Housing values remained flat this summer according to Quotable Value.

New Zealand's average dwelling value was $909,139 at the end of February, barely changed (+0.2%) over the three months from December, and down 0.4% compared to February last year, according to QV's House Price Index.

Around the main cities, changes in average dwelling values over the three months to February ranged from a drop of 1.8% in Nelson and Greymouth to a gain of 2.6% in Dunedin. See the chart below for the full regional figures.

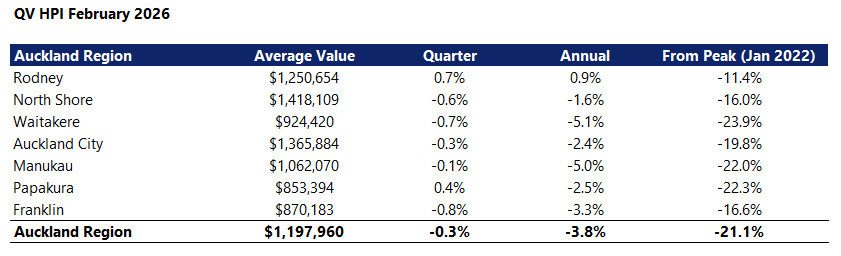

In Auckland the average dwelling value was $1,197,960, down 0.3% over the three months to February, and down 3.8% compared to February last year.

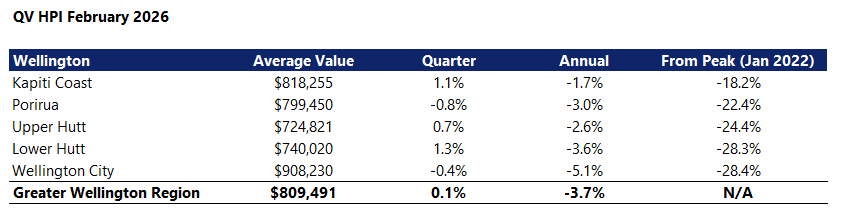

In the Wellington Region the average dwelling value was $809,491, up 0.1% over the three months to the end of February, but down 3.7% compared to February last year.

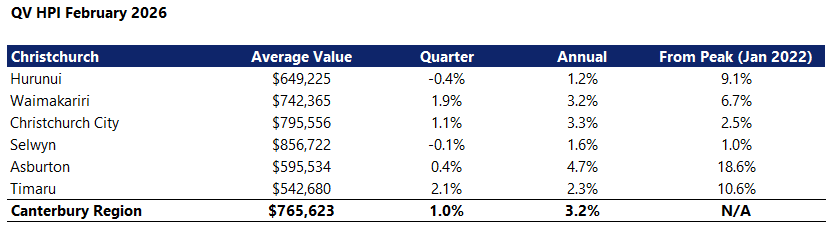

In Canterbury the average dwelling value was $765,623, up 1.0% over the three months to the end of February, and up 3.2% compared to February last year.

QV spokesperson Simon Petersen said this had been one of the housing market's flattest summers in terms of home value growth, even more so than the 0.5% average growth over the same period last year.

"The housing market remains in a state of 'steady as she goes' for now," he said.

"Listing levels and buyer demand are relatively well balanced, helping to keep property values broadly stable for the time being."

"At the same time, global uncertainty and geopolitical tensions mean the outlook remains somewhat murky right now, particularly when it comes to interest rates and inflation."

"The next month or so should paint a clearer picture of what we can expect in 2026," Petersen said.

The comment stream on this article is now closed.

12 Comments

Down 3.8% not flash for NZ largest city

45k loss on average house is making people feel less wealthy and less confident

that’s almost a grand a week, setting up for a sad winter

Agree, but its a pretty sick country when people have become use to " feeling wealthy," because a basic human essential housing becomes ever more expensive. The kiwi has grown lazy by relying on doing nothing to increase wealth. Game over.!

Poor Landlording, free capital gains dreamin/chasing spruiker, cannot get a break!

Values going down or nowhere and rents dropping, must be the worst time in NZs history, to be a rent seeking, tenant leachate, jock strapping, suction cup.

With inflation now amping up on a case of roid rage and mortgages repricing much higher now and over coming months, the new losses coming over winter, will be the stuff of urban legend!

What a time to be alive!! Cheaper homes for the poor FHBs and the lower and lower rents for the Landlorder crushed, downtrodden!

"Cheaper homes for the poor FHBs" - assuming they can pay in cash. If they need a mortgage its just got dearer as interest rates have gone up.

Much lower mortgage $$$ available, It will naturally force the home sales prices much lower.

Good times indeed.

I'm not sure it always works out like that. It was probably cheaper to buy a house at the peak with 2.5% mortgage rates than now.

Then when the ARM mortgages reset to 5, 6, 7%.....disaster for the thousands of teniously financially balanced buyers......

Half the story.

Yes perhaps cheaper from a payment perspective at the start of panic low rates. But then the greed of specu town dived in and drove prices to stupidity. Then it wasn't, and the last suckers are stuck with nil equity and a gigantic death pledge hanging over their heads.

Inflation charging = OCR up and thus payments up. To maintain equilibrium/affordability price must decline, or sit unsold for years. Unsold until the Bank gets offshore shocks sufficent to terminate their debtor scape goats.

Looking off shore How's that global private equity going? Good ol Deutsche Bank is back on the panic radar as well....

I'm pretty sure the articles on here (but happy to be corrected) were showing that FHB share of activity in the market increased, not decreased, as interest rates went up because the deposit hurdle was reduced (and simultaneously less demand from investors as their equity from existing properties was decreasing, not increasing - so less competition for FHB's and smaller deposit required as rates went up).

More spin, this time " steady as she goes" to explain a flat lining or at best afalling housing market. The truth is too hard to publish. Bad data always has to have lipstick put on it.

We hear a great deal about value and asking prices all subjective. How about the actual selling price huh.?

down 3.8% for Auckland, ie prices are falling, funny not one of the bank economists predicted this?

A country of two halves? South Island prices still quietly increasing in a lot (most?) places.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.