By Bernard Hickey

The Reserve Bank of New Zealand has again held the Official Cash Rate (OCR) at a record-low 2.5% as expected and has repeated its pledge to keep it there for all of 2013. It now expects to start increasing it from mid 2014 and lift it to around 4.5% by early 2016.

The central bank raised its forecast track for interest rates over the next 3 years by around 50 basis points or 0.5%, pointing to a surge in economic growth and some inflationary pressures from the Christchurch rebuild and Auckland's booming housing market.

It said its 'speed limit' on high Loan to Value Ratio (LVR) mortgages that is due to kick in from October 1 is likely to lower house price inflation by around 2.5% and halve the amount of new high LVR lending. It said this allowed the bank to reduce its projected increase in interest rates by about 30 basis points or 0.3%.

What does this mean for rates?

The Reserve Bank is slightly more concerned about inflation and therefore sees interest rates having to rise slightly faster and higher to keep inflation within its target band of 1-3%. It forecast the 90 day bill rate to rise by around 2% to 4.7% by early 2016, which was about 50 basis points higher than in its June forecast. Economists forecast rates will rise around 2% to 3% through 2014 and 2015.

Floating rates

Advertised floating mortgage rates have been broadly unchanged at around 5.7% since March 2011 and are likely to stay that way until at least early 2014, given the Reserve Bank's comments.

However, borrowers can often get cheaper deals through their brokers because the banks are competing hard for business, particularly for borrowers with more than 20% equity. Banks have increased their low equity premiums for mortgages with less than 20% in recent months.

The Reserve Bank has forecast the 90 day bill rate, which is the basis for floating mortgage rates, will only start rising from mid 2014, and then rise around 2% by early 2016. This suggests a peak for floating rates at around 7.5%.

Fixed rates

Fixed mortgage rates have been rising in recent months and are now at or above floating rates, making the fixed vs floating decision a tough one.

Fixed rates depend more on wholesale interest rate moves rather than the OCR. They also depend on the banks' funding costs on international markets, which have been falling.

The fixed vs floating decision depends on your outlook for the OCR and your personal situation. A flat to falling OCR makes floating more attractive, while a fast rising OCR makes fixing more attractive. Check out our Fixed vs Floating mortgage calculator to get a sense of the costs and scenarios.

In my view, the OCR is flat for now. It may rise next year, but not quickly. That's because the high New Zealand dollar is bearing down on imported inflation and New Zealand's households are very indebted, which means any increase in interest rates is expected to quickly slow activity.

What does this mean for the property market?

The prospect of lower interest rates for longer is encouraging many first home buyers to borrow and buy, particularly in Auckland and Christchurch where migration and a shortage of undamaged and watertight buildings is putting upward pressure on house prices. Some new building has started in Auckland, but remains below expected demand from migrants from overseas and from the rest of New Zealand.

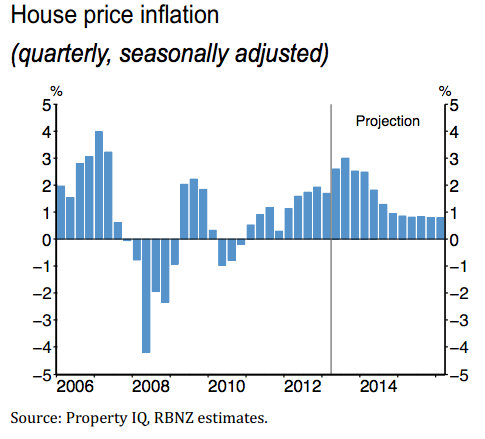

The Reserve Bank forecast annual house price inflation of 11% and 7% nationwide in 2013 and 2014 respectively, but noted it was seeing initial signs its high LVR 'speed limit' was dampening house price inflation.

Elsewhere in New Zealand, where there is more housing supply and less net immigration, house prices are more subdued, although they are heating up as the Auckland and Christchurch inflation spreads.

13 Comments

The House Price Inflation chart included in the article above shows inflation expectations for the whole country.

What it doesn't doesn't show inflation expections for Auckland and Christchurch.

These centres are the drivers that matter and show how misleading generalties can be.

Are there seperate charts for these two cities?

Unlikely, unless Chaston paid for the info:

The REINZ Housing Price Index data is no longer freely available to the public;

For access to historical House Price Index figures, please contact REINZ Business Analyst, David Shaw dshaw@reinz.co.nz. A fee applies for non-members. ($300.00 p.a)

The RBNZ won't be moving the OCR up in the next two years . cause they said that two years prior to now! They are between a rock and a hard place. They lowered the OCR to 60 year record levels to keep the housing bubble afloat which it has. but now cannot lift the OCR without currency traders taking full advantage. Screwed economy either way.

I even predict they will have to lower it further as the growth they highlighted was due to a city's destruction! Apparently national disasters are great economic winner! Broken window fallacy.......

Indeed Justice, the NZD has already climbed dramatically. It is difficult not to predict that without any capital flow controls at all, that capital will flood in as fast as ever. It will look for a home in buying assets, or indebting those locals willing to load up on more debt. Stemming some of these capital flows would seem a high priority, and a good place to start would be stopping Treasury funding offshore, selling any SOEs offshore, and even addressing quasi and local government foreign borrowing.

In the meantime NZbased trading and productive industries will take another hammering; and the excess currency value will be blown offshore. Med cruises seem the channel of choice this year for blowing unearned foreign currency on, all at the cost of future generations.

Indeed Justice, the NZD has already climbed dramatically.

Cmon Stephen L - get real - we are not stupid - has NZD moved significantly up against the AUD? This latest move is primarily a function of a weaker USD.caused by a moderation of Taper expectations.

Stephen,

I actually thought it was a given that the RBNZ would surely know that even hint at earlier and faster interest rate rises, and the NZD will climb significantly, causing all the currency and capital flow damage of which they also are surely aware. Your question suggests you don't agree.

The specific answer according to Oanda.com is that the NZD gained over a cent against the AUD in the day of the RBNZ announcement, from 0.866 to 0.877 now. That seems very significant, and nothing at all to do with any moves in the USD you would think. If I am misreading the actual data, then apologies, but it seems clear enough to me.

This dilemma is the single biggest reason in my view why a single target, single tool RBNZ approach is a disaster for NZ, even though it may suit a populist short term government. Spend up now everyone and damn the future.

Our currency rose overnight too, and is ending the week up 100 bps (sic) on the TWI, following last week's rise of 200 bps (sic) - courtesy of David Chaston

Hyperbole has it's place when witnessed reactions demand it - but when recent NZD currency pair ranges have yet to be broken, I hardly think so.

You might also look a little further afield in your endeavours.

By contrast, AU swap yields dropped sharply after the employment data. AU 2-year swap closed down 8bps at 2.88%. NZ-AU 2-year swap spreads have widened back out to 66bps after falling to as low as 52bps earlier this month. Ultimately we see this spread peaking above 120bps next year, reflecting diverging monetary policy on either side of the Tasman. The market now prices an 80% chance of a further 25bps RBA cut by mid next year. Read more

Stephen,

I guess we all see what we want to see; but your post seems actually to reinforce the point that exchange rates are extremely sensitive to perceived future interest rates changes. If on the same day that the RBNZ has made it clear we are going up hard and fast, the AUD is perceived to be heading south more quickly than previously thought, then I can accept that both facts have likely had a bearing on what was clearly a significant change in one day of over a cent with our main trading partner.

If the OCR needs to go up, and I accept it does for housing bubble reasons in particular, then capital flows need some managing. At the very least let's not kick stupid own goals by selling SOE stuff offshore, or having the government borrow offshore. The commercial banks actually now seem far more nationally responsible, with Westpac's domestic funding news today fairly positive.

They might briefly you know, raise it.....not for long or far IMHO. Dont underestimate human nature and the ingrained and trained focused ability to really get it wrong.

So far though I think our RB head honcho is shaping up very well to the task he faces...

regards

Looks like the Chinese are buying up big in Sydney. Link below:-

Extravaganza - Price no object

[quote]

At a recent property auction in Eastwood, 17 kilometers (11 miles) northwest of Sydney’s city center, all 38 of the registered bidders were Asian. The three-bedroom house with a double lock-up garage and two sun rooms opening on to the back yard, sold for AUD $2.39 million, more than AUD $1 million over the reserve price, after 62 bids from eight of those 38 hopeful buyers

A month ago it was suggested that property prices could be controlled by having a 4 in the street number

puketepapa 20 August 2013

a real lateral-thinking governor would have decreed that forthwith all street numbering throughout the Auckland region will begin at 4000 and continue on up 4001, 4002, 4003 etc

http://www.interest.co.nz/property/65955/rbnz-governor-says-new-lvr-lim…

That it is no longer an obstacle

They are now buying properties then applying to have the number changed - clever

Golden Visa Holder Invests $5 million, then buys house for $8½ million and given approval to change the Street number of the house from 64 to 66

http://smh.domain.com.au/real-estate-news/golden-ticket-holder-snaps-up-85m-vaucluse-designer-home-20130903-2t2nh.html

The Art of Selling Property - change the street number

Here's another one - nothing gets in the way

Agents well versed at such sales are also guiding vendors on how to target that market. A Mosman waterfront home for sale in Julian Street for about $7.5 million used to be number 24 but now has a new street number of 18.

http://smh.domain.com.au/real-estate-news/the-art-of-selling-to-the-chinese

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.