Housing is driving inequality in New Zealand, a new report by the New Zealand Initiative has concluded.

The think tank has found that with income and consumption inequality remaining broadly unchanged over the past 20 years, sky-rocketing housing costs are what's boosting inequality in New Zealand.

“Inequality is a very real issue and we seem to be missing the point in New Zealand,” says the institute’s executive director Oliver Hartwich.

“Imported narratives from overseas about ever-increasing income inequality and CEO salaries are not the issue here. New Zealand’s real issues with inequality are being driven by housing.

“Rising house prices have made homeowners richer while those in poorer socioeconomic groups are having to pay an increasing share of their income on housing. This is causing real hardship for too many New Zealanders.

“We feel strongly that a modern society and affordable housing do not have to be mutually exclusive, as long as the Government is willing to act.”

The authors of the NZ Initiative report, ‘The Inequality Paradox Why inequality matters even though it has barely changed,’ Bryce Wilkinson and Jenesa Jeram, argue undue attention and resources have been placed on income inequality, which has distracted us from the real issue. They say:

It is difficult to make sense of the increasing public concern with inequality if we look only to income or wealth statistics. But, there is a massive inequality concern that is rightly troubling many New Zealanders: housing.

In short, New Zealand’s ‘inequality crisis’ is really a housing crisis

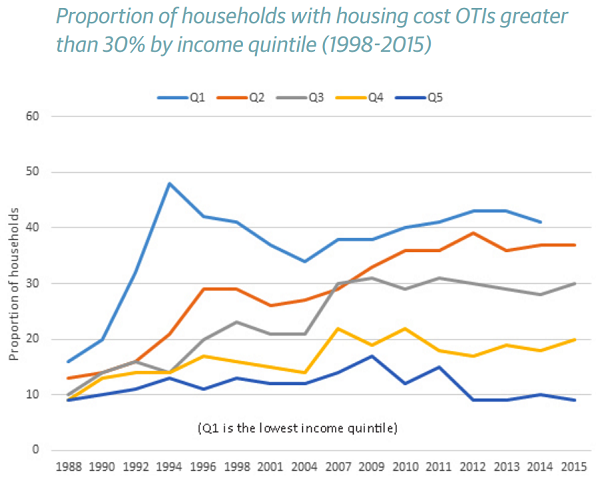

Inequality after housing costs is significantly higher than before housing costs. While incomes have risen for high and low earners, the rising cost of housing especially hits the poor.

The graph below shows the differential effect of rising housing outgoing-to-income ratios (OTIs) across income quintiles (where quintile 1 is poorest and 5 is richest). The proportion of households with OTIs greater than 30% rose markedly between 1998 and 2015 for each of the bottom three quintiles. In contrast, it was the same in 2015 as in 1998 for the top quintile.

Ongoing well-informed public debate about economic inequality and its sources is important. If, as our research indicates, rising housing inequality is of particular concern, then policies to address inequality in society should address the housing market. Less restrictive housing policies could reduce hardship and economic inequality.

Myths about inequality and the misperceptions in the public debate need to be challenged more. Some of the New Zealand narratives on inequality may have been imported from overseas without sufficient critical consideration. Inequality trends here simply do not mirror what is happening abroad. What should be of concern is barriers to mobility: what is unduly stopping people from getting ahead in life?

Misperceptions about inequality in New Zealand could lead to growth-reducing policies that will make people worse off, regardless of their effects on measured inequality. There should be ample scope for policies that lift earned incomes both on average (i.e. economic growth) and in the bottom quintile of the income distribution.

At the same time, it is important that differences in income and wealth are fairly earned – and perceived to be so. Social cohesion can be corroded by poor policies that create undue barriers to education or jobs, or that allow high incomes to be earned through privilege rather than merit or effort. Thus there should be a strong presumption against corporate welfare.

This report is the second of three reports. The first report was Poorly Understood: The State of Poverty in New Zealand. It argued that issues of hardship were more important than issues of inequality, or low relative income. The third report, to be released in 2017, will examine welfare policy issues.

75 Comments

A very narrow view of the cause of what is a global trend of the 1%'s significantly increased wealth at the expense of the middle class. The central banks of the world ie China, USA, Japan, Europe, UK have massively increased global liquidity by their money printing or QE as it is misleadingly called. This liquidity has gone into all sorts of asset classes, one of which is housing. This liquidity has however also flowed into fine art, antiques, diamonds, classic cars, stocks etc which are now all in bubble territory. Bubbles always pop and this will result in a massive transfer of wealth. It is not a matter of if but when. NZ is just following all the current global trends.

It's all about crushing the middle class and making them lower class so money can be made off their borrowing.

Haha. Cry me a river.

The lower class isn't the source of consumption. It is the middle class; it always has been, and always will be. As such, this is why we see the overwhelming majority of policy designed for enriching the middle class. There is no agenda to hurt the middle class.

If any of the overlord Illuminati agenda setters that you believe exist, existed, the one thing they would be ensuring is that as many people were in the middle class as was technically possible.

You seem rather out of touch. The most money in the financial sector is from the lower class and the wealthy. Wage and salary stagnation is diminishing the middle class so their ability to consume is increasingly impaired.

Also why would I cry a river? I don't give a shit what happens to the middle class in New Zealand. They keep voting for National without realising that it's not in their best interest.

Shame and support #National party

Agree apart from the "this will result in a massive transfer of wealth"...

The wealth is really illusionary. If you look at it logically the banks must keep the money creation Ponzi creating money and the reason all this new money is being funneled to the top is because the energy to exploit resources to create further value is actually entirely limited.

So the money has to be sequestered where it isn't actually spent ... ie in asset prices and art etc.

The big problem from the central banks viewpoint is that this doesnt lift commodity prices which are consumed by the masses... insolvent commodity producers spell trouble.

One piece of research I read suggested that one driver of inequality is the difference between those that invest and those that do not. Invested capital usually generates a return and accumulates more capital. Wealth may be part illusion but capital accumulation is real even if it cannot be accurately valued.

Wrong. And misleading. Perhaps purposefully so i can not say.

Everyone ignores it, pretends it is not the issue or misleads people away but the reason is blindingly obvious.

NZ is adding the equivalent of a city of Christchurch in population to the country every 5 years.

The rate of housing development is woefully behind the rate of population growth for various reasons ranging from stupidity to greed.

Those 90,000 people a year have to live somewhere - either rent or buy.

Because there's not enough houses and because it's a trapped renter/buyer market those with money to "invest" buy properties and rent them out knowing that while the population continues to increase the property prices will continue to go up even if rentals and low interest rates do not, or only just, cover the cost to invest.

The people making policy are the very same people buying the investment properties - so they are never going to do anything to spoil their party.

Yes, some of those coming in are buying - some are Chinese with assistance from family in China or here or willing Chinese banks but there's plenty of others coming in with money or they don't and they share rentals squeezing 2 or 3 families into a 3 bedroom house.

To make it even worse, the high numbers of people here and coming here on work visas must also be housed - and that pushes up prices too as they compete with immigrants.

It's the middle class - the baby boomers - those in their late 50s and early 60s who are doing most of the speculative buying

and it will never crash - as much as lots of people predict or hope - because all that is needed to to carefully adjust the rate of immigration so that there is always more people needing housing.

If immigration stopped tomorrow? You'd have prices stabilize until the number of houses/apartments meets the needs of existing population and if it stayed zero you'd see prices fall as the baby boomers start to die off or use their equity to fund their old age.

If boh immigration stopped and interest rates went up? You'd still not see a crash - it would be a gradual decline as long as the demand outstripped the supply - unless of course the banks all freaked out and pushed interest rates up where we had them in Paul Volker's day. Then we'd see a crash in prices maybe.

None of it will happen - the very people who are making a profit out of it all are also controlling policy and as long as the continue to do so it will exacerbate the problem until we reach a point where it will be impossible for those in the lower earning group to ever have enough political voice/power to effect change.

You do realise that that ever increasing population must be supported by ever increasing NET energy? ...

https://s18.postimg.org/pai8rq6p5/Graph.png

{kind=link}

I seem to always miss how your comments on net energy relate to the arguments in which you present them..

surely quite obvious ... if its never going to crash (as suggested by commentor above), then the system requires ever increasing population growth, which requires ever increasing NET energy from somewhere. The NET is the important bit - no good spending a barrel of Oil to get a barrel of Oil.

if only Gravitational Fusion (aka Thermonuclear Fusion by way of Gravitational Confinement) were possible, all our woes would be solved. It is possible you say?

If only we had a nearby fuel supply that we could use with Gravitational Fusion, all our woes would be solved. We do you say?

If only it didn't cost as much energy to run as it produced, all our woes would be solved. It doesn't you say?

Have you by any chance heard of a little star that some people know as the Sun which has the potential to supply us with a little bit of energy should we require it?

What about Gravity wells? If only we had an astral body nearby with sufficient gravitation to be used as a gravity well..... Anyone here heard of the earth/moon?

You might want to go back to the graph link I posted and remove the FOSSILISED sunlight fuel sources ... ie the coal, Oil, biofuel, natural gas ... then see how much (very diffuse) energy you get from your little star on an ongoing basis

1.367kW per square meter of atmosphere (there are 120 trillion square meters in our atmosphere) every hour.

https://solarpowerrocks.com/solar-basics/3-reasons-the-sun/

Yes. We are also going to require more toilet paper, dishwashing liquid, and televisions.

My point being that it is quite abstract to the key argument put forward b the OP.

This reads like a first year economics essay.

It gets the main gist of it, but is plagued by profound whimsy and ultimately comes to a dubious conclusion.

You are deluded. Tell me what do you think will happen if interest rates rise 1-2%. People buying in Auckland based purely on capital gains getting 2-3% return will default their mortgages, there will be a splurge of properties come onto the market as owners cant afford to finance their mortgages/speculators get out of the market (this could be in 1-2 years time once owners fixed mortgages come up again). People like you sound dumb, make me shake my head, and have the memory of a goldfish.

how on earth will interest rates rise without crashing the entire system?

When has an economist ever been correct? Interest rates are at historic lows. ALL markets go in cycles. Watch and learn over the next year or two how quickly things can 'unpredictably' change.

Do you have any empirical evidence that "all markets go in cycles"? Just asking.

History says yes. So with history as my witness yes i do. Do some research and you might be surprised by what you can learn.

I asked about empirical evidence. But if you say that history is evidence of "asset cycles", what is or are the main frameworks that you use?

All empirical evidence is based on actual events ie. history.....??? Thats like me asking you "What is your position on the role of government in supporting innovation in the field of biotechnology?"

Do you want to re-read that comment? Particularly "All empirical evidence is based on actual events ie. history.....???"

Unless I just didn't pick up on sarcasm..

There is a plethora of literature explaining the dynamics of asset prices during boom bust cycles and why they arise.

Some things you will never understand.

Luckily I understand what "empirical evidence" refers to..

I shouldnt even need to do this but here is a defintion for you nabbed off the internet... "The central theme in scientific method is that all evidence must be empirical which means it is based on evidence. In scientific method the word "empirical" refers to the use of working hypothesis that can be tested using observation and experiment. Empirical data is produced by experiment and observation." How any 'evidence' you speak of cannot be based upon something that has already happened ie in the past ie history is crazy. You are crazy haha.

Okay, we are on the same page then.

Your poor usage of grammar threw me off.

So I guess Japan can expect an almighty boom in house prices and stock prices based on "the cycle".

So I guess Japan can expect an almighty boom in house prices and stock prices based on "the cycle".

If it had the correct conditions, yes.

That whole population decline thing would sort of preclude it, though. That sort of ruins the whole forward expectations of positive growth thing.

OK, so "the cycle" only applies to NZ and Australia? What are the "correct conditions"? Is this an Anglo Saxon thing?

RE; "When has an economist ever been correct?"

I love it when people answer their own questions.

I don't know too many economists that disagree that the boom-bust trend doesn't exist in many markets.

Is boom-bust related to asset cycles? Empirical evidence is related to observation, but if there are cycles that apply to asset markets, what are the driving theories that have been proven over time?

History is a poor indicator of the future when the event of peak oil is only happening once and now. In effect there is no such history" in modern terms of such an event.

Oh lets say Steve Keen.

Interest rates are at historic lows in the "developed" world. Places like china, japan have paid almost no interest for decades.

Cycles sure based on the grow for ever model on a finite planet.

Change, yes sure 2nd Great Depression coming up......

I think people are actually so scared of an interest rate rise they reply with the likes of your reply. Convince themselves it will never happen so they can get to sleep at night. One word of advice if you care to take it. Diversification. Also sell when markets are hot and everyones buying. Sit on your cash then buy some bargins when the time comes. Getting 'rich' in these markets is ALL about timing.

The thing is, where do you park your cash? An OBR event will see much of it lost.

It isnt about getting rich in the future, its about not losing as much as everyone else.

Key word: Diversify. Have 20-30% in physical gold/silver, 40-50% property as its a tangible asset. The remainder in stocks with a varied portfolio.. again diversification. All these people that have their only investments in say property are opening themselves up to a huge burn in the coming years. Could say the same about someone with 100% of investment in stocks. And when it comes to your mortgages never extend yourself more than say if rates were 2% higher and you could no longer pay... Just my 2 cents

Politicians forget that inequalities give rise to Social and racial tension with other problems. It is not just about economy but also giving rise to crime.

Current national government policies are focused to support and protect rich and speculators. Time for them to go to bring balance back in NZ society, IF............

Oh what utter Bollocks ............ you cannot blame the National government for peoples ill-discipline with money.

Of course this will exacerbate inequality, but buying home requires sacrifices .........Lots of them !

The reality is that about 35 years ago we went through hell to acquire our first property , we had to do something you kids have never heard of called ............SAVING........... (you can GOOGLE it to find out more)

That involves putting 10% or more of your wages in a fixed deposit EVERY payday , and not buying clothes you dont need , cars and gadgets you cant afford ,weekend trips on a Mastercard to Sydney to see a concert ( What a waste ) and coffees for $5 a pop

The youth of today want it to be served on a silver platter, they want it all and want it now , and for free or almost free .

35 years the the average house cost 3 times the average wage. Now the average house cost more than 10 times average wage. It's a lot more expensive to buy a house today than 30 years ago.

Please, please stop this nonsense about the youth of today want everything on a silver platter.

@ ak79 YOU ARE WRONG , the actual cost of servicing a mortgage in relation to incomes has come down dramatically in the past 9 years since the GFC .

At one stage our Mortgage rate was 25% ............. and the mortgage rate is now under 4% on fixed rates , so your argument has no bearing whatsoever .

And whats - more, it is actually easier to get a mortgage now than it was 35 years ago , with all those stupid Building Society rules and requirements

Boatman time does not stand still.

While you might be correct for this brief instant in time, when our mortgages were 25% our houses were cheaper with the likliehood that interest rates would eventualy drop...which they did.

Looking at it from todays rates and house prices .....the likely scenario aint lower interest rates and wage inflation....which leaves......what? Utter carnage is what i see.

Sure when the mortgage rate was 25% , houses were cheaper than now , but they were NOT affordable..

Boatman going by the big mac index data posted a few weeks back houses in inner Auckland suburbs are 2.5x more expensive today than 1995. Less affordable now. So now 2.5 lifetimes, barring illness/bad luck, to pay off a mortgage rather just one.

Yes the Mortgage rate was high, once, at the time of the sharemarket crash in the late 80's.

Yes the cost of a mortgage has come down - as far as interest is concerned.

Comparing now to the 80s in terms of advertising/internet/culture - just doesnt bare comparison. Watch a Rick James music video. Watch a Lady Gaga video (both can be found on the you tube on an internet near you). Simpler times - nowhere even close to the number of ways advertisers/websites work to empty your pockets these days.

here's how you are so very wrong

at the time the interest rates were over 25% (for our family) the house we had mortgaged was worth $170,000 on the market - now that very same house is worth 2.8 million

we had borrowed about $100,000

25% pa of that is $25,000 per year and that was difficult at the time but we were on a reasonable income so not too bad

now - for that property assuming you could raise 10% = $280,000 (questionable) you'd be paying 4% of 2,520,000 = $100,800

boy oh boy are you wrong

you are also so very wrong about how easy it is to get a mortgage now vs then

back then all you had to show was your income - that's it - and of course disclose any bankruptcies

even easier if you had other assets

now days you have to have an established credit rating AND assets AND a heft deposit AND absolute proof your income is enough though i have no doubt there are ways to game the system

that was not the only house we bought or sold over the last 30 years - and i can go through each one of them and each one would again prove you are full of it

So are you saying that over 30 years ago in the 1980's and 1990's your take home pay was over $25,000 per annum?

What are you , a Surgeon , a Barister , or a judge ?

So it's not the home that is more affordable, it is the larger debt. What a well thought out, rational and sustainable objective to achieve.

Not this tired old propaganda again. Spouted by those who benefit from the structural problems and want them to continue. What extra sacrifices would have enabled the Smug Boomer cohort to afford those houses by only saving a pathetic 10% had those houses cost 4 to 5 times what they actually did, and were subject to an untrammelled speculative bubble with price increases that were out-running any savings possible on stagnant or declining wages, and you were in bidding wars with the money launderers, speculators and tax evaders of every continent?

I dont want this to continue ........... nor would anyone else , but the reality is that the increase in all asset prices (including the NZX, property and the like ) is a direct and unintended consequence of QE .

The flip side is that interest rates are now low enough to compensate for the higher asset prices .

There is an inverse relationship between asset prices and the cost of borrowing

QE?

bull swill other than QE has made low interest rates available

Steve Keen tried to prove that was the case back in 2008-ish

he was WRONG and it cost him his reputation, his house and his job

the facts are simple - the raising house prices in Aus and NZ are exclusively the consequence of immigration

all else is details

Aorak1 , you are partly correct , however , you fail on you assertion that ALL house prices in NZ are rising .

They are not , you can still find a section on the South island in some remote town for a few weeks of an Auckland wage .

Auckland property rises are a perfect storm of 3 deadly elements ,, viz , Cheap QE money , rampant migration , and Auckland Council utter incompetence in facilitating the orderly growth of the City .

What do you mean by QE?

Quantitative Easing?

If so, what quantitative easing is(has) being(been) undertaken in NZ?

We have not had QE , but just where do you think our Banks are getting the money from to offer fixed mortgages at under 4%

Its QE money from the US , Japan , Hong Kong and the EU washing up here looking for a yiled higher than zero

Interesting story, but I wonder what you're basing your beliefs on? Have you got data, have you surveyed this and preceding generations to establish their savings habits? If so, it's strange your conclusions are different to those of the Treasury.

"A surprising feature of the data is that the saving rates of younger generations appear to be generally higher than those of the generations preceding them."

"Contrary to popular opinion, successive generations of households appear to be saving at significantly higher rates than earlier generations did at the same age."

http://www.treasury.govt.nz/publications/research-policy/staff-insights…

Maybe the young people you're associating with are particularly poor examples of what is on average a generation that is saving quite reasonably in the face of huge challenges.

@mfd , thanks for the link , which makes for interesting reading .

What is not considered is that the profile of young New Zealanders is vastly different to what it was in the 1930's , 40's 50 and 60's , and I reckon there is an easy explanation for the supposed high average saving rate of young New Zealanders today, in the sample

Its possibly about culture and ethnicity of our multi-cultural society .

The population was mostly white with a Maori minority in the past century .

We now, today, have an unbelievable number of Chinese , Filipino , Indian and other Asians living here .

Their culture is one of saving, while us Honky's spend like drunken sailors , you need to look at see SHELDON GARON a Princeton Uni Prof who wrote the book:-

"Beyond our means , why America spends while the World saves"

The average young white Mr John and Joan Kiwi from Henderson has no savings, rents a home , has a pile of debt , a low paid job unless he is a builder or tradie and little prospects .

So you're saying that the non-Caucasians are savers. OK. Are you trying to say the incidence of non-Caucasian first home buyers is higher than Caucasians? Is that based on evidence or top-of-mind?

Also, what happens to the wider economy if all the younger people stopped buying iPhones and lattes?

@ JC , I am not suggesting that White or Maori or Pasikika are all "non - savers" , or that houses are only being bought by what you call "non Caucasians" only

Quite simply , generally Asians place much more emphasis on saving than Caucasians , and then there are exceptions , where out of my 3 kids , One is an avid saver and nearly has the deposit for a house , one squanders money and has nothing , and the youngest could not care less .

The young Asian on the other hand is more likely to be living at home with his parents ( in a mortgage free home because they saved like hell and their parents helped them ) .

He would be saving his spare cash running an import or export enterprise on the side with family and is less likely to have two or more children with different parents , AND less likely to consume excessive amounts of alcohol or abuse substances. He is also unlikely to have a pay day loan or even a big credit card debt

At his wedding they would receive cash gifts in the RED ENVELOPES of up to $10,000 from family attending the wedding , so if you get 50 guest families , he could get the cash value of a modest home .

Then he is expected to save around 30% of his take home pay .

These things would then feed into the stats of savings by young New Zealanders

When it comes to buying property they are not scared to syndicate money between friends and family thus giving us the false perception of unassailable wealth

I know what you're saying, whether it's top of mind or not (even though I don't believe that the profiles of young Asians is partly defined by business ownership).

I asked if the incidence of non-Caucasians buying houses for the first time is higher than that of Caucasians.

Plausible, but still more anecdote than data. Even if it's true, it doesn't fit with your narrative that houses are affordable if you just save. Young people are saving and home ownership rates are still falling. Perhaps back in the day it was easy to spend like a drunken sailor and still buy, these days the odds are stacked against young people.

And how many years of saving did it take you to raise a deposit? And your savings were making 20% interest. Try saving a deposit for a house nowadays.

What would you rather have

- a house for $100,000 and see you interest payments fall from $25,000/year to $4,000/year now

- a house for $600,000 with interest payments at $24,000/year which can only go up over the 30 year term.

Also note that a $100,000 house bought in 1981 would cost on average $1.328m now based on average national house price inflation (more in Auckland)

@kiwimm .....It took about 4 years of saving , and we worked overseas for a while and brought back quite a lot , so we half a deposit and my Dad stood Gaurantee for 2 years for the other half ( he had funds in the Bulding Society that we could use as collateral ) .

As matter of interest , 60 years ago my Mom would collect pennies when my Dad was in the army , so when he got home she had 100 pounds saved for them towards buying a piece of land ..... so there you go it took 6 years to save the deposit 60 years ago.

Quite simply it has never been easy to own a home .

Just for the record. Not all 'Joan and John Kiwi' are doing what Boatman says. There are more than a few of us out there working more than one job, no debt, no lattes, no sky tv, just bare essentials. Savings in the bank but not able to get enough deposit for a modest house in the very very outer suburbs. Some of us are trying. Failing miserably, but still trying.

Please dont get me wrong , I do understand your predicament , its a terrible place to be seeing a rampant market that has priced itself out of control, and feeling like you can never get into home ownership, and that you will be like a fuedal serf paying the landlord forever .

This will change , because it has to , it simply cannot go on forever .

Its tragic , but I dont see my kids getting into home ownership anytime soon, I may be able to help , but not for a full deposit for each . We were a young 25 year old when we bought our first place, and it was not easy , but we did manage .

You just need some patience , and keep saving .

I also think there will be a massive adjustment to housing over time , and as a layperson I would not buy into this stupid Auckland market .

The migrants door is being closed, so they will not be pumping the market so much , Auckland City is sorting its mess out , and a slight increase in the Fed rate may see our OCR go up , and then the chickens will come home to roost for those speculators who have bet their Nanna's false teeth on the market

I understand and I know for the most part you can see that it's not all of us squandering. To be honest over the past few months I have wanted to give up and blow some of my money on doing something more exciting than working and packing my lunch for 5 days so I don't spend unnecessarily. It all feels a bit pointless, like what am I even doing this for? But, rather than being addicted to spending, I'm addicted to saving (Scottish background) so I just continue to do so even when it doesn't feel all that worth it. I hate paying someone else's mortgage but at least for the most part our landlord is very good to us and it's a long term lease, we've been there for a couple of years now and I heard from him this morning that we'll likely have it for another 4 years if we want/need it (which I'm sure we will). I can't imagine being shunted from place to place year after year, I've seen that happen too. It's all a bit bleak really. Keeping calm, carrying on!

Auckland is not sorting its mess out, Auckland has fixed its land supply at short supply levels for the next 25 years.

If you want to buy a home, take a jaunt over to Aussie to have a look at a concert and whilst you are there check out their property & job markets. Young people can buy a house, just not in Auckland, just not for the next 25 years.

I have to choke as I say it, but the NZ initiative might well be right in the limited thing that they say - which is that housing is driving inequality in New Zealand. (tho housing might not be the entire cause)

It 's clear to me that a young person of today cannot replicate what I could in my early twenties. Which was build an architectural house to live in, when we were both quite low income. For them, missing out on that path will damage their financial prospects lifelong.

NO, housing is not the driver

It is the "money" pouring into Auckland property

That is preceded by decisions on the part of the participants who decide that property is a worthwhile profitable investment, or, in many cases a bolthole

The sources of those funds and the participants are varied and subject to differing opinions

One could say that the housing tax status in jurisdictions such as Hong Kong, Singapore, Canada and Australia are drawing attention to New Zealand's tax-free status and that's where the money is flowing, and why it flows

What we are now seeing is a spillover into the surrounding regions

The spillover is a financial game

That spillover will cause inequality in those neighbouring regions

Housing is but the 3rd element in the decision table - not the first

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.