.45% and floating rates around 8.61%

Another argument that doesn't make sense Jimbo.

Completely different asset classes with completely different roles in a persons investment portfolio. Like comparing apples to oranges.

Gold is an inflation hedge - and even though I was on here about 5 years ago telling people it might be a good idea to hold some at that time, I got laughed at by the property obsessed and called a 'gold bug' (and a doom gloom merchant). They told me that housing was the best inflation hedge.

Well in that time I think my gold holdings are up about 400% and housing is up nothing.

When cash flows are positive on housing then it will be a good investment again - but as IT Guy points out - it is not and in my opinion capital values need to drop another 20-30% before it probably does (assuming that 0% OCR isn't coming back anytime soon - and viewing the history of inflationary cycles and interest rates, it is something we may never see again in our lifetimes).

They are all speculative these days. Most people aren't buying gold as an inflation hedge, they are buying it because it is going up in value and they want to make a quick buck. Plenty on this site have said exactly that. Same with Bitcoin, people only want to buy it when it is heading up, they don't actually want it as an inflation hedge.

Housing is the least speculative of those as it also has a yield, but there is still a speculative component, so the yield doesn't have to make sense alone.

And even just assuming the house keeps up with inflation (which it should do in theory) means you get the yield on top of inflation, and the inflation part is currently tax free, which is better than many other investments.

"Housing is the least speculative of those as it also has a yield, but there is still a speculative component, so the yield doesn't have to make sense alone"

100% disagree. Yield is as fundamental to housing as it is to a bond fund. And bond funds are down 50%.

I'm guessing you haven't spent anytime discounting future cash flows to understand what I am talking about (I have a finance degree).

You are arguing along the lines of 'markets can remain irrational longer than you can remain solvent' by Keynes. This is true in the short term, I agree. But in the long term it is a foolish proposition. Its saying that an irrational market will forever be an irrational market. It will not. The market will always return to fundamental prices (based upon cash flows and discount rates) eventually and if you don't see it coming because you believe the irrational market is the 'new normal' (where you can rely only on the irrational behaviour of others that ignore cash flows and discount rates forever into the future), you've become delusional in your thinking and will get caught with your pants down. It is like saying that somebody has invented an anti-gravity device because you saw something go up (and not come down) and believed the sales pitch - gravity will always exist as a timeless principle - just as cash flows and discount rates do. There are no anti-gravity devices and there are no housing markets that will over decades defy the laws of cash flows and discount rates. 40 years of falling rates and rising rents gave spectacular returns (and worked just as you would expect based upon the rules of finance with cash flows and discount rates). The opposite is now happening - falling rents and rising rates. Watch out.

Yield is as fundamental to housing as it is to a bond fund.

Of course. Whether owning property as an investment or for personal shelter.

And the problem is that the financialization of property has unfortunately been interpreted by the sheeple seen as a savings vehicle that is far superior to saving or investing prudently - and why save when the house does it for you? When house prices increase at a rate greater than people's ability to save, this impacts on beliefs, attitudes, and behaviors. Hence, people attached themselves to the urban myths that property is some kind of celestial prophecy.

Rates falling from 20% to 2% has, in my opinion, completely deluded a couple of generations about how finance works. They are lost in recency and confirmation bias, and not the timeless truths and principles of finance.

And recency and confirmation bias can work well in the short term, but can be deadly in the long term, when circumstance change. eg 'house prices double every 10 years'. Absolutely true when mortgage rates are dropping. Absolute myth when they are not. So a truth is only a truth when certain conditions exist. But a fundamental principle is always true, regardless of the changing circumstances. That is why I think 'house prices double every 10 years' is highly misleading.

And in my view, 2021 - 2022 was a turning point in 40 years of financial history (ie the point where interest rates hit a bottom and we now live in a new world which is going to be very different to the last few decades).

Housing prices went up way more than rents / yields for decades.

Until they didn't anymore and at that point many of us said, oh dear, as we knew that the bottom would be when the house prices repriced downwards so that they returned the risk free bank rate + a margin for capital gains, change of zoning subdivision etc

Sadly, we are still a long way above that rate, hence investors keep saying they cannot make the numbers work...

Investment commercial properties are advertised on a cashflow basis, wake up people, what makes a shit box in flat bush so special you do not have to understand cashflows?

Tony refers to these people as professional investors, perhaps compared with average scmhuck's fresh out of the latest property seminar full of FOMO. If you are holding the bag here, it's time to consider you are not as professional as you thought you were.

JJ, You are sounding very, very overweight on property...... and mind captive to the 40 year boom, that ended cold, dead, late 2021.

It like your standing in a rising tide, trying fruitlessly to defend a languishing sand castle.

Most people aren't buying gold as an inflation hedge, they are buying it because it is going up in value and they want to make a quick buck. Plenty on this site have said exactly that. Same with Bitcoin, people only want to buy it when it is heading up, they don't actually want it as an inflation hedge.

Disagree. "Most people" don't own gold or ratty. And "most people" are not traders of gold or ratty.

If the fiat price of gold and BTC are going up because of monetary debasement, then both are arguably inflation hedges.

Ok so if gold / Bitcoin goes down (as has happened many times before), it’s because fiat has increased in value?

The value of currency (fiat) should be determined by its purchasing power over time. Not the fiat price movements of gold and ratty.

If the purchasing power of gold / BTC increases over a time period, we could make the argument that they are inflation hedges. We know that if our time horizon is >4 years, fiat currencies have never "increased in value" relative to those assets.

If gold fell 10% in a day and BTC 20%, that hasn't changed. F'more we know that fiat currency, without gold / BTC as benchmarks, does not increase in value over time.

Or when investors believe the return on bonds is more realistic to actual economic inflation (they will sell gold and buy bonds - so the supply/demand changes for gold - causing the price to drop - you might see this happen again in the next few years if central banks start raising rates again).

As I've been pointing out on other threads, fiat increasing in value is kryptonite to central bankers. Who would possible want the people in society to be able to buy more goods and services with the money they have?

Ponzi bridge is burning down, burning down...

🍿

Yep been burning slowly now for 5 years.

The Gecko called the crash, along with a few other Objective, IT, Average and above Average luminaries did in 2021/2022.

This crash has now, without doubt, had incendiary lighter fuel poured on the NZ Housing crash.

The Fred chart over later 2026, will display the next NZ property downleg, of this epic NZ housing crash, many of us warned the cockahoop spruikers about........

The funny thing is that the spruikers expected us to call the dip bottom, not realizing that the bottom is a hell of a long way off because the game has changed. NZ housing is still so overvalued as an investment class, that there is buy level in sight.

OneWoof is super excited about $5-20million dollar sale's, trust me these are not typical property apprentice buys.

now that 1.6 million sites will be approved by ACC, its shitboxes all the way down.

hint:Manurewa has a long walk to the trains and bugger all buses.

The walk home in the dark in winter will not be inviting.

Moyes car yard will be apartments soon, maybe 10 levels?

I was called by a property agency yesterday asking if I was intending to sell my house. I told them to delete all records of my contact details immediately and I would make a complaint should they ever contact me like that again out of the blue. Seems they are getting excited at any whiff of potential good news.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.