The average asking price of homes in the Bay of Plenty has increased more than those in Auckland over the last 12 months.

According to Trade Me Property, the average asking price of Bay of Plenty homes advertised on the website was $533,600 in May, an increase of $101,250 compared to May last year.

Over the same period, the average asking price of Auckland homes listed for sale on the website increased by a slightly more modest $95,100.

Trade Me's head of property Nigel Jefferies said the Bay of Plenty market had experienced rocket fuelled growth over the last 12 months on the back of explosive growth in Auckland.

"The City of Sails has been propelling the property market forward at real pace for the better part of three years, consistently exceeding $100,000 in year-on-year growth and in the last 12 months average asking prices there have lifted by almost 13%," he said.

"But the Bay of Plenty is fast becoming the new kid on the block, challenging Auckland and clocking up a 23% asking price increase since May last year.

However the market remained patchy around the rest of the country.

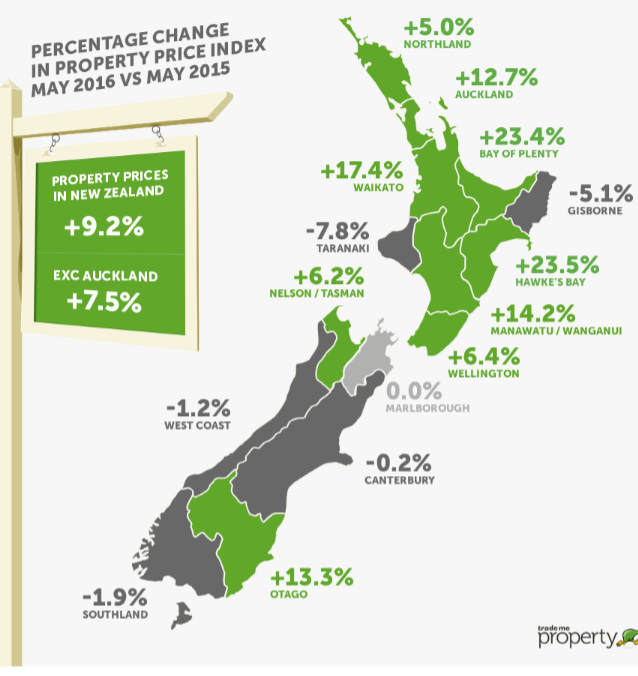

Nationally, the average asking price of homes advertised on the website in May declined by a microscopic 0.1% compared to April.

On an annual basis, average asking prices in May were below where they were a year ago in five regions, while six regions recorded double digit increases for the year (see chart below)

Average asking prices on Trade Me Property May 2016

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

95 Comments

Shame National Party Government for not taking any action. They just Cry Supply supply if this is the only reason for housing problem everyone, are wrong or just hide behind supply excuse as they do not want to take any action. Shame

This a problem which has been in the making for many many years a combination of the RMA, dopey city planners and endless cheap credit. I cannot be corrected over night a perfect storm.

The real news is HB and manawatu joining the party as 'next in line'. Hamilton and tauranga have been double digit for over a year now - now too expensive for most yield seeking investors - hence the money now flows to places like Palmy and HB and by the looks Dunedin.

Otago is more likely due to Queenstown I expect.

That map looks like a virus spreading across NZ - not a good thing at all.

Dunedin property is booming, the place is infested with 'investors' from the north chasing property the great returns there. As for Queenstown, property is booming too. But it's pretty much an independent country and marches to a different drum. I'm never sure what drives it.

Yup. Dunners and Palmy have big uni's which means rents across whole cities get pushed up esp in times of high international student inflows. Great buying in these gems. Interested to see p.n has greater population growth than Dunedin (and HB for that matter). Young city with army base too probably helps the growing demographics there.

Same in Nelson KH. Although it may of slowed alittle from a few months back. Still way over priced IMO

But are these highs prices justified. What I mean is there an economic supply / demand issue or is it "investors" buying property and pushing up prices which aren't justified because the demand isn't there i.e. yields are getting squeezed in the belief that prices will continue to rise. As an example there are 316 houses for rent in Tauranga according to TradeMe and 670 for sale. PN has 120 for rent and 149 for sale (wtf). Dunedin has 762 for rent and 325 for sale (wtf). Something tells me that this doesn't make economic sense. Where is the demand for housing coming from......I don't think it exists (in the regions at least) . I think Auckland "investors " are investing everywhere without understanding the rental markets they are in.

Yes you could well be right. Though I also think that there are probably a glut of people downsizing, trying to get out of Auckland before prices get too high in the regions for them to enjoy a more comfortable retirement.

While there maybe people getting out - I believe Tauranga is one of God's waiting rooms - I don't think it explains all of the price rise and there is no guarantee that the high house prices will remain. If there is a downturn I think it will start in the regions.

Family report unusual number of empty student flats in Dunedin, perfect for sale to Auckland investors.

Lambs to the slaughter....

Welcome, Auckland investor, we offer free coffee..and bluff oysters not cut into small pieces...

Yes p.n market is extremely tight at present with a severe shortage of listings. Always going to translate into higher prices which is what is starting to happen. As prices rise you may see more people thinking about listing, tga getting pricey so more people thinking about selling.

On a per capita basis there are both far fewer houses for either rent or sale in pn than tga or Dunedin. P.n has a similar shortage as Auckland just without the mindless speculation blowing prices up so has been great for investors although I can see price rises in double digits making good yields harder to find.

Oh I think they do understand one thing. That Tenants in these regions are locked in to paying whatever rent increases they demand until something drastic changes. As a collective tenants are powerless at the moment and as more homes are owned buy less people this will continue to be the case. Thus the nationwide demand by investors and speculators will grow until their own finance options run out as they are close to in Auckland. The problem has just been shuffled to everywhere but.....

You make an assumption there is a supply / demand issue - it may not exist.

1000 immigrants moving to manawatu each year for last 3 years. With 150 houses for rent or sale you tell me there isn't a supply-demand issue in pn.

Build costs are the same in pn as in auckland, if all new supply is 500k plus in pn what do you think that's going to do to the limited number of existing houses in pn that are currently selling for 300k on average?

Firstly do you have reliable statistics that support your claim that 1000 immigrants are moving to Manawatu each year ( and PN is not all of Manawatu). TradeMe currently lists 118 properties for rent and 148 for sale in PN, with say an average of 2.7 (which is the NZ average) persons per house that is enough room for about 718.2 people. That does not take into account an expansion of the housing stock.

Just because a new build is 500k , does not mean that a 300k house will increase in value. It depend on the quality of the house, size of the section , neighbourhood etc.

Based on that logic auckland has 11000 empty houses (6500 for rent, 4500 for sale on tm), enough for 30k people. Auckland had 31k migrants net enter in year to April 2016 - therefore NO AUCKLAND SHORTAGE. This is before accounting for the 9k houses built in auckland in those 12 months.

So as you can see, pn shortage at similar level (or much much worse if worked out in % terms shortfall) than auckland for last 12 month period.

Houses for rent and sale is not a good measure of empty houses available to occupy as always a degree of churn in both rental and sale market.

Stats.govt.nz is my source: look at excel file for immigration data to see the 1k net to manawatu and 31k net to auckland.

What I can't get over in the P Nth market is the premium being asked for new builds in Hokowhitu.

Take this one at $620K in Albert Street vs this one for under $350K in Ashurst;

http://www.realestate.co.nz/2824584 (3.7 km to The Square)

vs

http://www.realestate.co.nz/2835671 (14 km to The Square)

Both 3 bed, 2 bath, 2 car garage.

Yeah and 550k ish in kelvin gr which is about the only place you can build new other than on the hill over the river which would likely be expensive builds. You'll probably find developments in places like milson or hokowhitu have rules on what can be built to keep the neighborhood 'of a certain standard'. Still cheap compared to auckland Hamilton or tauranga.

Ashurst is a disconnected 14k away which is actually a long way away in Palmy terms I don't really consider it a pn suburb

Yet for someone from Auckland, Wellington or Christchurch that would be considered an acceptable commute.

Kelvin Grove is 10km from The Square. It's 14km from Riverdale to the Bunnings. 14kms is nothing really, but I agree, folks around here don't think of Ashurst as a suburb. Mind you, as prices get more and more unrealistic closer to the centre, I suspect it will grow in popularity, particularly for new builds. That sort of price differential is pretty compelling.

Under your logic just because there is 1k of new migrants that house prices must increase in price / value - so you can see that the logic doesn't hold up either ( and realestate.co.nz list 200 houses for sale in PN). There are new builds, deaths, internal migration, etc. You still haven't proved a supply / demand issue - you only assume it. Additionally you seem to assume that all the 1k of migrants go to PN.

Checking dwelling consents for Manawatu-Wanganui indicates approx 41 new buildings per month in 2014. At the national average 2.7 persons per house enough housing for 1323 persons.

Pick your time periods why don't ya! Last 12 months 213 consents = about 575 persons housed about half the new migrants and that's without considering natural population growth or internal migration into pn from the large surrounding farming districts as boomers get older. 2014 may have been retirement village from memory..

2014 was the period I came across. All I am saying it is not as simple as you make it out to be. Who are you trying to convince me or yourself.

I've taken a position I obviously own in pn and am still buying there while yields make sense. So always like to listen to people who challenge the positions I've taken to keep me on my toes.

Shame alright. The only certain outcome here is that the nation will end up paying more of its income servicing debt and paying rent. To much apathy and self interest, we have..

Time has come to Name, Shame and Blame whoever is responsible and we have to use all social platform to expose. Even one tweet, facebook, whatsapp, V Chat will go a long way, so act now if want the government to act (May be as are Too Thick Skin)

yes and with more income being spent in housing, little wonder why many retailers are struggling

I'd say it is more/worse than this report.

Since looking to purchase a property in Tauranga from Dec/Jan of this year, homes are easily going for 80-100k more than they were then.

It is depressing, it is difficult. The number of advertised homes in winter is low, competition is still very high and it seems almost each week prices just go up at auction by 10k. Investors are still very much alive in Tauranga. Yields are still here to be had. And I don't think this market is going to pull back any time soon. Come summer, things will take off again. If I do not get in now, I'll be another 100k off the mark.

Nothing I've seen that yields 7% plus. Not going to take on debt for 30 years on an asset returning under 5% .. 30 years is a long time and mortgages long term tend to be around the 7% mark. But speculators view things differently to me..

In Auckland between December / January and Now, prices have gone up by 100000 to 200000. SHAME

BOP and Hawkes Bay up 23% ish not surprised as baby boomers starting to retire somewhere warm, not many keen on up North or Southland. BOP has Fhb,oldies competing,smart investors would of known this years ago.

Not sure why you say the retiring BBs are not keen on the move North - we seem to be getting infested with the buggers here in the BOI. With achieved sale prices in the four Northland districts up 15 to 20% YoY it looks like the Auckland refugees are definitely having an impact.

a lot of born and bred kiwis are leaving Auckland many to try to find the NZ they grew up in, space to do your own thing, a slower pace, and living in communities where everybody knows their neighbor and will help out at a shout.

Yeah this government has made Aucklanders Migrant in their own city to give way for reach immigration.

How one looks at this. Prosperity or Failure of the government.

Government is very proud of this achievement so officially for national party it is prosperity.

It is now upto us the people of NZ to judge National party.

At this stage compare to national party any other party seems like angel.

See how things change with a BIG North Island earthquake.

More people being locked out of the property market in their own town :(

Yawn.. So obvious this was going to happen. Not only is Taruanga a retirement destination for cashed up baby boomers, it's also within driving distance of Auckland so it's an investment target for young kiwis who've been displaced from the Auckland housing market by the Chinese. Not to mention the heavy industry, port of Tauranga, construction boom, beautiful location, hospitals, and relatively metropolitan lifestyle.

Got rent index too Greg? Trademe website still showing April...

Tauranga is having a construction boom, they are converting this demand into value. Meanwhile Auckland is converting its property boom into debt and land speculation.

Wake Up Mr PM before you policies and inaction destroys other cities and comunities the way you have destroyed Auckland.

In Auckland either havemillioners (who have home) or have anguish and frastrated helpless (who do not have house and will never have as cannot dream and hopè also). The damage done to Auckland social fabric is beyond repair. Congratulatio PM.

Isn't this exactly what was wanted? Look at all the RB and Central Government comments from 1-3 years back. Lots of us have been saying for a long time Waikato and BOP are set to go. The only thing that surprises me is that some are surprised by this news.

correct many on here said the cancer will spread to the regions,

True. besides pricing out many First Home Buyers, the danger with the spread to the regions is that there aren't enough jobs there(with the exceptions of some) so the demand there is probably not as long lasting as in Auckland where the fundamentals of house shortages, building constraints, new migrants and jobs, are greater then in the regions. So the rapid price gains in the regions could also mean faster price declines there one day. Anyway, interesting (and worrying) times.

Mystery. Jobs are not great in Auckland actually. You are probably comfortable with Auckland because you are familiar with it. Nothing wrong with that. But the rural areas have great opportunities, possibly more if you are entrepreneurial.

Exactly. Think new jobs are growing at a rate to match immigration into auckland? No chance. The big unmeasured metric is the internal flow of ppl out of auckland into the regions. Only census data picks this up.

I don't understand the big hang up about all this housing chatter as still better to rent in NZ than say living in other places in the world with a no decent health system,no welfare, heavy pollution and over 50 degrees Celcius ie India, Middle East etc or a war zone wake up and have some form of coffee and going on a killing spree.Rent money goes to banks, as does home owners mortgage, only difference is not much stability renting and can't renovate. So my point being is there a people worse off than others some people better off. $ doesn't make me as happy as my wife does.

Your exactly right, its all relative and Kiwi's don't know how lucky they are living in this country. Try a stint in Syria with Russian jets dropping bombs on you every day. Buying a house is hard work and commitment, always has been the way. Sure prices have gone up but the commitment has gone down. You simply need to realize you "Cannot have it all" and these days you need to make hard choices in life.

Labour have a lot to answer for with their RMA, it's cut off land supply everywhere.

that and the fact they only built 8 yes eight new state homes in their last year in government! Also reduced the number of houses under HNZ control in the last three years of government - pretty rich to blame National who have at least supported a growth in the number of properties that HNZ manage

See head down bump's comment above. They are reflective of the frustration that is building in other cities also. Rise of 25% to 30% each year will destroy the economy. Not only first time buyer but also businesses as rent goes up and hard to find good workers as wages does not support rent.

Yes for speculators is Boom Time under current government

ala queenstown, where seasonal workers are struggling to find affordable accommodation.

NZ ski are housing there workers in Cromwell and busing them in daily

http://www.scene.co.nz/ski-workers-to-call-crommers-home/328000a1.page

HaHa BOP have a supply problem

Would not surprise me if the whole thing really started to tank nationwide leading up to the election. More and more people are seeing this sham for what it is. One huge over hyped and over pumped pyramid. Last on the bandwagon will be hit very very hard.

there was a slowdown before the last election, especially when labour was campaigning on CG tax. I would expect a slowdown next year as well until people see which party is in power

A Question. In NZ like in some other countries can a activist or a lawyer file a Public Interest Litigation (Call PIL) against the government. With court action truth comes out and government can be exposed. If yes would be good if some good lawyers does it as here too expensive for an individual.

Would like the government to be exposed. If god ask one boon will not be a house ☺ but the government to be exposed as hate when they come on tv with lie and smirk on their face. How I hate and am sure that so does many Kiwi.

The more the government denies, morewill be the anguish againdt them as never seen in NZ

Evita, it is not you alone but most NewZelenders will like them to be expose as do not like to see that smirk on their face n all rubish statement that they come up. They are so much in power that they do not undertand that their game is up and that people are able to see through their lie.

Even now is not too late as they can still do something but are so full of themself that have doubts.

Sometimes exposing a smirk is not all that bad. And all associated rubbish. When you scratch the surface off a sore, See what comes out. Watch those who scurry for cover.

Bay of Plenty new kid on the block is it? A nice lifestlye used to be had in BOP. Fishing, hunting nice beaches. Now it's full of bleeding immigrants wanting a free ride cause their own homeland is pigsty. Well one message. F.O.W.F.

Why do so many people want to see a house price correction? Because they want to buy a house. See the problem?

It's not a question of wanting to buy a house - it becomes a question of financial stability. As the ability of people to buy or rent a house becomes more unaffordable the risk to the economy increases. All the actions by the banks (private and RBNZ) in the last few days have been about risk - real or perceived. The actions by the banks may reflect what has happened in Australia - but the consequences could very well be felt by both Australia and New Zealand e.g. if there is a housing correction in Australia and bad debts increase the banks may increase interest rates to cover those losses and New Zealand will pay as well

A great majority Zac are not buying a....house (home). A great majority are buying to flick off in very short time frames for profit, hoard, or hide cash.

No one wants an asset of any kind knowing you are buying into that asset class which is most definitely 50% over valued. Hence the 10-11 times incomes to fund, rather than the 3-5 times annual incomes which is the more sustainable and economic modeling norm.

And no one knows when the party will end...

When the savers have had enough? You think? And stop funding the profligate losers perhaps?

Savers will lose also because they are stupid enough to trust a bank.

Where you got your savings Moa? Hoarding cash at home can be risky also due to the questions (audit+ police investigation)asked IF you ever want to deposit again. Savers need to diversify their investments as much as possible but it can be very difficult to do if wanting/ needing immediate access to those funds.

Banks are good at somethings. Securing Cash is one of those. It is when banks get too big for their boots, i.e. thinking depositors funds are an bottomless pit, and treat depositors with disdain whilst lending out said depositors funds and getting it all wrong. Then banks run off to the Govt, and say,

-Sorry we are poor, Mr Govt, what can you do about it for me.

Govt panics, it has voters to think about after all, and voters live in houses.

Connect the dots.

Govt says well lets print some more money or let some more foreigners in to buy the existing houses.

Then everyone feels better off. For a while

Reality may hit at some point.

Any binge has a hangover.

To a degree JK is right in calling it symbolic but at the same time he is being disingenuous. The banks are recognising that that there is a risk and they are seeking to minimize that risk.

I tend to agree. For once banks seem to be reigning things in before the peak rather than just after. With the massive supply problem in Auckland I don't think prices are going to roll over until next year at the earliest. That doesn't mean there won't be a correction in due course....hopefully.

Great news

Goverment takes relief with the thought that only a tiny fraction will be effected (even we know) but It goes on to show their mindset. It is a relief for them that majority of the overseas buyer will not be effected.

Again they say that data shows only 3% overseas buyer but the agency has admited that data is faulty as have not taken into account students and other short term visa holders.

Even today after so much media coverage n even bank accepting that demand is the reason- still government in denial.

Today I am sure of one thing that govt will not take any meaningful step to put break on speculation. The only hope is if it happens by itself for reasons nothing to do with govt.

Property agents that I met today are confident that as long as John Key is PM the housing buble will continue and by chanse is next term also elected than Auckland wiĺ be neari g 2 million mark,

In the modern world with QE cannot use old income multipliers. What happens to property prices it mortgage rates are sub 3%, and term deposits pay 0.25%? What happens if influx of refugees destabilises Europe and white flight from UK/ continental Europe accelerates? What happens if USA slips into recession, and QE opens up even more, forcing negative yields on govt bonds in USA as well as Japan and continental Europe? What happens if a 2% net yield is considered a good return as banks have excess funds from worldwide QE and term deposits have a negative rate. Many have not adjusted to the new paradigm, they think interest rates have to rise, from where I'm sitting they are more likely to fall, as a recession equals QE, and these excess funds increase demand for bonds forcing down interest rates.

Exactly. Close to inverted US yield curve so rates to head lower and stay low for a very long time.

What happens to 7% yielding property? Money flows to it until price bid up such that yields fall to 4% or less (this would mean a close to doubling of price)..

What happens mja is, because of the low yields, a multitude of global institutions such as pension, insurance funds, many of whom have defined benefit schemes, will go broke and/or have to be bailed out by Govt/taxpayers through more borrowing when most countries are up to their eye balls in it already, or through QE - if you actually look wider at the total picture you'll realise that the current level of interest rates globally (500 plus years historic lows) is not sustainable for an extended period, and we're already approaching that period.

So that provides the answer to property prices, they won't be sustained and all the apologists claiming "this time is different" is biggest signal yet that this is the case, Yes it will be painful, indeed insufferable, but that's what crisis are all about - we've had them before and we're going to have another at some point because QE to infinity has never occurred without one, just no idea when - just keep spinning the chamber and pulling the trigger.

If pension funds and insurance funds go under, and require government bail outs this will in most cases lead to more QE that will force interest rates lower. If pension funds go under, I would say the average investor would be inclined to purchase bricks and mortar, rather than place funds with a financial institution. Grant A why are the current level of interest rates unsustainable?. Studies have shown that high debt to income ratios lead to lower interest rates going forward, as if reserve bank ups rates, country dips into recession due to debt load, and the reserve bank is forced to cut rates. You need to examine your assumptions, or you may find yourself on the wrong side of the ledger regarding investments going forward.

If a pension fund goes under then the average investor has no control. The investor gets a statement in the mail that says, sorry Pension fund got it wrong. Well what can pensioner do?, What can the investor in the pension fund to do? Nada. They are on the the bottom rungs of the ladder. Brown stuff flows downhill. Until you get a bigger ladder.

My point was with future money and other funds, in the scenario of failing pension funds, these funds would be more likely to flow into property. With property you aren't going to get a statement in the mail stating your property has evaporated into thin air. Over the last 10-15 years I have advised colleagues (worked in Aus) to ensure have significant amount of self managed super in well located residential property in major centres. Advised that if can live well off net rent on say 3 residential properties, you can be fairly sure that in 2050, these properties will afford similar lifestyle as rent will adjust to inflation. Would you back funds in a managed fund or share index to be around in 2050 let alone generating a good standard of living. This is what mainstream living in the 1990s investors/ advisors have not adjusted to. 2020 retirees may very well be alive in 2050 or 2060 and they would rather get a net 2-3% from a well located property than trust their life savings to a financial institution. Because once you retire if that asset base is lost there are no second chances other than a lotto ticket.

Ticket Clippers, associated fund mangers et al don't like it when their own ticket is clipped.

Property ownership in NZ is like a drug. An easy way out.

Sell the country to the latest import off the boat.

Then what's left? Not much of New Zealand.

Just a pile of steaming brown stuff. Look at Europe.

They say in finacial world that when everyone and everytime is talking about share is the time to get out of it and have experience it twice. Similar is with property market. Day in and day out everyone including media is talking about it. It is also true that in history no where we have seen one way up or down. It is a matter of When and not if.

The main reason of it not going burst now is government inaction and would have happened without govt inaction as it just need one trigger and will fall like pack of cards and many have entered into it beyond their means and worst to be affected are late entrants that is now - who will be worst hit.

With current govt it has to be seen that for how long will they be able to manipulate / hide thr overseas data to help and protect their new chinese friends.

Truth cannot be hidden for long even that is universal truth. National boses be aware.

It's a wave. UK,Spain,US all been through it. Property Mania. It didn't work out well.

Tin hat time, this bubble won't be sustained.

Otterwood

The press and Twitter are full of supposed reasons why yields continue to plummet. I believe the aggressive QE programs by Europe and Japan are distorting bond markets, limiting supply of tradable bonds and in doing so driving down yields (prices up). See the chart below from BAML on how many bonds are now sporting a negative yield. Fitch says it's even higher.

In essence, the aggressive QE programs of the ECB and BOJ are killing banks which impacts their lending behaviour and slows global growth which hits yields. Commerzbank is considering storing billions of Euros in physical cash instead of paying the penalty on funds (essentially negative rates) held at the ECB. This would be one of the strongest protests against the ECB's ultra-low rates, can you blame them?

The BOJ is widely expected to push further into negative rates when they meet next week and even increase their already insanely massive QE program.

Negative rates are an absurd concept. Paying someone to borrow your money is not how banks or the global banking system are set up to operate. The rate at which yields are falling cannot solely be blamed on the onslaught of buyers, if that were the case the U.S. Dollar would be much higher than it is today. I believe growth will continue to slump in the months ahead. A banking accident to an entity like Deutschebank in Germany cannot be ruled out. We will remain alert.

When people have such little faith in any store of value they will pay money just to ensure principle remains largely intact - that's what's behind negative rates.

Who thinks negative rates makes your deposit safe? A great way to create speculation and asset bubbles.

Who would lend at ZIRP if there is any risk, hence the deleveraging and liquidity problems we are facing today.

Who thinks negative rates makes your deposit safe? A great way to create speculation and asset bubbles.

Who would lend at ZIRP if there is any risk, hence the deleveraging and liquidity problems we are facing today.

Exactly.

Low interest rates are not the mark of further “stimulus”, they are the bright shining light of complete, continuing failure; financial, meaning “dollar” and wholesale, as well as the related global slowdown undeterred by any central bank’s overestimation of itself.

At the margins, then, the BoJ is only transacting at the price which mostly secondary market participants would be willing to give up their JGB’s. It is quite reasonable to assume that if the world were looking much better, as it did between January 2015 and that July, JGB sellers would take a relatively lower price at each transaction iteration. Conversely, if the world were looking much worse, JGB sellers would “need” greater premiums in order to part with the perceived safety of these sovereigns. The focus on quantity of Japanese bank holdings is misplaced or at least inappropriately over-emphasized in the context of price. Read more

Safety is a relative concept. The interest rate doesn't set the safety level but it's a responsive indicator as to how safe the market sees it.

Interest rates, once introduced, are a mathematically certain to drop over time. The only uncertainly is how long it takes, and the peaks and troughs in between.

"Live within your means" used to be an adage.

National saying that the 'market' will solve it, assumes the market is 'Moral', and parties won't be trying to make big profits. But the market is a business, and business aren't always moral. eg companies that go out of their way to pay the fair tax rate for the area they are trading in.

Really the only answer in terms of the supply problem at the moment, is for the government to start building a huge number of houses, and force these onto land that the council has yet to release. Even build them on a golf course. The at some stage supply will exceed demand. But property developers, many who are National voters don't ant this, so I doubt it will happen beyond the token number currently being built. Also cutting immigration may help, as NZ is becoming full of low skilled people who haven't been through our education system.

Then you have problems with monopoly/duopolies in the building materials market, meaning NZers pay a lot more for building. Overseas buyers being able to buy existing housing stock. (Around 10% of Queenstown houses are supposedly owned by overseas owners). Cheap credit, meaning people can afford to pay more etc,. it is a perfect storm, but i won't last forever as these thing go in cycles.

All experts, professional whose articles are published in media and are interviewed on TV shouls stand up and try to expose the national government who were crying supply supply and now that farce has been exposed ( supply is very important but not the only solution n much is need of tge time on demandvsise) they sre not even talking about housing bubble but we the peopke with help from media and sll experts should bringbthe truth out.

Not even one person i have talked believes the overseas data to be correct but the govt. Noone believes that housing is more affordable than 2008 except the govetnment AND everyone beliefes that yhrir is a housing crisis but not the government.

WHY ?

Simple as govt does not want to act to curb speculators and specially sensetive about overeeas buyers WHY ?

Vested hidden interest.

To start with can essily apply stamp duty for non residence as in many country and can also put redtriction on ovrrseas buyer that can only buy land n build house as a result supply too will be taken care of. Can also allow migration to NZ with condition cannot stay in Auckland for 3 years as it happens in other country as a result ooth area will also get developed and less burden on Auvkland. This are only few but so muvh can be done where their is a will - which unfortunstely is lacking in nationsl but in fact adding fuel to fire.

Similary RBNZ is worried so why not act now and say that we will in future. Why wait srecwe waiting for finances to go beyond before acting. If govt is not acting stleast RBNZ should act and do their part.

Very shameful that no one is taking any intiative to act.

But the Govt will have some say in the appointment of those acting on behalf of the RBNZ . After all, the RBNZ is 100% owned by the NZ Government.

Correct Evita. No will on the part of national and all media and experts are too soft to expose their bluff. May be an article here and their thats it. In NZ hard journalusm is missing where they pik up national issue and ask tough question to govt till get a satisfactory reply or make the govt realise their failure. Being voice and raising concern of people is missing by the media and so called experts,which is very important in democracy.

http://www.nbr.co.nz/article/book-extract-home-truths-–-confronting-new-zealand’s-housing-crisis-183320

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.