Residential property auction activity has softened slightly over the last two weeks, with fewer properties on offer and fewer selling under the hammer.

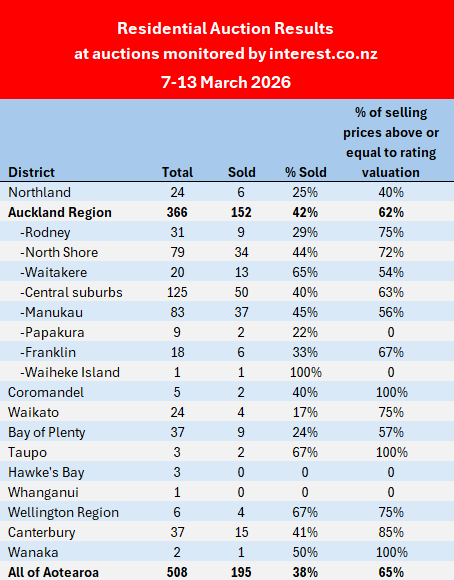

The number of residential auctions monitored by interest.co.nz so far this year peaked at 562 in the last week of February, then dipped to 538 in the first week of March, and dipped again to 508 in the week of 7-13 March.

The number of properties sold under the hammer has followed a similar trajectory, peaking at 219 in the last week of February, and declining to 195 at the latest auctions.

Significantly, the under-the-hammer sales rate has been below 40% for the last four weeks, after starting the year in the 42% to 45% range.

February and March are usually the busiest months of the year for both auctions and residential sales activity generally, so it's too early to say the market has already peaked for the summer season as it could pick up again in the next few weeks.

However, the prevailing mood is one of caution.

This was noted by Real Estate Institute of New Zealand Chief Executive Lizzy Ryley in the REINZ's latest Housing Market Report.

"February's housing market shows patience on both sides, with selective buyers and sellers prepared to wait for the right price," Ryley said.

The latest auction results show many are continuing to wait in March, as they face growing economic and political uncertainties.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

42 Comments

Funny how a 38% auction clearance rate suddenly gets framed as “soft”. In lots of past years the market ticked along just fine in the 30–40 range.

Doesn’t really look like a broken market to me, more like buyers and sellers still negotiating price than the “nobody can sell” narrative you sometimes see.

For peak season selling, this atrocious result list, shows how buggered the market is.

The NZ housing price crash dowwards continue, if prices do not lift a meagre +3.1%, they are losing REAL VALUE!

Losing real value, while topping mortgages by hundreds a week, as the rental earnings are so meagre.

Soon mortgage rates will rise strongly, this shamling zombie dead market will see the next major leg down.

How bad is this as a store of wealth?

So soggy are the bags and the bag holders, investors are better off in super boring TDs!!!

Certainly an increase in stock in the suburbs I follow on trademe.

I'm in a small town in the South Island. Have gone from no listings here to 8 in a couple of weeks. One sold fairly quickly. A couple others have gone from Negotiation to Enquires over $xxx a week after listing. Will be interesting to see how quickly they sell.

Interesting Snowy one.

- Are the sellers mostly the older generations, downsizing or health related??

----------------------------------------

Fun Fact 1:

We have 1 million boomers, who will be selling homes (some with multiples) over the next 10 years, via passing, to fund increased health needs and/or a Rymans holding cage. 500K will pass.

----------------------------------------

Fun Revelation 1:

Warning to recent and current home hoarding Landlords, this obviously does not end swimmingly for investment properties........

Fun fact: Boomers selling houses doesnt remove housing demand though.

Fun fact: Those homes are bought or inherited by the next generation.

Fun fact: The housing stock doesnt disappear just because ownership changes.

Yep. Probably nothing.......:)

This sold 4th march

https://www.bayleys.co.nz/listings/residential/auckland/auckland/2-pemb…

good entry to great school zones for the money

44 properties for sale nearby.....

I went unconditional on a house just outside Christchurch yesterday. This is after seriously looking since mid last year & missing out on a couple. The Christchurch market price for good family homes increased over 5% during that time & some properties sold within a week; however 90% of the 20 or so properties remaining on my watchlist this year have apparently not sold.

Not considered desirable of price not meeting the market?

I suspect that the market has gone very quiet since Christmas. I asked the ? of a couple of RE Agents this week who put it down to all the solicitors going away for January however we have now passed the summer selling season. Definitely seeing more houses move through process from auction & deadline sale to enquiries over & asking prices

Chch has always been 5 years behind the rest of the country not just in realestate.

As fuel driven inflation reaches every corner of the economy, interest rates will be driven upwards to suppress surges in general inflation. Sellers holding on for covid based pricing are likely to be disappointed.

🍿

The last 5 years is starting to remind me of the 1970s...& now the1973 oil crisis

"Between 1974 and 1980, house prices increased 47% in nominal terms, but the high rate of inflation at the time meant, in real terms, they actually fell 38.1%."

https://www.stuff.co.nz/business/money/300621088/susan-edmunds-what-can…

AI:

"Real house prices soared by 60% between 1971 and 1974 due to high immigration and building shortages. This was followed by a 38%–40% crash in real terms from 1975 to 1980, leaving prices by the end of the decade roughly the same as at the start."

Yes correlations are being made.

Excepting we have had a NOMINAL housing price crash since late 2021, here in NZ. Adding on the Real high inflation adjusted price, looks much worse.

Real Residential Property Prices for New Zealand (QNZR628BIS) | FRED | St. Louis Fed

Will we eclipse the Japanese crash?

High oil now (if sustained) will make prices crash further, as mortgages get more expensive and new mortgages get much smaller, as servicing constricts borrowing amounts significantly and bank test rates move up again.

Yes and the difference between the 1970's and now when it comes to house prices is that in the 70's housing started on the baseline that was more of less flat for the previous 100 years (ie prices more or less went up with inflation) and returned back to that baseline with the high inflation that occurred in that decade.

In the mid-90's we departed from that baseline and since then we've seen house prices go up significantly above inflation - which is highly unusual.

Why I've been warning on here for a long time that I thought we were in an asset bubble, in real terms almost certainly, and perhaps in nominal terms.

Where is the real terms baseline for house prices now? Back at 2015 prices, or 2008 prices, or mid 90's prices? I have no idea but that chart shows that we could be in for some extreme volatility in real terms even if it doesn't look like much in nominal terms.

There are so many factors it's impossible to predict. It comes down to affordability of the mortgage. Back in the 70s, most wives stayed at home. Now they are out working full time, meaning a much higher ability to service the mortgage. Interest rates were also in the double digits for a chunk of the time back then which really made it tough to service.

You’re highlighting a factor that has helped push prices up in the past.

If every couple suddenly has two salaries, they compete against other dual income couples. This shifts the floor of the market upward. Dual income has shifted from being a competitive advantage to a baseline requirement regarding property.

Today because dual incomes have pushed prices too high, even a small move in interest rates has a far more devastating impact. Interest rates hit double digits rates in the 70s, because the total prinicipal was much lower relative to wages. The massive principal today creates a high leverage environment. Dual incomes are locked in just to stay afloat.

We can't play the dual income card twice to lift prices. Unless of course, the triad relationship becomes the social norm using triple income households to bid prices up to the next impossible level.

To keep the ponxi fueled perhaps we can allow Polygamy and rebrand and New ZeaUtah. The vested just dont get it. Blinded by greed.

Coupled with longer mortgage terms of 30 years. This and the increase in household income due to both owners having to work is often overlooked when it comes to explaining house price increases and why the same scenario isn't going to keep happening. Unless we figure out how to double our work/lifespan and change our culture regarding shared mortgages.

Exactly, and orange man has just proposed 50 year mortgages. Their next magic trick to keep the bubble inflated

Have dual incomes become a necessity just to keep up with the rises?

Chicken/egg

Not impossible to predict.

May I suggest reading Robert Shillers book 'Irrational Exuberance' and in particular for you, the section on Real Estate.

https://www.paperplus.co.nz/shop/books/non-fiction/business-finance-law…

The signs of a property bubble were all around us in the 2000's and 2010's - like alarms going off saying that we were living in a period off madness that would likely turn into a bust at some point in time. It would appear 2021 - 2022 was the turning point and we may now have years, or even decades of little or no (or even negative) house price growth.

Yeh the 70s example is often misunderstood. Prices still went up about 47% in nominal terms, they just didnt keep up with the very high inflation.

Worth reading the whole section in the article though, as it notes that nobodys house price actually fell during that period

Anyone who bought at the beginning of the 1970s and held through until the early 1980s saw a slight real price gain. Long story short, houses were a good investment though times of high inflation.

However in most recent times Gold has been VERY positive for gains. Better than any other asset, hands down.

That's basically gambling IMO. If you're comfortable with the risks then by all means knock yourself out.

Buying houses with negative cash flow was also gambling, but didn't stop people piling in a few years ago.

The HPI has risen 80% in the last decade, while Gold has risen around 350%. Gold is in the midst of the mother-of-all bubbles and anyone investing in it is gambling - pure and simple.

Comparing NZ house price index to gold is apples to oranges.

HPI is a barometer tied to the local NZ economy, whereas gold is globally priced. A decade ago the NZD hit 0.88 USD. Today you get just 0.58 USD

No it's not like comparing apples with oranges. They are both tangible assets. Regardless of the value of our currency vs the US$, the crazy spike in the gold price in the last few years is totally out of whack with housing. I find it alarming that anyone would think that investing in gold right now is a better alternative to property.

Sure they’re are both tangible, but the yardstick used to measure them has changed. You’re using a faulty yardstick.

I haven’t made any speculative judgement on the price of either in my comment.

OK, then what is a better yardstick?

You need a neutral unit of account that isn't tied to local inflation or currency woes of a single small nation.

Adding to that, we're late in the fiat currency cycle. History shows as confidence in paper money falls due to debt and printing, capital flows towards assets with no counterparty risk. Gold is that global, debt free reserve asset, which you're comparing with a small nation’s local debt leveraged asset.

This is why it’s like comparing apples to oranges

Oh so now we’ve pivoted to gold. Gold aint leveraged and doesnt produce an income, whereas housing typically does both, so its not really comparimg apples with apples

Agree that inflation will cause the NZ economy to tank even more, and with it house prices (note that I believe house prices are influenced by the economy and not vice versa). That is assuming fuel does stay elevated for a while.

Oil is inflationary.

AI is deflationary.

More sellers then buyers is deflationary.

Interest rates are still at emergency lows, trying hard to be inflationary but not really working.

War is very unsettling for all, i suggest it makes everyone pull heads in and sit on hands.

If the equites market falls hard here its an interesting setup to election 26...

I see the NZ Housing market drifting lower over winter and nothing happening until next summer.

The massive glut of unsold new builds (and still building) and the additional 54,000 homes vacant in Auckland, will ensure prices keep on falling:

Auckland Homeowners in CRISIS as 54,000 Empty Homes CRASH Housing Market!

That 54k figure always gets presented as if its 54k abandoned homes, but Ak has about 600k dwellings so thats only 8% unoccupied, which is about right\normal for a functioning housing market.

Stats nz also counts “unoccupied” as anything empty on the day ie/ houses between tenants, recently sold waiting settlement, renovations, new builds not yet occupied, people away etc....

It aint 54k ghost houses sitting empty ya know.

Also if 54k homes were genuinely sitting idle long term then we’d see huge rent collapse not just a dip

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.