Housing rents are flat in Auckland, declining in Christchurch and rising in Wellington, according to Trade Me Property.

The national median asking rent for rental properties advertised on the website was $440 a week in September and the head of Trade Me Property Nigel Jeffries said it had been stuck in a rut since April, with the only exception being June when it declined to $430 a week.

"Last month median asking rents stubbornly refused to rise across New Zealand, including in the major regions," Jeffries said.

"Tenants will be pleased with the extended breather but landlords might be starting to scratch their heads."

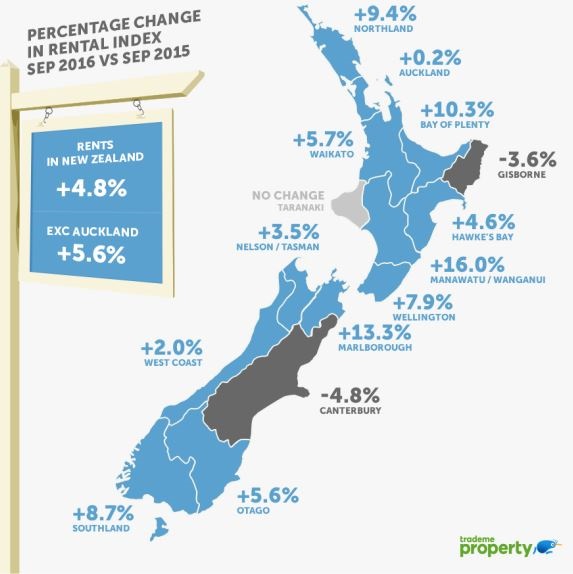

Over the last year the national median asking rent has risen by $20 a week, or 4.8%.

The situation is worse for landlords in Auckland, where the median advertised rent has increased by just $1 a week over the last 12 months and has levelled out at $500 a week.

In Christchurch it is definitely tenants that have the upper hand with median asking rents there unchanged at $400 a week for the last five months, which is down 7% compared to a year ago.

Of the major centres, Wellington is the exception, with median asking rents in the capital up 7.9% compared to a year ago.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

77 Comments

I notice rents are going down in Christchurch which will reflect the dropping property values. Anyone who has all their rentals in that city is certainly taking a risk especially when you factor in the chance of more major earthquakes.It pays to be diversified.

Please show me the stats that show Christchurch property values are declining?

Palmy population/property BOOMING

Is there a link between property values and rent? Currently tenuous at best.

Such low rent rises must mean a surplus of accomodation Shirley.

You can't speculate with rent you can by buying.

Rents show the real supply demand imbalance with the effect of speculators removed.

There is no direct correlation between property prices and rents. Rent increases correlate more with wage increases, inflation etc.

In other words, true market fundamentals.

Cue THE MAN

Maybe I should sign up to your newsletter, is it by any chance called 'Out of town expert who knows a lot about Christchurch Earthquakes and the effect on property & rental prices on a short and long term basis'

Trademe Property stats are a joke.. based on asking prices, not actual sale figures. From a property valuers point of view it sickens me that people are going to read stats from TradeMe and take them for fact.

You're telling me. Have a look at 3/6 Porters Ave, Eden Terrace . It was bought by a speculator in June for $520,000 who is now trying to sell it for $629,000,but when you look at past sales in Trademe this sale doesn't show. Great for the vendor eh?

On cue Gordon.

Not going to waste my time on here with tunnel visioned people not prepared to help themselves and are green with envy of anyone that has been successful,and wish to help,others.

Are rents dropping in CHch, some are.

Are our tenants staying on next year without dropping the rents? All but 2 are!

Are property prices dropping in ChCh definitely not from what i am seeing.

Have investors slowed down due to the LVRs, yes.

Are landlords better off than 2 years ago? Yes as interest rates are down by 25 percent or so.

Have property prices dropped like the sharemarket has? NO

End of story, can't be bothered going around in circles.

Good investing!

No envy here, simply trying to help with your own tunnel vision.

Property prices in Chch up ~4% in the last year, NZX50 up ~18% in the last year. Chch house prices up ~25% in the last 4 years (earliest QV data I could find), NZX50 up ~75%. S&P500 numbers are ~6% and ~50%.

Not saying you're not making money, it's just sensible to accept there are many valid investments and it's wise to not stick all your eggs in one basket.

MFD! Chch figures are totally skewed by all the "As is where is" properties that are still being sold innlarge numbers

S.

Beleive what you want doesn't affect me, if anything probably helps being able to buy more if at the right price so that we can rent out for good returns.

There are good investors and there are poor ones who don't give a rats and are prepared to prop up their rentals.

How could someone sleep at night after getting all that unearned income from shares? It doesn't seem right.

I sleep like a baby, if any of my investments are going to keep me awake it's the rental. Boiler went the other week, that's a few months rent gone, never forced to dip into my own pockets for my share holdings (I'm not against the odd voluntary capital raising though, always nice to feel like you're contributing to the economy)

don't ask the bank for money...they wont give it to you...

Unearned? Shareholders are putting their capital at risk.

Capital doesn't exist without people taking risk.

Businesses can't exist without capital,

Jobs can't exist without businesses.

MFD if you are wanting to compare property with NZX50, you would have to add rental yield to the capital gains in property. As NZX indices are gross indices (only major indices that are gross and not capital indices), so dividends get added to the capital value of the equities to derive an index value. Initiated due to long term poor performance of NZ equities. A way to pull the wool over the eyes of the uninformed.

You're quite right, that's why I added the S&P500 capital index returns on the end. I'm not going to do the work adding rental yield and subtracting costs. Out of interest, the NZX50 capital index returns are ~13% for the year and ~46% for four years.

so MFD - what you are saying is someone with 100K to invest four years ago - buys shares - now worth about $175K - gain of 75K - plus say dividends at 5% - call it another 25K max - so roughly a capital gain of 75K and income of 25K before tax ?

same 100K in the property market - leveraged at 20% as was common 4 years ago - so a 500K property - now up 25% - so 125K capital gain and 4 years rental yield at 5% after costs - 25K maybe -

very ballpark I know - but even using your figures - the power of leverage wins - hence why so many people are there - and risk wise -- well most housing downturns are under 10% drop in values - most market crashes are far higher!

and of course you are talking Christchurch - probably the worst major centre performing property market over four years - as opposed to Auckland, Tauranga, Hamilton - the latter two both with over 25% in the last 12 months alone!

Being just a bit disingenuous - while leverage works in a rising market - in a falling market it can be your worst nightmare. Your equity is eaten first - the debt still remains. You make the assumption that the drop will be only 10% - any proof of that or are just making up as you go along.

Kpnuts 10% thing is going by what has generally happened in NZ in the past like in 1997, 2008.

The past doesn't predict the future.

I think you are getting confused with straight out gambling like the roll of a dice. Future events are connected to past events. We can make fairly accurate assumptions about the future based on past events. That's why some of us are worth millions now.

For example: In the past grammar zone properties are in high demand three months before school starts. We conclude that this will be a good time of year to market such a property.

Rubbish - read "Fooled by randomness" by NNT

http://www.economist.com/blogs/freeexchange/2009/09/does_the_past_predi…

That I think is the problem - you need the future to the same as the past because if it is not ...... it becomes uncertain. People need certainty in an uncertain world.

If you are so certain why are you even arguing this point - it seems like it may be an inconvenient truth. There is something else going on here.

Have you ever been diagnosed as autistic?

Surely a store keeper stocks his shelves with things that have sold in the past. What has randomness got to do with it?

Have you ever been diagnosed as thick?

If I was autistic I don't think I would understand that you seem to have a very black and white view of the world.

Luck / randomness has far more to do with people's lives that they would like to believe - you have just been lucky (as an example - did you know exactly when you would meet your significant other...it is a purely random stochastic event) .

While a store keeper may stock things that sold in the past , tastes change and it is not always predictable. I've got some cassette tapes , they sold in the past so there must be a future.....

I wouldn't stock cassette tapes because they didn't sell in the past - get it?

I believe people make their own luck. Things are hardly ever certain but they are often probable.

Meeting my other half wasn't random, I went out hunting! Followed a trail. Hatched a plot.

Cassettes sold in the past - just that they won't sell today - I'm just using your logic - they sold in the past.... therefore they must sell in the future. The old cliché - you make your own luck - while true in part - you can increase your chances - luck still plays a role. While many things are probable it's improbable that are the problem - or to put it another way there is the known unknown and the unknown unknown. The known unknown are things that can be predicted to some extent. It's the unknown unknown's that are the spanner in the works (they are also known as Black Swans).

With meeting your other half who's now being obtuse.

You're too hung up on the possibility of a 'Black Swan". They are rare events that are not worth factoring in. This behavior will hold you back unnecessarily.

They are more common than you think and you seem to be all to dismissive of any possibility that they could occur in the Auckland housing market. Recently everyone was talking about supply and demand for houses , but what turned out to be the real kicker was the supply and demand for money / credit, and the next kicker will be the price of credit (interest rates).

While ignorance of Black Swans can be a blessing - you're ignorant of the risks that you are taking - it can also be a curse because you just don't see it coming....and are left wondering what the f**k happened on the other side ( did I mention luck has a great deal to do with this).

We know about so called "Black Swans" because they happened in the past right?

Yes - read the Wikipedia page.

"Rare and improbable events do occur much more than we dare to think.[8] Our thinking usually is limited in scope and we make assumptions based on what we see and know. Reality, however, is much more complicated and unpredictable than we think. Also, assumptions relevant to average situations are less relevant to irregular situations, especially when the "rules of the game" themselves change."

Investor friends in Christchurch say property prices are dropping off there. As workers leave less demand for accomodation. It is all about supply and demand as always. As interest rates increase prices will drop even faster in Christchurch. There is plenty of land for new houses to be built and second hand shitters will get less and less popular.

The median price that TradeMe quotes of $400 per week would only get a 2 bedroom unit from us.

Cheapest 3 bedroom is 420 per week in a lower socio area otherwise you are looking at about 470 per week for 3 bedrooms up to 600 for 4 bedrooms and have no problem filling as the homes are maintained.

Now for the hundred millionth time the problem is that the bank doesn't like to lend you money to buy shares. Why do the banks not share the same confidence in shares?

You could have a million dollars and buy shares and make a half million profit and people will be patting you on the back. You could be but a poor unwashed hoi polloi and borrow a milion dollars and make a half million profit and everyone is cursing you. It occurs to me that people don't like to see low class people making the old unearned income. The already rich they are okay with. Property speculators are just one step above beneficiaries in many commenters eyes I reckon.

You can re-mortgage your house and invest the money into shares. Interest on the loan is also tax deductible. So borrow the money at 2.7% after tax and invest in shares yielding 6%. Capital gain another bonus.

You can also borrow on the margin from a broker or invest in a leveraged ETF.

Has anyone tried this? If you have a million dollar house can you borrow a million dollars to buy shares like you can with property?

Yes, just keep the loan balance separate for tax reasons - can't be part of a general revolving credit loan. Remember that if you have a mortgage and investments then you are already borrowing to invest (without the tax saving)

I'm a little way away from my expertise and don't have time for extensive research right now, but I suspect part of the answer is to do with the bank's capital weightings, i.e. what lending ratios they are allowed depending on the risk weighting of their assets. I understand that money lent out with a property as security is treated very kindly, while perhaps money with shares as security is less useful.

This means the bank has to hold more capital (which has a cost) to lend out the same amount margin lending as it would for mortgage funding, making it more expensive to do so. Some banks are certainly happy to lend you money to buy shares (ASB will lend you up to 70% of your purchase price for certain stocks, more than most property investors can get with the new rules), but the interest rate will be higher than a mortgage, just as it would be for a small business loan.

I have certainly read that a tweaking of the capital weightings could be used to help encourage investment into productive assets, rather than flowing into housing.

Someone please correct me if I'm wrong.

Gordon, you always seem to have these friends all over the place.

Your only friends seem to be your shares.

I can tell,you now that prices are not dropping in Christchurch you are misinformed.

How can prices drop,when so many new houses at 700k plus keep getting sold?

Properties are getting multiple offers on them!

Second hand houses are actually becoming more and more popular with both first home buyers and investors as they are the only ones people can afford as the new ones are far dearer.

But then a friend will tell you different won't they?

Why are people in Canterbury saying there is no problem. They have 2213 properties advertised to let and every month the numbers go up. They also have 4773 listed to sell (on trademe alone).

This is a massive oversupply. You need to stop building new properties until the demand catches up.

As the rebuild gets closer to completion more and more people are leaving the city for nicer places to live and work. No more small earthquakes that constantly remind one that there could always be another big one.I rest my case. Keep taking those pills young man.

Gordon, harden up.

Earthquakes are common all around NZ.

The quakes have been bad for many people and unwanted and unfortunately we lost lives.

However, many people have,done extremely well since the earthquakes.

Where are all these better places that people are moving to Gordon?

Quite the opposite is that overseas people who came in for the rebuild have made Chch their home.

Yes there are a surplus of rentals inChch now solely due to too many new subdivisions.

Providing you maintain your rentals they are easy enough to rent and provide an impressive rental income unlike Auckland currently.

You can talk as much crap as you like but you haven't taken me up on my offer of a couple of weeks ago?

Are you up for,it?

Me talk crap! What a laugh. Christchurch is exceptional in terms of earthquakes. No other place like it in NZ. That's why people leave it every day.

Before the earthquakes there were apparently 1300 properties for rent in Christchurch and now we seem to have more. I wonder how many are accidental landlords...

Good to see rents flat in Auckland.

There isn't such a big housing shortage but don't tell anyone... Let's get a glut of housing built to make sure those rents stay flat or even go down for us renters for quite a while yet

Let's keep those media headlines going talking up high rates of immigration when a large chunk of those 'immigrants' are students most of whom will be here short term and in cbd apartments or renting with families

It seems not all landlords are equal

http://www.stuff.co.nz/business/85573055/changes-should-not-worry-good-…

http://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=117…

All very interesting.

The Christchurch property market is a real worry with oversupply in rentals, new builds and sections, not to mention many substandard repairs, builds and patchup jobs. A number of long term investors have taken the opportunity over the last couple of years to exit. I have property investments ...... no debt, good returns but took advantage of the market a couple of years ago and got out of Christchurch. Here's the thing, I have to say I have never had my share broker call me round to unblock the toilet, he has never damaged my property and sold drugs from my house, made me got to the tribunal to get paid (all this has happened). I get paid in 3 days everytime, never had a dividend payment late, in fact he has never complained about anything!! I get 5 - 6% and the capital growth over the last few years has been exceptional just a nice little bonus really

Seems a like a major pixxing contest between posters or simply stirring... which would not matter for the misinformation for other posters who may read it. Certainly some property prices and rentals across the Canterbury are falling while other areas are increasing and have had record prices this year. To treat Canterbury as one market is meaningless for anyone actually making decisions in the area. Prices way to aggregated.

Those talking about shares seem to forget same can be said for the NZX..all the oldies looking for yield who have suffered major capital losses in shares..such a common story... This comment section usually is insightful..certainly lost that aspect in this thread:-)

Agreed, the byline for this site is "Helping you make financial decisions" - I frequently choke on that with many of the comments.

Hey guys, re the Christchurch thing, enough of dancing on the graves of dead people. Such glee that the housing market is not gungho like Auckland and some regional places! Spare a thought for those of us suffering. To those who lost loved ones. And just on a material level - take myself, a high six-figure sum of equity locked up for over FIVE years as I struggled with insurers and their appointed builders to get my wrecked executive-level house replaced. And the new build is still not finished even now! Perhaps by Xmas - of course, all you doomsayers will be so happy that I won't have a pool of buyers to purchase it by then, nor a pool of tenants to afford it. As Mike Hoskings is wont to extoll, Happy Days.

The Chch housing market is still very strong despite many on here saying otherwise.

Auction today for an aged home in an average area sold under the hammer with many bidders.

Sold for $605,000 with a Rateable Value of $465,000

Sold just over 3 years ago for $450,500, so an increase of 154,500 or $1000 per week over the 3 years.

There is also a huge number of first home buyers attending open homes currently as well with multiple offers on properties.

Yes there possibly has been too many new homes being built which is of little use to first home buyers but this is definitely forcing the low to middle prices up as well.

The "As is where is" properties are also selling well but reduces the average or median prices.

The Trilogy International Ltd 52 week share price is a low of $1.65 and a high of $5.00 ( if you go back two years the share price was @ $0.60). So if someone bought 270,000 shares at the low ($437,400) and sold at the high ($1,350,000) their capital gain would be $912,600 and going out two years over $1.1million. Even at the current price the capital gain would be $594,000. Ain't it fun playing with numbers and being selective with what you choose to report.

Sure is.

Tomorrow it could be worth as much as Pumpkin Patch shares.

While true - the company is making a profit so very, very unlikely. Again you are being disingenuous - anything that proves you wrong in any way, you seem to instantly dismiss - I'm curious as to why. Speaking of Pumpkin Patch in early August the share price was @ 0.072cps it then jumped to 0.12cps - so lets do the maths - if you bought 6 million shares at 0.072cps ($432,000) and sold at the high 0.12cps ($720,000) the capital gain would have been $288,000 for little more than holding the stock for 2 weeks. Again playing with numbers and hindsight.

Not too sure what you mean by "proving me wrong"?

....your comments about the share market.

What coments exactly that I made did you prove me wrong???

You have been rubbishing investing in the share market - when returns can be as good if not better.

Do you invest in the share market BadRobot?

Yes I do.

What I have clearly said is that it is a gamble as you have no control over what a company's performance is!

If people are happy investing when you have no control then that is their perogative.

Shares are not guaranteed as we all know that shares can be toilet paper, and I have experienced that.

What I have also pointed out many times is that the so called housing market is just not Auckland and that you

Can get good rental returns plus capital gains away from Auckland.

I have also stated that first home buyers can afford homes away from Auckland for less than what they pay in rent.

What anyone takes from what I say is up to them and doesn't affect me whatsoever, but what I do say is absolute gospel, with no fiction at all!

So house prices have never crashed.....

No one has ever lost money on housing....

No one has ever lost money on housing in Auckland...if they have held on through the odd and generally quite short and mild downturn - fact!

Don't have any statistics on that - but I'll add - lost money yet..... the past doesn't predict the future....

Okay, the present has nothing to do with the past. What is happening right now will not affect the future. Got it.

Yes, totally agree with you Zach :-)

Yes you have total control over rental investments except for rising interest rates, rising rates bills insurance premiums maintence and repair costs, earthquakes and other major catastrophies, major world incidents such as September 11, disrespectful tenants not looking after your asset, P use and manufacture, supply and demand changes etc etc. Yes you are in total control. In fact you are in less control. The banks through their mortgagee rights have major control over your mortgaged rentals. The RB and the government have implemented controls of late that are affecting the ability to raise finance. More could follow at anytime. Yes you have total control.

The world property market is in bubble territory, what drives new bubbles like Auckland are cashed up buyers from overseas bubbles. In the provinces we are getting cashed up Aucklanders turning up and buliding two million dollar houses ( on a section they are probably paying 150 thousand for). But markets have to keep going up to sustain it.

It does not relate to incomes. so it must be driven by capital gain or lower rates or lending growth. The world has adopted the failed economic policies from Japan, and when all new bubbles are exhausted that's when there could be a problem.

Sydney and Melbourne will crash within the coming year due to a glut of apartments, the Chinese who lump Aus and Nz together will get the jitters and pull out of both markets, and both markets will crash

It seems to me that people continually over-estimate the risk in shares and under-estimate the risk in Residential property to the point where they see Res property as a sure thing!! It isn't, never has been and never will be especially with leveraging, most people I speak don't even consider leveraging works both ways,on the downside it is dangerous. Always have a plan B,

Govt policy towards residential property is signaled well in advance.

Share prices move at the whim of the incumbent company CEO.

I would say the incumbent board - but I don't think they have as much control as you think. The performance of a company is due to many factors that are outside the company's control - the economy in general, regulatory constraints, barriers to entry, competition (effective v's ineffective) etc.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.