By Greg Ninness

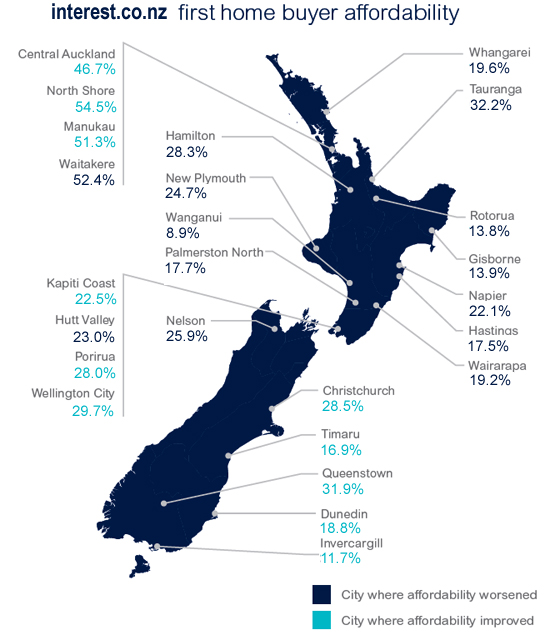

Life became slightly easier for first home buyers in many regions last month thanks to a small drop in the lower quartile selling price and the ongoing slide in mortgage interest rates, according to the Interest.co.nz Home Loan Affordability Report.

The report said the REINZ's national lower quartile selling price dropped back from its all-time high of $309,000 in September to $305,000 in October, with falls occurring in Auckland, Waikato/Bay of Plenty, Taranaki, Canterbury/Westland Central Otago/Lakes and Southland.

The biggest falls were in the two most expensive regions, with the lower quartile price in Auckland dropping back to $611,500 in October from its all-time high of $630,500 in September, and in Central Otago Lakes where it dropped back to $334,400 in October, compared to $368,700 in September and it's all-time high of $403,800 set in June.

However six regions, Northland, Hawkes Bay, Manawatu/Whanganui, Wellington, Nelson/Marlborough and Otago, went against the trend and posted increases in their lower quartile selling prices in October compared to September, and lower quartile prices hit new all-time highs in four of those - Northland, Manawatu/Whanganui, Wellington and Nelson/Marlborough - leaving first home buyers in those regions with little to cheer about.

Mortgage interest rates have also continued to fall, with the average of the two year fixed rates offered by the major banks dropping to 4.84% in October compared to 4.97% in September and 5.95% in October last year.

That combination of falling interest rates and lower prices saw the mortgage payments on a lower quartile-priced home in Auckland drop from $791.12 a week in September to $755.19 in October, providing a saving of $35.93 a week.

Auckland home ownership out of reach for many first home buyers

Unfortunately while the improvement in affordability would be welcome, housing in Auckland is now so expensive that even with the latest fall in prices and interest rates, owning their own home will remain out of reach for many first home buyers.

Housing is considered affordable when the mortgage payments take up no more than 40% of take home pay and the Home Loan Affordability Report estimates that the combined take home pay of a typical first home buying couple in Auckland (both aged 25-29 and working) would be $1529.65 a week, which means mortgage payments of $755.10 a week would consume 49.37% of their take home pay, and that's before adding other property-related expenses such as rates, insurance and maintenance.

That means the lower quartile selling price in Auckland would need to fall about 20% before mortgage payments could be considered affordable for typical first home buyers, even at the current record low interest rates.

However even before they could take on a mortgage to buy a home, one of the biggest hurdles first home buyers in Auckland would have to overcome would be scraping together a deposit.

A $122,300 deposit

A 20% deposit on a lower quartile-priced home in Auckland would be $122,300 and although lower equity loans are available, these usually come with an interest-rate premium, meaning buyers with less than a 20% deposit probably wouldn't be able to take advantage of some of the fiercely competitive specials many banks have been offering, because these are usually reserved for buyers with a deposit of at least 20%.

According to the Home Loan Affordability Report, Auckland remains the only region of the country where housing remains severely unaffordable for first home buyers.

In Wellington where the lower quartile price was $349,600 in October, making it the second most expensive region for first home buyers, they would only need to save $69,920 for a 20% deposit and the mortgage payments of $407.83 a week would take up just 26.04% of a typical first home buying couple's take home pay.

In Canterbury the lower quartile price was $346,000 in October, which would only require $69,320 for a 20% deposit and the mortgage payments would take up 26.6% of a typical first home buying couple's take home pay.

26 Comments

It appears the Government's plan to shift the investors to the regions is paying off. The problem is this is not a positive for anywhere except the major growth areas. The regions with low economic opportunity and activity, and consequential lower wages all have their housing cost rise against a population that isn't seeing an income increase. Thus failure to do anything effective about affordable housing is actually increasing poverty in the regions now as well as the smokes. Despite the screams against it, I am becoming more convinced that the only real solution is regulating a cap on rents. Property investors (Landlords) are predators, preying on the vulnerable and sucking off tax payer funds in the form of accommodation supplements. They are parasites who are trying to get people to believe they are providing a social service, while they have no restrictions on their greed. If John Key won't act decisively, perhaps Andrew Little (Labour), Te Ururoa Flavell (Maori Party) and Winnie (NZ First) will have the courage to step up?

If accommodation supplements just benefit landlords, as a Landlord I am in favor of having them abolished :). Lets try that for a few decades before we try rent caps aye?

That's why National will keep winning. Basically there is a show down between the workers and shirkers. Labour Party (dole bludgers), Maori party (Treaty train) and NZ First (the vampire oldies sucking the young dry) will all see NZ brought to its knees to pay for the bribes needed to keep their voters happy (increased benefits; treaty payments; Super duper gold card).

Communism failed, rewarding the lazy is not the way to make a good society. Try "pulling finger" and earning your house rather than expecting someone else (either a hard working landlord or the Government) to suckle you.

I'm a hard worker that earns a very high income. I wouldn't vote National because I abhor rent seeking ponzi economics. I hope that hasn't left your simplistic world view in tatters.

LOL, agree.

Sadly the Labour party is frankly just as bad just in a different way.

Shifting the problem is not the answer. Addressing the primary causes is.

murray86 you are wrong. There are no vulnerable people living in the quality houses I provide. Instead they are good people working to get ahead.

Landlords are not parasites. Instead, they are 'salt of the earth' people. And far from being greedy, they are all people focussed instead on doing their best to make it easy for people to live in quality homes at the cheapest possible cost to not only the tenant but also the government.

Landlords make a massive contribution to the community and are rewarded fairly for their efforts. Nothing more than that.

You should celebrate their presence in the community. Next time you see one buy him/her a beer and say "thanks for investing in your community, you guys do a swell job."

Better still murray86... become a tenant. Life will be better for you.

All's good in la-la land

LOL....

deluded....

The real reason many people don't become landlords is simply laziness. It's hard work managing and dealing with tenants and property and has significant risks especially these days with p labs capable of destroying places.

If all affordable housing was provided by the government it would end up costing the tax paying far more than what is currently spent on accom supps.

The government is ineffecient and layers upon layers of red tape would make providing social housing a nightmere hence why they dont want to do and can't find anyone who wants to take over from them.

Face it, n.z landlords are essential and govt knows this.

Affordable housing is related to supply, read the demographia studies I've past decade. Rma reform, land freed up for 20 plus years of predicted growth, or best idea ive heard lately is price ratio limits.

From what I have seen this past fortnight at (3) auctions , there is certainly sufficient anecdotal evidence suggesting the Auckland market is very much alive and well.

I am looking for a starter for my daughter , ( she has a healthy deposit in cash ) and nothing has changed at the middle of the market , prices are firm and properties are selling for what I regard as way over value .

And the seller will say they are under value. Strike now or forever watch from the sidelines.

I'm all for encouraging enterprising people to succeed and am an advocate of the free-market - however, when it comes to real estate there is something just inherently distasteful about people associated with the "investment" side of things.

Basically it's totally a mug's game - they'll sit smugly thinking how smart they are but it's ultimately dumb, unsophisticated money with leverage locking young families out of houses then laughing in their face "shame, you missed out". I'll have zero sympathy when the worm turns - sure it might be 5-10 years away but inflation will return, interest rates will rise and then we'll see how smug this lot are.

This is not fostering the society that NZ was built upon - "forever watch from the sidelines" - this is landed-gentry thinking that my great-great grandparents sought to escape. I've been successful and my family is successful but, proudly, none of it was through property "investment".

150 years on and we have a flood of immigrants - coincidentally the johnny-come-lately Poms make up a third of that number and are dragging us back to the landed gentry state of existence they came from and away from what makes this nation great.

Invest in businesses, ideas and people. Not houses.

This country is built on stolen land.

You show your naivety when you state "this is landed-gentry thinking that my great-great grandparents sought to escape". They didn't want to escape it; they sought to emulate it by becoming landed gentry in NZ by stealing it from the Maori and carving it up.

Don't let the truth get in the way of a good story though;)

Rubbish. A few greedy may have, but most kiwis have been content with a roof over the head and a hand up with their neighbours. The paradigm shift where it's all about me is a recent phenomenon.

Yes and no. I think there has always been a % of ppl who have certainly exploited, but yes its definately changed for the worse, both in degree and numbers. Today however I think its "tulip mania" ie ppl madly speculating on capital gains selling to the bigger fool and not 'real" businesses making a good. Sadly real, long term landlords will be getting a bad rap from the way some of the idiots we see here act. On top of that a real landlord is facing a very low return/yield at I think huge risk.

Perfectly said cmat - encapsulates my thoughts and position almost to a word. I despair for what is becoming of our country and the attitudes / goals some aspire too.....and I'm no whinging lefty, I'm a NAT voter and well right of centre BUT more importantly I'm a proud NZ'er who now realises I had a blessed upbringing where everyone we knew at least had a fair crack and wasn't effectively locked out before they started. We did have a near as damn it "meritocracy" ...now a huge divide starting to appear and my children will reap the problems that will come with this....it bothers me.

".......and my children will reap the problems that will come with this....it bothers me" same here but its more than just a "bother" IMHO.

Family in Auckland are saying the opposite to you Boatman. I would not let my daughter buy currently in Auckland as we will not find out what the the government/reserve bank measures achieve for some months. Volume of sales has decreased, listings have increased, less auctions succeeding and prices starting to drop. We know that much. Can we presume you are helping your daughter with a guarantee which in itself masks just how expensive Auckland has become.

Agree. Massive risk to downside and little room to move higher. Safest to watch and wait even if it turns out prices still edging higher, might miss 20k but at least not caught catching a falling knife and seeing all of 100kbplus deposit wiped out in a few months

interesting 70 with a mortgage, I don't quite understand this story, why no reserve? why turn down two good offers? Still sold for 220k above CV not happy,there seems to be more to it that meets the eye.

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11553103

Could this be a highly leveraged property investor trying to knock out his loans in one hit and misjudged the market

Another sign the mood is changing in Auckland and this is just the start. Not a problem as investors don' t mind when their valuations drop.

"Mood is changing" dream on Gordon, the game has changed, this is not a boom this is the new status quo, those with money buy houses, as was said elsewhere we are entering an age where the landed gentry are back and the new rules of the game will ensure it stays that way, if my daughter were old enough i would do her a favour and get her a house now lest she becomes a freemen or worse a villein

Note the Stuff.co.nz article of November 28, pointing out the percentage of people who own their own homes compared with those who rent.

Home ownership rates are "only about 6% lower today, compared with 1966" the article says.

Yet so many on interest.co.nz are telling us investors are blocking home buyers and houses are too expensive.

Yup... the Stuff article is still more evidence that home buying is as accessible and popular as ever.

What is more accessible and popular than ever is to get a huge loan and to work for a bank.

But accessible as in affordable.. no way.

Clearly lots'a people find property affordable and are confident of its future.

That you are not one of 'em indicates you are doing something wrong perhaps?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.