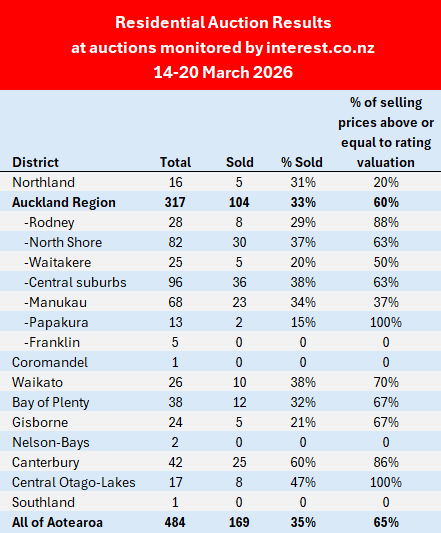

Auction activity continues to decline from its peak, with just a third of the properties on offer selling under the hammer at the latest auctions.

Auction activity appears to have peaked so far this year in the last week of February, when interest co.nz monitored the auctions of 562 residential properties.

That number has steadily declined for the last three weeks, dropping to 484 in the week of 14-20 March.

The number of properties selling under the hammer has followed a similar trend, dropping from 219 in the last week of February to 169 over 14-20 March.

That has pushed the overall sales rate down from 39% to 35% over the same period.

The sales rate has been below 40% for the last five consecutive weeks, after starting this year in the 42% to 45% range.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

35 Comments

Sub 40% clearance....right on cue for the "back to 2015" takes

Markets softer for sure, but we’ve been sitting under 40% for weeks now. As said earlier, I think this is more like price discovery than any massive disaster

Lets see where it ends up.

With the Strait of Hormuz now being truly an Iran - China affair for the foreseeable future, I think you're right about the price discovery

2015 sounds right - just remember that in 2015 the housing market had been looking very much like a Ponzi scheme for a long while already. The 2008 election had already been won on prices being unaffordable

Yes, money did depreciate in the meantime. And so they will in the future, until ships pass in Hormuz at a predictable non-zero cadence

Interesting times, but surely not one to be a buyer if you start looking at the numbers and trends. Not for a long while

Nah not quite, Im not calling 2015 prices

Just saying the current data looks more like ongoing price discovery than any kind of sharp reset

Big difference between a grind lower and a full rewind

Its always a grind lower. Price never drops like shares because sellers would rather eat petfood and default than miss any perceived tax avoided capital gain.

Good that you agree it's free fall out there.

interesting interpretation

“Grind lower” somehow became “free fall”

Just a metaphor for "downwards" ol bean.

Once more global banks drop, and interbank trust craps out, banks in NZ will finally have to start shooting the debt addicts that they have been stringing along. At that point lets see whose metaphor is closer to reality.

Meanwhile 8-9 × earnings price is demanded, with a strong side of debt not supported by income. Classic denial phase activity, which is followed by capitulation.

Ony question is...when.

we lost 3.8% in auckland last year and are on track for another 3.8% this, its 45k a year on average house, that saving of 5k a year in interest on 100k buys you international holiday to fiji every year of the mortgage

Be Slow

Great to see the ridiculous NZ property bubble has burst, and the kiwi obsession with houses and interest rates are turning to a money losing nightmare. Now kiwis will have to try something else other than selling poorly made low quality boxes to each other at ever inflated prices, all the while watching their wealth grow by doing nothing. Game over NZ.

Yeh theres a grain of truth in there but youre assuming that because it was overvalued that it has to crash hard. It doesnt.

So def a shift from the boom years, but so far it looks more like a grind lower/sideways than any kind of messy unwind

and what does that "something else" auctually look like?

20 long year grind, back to 2012 pricing, as interest rates rip towards the 7 to 9% range.

Speculand seeing no cap gains, looking to exit at any price available soon, not a silly idea.

NZ is in Dire Straights.

April not far off and the best month to enjoy with friends and family!!

20 year grind

Back to 2012

7–9% rates

Nice little doom-stack there, miss anything?

Meanwhile we’ve got sub-40% clearance and a slow drift

Doesnt quite line up with the apocalypse....

Its positive as!!!

DTI OF 3 AND 4X. HAPPY DAYS.

Right, so back to 2012/2015 prices first...then “happy days”

Just missing the small detail of how we actually get there from here

I think they meant "2012 prices mean happy days". It's either irony for the sellers or genuine sentiment for the buyers, or both

As for 'how'? Easy: open up any news outlet and then try to answer a simple question: how will VLCC oil tankers resume the 2025 traffic levels in the Strait of Hormuz? Keep in mind insurance is part of the equation. Also that 'asymmetric warfare' means one can achieve a significant result with low investment. I'll wait for a realistic answer...

“Easy” is doing a lot of work there

Thats quite a chain tho, Hormuz -> global shock -> NZ housing back to 2012

Anythings possible sure....just needs everything to line up perfectly

I love how you gloss over history WellyLHB, like all of the '70s

The chain you've identified is more than probable. You forgot to add that the current housing market has divorced from incomes long ago. It's been tethered on belief, in a self sustaining loop for far too long. In any economics dictionary that definition fits squarely in the Ponzi section

So Hormuz too risky to navigate with $300M slow moving football fields -> everyone making a killing out of it and hiking prices through the roofs -> economy in shock -> either import inflation or hike interest rates -> the pile of rubble that this housing market was gets its last kick

I don't see how Hormuz will be solved without Chinese intervention. And that won't come soon

Well calling that “more than probable” is a big step, as there are a lot of assumptions in that path you've painted

I'd have to argue the same for assumptions in relation to your outlook on immigration and the housing market.

Welly-FHB must be getting close to negative equity on his home - otherwise his desperation to talk up the housing market, in probably the worst conditions I can ever remember in my lifetime for housing (prices that is and outlook), seems rather bizarre.

Welly- FHB and the housing market: 'Tis just a scratch' 'Its just a flesh wound'. Armless and legless, but still fighting on.

Not really about personal positions tbh, just discussing the market

I reckon the spruikers can only afford 1 paid up posting account at a time.... right now its welly

even Yvil is off, but sadly he is probably underwater on gold as well as property right now.

Yeh ok fair, Im just not really treating it as a straight line thing tho.

Migration feeds into demand, but how that flows thru to prices is a bit more mixed than that

youre assuming that because it was overvalued that it has to crash hard.

It's not the overvaluation alone, it is the ability for people to access the credit needed to sustain such silly high pricing. A house is worth what someone is willing to pay, and therefore the access to credit was a huge factor in the great 2021 peak. LVR restrictions were removed and at the time my wife and I, on a combined income of around $120k were able, if we wished to, borrow 10x or more of our income which was simply stupid. Naturally we didn't buy then as the prospective interest cost should mortgage interest rates increase (which they did of course) was crippling and unsustainable. We not have DTI limits, downward pressure on wages/salaries and a public who have realised the problem with high prices so they aren't buying.

Yeh totally agree credit matters it played a big role in the peak

But it works both ways. Tighter now sure, but that doesnt mean it stays that way

I think its more like a cycle than a one-way reset

So what changes the path from here, rates, lending conditions, or something else?

There are big cycles and small cycles. Big cycles every 80-100 years. Don't get caught out if this is the end of a big cycle, thinking its just another small cycle (which you suggest it probably is - could be, could not be)..

That is how people went bankrupt 1920's leading into 1930's.

https://finance.yahoo.com/news/ray-dalio-thinks-world-looks-084827810.h…

Well I aint gonna debate Ray Dalio or 100-year cycles....thats a rabbit hole

Having said that tho, sure....maybe. But I’m just not seeing anything in the current data that points to a 1930s style reset

So what are you seeing locally that suggests we’re in that kind of cycle shift then?

The things I say you don't won't to see so you won't see them.

Right, so no actual examples then

All good

I could list many and have over the thousands of comments made on this website the past 10 years. But because they aren't good for the valuation of your Wellington home, you will not see them as valid points. So no matter how many points I make, you will refuse to acknowledge them. Your net worth is dependent upon them not being true.

Well if there are clear local examples, feel free to put a couple of those “many” up

Otherwise it starts to seem a bit hand-wavy

So what changes the path from here, rates, lending conditions, or something else?

That depends if you are wanting a path in a specific direction, or open to interpretation of where the path may lead. If you own investment property you will be skewed to be looking to the positive and finding ways to fit in a future capital gains expectation which is understandable given the vested interest. Not an insult, just observation of those vested in this area.

We have seen cycles due to the way the OCR is set up to work, however it's effectiveness is questionable given the % of population as mortgage holders today vs its inception. We also saw 35 years of lowering real interest rates fom 1990 onwards which inflated asset prices along with immigration.

Personally I see it more likely that some form of external event will cause a further downshift in property prices than not, be it war, longer energy crisis than anticipates squeezing living standards, private credit collapse, loss of faith in AI investment, or any of the aformentioned causing a run on the stock market. Any of these will cause much loss, and force the population to reconsider what wealth means. It will also cause those with means currently, to capitalise and widen the wealth gap unless addressed at a political level.

I also foresee the govt being forced to address pension and healthcare costs via higher taxation - however how the country chooses to deal with this will be key. In addressing these matters we will address the fundamental systemic flaw of assuming population must always increase exponentially and thus will likely impact immigration expectations in future, and thus housing demand.

Ultimately none of this may come true, but my observations tell me at present that self-sufficiency is key, resiliance, community and ideally wealth generation through productive investment.

Nek Minnit

Auction clearance rates dive for the fourth week in a row

It is time to stop using auctions as any meaningful measure as what the market is telling us.

Auctions only work when there are at a minimum two buyers for one property, or the property has gone back to the bank, under which they legally have to take it to auction, or the property is so unique that there are no comparables.

That is, auctions mainly work best in speculative markets where demand exceeds supply.

Where not in that market anymore and if Govt policy works, we won't be in going forward.

And we never use to be 40 years ago when auctions only accounted for a very small % of how properties were marketed.

It was only with policies that caused speculative investment in properties, that we saw the increase in auctions as to the main way to sell property.

Agencies push for the money and ability to force all parties to a comission.

Do you need to sell or not?

NLP just after auction day

Need to sell is $1 reserve.....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.