Most of the news around housing affordability revolves around first home buyers, but an often overlooked group are the so-called second rung buyers. These are people who bought their first home several years ago and are now ready to buy their next home, moving onto the second rung of the property ladder.

The latest data suggests they would've received a helping hand. That's because prices at the more affordable end of the market favoured by first home buyers have increased more quickly than prices in the middle of the market, which is where the second rung cohort are likely to be buying their next home.

That would have helped these second rung buyers build up equity in their first home, giving them a bigger deposit to buy into the middle of the market several years down the track.

The currently low interest rates would then help with ongoing mortgage payments.

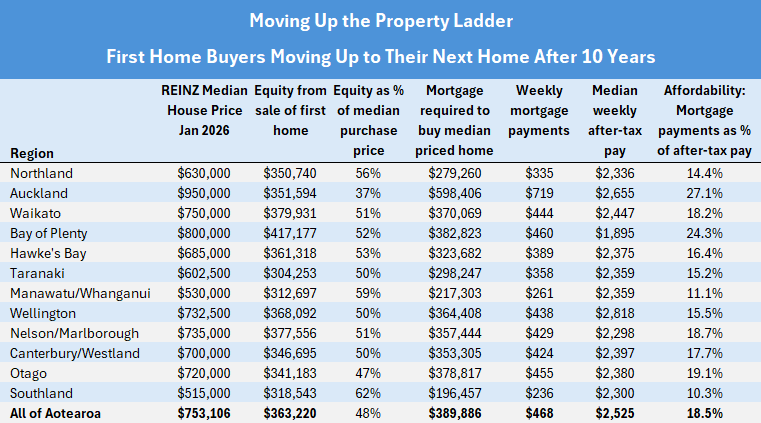

Let's assume a couple bought their first home 10 years ago for $302,500, which was the Real Estate Institute of New Zealand's national lower quartile selling price at the time.

Ten years later and they are ready to move up to something a bit better, so sell their home at the REINZ' s January 2026 lower quartile price of $580,000, up 92% on their original purchase price.

Assuming they had originally purchased that house with a 20% deposit, interest.co.nz estimates they would be left with equity of $363,220 once they repaid what was owning on the mortgage and selling expenses such as agent's commission.

That would give them a 48% deposit on a home purchased at the REINZ's January 2026 median price of $753,106.

That's a pretty good deposit, but of course they would need a mortgage of $389,886 to complete the purchase. Interest.co.nz estimates repayments on a mortgage of that size would be around $468 a week, at 4.74% with a 30 year term.

If the couple were both working full time and earning the median pay rates for 35-39 year olds, they'd be taking home around $2525 a week between them, after tax.

So at current interest rates, the mortgage payments of $468 would eat up just 18.5% of their after-tax pay, putting it well within affordable limits.

Even when allowing for regional differences, moving up to the second rung of the property ladder should be an affordable exercise for people who have owned their first home for a reasonable amount of time.

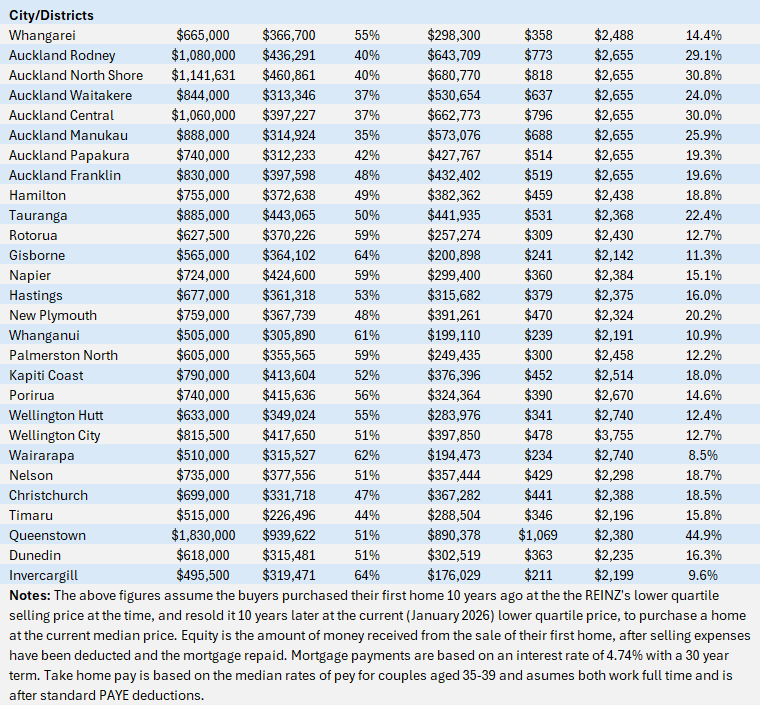

At the regional level, the amount the sale of a first home would provide towards a home purchased at the current median price ranges from 37% in Auckland to 62% in Southland, based on the formula above. See the chart below for the full regional and district figures.

And the amount of after-tax income the payments on the mortgage would eat up would range from 10.3% in Southland to 27.1% in Auckland.

This suggests moving up the property ladder should not only be achievable for most first home owners after they've owned their property for a reasonable amount of time, it should also leave them with some flexibility to manage their finances according to their changing circumstances.

The tables below show the main affordability measures for first home owners looking to move up to their next home after 10 years.

The comment stream on this story is now closed.

24 Comments

Soon the property values will be back to 2015 / 2016 values.........then maybe lower.

Great buying, coming up in 2027 and 2028, for the patient, when yields range 6 to 10%..

Middle and Higher priced homes are languishing on the market, often for hundreds of days - as cost to own these Debt Nooses accelerate.

These higher yields will be required by the market, as all costs to own/service/maintain are skyrocketing!

Simple fact of the income required, to be covering higher and higher costs, including much more expensive debt servicing, that's coming down the pipe! (yes more expensive oil pipe and oil, as we continue our resources war footing and hot war period)

Hard to get 2015 prices when nz still aint built enough houses for 2026

Your joking right??

The is over 50,000 empty houses in just Auckland alone.

There are thousands still being built and still many unsold, for over 1 year.

We have a growing glut.

Nah not at all. Sounds like the lizard is confusing “unoccupied” with “empty”. Ak has about 54,000 unoccupied, but only around 24,000 are classed as empty, the rest are primariky residents away. Not quite the glut the geckos are hoping for...

Some new builds are sitting longer because lending not as loose, and consents been falling. usually means less supply coming not a glut

We are amidst and in a deepening Housing GLUT GLUT GLUT. Like a loose lady loves the fellas!!

However, that does not change the basic equation that we have been building a lot relative to where population growth has been.

Through a static lens, if we assume 2.5 people per home, we needed to build about 50,000 houses. Consents were issued for about 67,600 dwellings. Population growth of 34,700 in the past year divided by 2.5 people per house equals demand for 14,000 houses.

Welcome to an overbuilding phase. That calculation is a simplistic flow measure of housing demand relative to supply and needs to be treated with caution. It’s an indicative snapshot.

Auckland’s population has risen 17,700 in the past year. Building consents for 14,295 dwellings have been issued. That is almost a consent per additional person.

https://businessdesk.co.nz/article/markets/what-soft-housing-demand-signals-is-next-for-nzs-economy

What your stats portray is a Housing GLUT GLUT GLUT. Like far too many seats and stuff all passengers!

Those that need school zones and have secure employment going forward will have to seriously consider moving. Those that don't have either of these keep paying down debt. That will give you far more choices than leveraging up to an inch of you wallet to fund a boomer retirement lifestyle.

Very useful analysis. The issue is the unusual growth in the ten years 'til now. The challenge will be those that bought in the more recent period.

I applaud the fact that we no longer have the 'double in ten years' market. But many will find that the level of debt they currently bear means they are into their 50's before the mortgage becomes manageable. And the house won't have increased in price much above the inflation rate, but they now have roof, windows, kitchen, bathroom that needs upgrades.

The young are going to spend their life paying off the wind-fall gains to my generation, and won't have the luxury of preparing for their own retirement.

Interest rate of 4.74% with a 30 year term.

Is that realistic?

Would more likely be 7.5 to 9% in NZ for 30 years, but no NZ bank wants that long tail risk.

US 30yr mortgages have ranged 6 to 7%recently.......

Which the 30 year term or the interest rate?

30 years puts the average buyer well into their 70s.

Assuming they never increase their repayments with inflation / pay rises / etc.

Who knows what the future holds. Its the first 5 years that really matter, maybe they should have used the 5.29% rate from BNZ.

Something doesn't add up here, average age of a FHB in 2016 was 36, so they are 46 today, or less than 20 years to retirement (ish). Which means kids (if any) leaving home soon so no real reason to upgrade.

[EDIT] Also the narrative works well for pre-covid buyers, the same exercise in 5 years will show a completely different outcome.

Also consider staying on the first rung, pay off your mortgage, after that save or invest, or spend in the real and productive part of the economy.

It feels like property incl. bank lenders are just rent-seeking 50% of everyone's income, forever

Perfect way to stay.

First rungers rule:)

Agree that some people upgrade for little reason. Have seen people take another 600k mortgage to move up a rung when their last place was perfectly adequate. Could have spent that 600k on a life instead.

It didn't use to matter as that extra value was working for you, not so much now.

which "real & productive part of the economy" would that be?

ANYTHING but paying the total wasters and grifters in the FIRE industry !!!

The ladder metaphor is a problematic one

Thanks to the flood of crappy little medium density units built recently in Christchurch there has been another rung added at the bottom of the ladder! My humble abode is now 2nd rung and I didn't have to do a thing :)

The rungs of the ladder have been to far for most people to scale in Auckland for well before covid.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.